Jasmin Merdan/Second by way of Getty Photos

Krispy Kreme, Inc. (NASDAQ:DNUT) not too long ago reported important internationalization efforts in 7 new nations, severance bills, and store closure bills, which can deliver future adjusted EBITDA development. As well as, new merchandise in new markets like Insomnia Cookies might deliver important internet gross sales acceleration within the coming years. There are apparent dangers from failed internet leverage makes an attempt, inflation points, and provide chains. Nevertheless, DNUT might definitely commerce a bit extra expensively. I imagine that it’s a purchase.

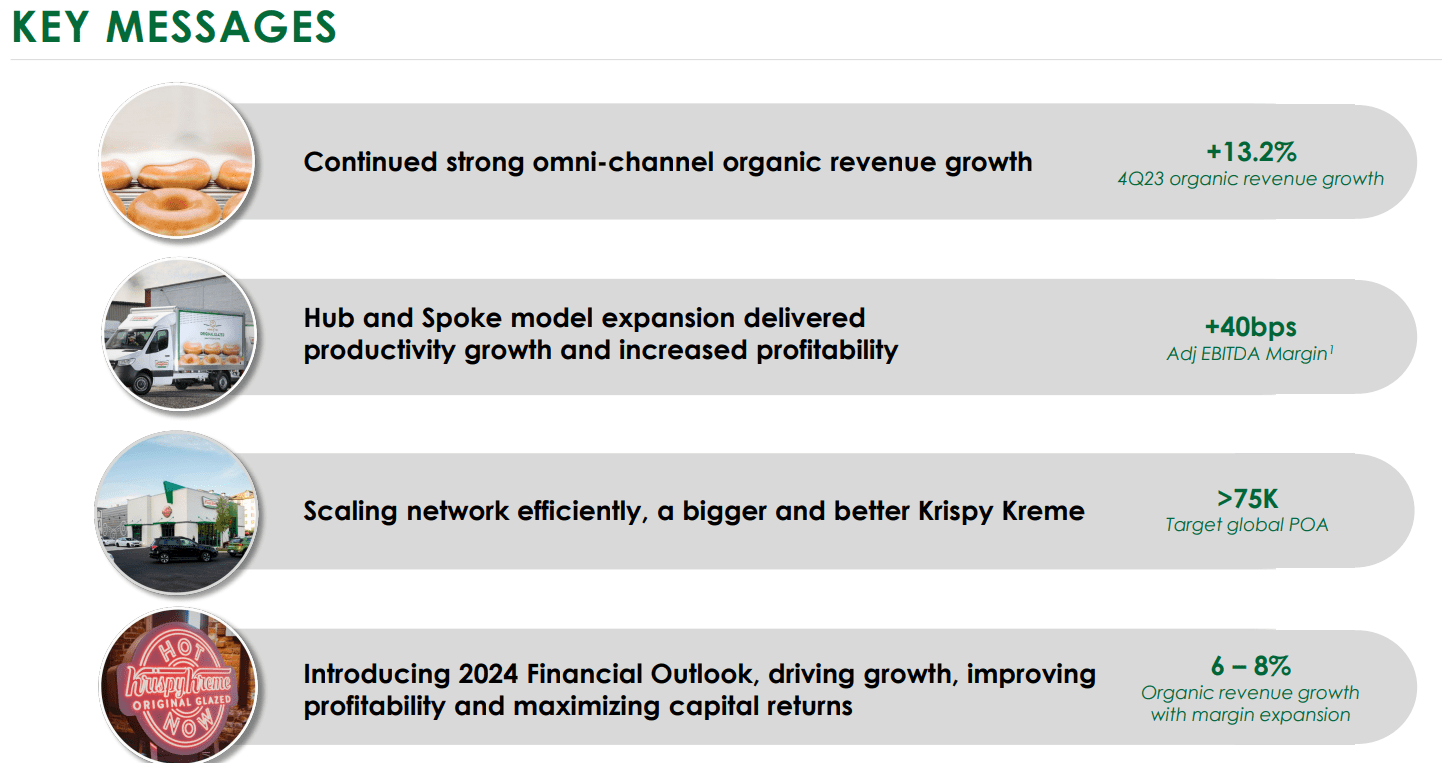

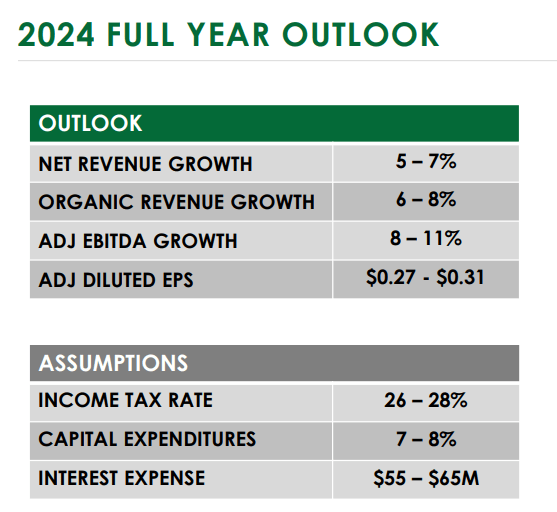

Useful 2024 Steerage Not too long ago Reported

Krispy Kreme presents itself as one of the vital beloved and well-known candy deal with manufacturers on the planet. Working in additional than 35 nations, the corporate provides contemporary doughnuts with know-how accrued since 1937.

With that fast tackle the enterprise mannequin, I imagine that it’s value noting that Krispy continues to ship double-digit quarterly income development due to its omnichannel technique. As well as, for my part, Krispy Kreme seems to be a must-follow inventory due to its 2024 steering, which incorporates 6-8% internet gross sales development, and scaling community effectivity promised within the final quarterly report.

Presentation To Buyers

