Grant Faint/Second by way of Getty Photos

KKR Actual Property Finance (NYSE:KREF) has been pressured to chop its quarterly dividend. The business actual property lender declared a $0.25 per share quarterly distribution, a 42% dip sequentially, and $1 per share annualized for a roughly 10% ahead dividend yield. Once I last covered the mortgage REIT, I highlighted inadequate dividend protection of simply 58% towards its prior third-quarter distributable earnings. This prior setup embedded e book worth erosion, so a dividend reduce was not solely essential however prudent, and comes towards renewed regional banking angst on issues over CRE publicity that is harking back to the identical interval a yr in the past when a number of banks folded.

KKR Actual Property Finance Fiscal 2023 Fourth Quarter Supplemental

What’s subsequent for KREF after the reduce? Probably extra uncertainty on the again of its workplace property publicity as this asset class turns into the villain for a REIT inventory sentiment seeking to the Fed to outline its near-term future. The commons fell 14% intraday on the mREIT’s fourth-quarter earnings launch that confirmed income dipped by 10% year-over-year to $50.67 million. KREF additionally realized a $58.7 million loss, round $0.85 per share, on a defaulted senior workplace mortgage. Adverse sentiment has additionally fed by means of to the preferreds (NYSE:KREF.PR.A) regardless of the dividend reduce being factor from an asset protection perspective. Each securities stand to presumably see extra market nervousness on continued market angst round CRE and expectations of extra workplace mortgage defaults.

