stellalevi/iStock by way of Getty Photos

Shares of Kiniksa Prescription drugs, Ltd. (NASDAQ:KNSA) have been risky after the corporate offered one very optimistic update on Arcalyst and one other replace that I can solely say is blended at finest, however primarily unfavorable – the part 2 outcomes of KPL-404 in sufferers with rheumatoid arthritis (“RA”). My view on KPL-404 stays the identical – the corporate ought to rapidly put the RA trial behind it and give attention to different much less prevalent ailments the place this candidate could make a distinction. The main focus ought to rapidly flip again to the business uptake of Arcalyst, and it continues to impress, with the full-year web gross sales steerage vary of $360-380 million coming in effectively above the $351.5 million consensus.

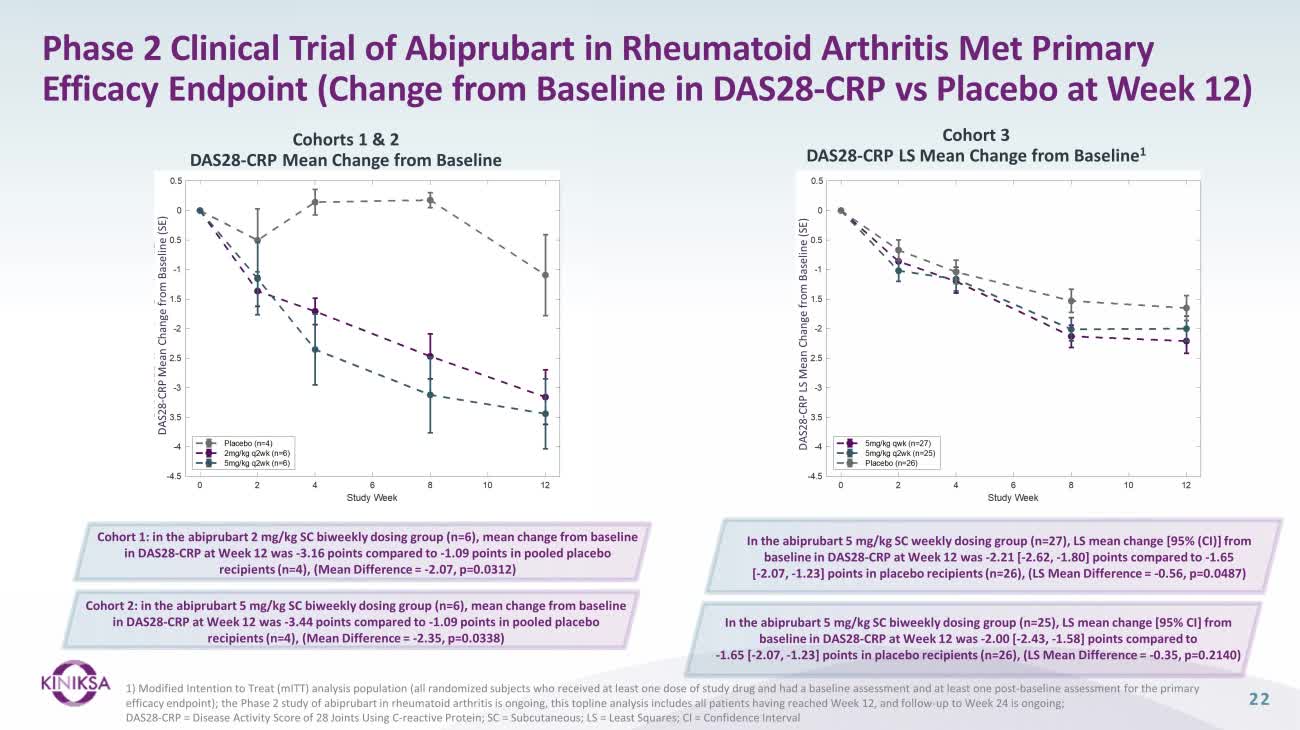

KPL-404 (abiprubart) delivers unimpressive RA knowledge

I mentioned final 12 months that this was not a catalyst price ready for and that rheumatoid arthritis shouldn’t be a sign of curiosity for this asset as a result of there are extra fascinating and fewer prevalent ailments to go after and since the information from rivals was not notably spectacular both. It turned out KPL-404 was no completely different and it too has didn’t impress within the RA inhabitants.

The 2 preliminary cohorts of KPL-404 regarded good in comparison with placebo however such is the character of very small cohorts as it could present false indicators. The bigger third cohort offered a greater glimpse of how efficient KPL-404 was on the first efficacy endpoint of DAS28-CRP – it was barely numerically higher than placebo, and the outcomes didn’t attain statistical significance. The imply change from baseline was in keeping with knowledge Horizon, now a part of Amgen (AMGN), reported with dazodalibep.

Kiniksa Prescription drugs investor presentation

Granted, there are some optimistic biomarker indicators even within the third cohort and security regarded clear, however total, KPL-404 doesn’t appear to be a promising candidate for the remedy of rheumatoid arthritis.