Different figures included within the final steering embody adjusted EBITDA development of near 8-11% and adjusted EPS of near $0.27 and $0.31. Check out the desk beneath, and observe that the corporate additionally reported expectations for curiosity bills and capital bills. With such detailed expectations, I feel that many monetary analysts could resolve to run DCF fashions.

Presentation To Buyers

Stability Sheet: Giant Quantity Of Goodwill

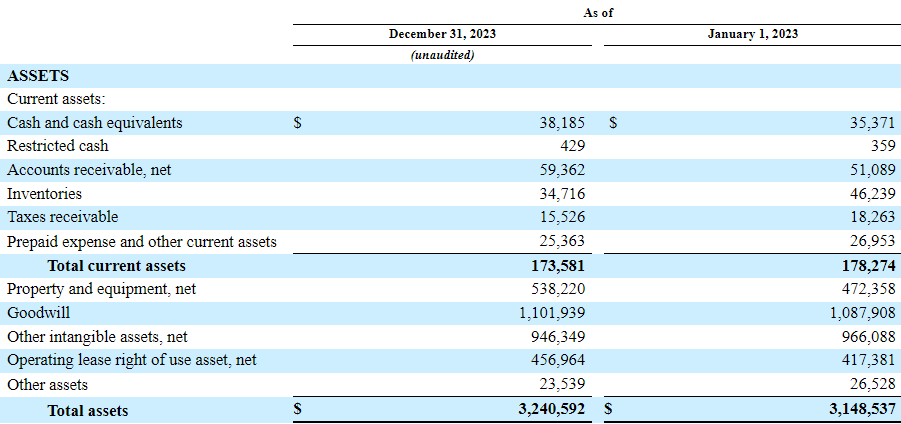

Probably the most exceptional concerning the firm’s steadiness sheet is the big quantity of goodwill and intangible belongings reported. A couple of-third of the whole variety of belongings is represented by goodwill and intangible belongings. These belongings are primarily financed with debt, lease liabilities, and accounts payables.

Particularly, the corporate famous accounts receivable value $59 million, inventories of about $34 million, taxes receivable near $15 million, and complete present belongings value $173 million. The ratio of present belongings/present liabilities is decrease than 1x, which most buyers on the market could not admire. Provided that the corporate has been working since 1937, I imagine that bankers would provide financing if obligatory. The worth of the model might not be acknowledged within the steadiness sheet.

Extra specifically, the corporate famous property and tools value $538 million, goodwill of about $1101 million, different intangible belongings near $946 million, and total assets of $3.240 billion.