Credit score High quality, Originations, And E-book Worth

KKR Actual Property Finance Fiscal 2023 Fourth Quarter Supplemental

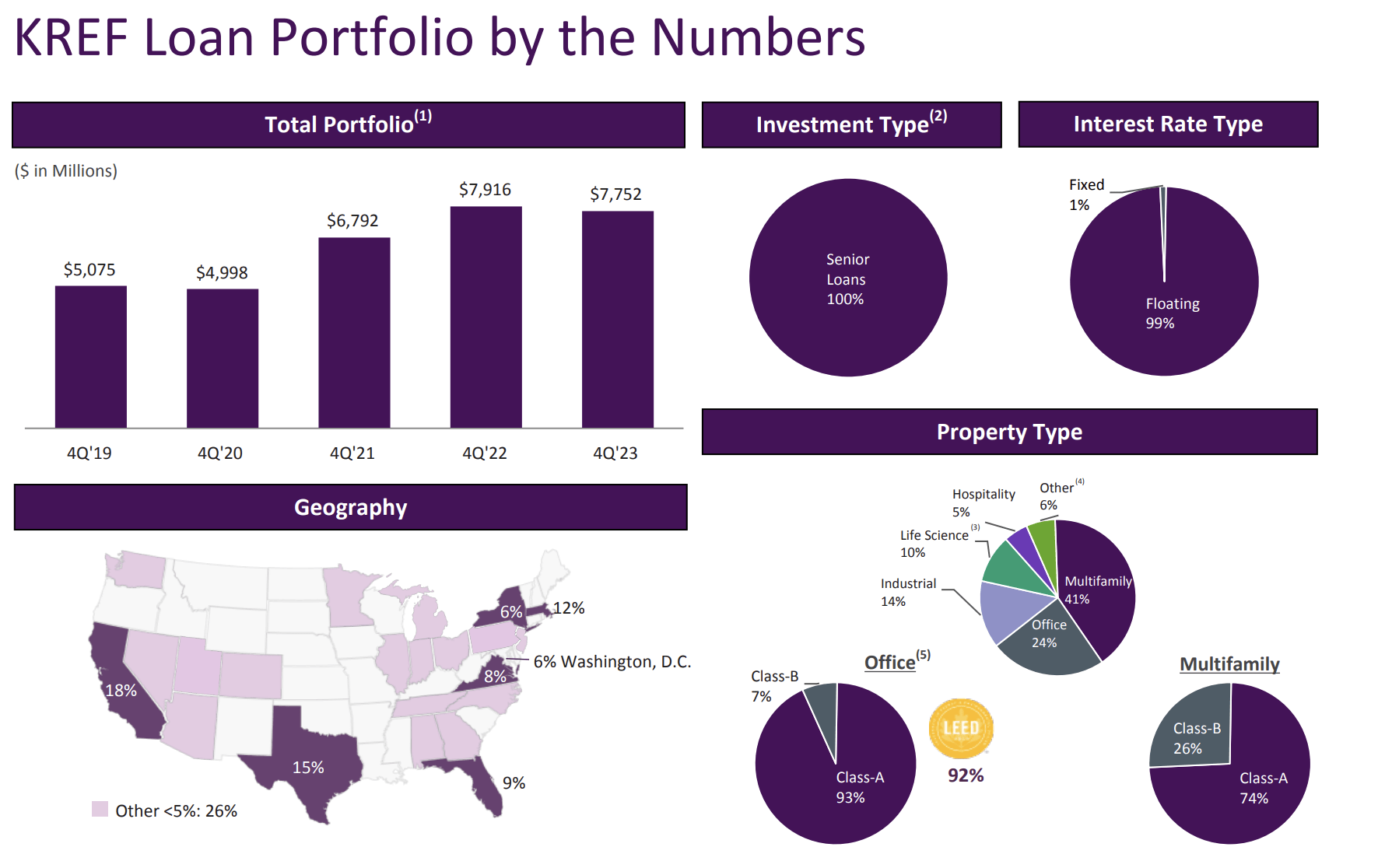

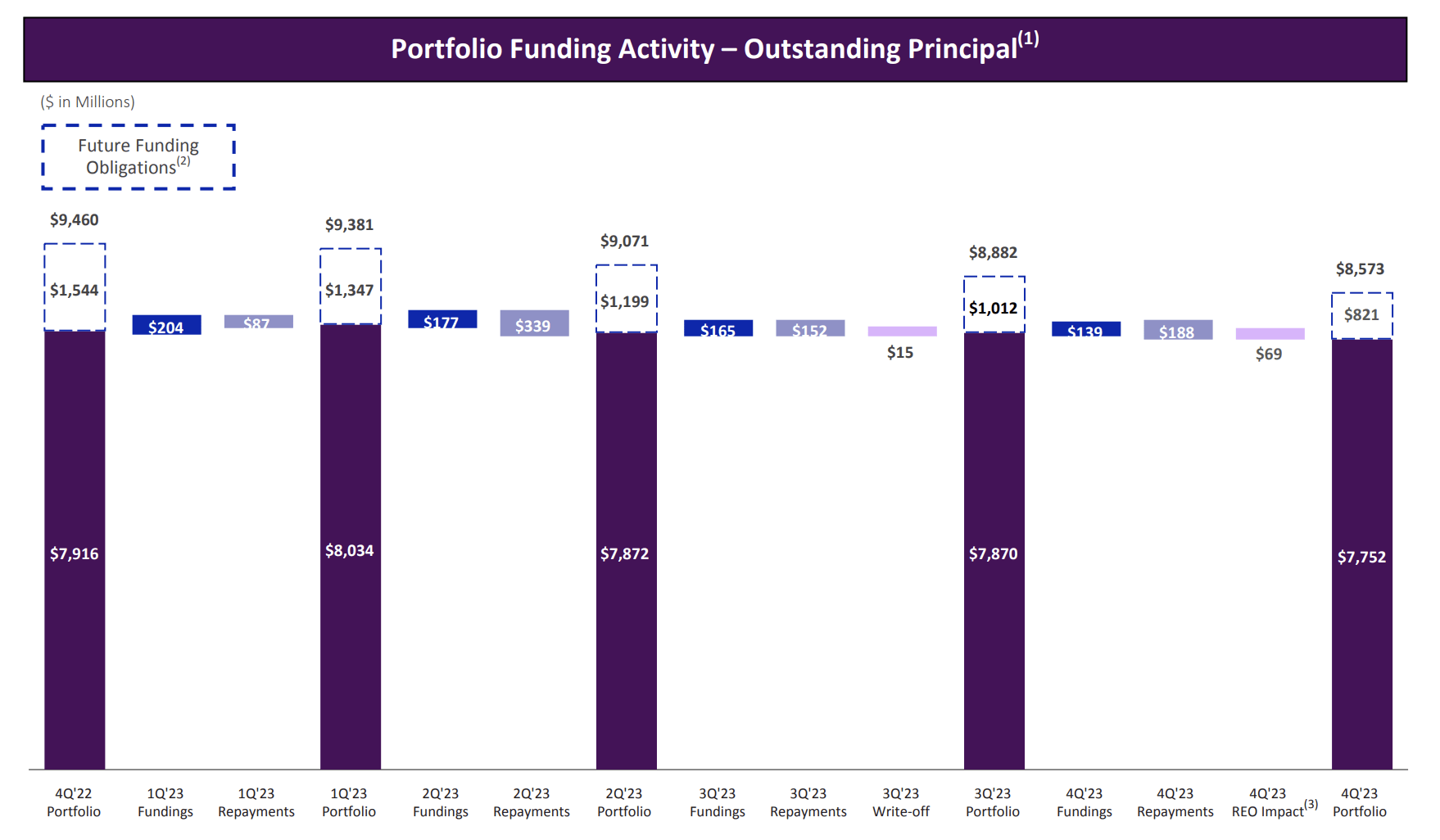

KREF’s mortgage portfolio on the finish of the fourth quarter was $7.75 billion, dipping by $118 million sequentially on the again of repayments operating forward of originations and the write-off related to the Philadelphia senior workplace mortgage. The mREIT’s portfolio has been retrenching sequentially for the reason that begin of its fiscal 2023 with KREF taking a prudent stance by permitting repayments to run near or forward of originations towards a disruptive macro backdrop. The mREIT’s e book worth on the finish of the fourth quarter was $1.08 billion, round $15.52 per share, and down 77 cents sequentially from $16.29 per share on the finish of the third quarter. This was additionally down from $18 per share initially of fiscal 2023. Therefore, it is now essential that KREF take steps to cut back e book worth erosion, and the dividend reduce ought to contribute in direction of this goal.

