TOLGA AKMEN/AFP through Getty Pictures![]()

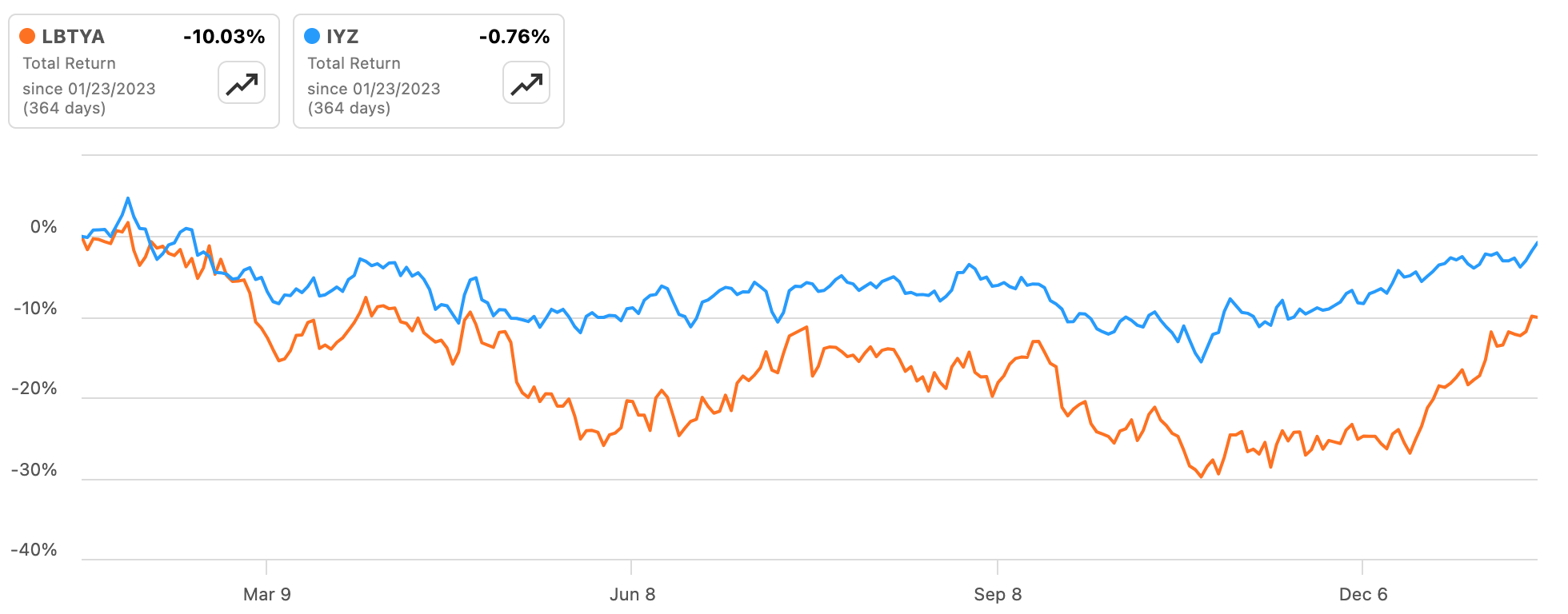

Regardless of rebounding sharply over the previous few weeks, shares of Liberty World (NASDAQ:LBTYA) (NASDAQ:LBTYK) (NASDAQ:LBTYB) have had a fairly lackluster 12 months, shedding round 10% of their worth and underperforming U.S. telecoms (IYZ) by a good margin in that point.

Supply: Searching for Alpha

Liberty’s European telecoms companies have confronted a troublesome working surroundings not too long ago, with earnings coming underneath strain from value inflation and declining fastened subscribers. Liberty can also be a troublesome inventory to get a deal with on given its complicated construction, one other issue which may be weighing on the shares. Nonetheless, with the present sub-$20 inventory value solely implying a modest valuation for the core telecoms companies, these shares seem like an excellent cut price for worth buyers, and I open on the inventory with a Robust Purchase score.