10-Q

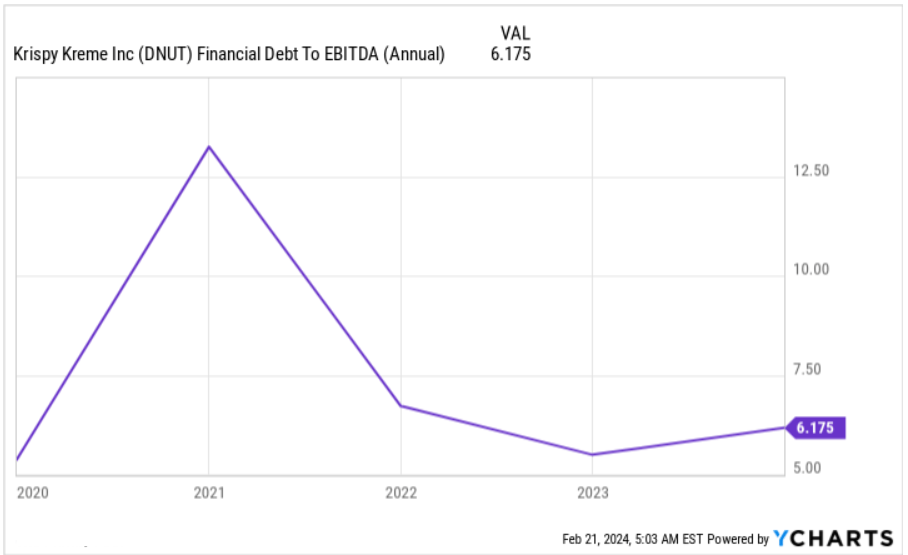

I do imagine that the whole quantity of debt does seem important. With that, it’s value noting that the corporate’s internet debt/EBITDA ratio stood at near 12x in 2021. The corporate managed to cut back its ratio to 6x. For my part, an additional lower within the complete quantity of debt could result in higher EV/EBITDA valuations.

YCharts

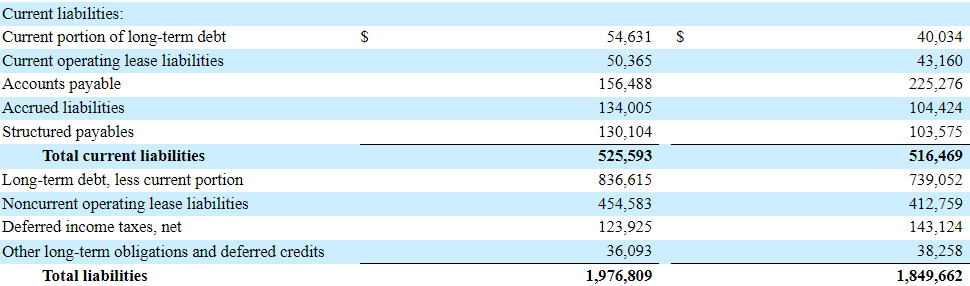

Concerning the listing of liabilities, the corporate famous long-term debt of near $54 million, accounts payable value $156 million, accrued liabilities value $134 million, and complete present liabilities of about $525 million. Lastly, with a long-term debt of $836 million, complete liabilities stood at $1.976 billion.

10-Q

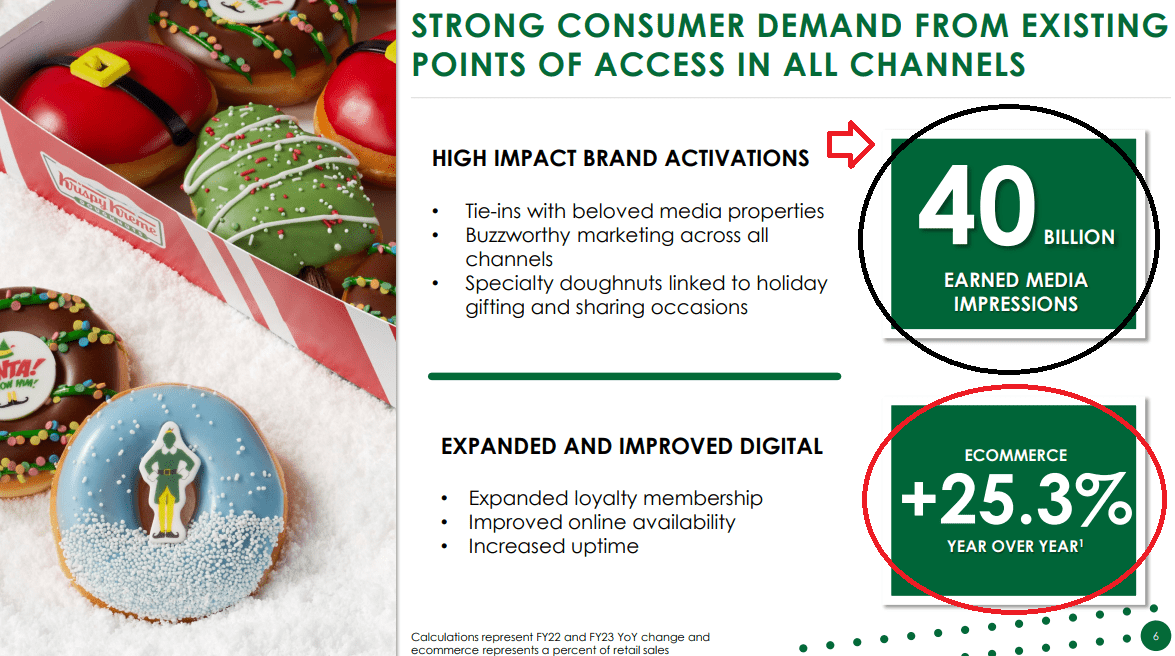

Ecommerce Efforts, Loyalty Memberships, And Media Impressions Are Web Gross sales Catalysts