This isn’t the tip of RA trial updates. There may be nonetheless cohort 4 the place KPL-404 is dosed each 4 weeks and this cohort ought to inform the dosing schedule for future trials.

My view stays the identical – the corporate ought to rapidly transfer on and begin trials in indications the place there are higher efficacy indicators and the place KPL-404 might be priced as a uncommon illness drug.

I used to be not assigning worth to KPL-404 in RA, or different indications, so, the unimpressive outcomes make no distinction to my expectations.

Arcalyst continues to carry out effectively; the 2024 steerage vary seems to be lifelike

I used to be initially impressed by the full-year 2024 Arcalyst income steerage because it was effectively above the Avenue consensus, however I do marvel if it was offered to restrict the harm from the unimpressive KPL-404 knowledge and whether or not we’ll see the corporate beat and lift all through 2024. Even so, Arcalyst’s trajectory seems to be robust, and it could not be a catastrophe even when the web gross sales find yourself on the low finish of the $360-380 million steerage vary.

Administration does have a blended steerage file. Firstly of 2022, they guided for full-year Arcalyst web gross sales of $115-130 million and stored it unchanged all year long, and delivered $122.5 million, which was proper on the mid-point of the preliminary and solely steerage vary.

Administration acquired higher at managing expectations in 2023 when the preliminary steerage vary was $190-205 million and so they raised it to $200-215 million after the primary quarter report, and to $220-230 million after the second quarter report. The vary was unchanged after the third quarter report, however administration did word web gross sales have been trending towards the excessive finish of the vary. They managed to exceed the excessive finish by reporting $233.1 million in web gross sales in 2023.

Based mostly on the execution in 2023, the steerage for 2024 doesn’t look very demanding. I might anticipate Arcalyst web gross sales to be nearer to the excessive finish of the $360-380 million vary. The query is whether or not there may be upside from that steerage vary as analysts will alter expectations accordingly, and the upside could also be restricted if execution is in line and if there aren’t any will increase within the full-year steerage vary.

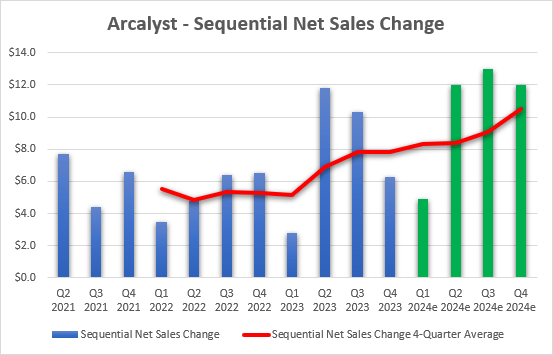

The chart under reveals a tough estimate of what sequential web gross sales must appear to be for Arcalyst to hit the excessive finish of the steerage vary and the trailing 4-quarter common.

Kiniksa Prescription drugs earnings stories, creator’s estimates

Q1 is the worst quarter of the 12 months as a result of seasonal components, and we see usually robust sequential progress for the rest of the 12 months. The anticipated progress to get to $380 million in 2024 seems to be considerably demanding however in the end achievable by means of elevated adoption, improved productiveness of the prevailing gross sales pressure, and extra gross sales pressure enlargement.

Kiniksa introduced plans to additional develop the gross sales pressure from 50 reps on the finish of 2023 to 85 reps, which the corporate believes shall be ample to cowl 85% of the recurrent pericarditis inhabitants in the USA, up from 70% with 50 reps, and to achieve 11,000 prime and mid-tier prescribers in comparison with 7,000 beforehand.

A step-up in sequential gross sales from the late 2022 gross sales pressure enlargement might be seen within the chart I shared earlier, and the inflection level was virtually quick in Q2 2023 and after a seasonally gradual Q1. We should always see an analogous and even higher impression in absolute numbers because the variety of new reps this 12 months is 35 versus 20 final 12 months.

There may be nonetheless loads of room for progress, as Arcalyst has simply scratched the floor within the U.S. recurrent pericarditis market. The corporate estimates that market penetration on the finish of 2023 was round 9%.

I’ve stored my long-term income estimate vary unchanged since launch at $600-700 million, because it was monitoring usually between the decrease finish of the vary and the mid-point, however the change within the trajectory in 2023, the anticipated impact of the moreover expanded gross sales pressure, and what I see as not less than achievable steerage have improved the outlook. I’m tightening up the vary to $650-700 million, which will increase the decrease finish of the valuation vary from $25 to $27 and the brand new vary is $27-30 per share.

Conclusion

The outcomes from the part 2 trial of KPL-404 are underwhelming however in the end not related and I anticipate Kiniksa Prescription drugs, Ltd. to rapidly change its focus to much less prevalent ailments comparable to Sjogren’s syndrome. The improved outlook for Arcalyst is what issues within the close to and medium time period.