Liberty World Overview

Liberty is a holding firm that owns numerous telecoms companies in choose European international locations. The corporate’s wholly-owned subsidiaries embody Dawn (Switzerland), Telenet (Belgium), and Virgin Media Eire. As well as, the corporate has 50:50 joint ventures within the Netherlands (VodafoneZiggo) and the UK (Virgin Media O2, hereafter VMO2) which aren’t consolidated by Liberty.

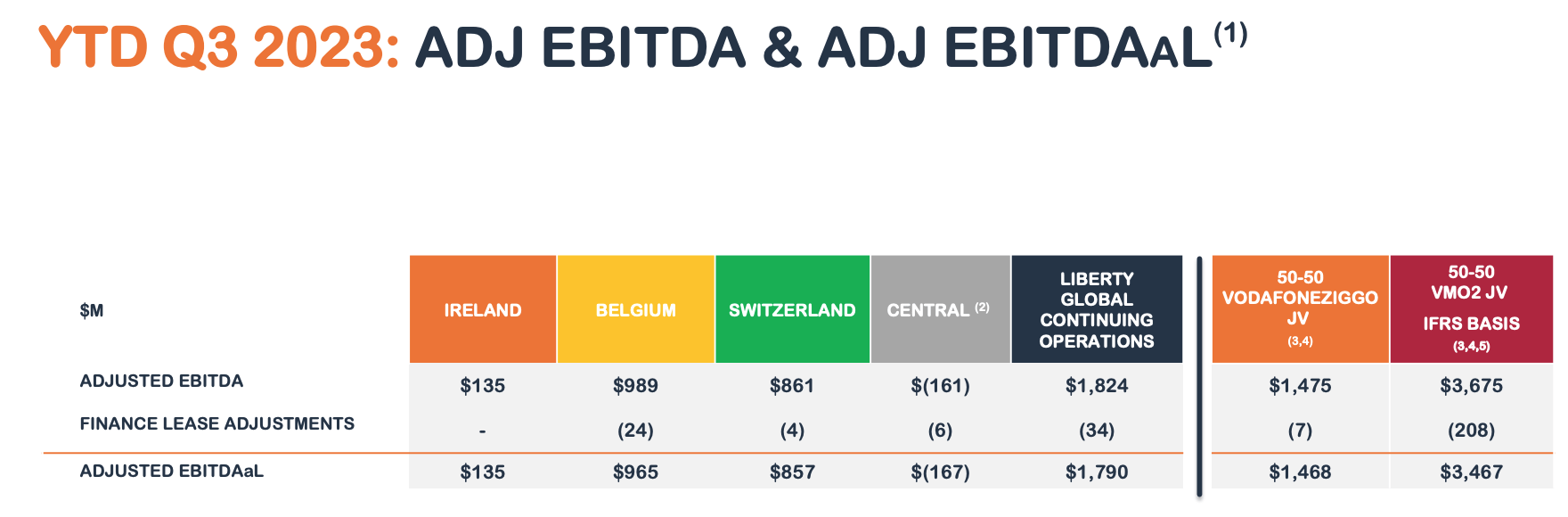

Supply: Liberty World Q3 2023 Outcomes Presentation

Broadly talking, I like Liberty’s companies for 2 causes. Firstly, Liberty sometimes operates cable belongings within the markets it’s current in, with these networks requiring much less onerous CapEx necessities to improve versus the incumbent operators. As an illustration, within the U.Ok., VMO2’s principal competitor BT (OTCPK:BTGOF) has been spending closely on upgrading its copper community to full fiber, leading to a pointy improve in CapEx in recent times.

Secondly, though telecoms is an inherently aggressive trade, Liberty’s markets are pretty steady, with the agency not current within the extra aggressive European markets equivalent to Italy and Spain. The corporate’s broadband market shares land within the 50-60% space on the excessive finish (e.g. Telenet, which does not function on the nationwide stage however is concentrated within the Flanders area) to round 20% (e.g. VMO2). Through M&A, Liberty has additionally been bolstering its conventional cable companies with cellular companies, leading to higher convergence throughout its companies. Amongst different advantages, cross-selling a number of companies sometimes reduces buyer churn, which in flip improves buyer acquisition prices as it’s cheaper to retain an current buyer than purchase a brand new one.