The latest info delivered within the final quarter about ecommerce outcomes, which included development of 25.3% y/y, and loyalty membership growth could also be internet gross sales drivers sooner or later. As well as, it’s value noting that the corporate obtained near 40 billion media impressions, which represents important efforts when it comes to advertising and marketing. With many extra prospects having a look on the firm’s doughnuts, I’d count on important internet gross sales development within the close to future.

Presentation To Buyers

On this regard, the corporate famous that natural income grew near 13% pushed by ecommerce efforts, model activations, and seasonal choices.

Complete firm natural income grew 13.2%, pushed by excessive impression international model activations and seasonal choices, elevated Factors of Entry and premiumization efforts. Ecommerce as a p.c of retail gross sales elevated 130 foundation factors to 19.3% of gross sales. Supply: Quarterly Report

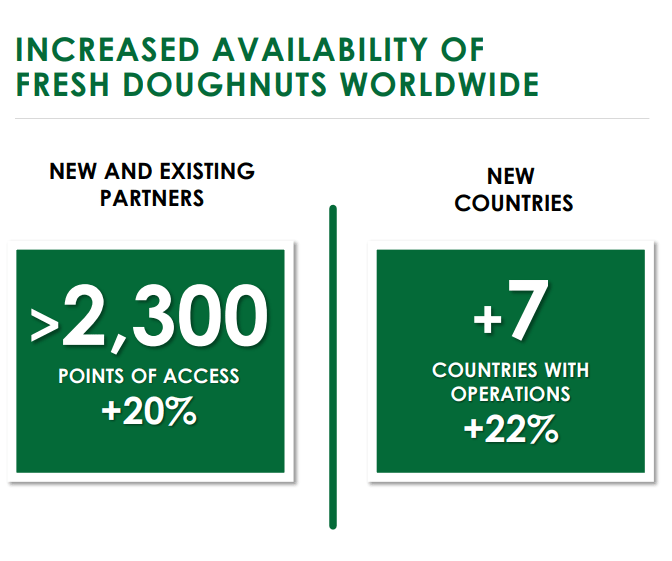

Internationalization Will Most Possible Be A Catalyst

With know-how accrued from working in america for an extended time period, I imagine that the corporate might promote efficiently abroad. Within the final quarterly presentation, the corporate famous new operations in 7 new nations and 20% extra factors of entry with new present companions.

Presentation To Buyers

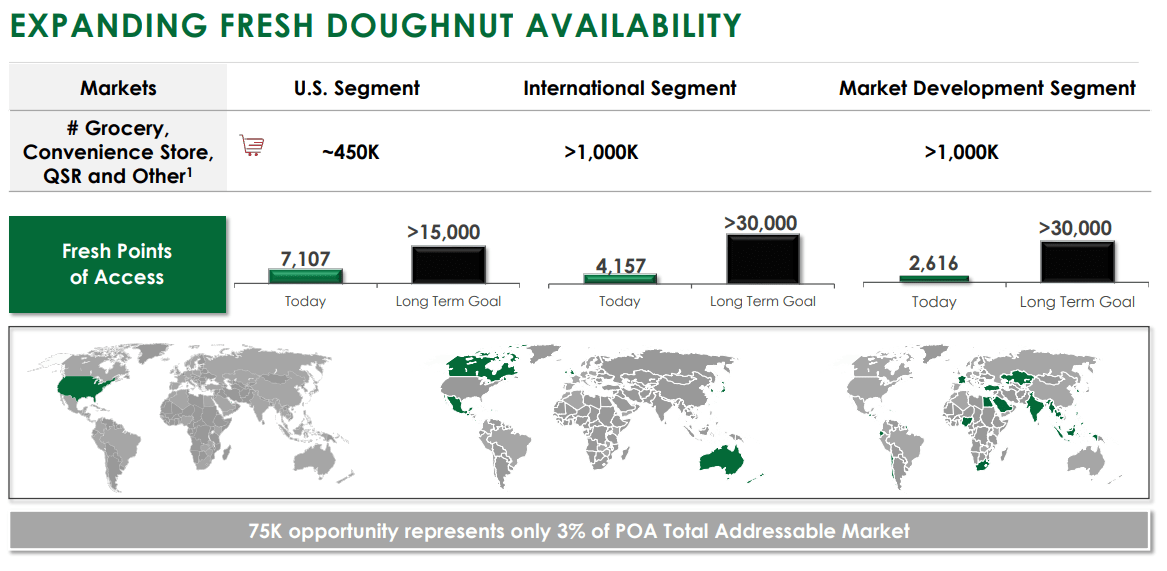

Based on figures reported by Krispy Kreme, the U.S. section represents near 450k factors of entry in groceries and comfort shops. The worldwide section contains greater than 1 million factors of entry. Therefore, I imagine that the potential alternative for Krispy Kreme is critical.