KKR Actual Property Finance Fiscal 2023 Fourth Quarter Supplemental

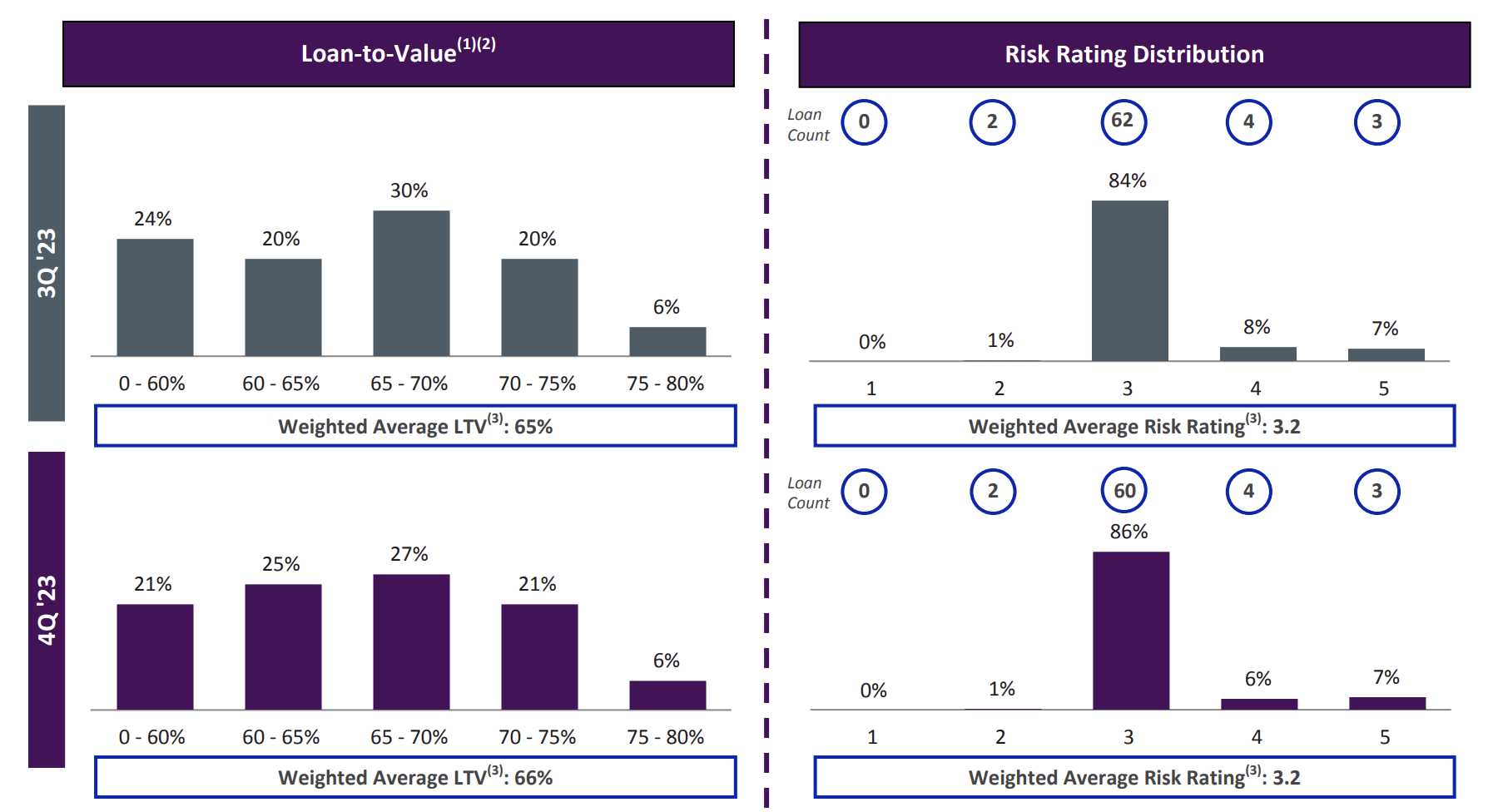

KREF’s workplace property publicity is the place the market angst lies, nevertheless, this types 23% of its mortgage portfolio. Not insignificant, but it surely’s not at a stage that may demand a ceaselessly discounting of commons, presently buying and selling 36% under e book worth per share. The market is forward-looking and pricing in a continued dip of e book worth, however this will probably be true till it is not with the rightsized dividend set to avoid wasting 18 cents per share of e book worth sequentially, round $0.72 per share annualized. Round 84% of KREF’s loans are nonetheless with a threat ranking of three, a small enchancment from 83% within the third quarter. All different threat ranking distributions broadly stayed the identical other than loans rated 4 which dipped by 200 foundation factors sequentially.