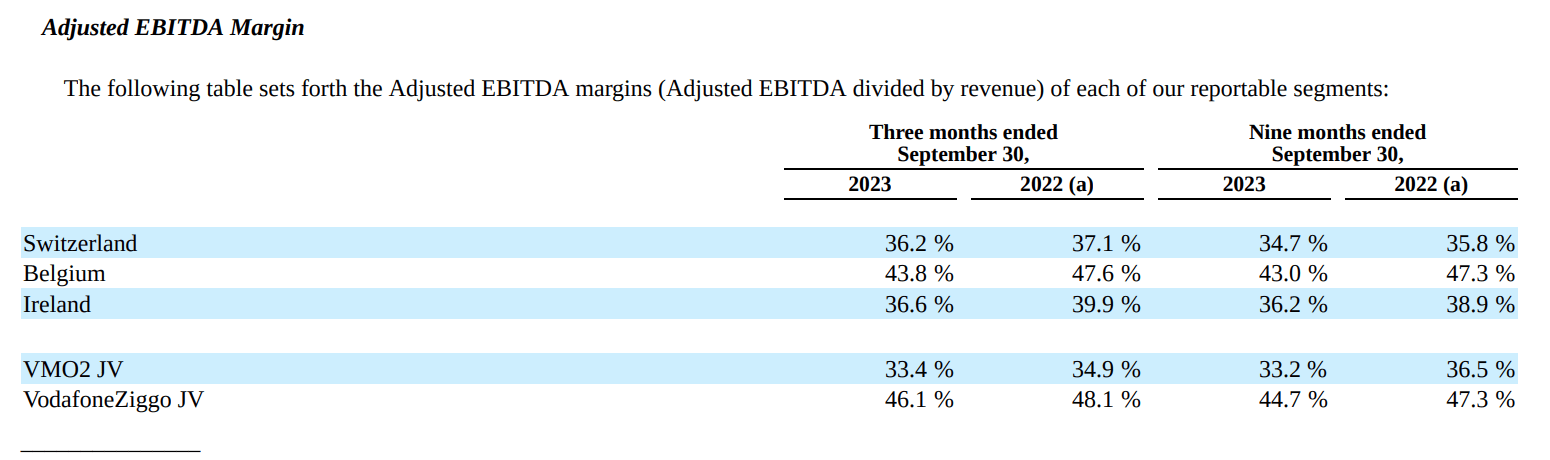

Inflation Weighing On EBITDA

Liberty has been working in a difficult macro surroundings not too long ago, with inflation and declining fixed-line prospects placing downward strain on EBITDA. Liberty misplaced virtually 50,000 video subscribers throughout its consolidated companies in the latest quarter we’ve got figures for (Q3 2023), accelerating from 40,000 losses in Q2. Fastened phone and video are battling secular headwinds, however web subscriber progress has additionally been damaging not too long ago, with the agency shedding circa 25,000 subs throughout its consolidated companies in Q3 plus one other 34,000 at VodafoneZiggo, offset to a big diploma by virtually 41,000 web provides at VMO2.

Worth hikes are offsetting the above to a level. The consolidated companies posted $2.25 billion in 2023 fastened income by Q3, equal to a 1.3% year-on-year decline on an natural foundation. Cell has additionally helped up comparatively effectively compared, with optimistic subscriber progress throughout each the consolidated companies and JVs. This led to flat residential cellular income over the primary three quarters of final yr within the consolidated companies, with VMO2 and VodafoneZiggo posting 2.9% progress and three.7% progress, respectively, over the identical interval.

EBITDA has seen additional headwinds from value inflation, weighing on margins.