Presentation To Buyers

Within the final quarterly report, the corporate famous spectacular ends in the worldwide markets, together with income development of 9% pushed by power in Australia. Given these outcomes, I imagine that internationalization methods are at the moment working fairly nicely.

Within the Worldwide section, internet income grew $14.1 million, or 15.2%. Worldwide natural income grew 9.0%, pushed by POA development of 686, or almost 20%, and continued premiumization efforts. 10-Q

Worldwide Adjusted EBITDA grew 7.8% to $22.1 million with adjusted EBITDA margin declining roughly 140 foundation factors, as power in Australia was offset by decrease quantity within the U.Ok. resulting in deleveraging all through the assertion of operations. 10-Q

New Merchandise In New Markets May Additionally Deliver EPS Development

I additionally count on important internet gross sales development due to new merchandise already examined in america, which the corporate makes out there abroad. On this regard, it’s value noting the supply of doughnuts and Insomnia Cookies globally, which have a helpful impact on the final quarterly EPS.

Adjusted Diluted EPS declined $0.02 to $0.09 from $0.11 in the identical quarter final 12 months, as a result of elevated depreciation and amortization, as we expanded availability of our doughnuts and Insomnia Cookies globally. 10-Q

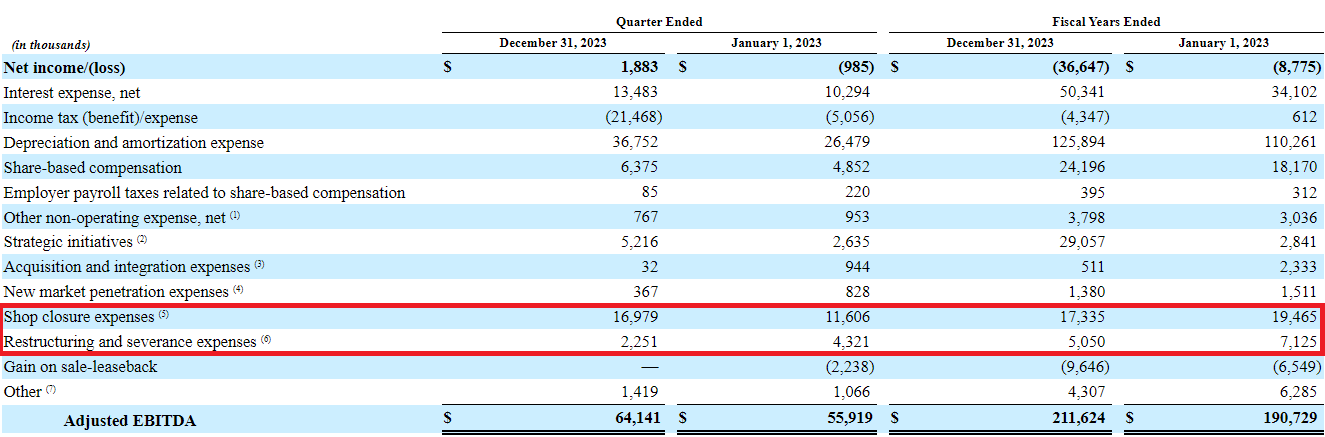

Severance Bills, Store Closure Bills, And Strategic Initiatives

Within the final quarter and in 2023, administration reported store closures, restructuring, and severance bills, which can deliver monetary flexibility within the coming years. Given the growth into new territories, it seems clear that DNUT is able to shut some places, that don’t carry out, and open new shops.

10-Q

Extra specifically, within the final 10-Q, the corporate famous prices related to international transformation and U.S. initiatives, such because the closure of the Branded Candy Treats enterprise, amongst different prices. The next strains provide additional info on this regard.