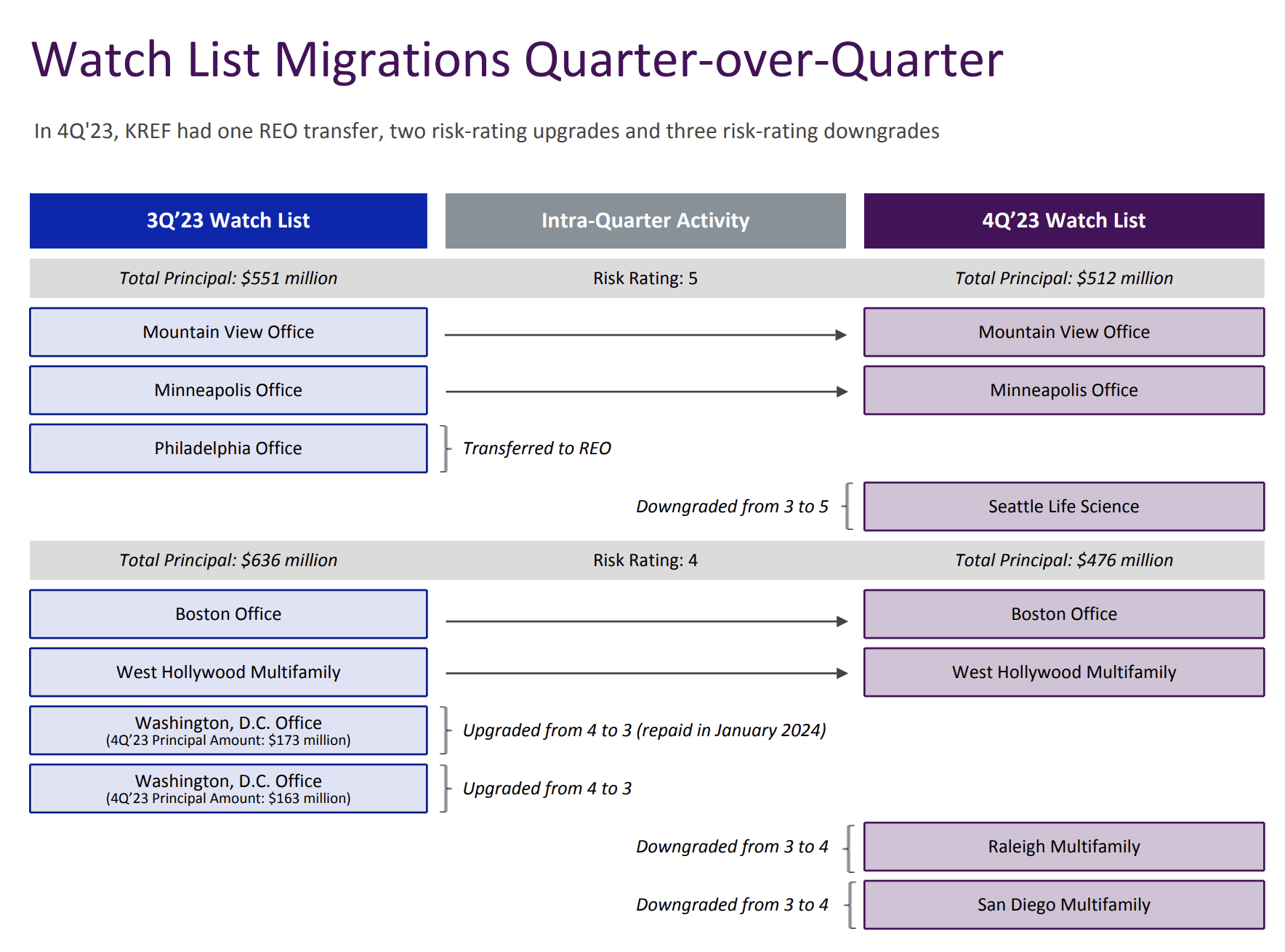

KKR Actual Property Finance Fiscal 2023 Fourth Quarter Supplemental

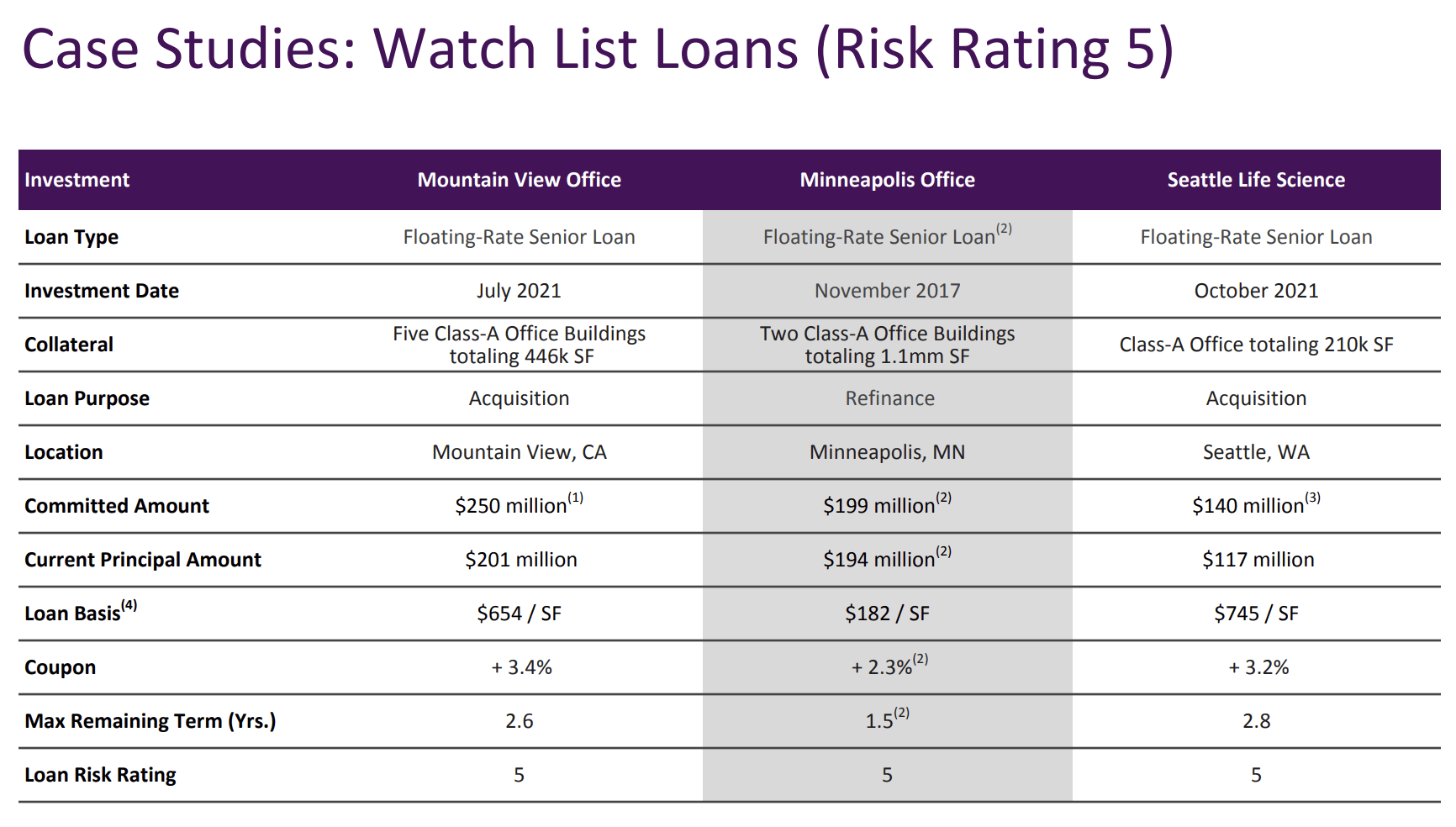

There are roughly three loans with a threat ranking of 5 with a default on the Philly workplace loans seeing KREF take possession of the collateral. Nonetheless, a Seattle Life Science workplace constructing was downgraded from 3 to five. Critically, while the default on the Philly workplace loans which nonetheless had $149.8 million of excellent principal left just isn’t nice, it is 1.9% of the mREIT’s mortgage portfolio with the market response seemingly outsized however admittedly forward-looking. There’s one other $512 million in excellent principal throughout watch record loans with a 5 threat ranking, which had a mean max remaining time period of two.3 years.

KKR Actual Property Finance Fiscal 2023 Fourth Quarter Supplemental

Liquidity And The Fed

Critically, KREF and REITs will stay within the doldrums absent any rate of interest cuts from the Fed. It is an odd sensation to see the market making new highs virtually every day as revenue performs get pushed to new 52-week lows, however greater for longer will see sentiment saved low and the present low cost to e book worth will stay sticky.