Supply: Liberty World Q3 2023 10-Q

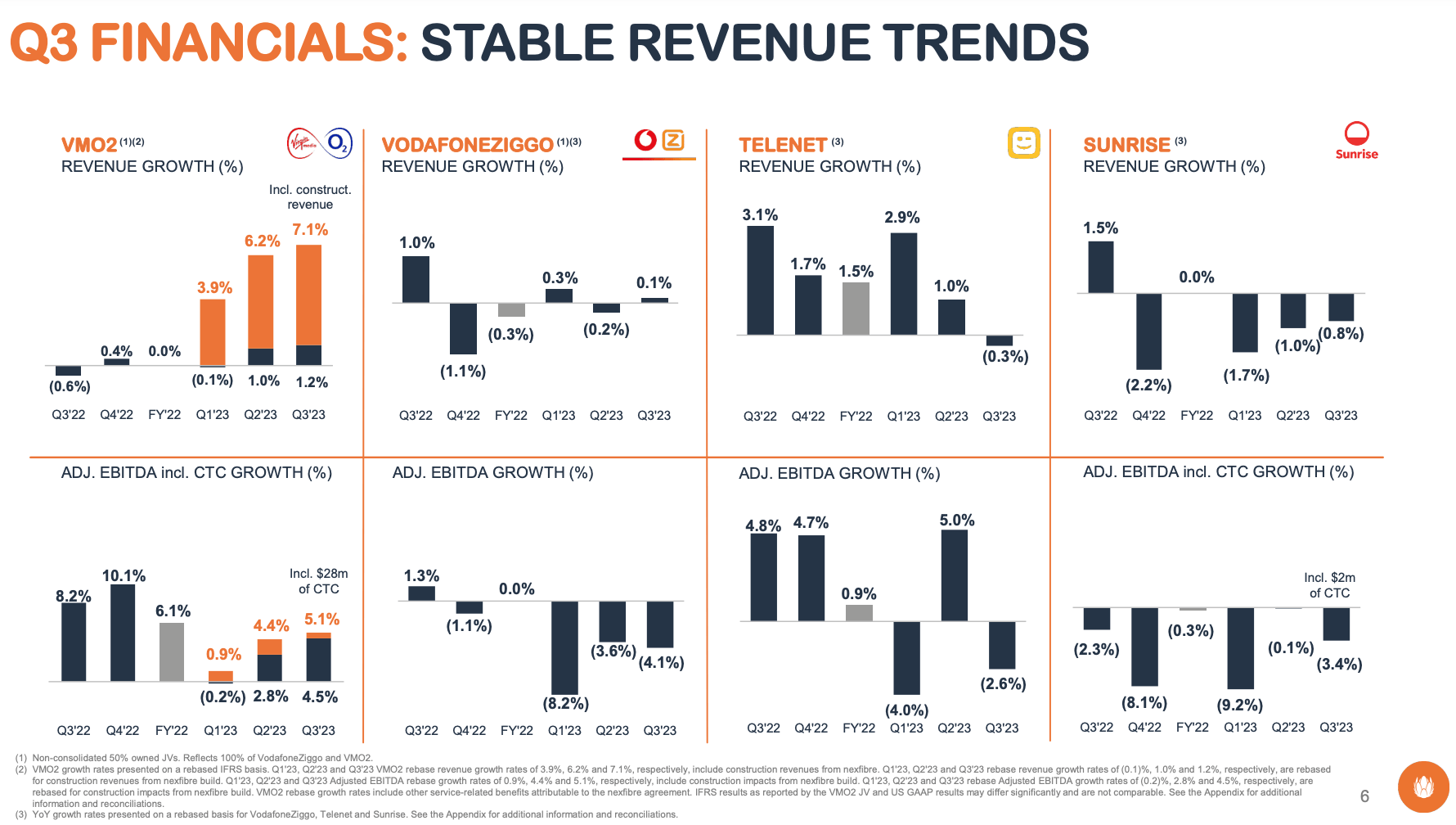

Whereas income on the consolidated companies was down 1.2% on an natural foundation over 9M’23, EBITDA is down extra for the above purpose. On the plus aspect, VMO2 is a vivid spot, posting accelerating EBITDA progress in Q3:

Supply: Liberty World Q3 2023 Outcomes Presentation

Looking forward to This autumn and full-year outcomes, there are good causes to count on this to mark a backside in earnings. Firstly, although up barely month-on-month in December, inflation within the Eurozone is now round 2ppt decrease than the Q3 common. This could assist ease strain on the price base as we lap 2023 outcomes this yr. Worth hikes can even profit from having an entire interval behind them, with VodafoneZiggo, for instance, placing by a ten% cellular value hike in This autumn:

In the meantime, VodafoneZiggo continues to develop postpaid cellular advertisements supporting our tenth consecutive quarter of cellular service income progress, and we simply introduced a ten% cellular value rise from October, which ought to assist the total yr outlook as effectively.

Mike Fries, Liberty World CEO, Q3 2023 Earnings Call

Moreover, each Dawn and Telenet have seen some company-specific points weigh on subscriber numbers, with Dawn migrating prospects over from the UPC model and Telenet working with depressed advertising and marketing spending not too long ago as a result of some IT points. The latter has now been resolved, whereas Dawn has moved over its most value-sensitive prospects. This also needs to assist comps this yr.

By yr, for instance, we’ll have migrated almost half the UPC base, and importantly, probably the most worth delicate section of that base. The Belgium market stays comparatively rational with value rises offsetting inflationary strain, however Telenet continued to be impacted by a decreased advertising and marketing spend because it managed by some IT points in Q3. In consequence, each postpaid and broadband advertisements have been damaging within the quarter. On a optimistic observe, although, September noticed a restoration and subscriber volumes and the advertising and marketing machine has ramped again up in This autumn.

Mike Fries, Liberty World CEO, Q3 2023 Earnings Name

Lastly, I’d observe that analysts proceed to expect progress at VMO2, which might offset the above struggles within the consolidated companies in any case, leading to flatter EBITDA general:

Supply: Liberty World

Inventory Seems to be Materially Undervalued

Liberty World’s Class A shares commerce for $19.37 every on the time of writing. Liberty has three courses of inventory: A, B and C. The Class A shares entitle holders to at least one vote per share; the Class B shares entitle holders to 10 votes per share; and the Class C shares don’t provide voting rights. In apply, the B shares commerce on little or no quantity and we are able to ignore them, leaving buyers to decide on between the A and C shares. Now, the C shares at the moment commerce at a premium to the A – round 6% on the time of writing. That is potential as a result of buybacks have been focused on the C shares not too long ago, however this isn’t one thing that’s set in stone – it’s largely a mirrored image of historic buying and selling patterns and might change sooner or later. With that being the case, I’ll reference the cheaper A shares on this piece.

Thanks, Polo. Hear, on the buyback query, our coverage has been traditionally to purchase Ks over As, principally as a result of they’ve traded till extra not too long ago at a reduction. And we do not imagine both shares ought to commerce completely different than the opposite as a result of though one is voting and one is nonvoting, we have all the time seen them as economically equal. The rationale for traditionally shopping for Ks over As was to attempt to keep the liquidity of the As since there have been fewer of them, and there are nonetheless fewer of them in order that we’ve got two wholesome buying and selling markets. In fact, that is modified extra not too long ago.

Mike Fries, Liberty World CEO, Q3 2023 Earnings Name

Valuing Liberty is a barely cumbersome endeavor as a result of there are a number of shifting elements to think about. Firstly, we’ve got the varied European telecoms companies, together with the JVs. Liberty additionally sports activities important money on the holding firm stage, plus a portfolio of investments. The latter contains stakes in listed firms, together with Vodafone (VOD) and U.Ok. broadcast community ITV (OTCPK:ITVPY) (OTCPK:ITVPF).