Fiscal 2023 consists primarily of prices related to international transformation and U.S. initiatives equivalent to the choice to exit the Branded Candy Treats enterprise, together with property, plant and tools impairments, stock write-offs, worker severance, and different associated prices (roughly $17.9 million of the whole). 10-Q

Finest-Case State of affairs

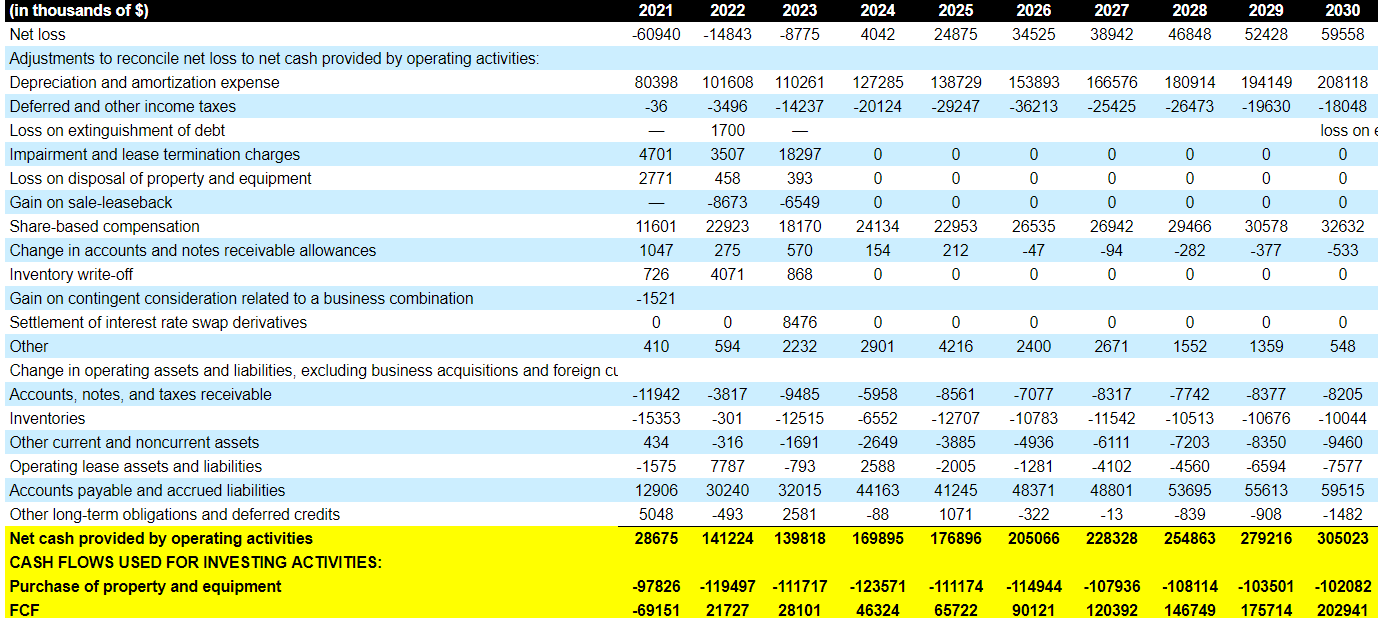

With earlier helpful assumptions, I designed my best-case situation. First, I assumed a 2030 internet earnings of $59 million, with depreciation and amortization bills near $208 million, however with out loss on extinguishment of debt, impairment, and lease termination costs, losses on disposal of property and tools, or acquire on sale-leaseback. I assumed that these had been extraordinary occasions.

As well as, I included share-based compensation of near $32 million, with adjustments in accounts and notes receivable allowances value -$1 million, notes, and taxes receivable of -$9 million, and adjustments in inventories of -$11 million.

Moreover, if we additionally assume adjustments in accounts payable and accrued liabilities of about $59 million, 2030 internet money offered by working actions can be near $305 million. Lastly, with 2030 buy of property and tools of about -$103 million, 2030 FCF can be $202 million.

Writer’s Expectations

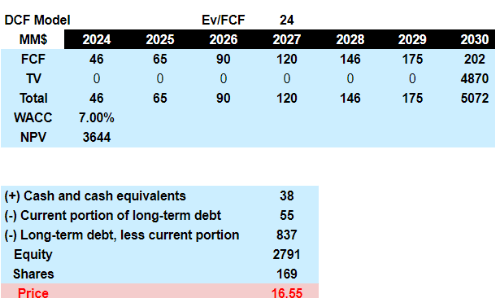

Given the current valuation of DNUT, I assumed an EV/FCF of 24x, which I assumed was conservative. If we additionally use a WACC of seven.05%, the implied enterprise worth can be near $3.6 billion. Including money and subtracting debt, the implied inventory worth can be $16.55 per share.