KKR Actual Property Finance Fiscal 2023 Fourth Quarter Supplemental

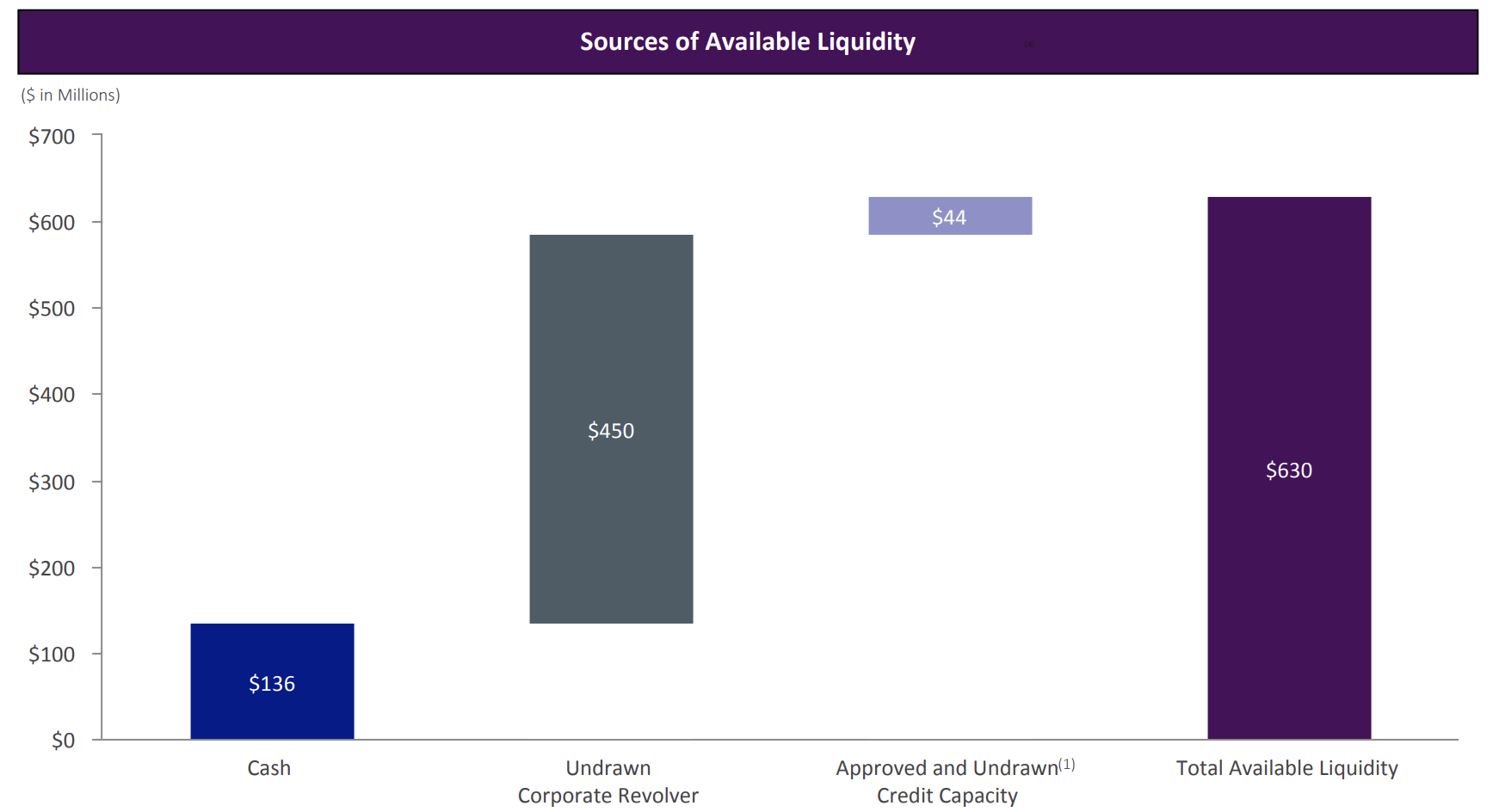

KREF reported a web loss attributable to frequent stockholders of $18.7 million throughout the fourth quarter, round $0.27 per share. This drove damaging distributable earnings of $26 million, round $0.37 per share. The mREIT has sufficient liquidity to take care of its present $17 million per quarter commons distribution with distributable earnings previous to the realized loss from the Philly workplace mortgage of $0.47 per share proving sufficient protection for the rightsized dividend. I do not personal a place within the commons although, however 2024 might open up some alternatives if KREF’s e book worth is stabilized.