With the shares at $19.37, the market appears to be implicitly making use of a really subdued valuation to the telecoms companies. Together with investments held underneath individually managed accounts, money & equivalents on the holding firm stage stood at circa $3.5 billion on the finish of Q3. Name it round $8.90 per share primarily based on just below 400 million shares excellent. As for its investments, Liberty put the honest worth of its ventures at $3.2 billion, implying one other ~$8.15 per share on high of that.

Subtracting these from the present $19.37 inventory value leaves little or no for the fairness of the telecoms companies. Now, Liberty does function with substantial leverage on the subsidiary and JV ranges, sometimes within the 4-6x EBITDA vary. Even so, the implied valuation seems to be low. Analysts count on the telecoms companies to collectively generate ~$9.4 billion in 2023 adjusted EBITDA. Together with debt will get me to an implied EV/EBITDA of circa 5.7x. That is what the market seems to be valuing the telecoms companies at in mixture.

Supply: Liberty World

Evaluating to friends suggests important upside. In keeping with Searching for Alpha, U.S. cable firms Comcast (CMCSA), Charter (CHTR) and Altice USA (ATUS) commerce for round 7.2x ahead EBITDA. Trying a bit nearer to Liberty’s geographic footprint, comparable European telecoms friends like Dutch incumbent KPN (OTCPK:KKPNY) (OTCPK:KKPNF) and Swiss incumbent Swisscom (OTCPK:SCMWY) (OTCPK:SWZCF) equally commerce for round 7.4x EBITDA. Each firms in fact compete instantly with Liberty in these markets. Whereas ~7.4x EBITDA represents a premium to different European telecom gamers, I’d counsel these are higher comps for the rationale I set out earlier – particularly that these markets are extra rational, steady and fewer aggressive than different European international locations. Moreover, sure different friends have company-specific points that make a direct comparability considerably tough (e.g. U.Ok. incumbent BT is on the hook for giant top-up funds to its pension fund, absorbing a good portion of its free money circulate and miserable its a number of).

Even making use of a conservative blanket a number of of 6.5x to Liberty’s telecoms belongings factors to important undervaluation. At that stage, and adjusting for Liberty’s share of the JVs, the telecoms companies can be price round $13.50 per share in whole, resulting in a circa $30.55 honest worth general after together with money and Liberty’s investments. Implied upside can be virtually 60% from the present share value, additional suggesting a big margin of security. A extra sensible, however nonetheless very affordable a number of of 7x EBITDA utilized to the telecoms companies will get me to a good worth of ~$37 for Liberty inventory.