Writer’s Expectations

Dangers Relevant To My Worst-Case State of affairs

Beneath my worst-case situation, the money circulation assertion might undergo from sure dangers, which embody the next. First, I imagine that credit score situations could change within the close to future. Because of this, the corporate could not have the ability to finance its steadiness sheet like previously. Curiosity bills can also enhance, which can push the EPS figures down. On this regard, the corporate talked about the next within the final annual report.

Now we have important indebtedness, which might adversely have an effect on us, together with reducing our enterprise flexibility and rising our curiosity expense. Our indebtedness might additionally scale back funds out there for working capital, capital expenditures, acquisitions, the reimbursement or refinancing of our indebtedness because it turns into due, and different common company functions. It might additionally create aggressive disadvantages for us relative to different corporations with decrease debt ranges. If our monetary efficiency doesn’t meet present expectations, our skill to service our indebtedness could also be adversely impacted. Supply: 10-K

Within the final quarterly report, the corporate famous that it expects a lower in internet leverage in 2024. I imagine that it’s fairly helpful. Nevertheless, sudden enhance in internet leverage might result in pessimistic sentiment concerning the efficiency of the corporate. Because of this, decrease demand for the inventory could push the inventory worth down.

The Firm continues to count on to cut back its internet leverage in 2024, as we make progress in the direction of our 2026 aim of roughly 2.0x to 2.5x internet leverage. 10-Q

Current capex within the development of Hub and Spoke mannequin, amongst different IT capabilities, could result in extreme expectations about capability growth and internet gross sales development. If capital expenditures do not result in will increase in income development and EBITDA margin growth, I’d count on some pessimism from market members.

In the course of the fourth quarter 2023, the Firm invested $32.8 million in capital expenditures, pushed primarily by investments within the development of our Hub and Spoke mannequin alongside selective transforming exercise and investments in info know-how capabilities. 10-Q

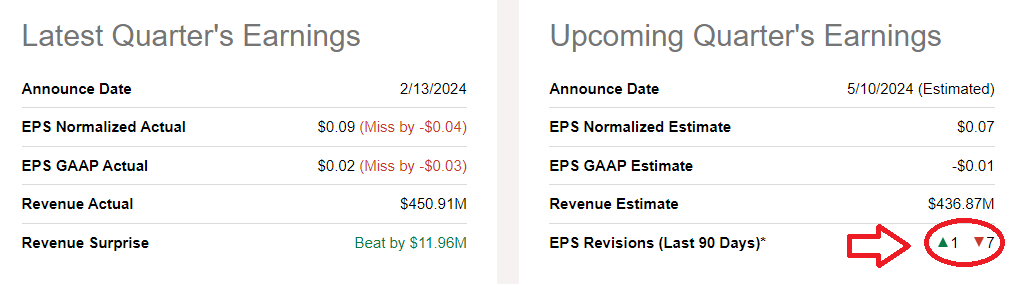

I’d even be involved concerning the latest EPS, which was decrease than anticipated, near $0.02, and the EPS revisions by 7 completely different analysts. If funding analysts out, there don’t provide helpful expectations for the long run, demand for the inventory might additionally decline.

Looking for Alpha

Lastly, adjustments within the labor situations, inflation, provide chain, or distribution issues can also come up within the coming years. Because of this, the corporate might undergo from declines within the FCF margin, and the implied truthful valuation might decline.

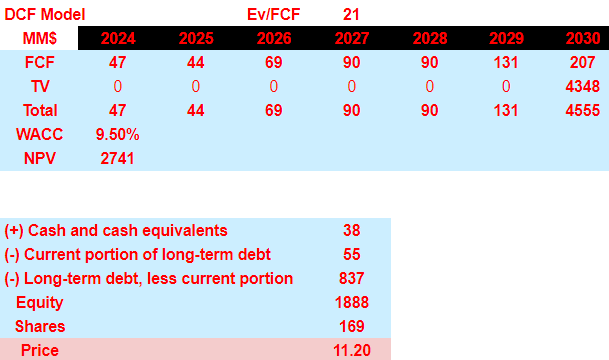

Worst-Case State of affairs

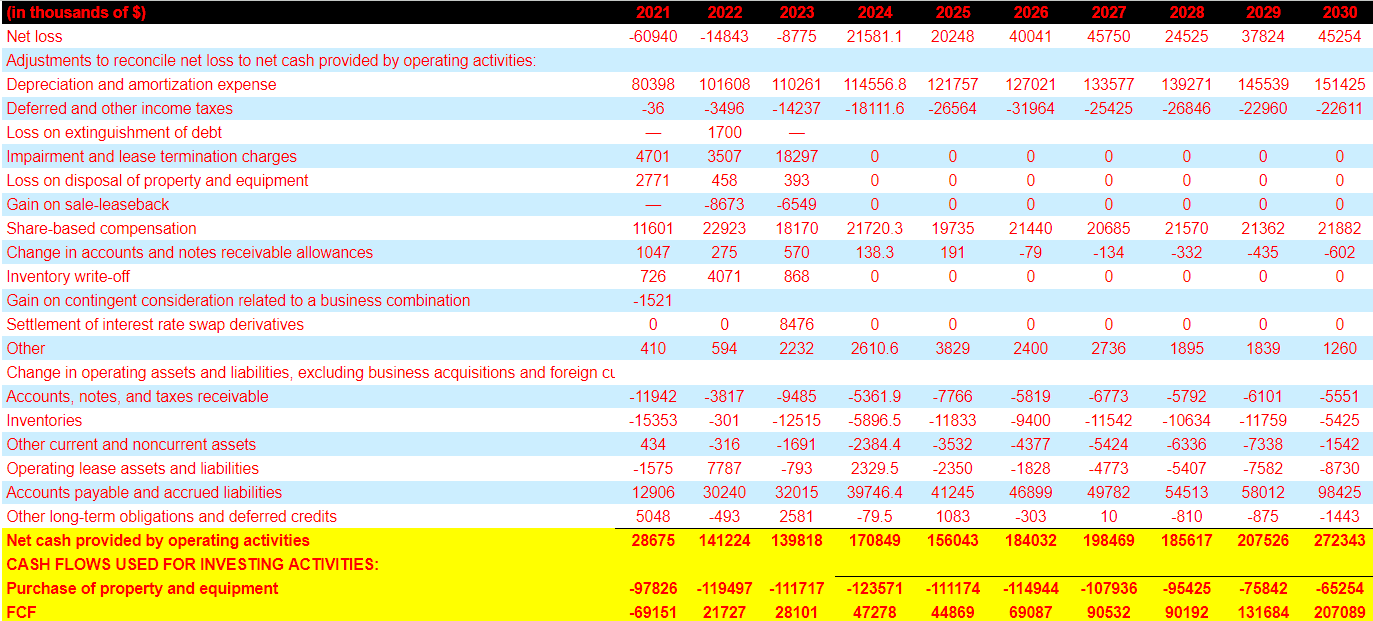

Beneath my worst-case situation, I included many of the dangers beforehand famous and obtained the next money circulation assertion projections. First, 2030 internet earnings would stand at near $45 million, with 2030 depreciation and amortization expense of about $151 million and share-based compensation of about $21 million.

As well as, with adjustments in accounts and notes receivable allowances of about -$1 million, adjustments in accounts, notes, and taxes receivable of -$6 million, and adjustments in inventories of -$6 million, I additionally included adjustments in accounts payable and accrued liabilities of $98 million.

As well as, with adjustments in different long-term obligations and deferred credit of -$2 million, I obtained 2030 internet money offered by working actions of near $272 million. Lastly, with buy of property and tools near -$66 million, 2030 FCF can be $207 million.

Writer’s Expectations

If we additionally assume an exit a number of of 21x FCF and WACC of 9.49%, the implied enterprise worth can be near $2.741 billion. Including money in hand of $38 million and subtracting debt, the implied fairness valuation would stand at $1.8 billion. Lastly, the truthful worth wouldn’t be removed from $11.2 per share.

Writer’s Expectations

Rivals

The corporate seems to compete with a big variety of home and worldwide opponents, which embody retailers of doughnuts and different treats, espresso outlets, and different bakery ideas. Retailers with candy treats and ice cream outlets had been additionally highlighted as opponents within the final annual report. With that concerning the listing of opponents, I’m not actually involved about competitors as a result of the corporate has operated for a lot of a long time and is aware of its purchasers nicely. On this regard, administration offered the next clarification.

We view our model engagement, total client expertise and the individuality of our Unique Glazed doughnut as vital components that distinguish our model from opponents, each within the doughnut and broader indulgence classes. Supply: 10-Ok

Conclusion

Krispy Kreme not too long ago promised a big lower in internet leverage and introduced important internationalization efforts in 7 new nations and a big worldwide market alternative. These efforts together with latest severance bills and store closure bills might deliver important FCF margin enhancements and monetary flexibility. If we additionally take into consideration the helpful steering of Adjusted EBITDA development near 8-11%, I imagine that the corporate seems to be like a purchase. There are clear dangers coming from the whole quantity of debt, inflation points, or provide chain points. Nevertheless, for my part, Krispy Kreme may very well be a bit costlier.