Closing The Hole

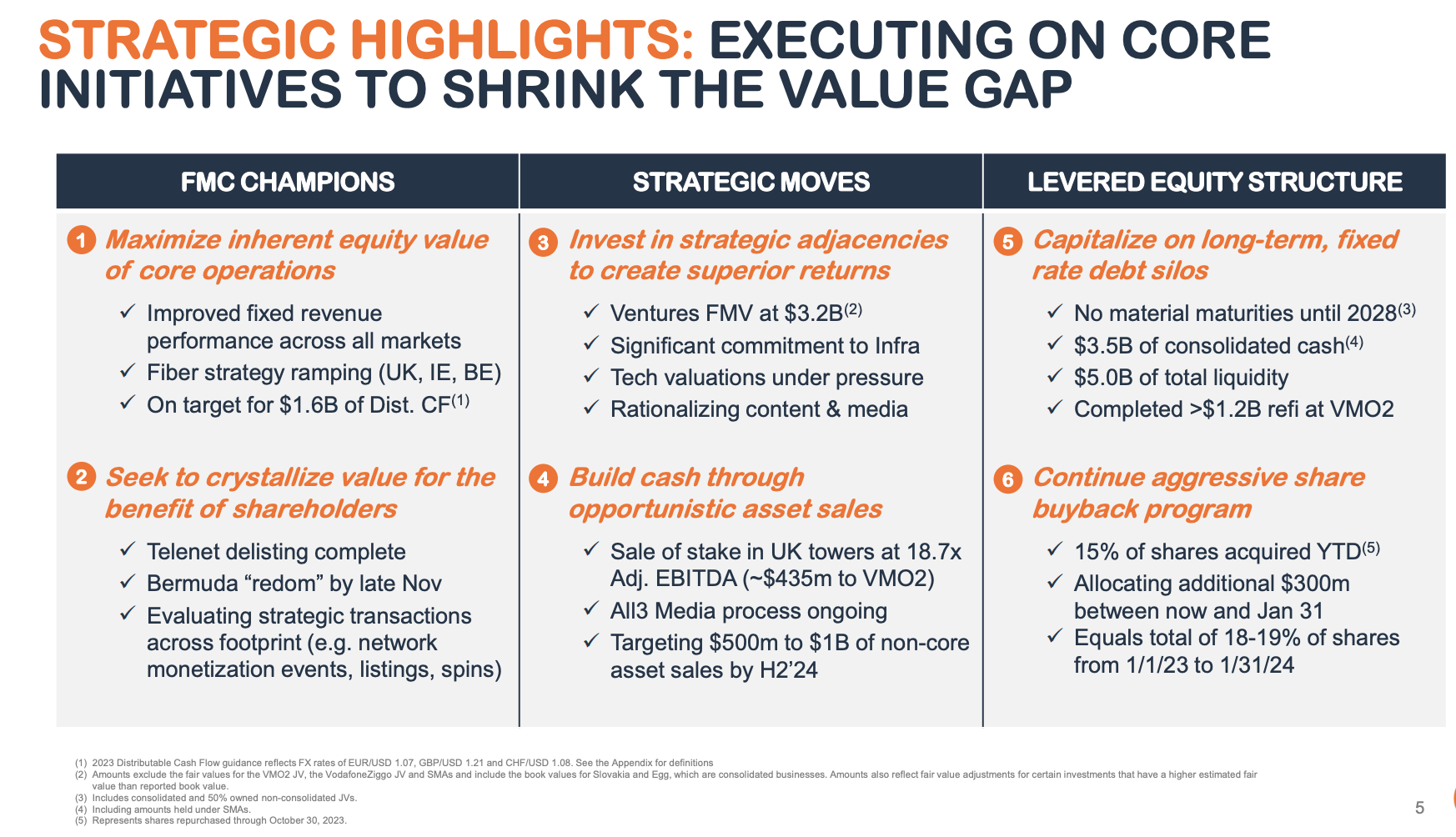

Whereas there isn’t a purpose why the market could not keep this obvious low cost indefinitely, Liberty is no less than attempting to shut the hole with aggressive inventory repurchases. It retired 15% of shares excellent in 2023 by Q3, and that may have been prolonged to just about 20% by the tip of the month:

Supply: Liberty World Q3 2023 Outcomes Presentation

Between money generated by its consolidated companies and dividends from the JVs, Liberty can have a stream of money which can enable it to hold on shopping for again inventory sooner or later. It would not pay a dividend and possibly by no means will, so buybacks are the first supply of capital returns to shareholders. I see this as an excellent factor given the present implied low cost to honest worth.

Dangers

There are a selection of dangers to think about right here. Firstly, and as talked about within the piece, Liberty operates with important leverage on the subsidiary and JV stage. Whereas there are not any maturities over the following few years, leverage is excessive versus friends and leaves the fairness extra uncovered to comparatively modest adjustments in earnings. Liberty’s markets are at the moment steady and the cashflows generated by mature telecoms are likewise sometimes defensive, however it’s potential that this might change sooner or later if extra rivals have been to enter its markets.

Supply: Liberty World Q3 2023 Outcomes Presentation

One other threat to think about is forex. Liberty inventory trades in USD however the underlying income and earnings of its telecoms companies are in CHF, EUR and GBP. Lastly, the acknowledged worth of its ventures might not replicate their intrinsic worth, which in fact would negatively have an effect on my honest worth estimate of Liberty inventory above.