JamesBrey

The mixed market cap of the Magnificent 7 shares is now equal to virtually 50% of GDP, which is greater than the determine for the complete S&P 500 on the 2009 low. Regardless of robust features, their valuation multiples have fallen markedly over current months, main some analysts to imagine that they’re undervalued given their excessive progress charges. Nonetheless, if we add again the influence of surging stock-based compensation, this group of shares nonetheless has a collective value to free money circulation ratio of 50x. That is a particularly excessive a number of to pay for corporations which might be already big and prone to develop little sooner than GDP progress over the long run.

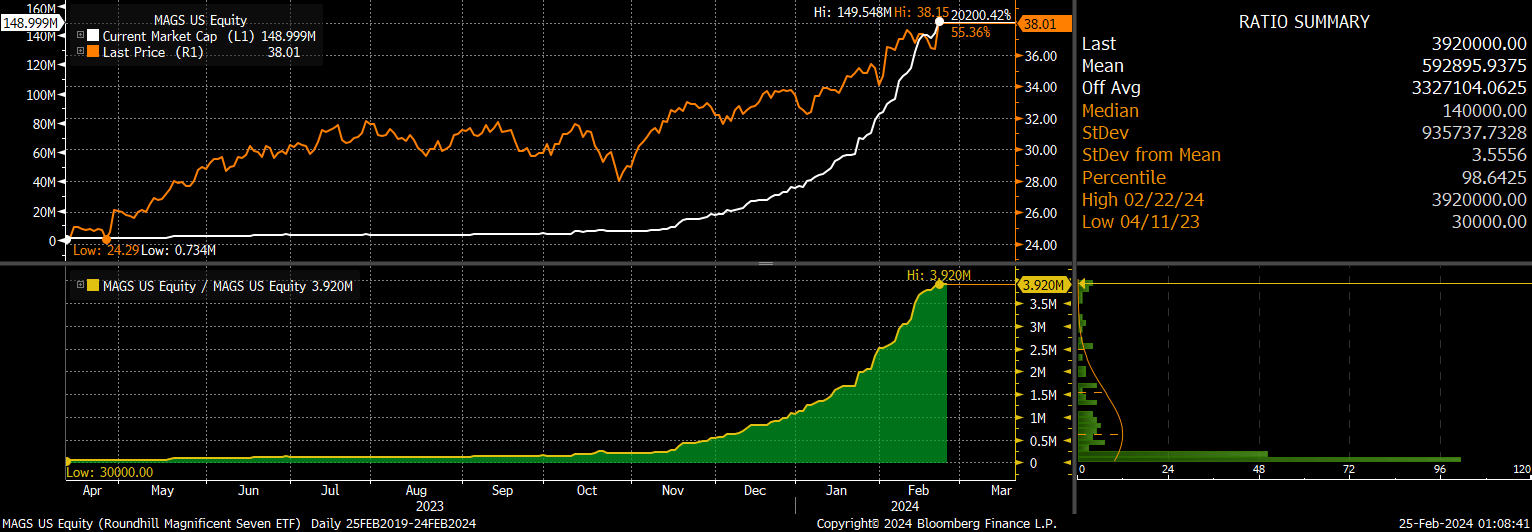

The Roundhill Magnificent Seven ETF (NASDAQ:MAGS) holds an equally weighted portfolio of Microsoft (MSFT), Apple (AAPL), Nvidia (NVDA), Alphabet (GOOGL), Amazon (AMZN), Meta Platforms (META), and Tesla (TSLA). Though it rebalances on a quarterly foundation, the surge in Nvidia and the weak point in Tesla has meant that Nvidia now has a 20% index weighting whereas Tesla has 9%. The fund fees an expense ratio of 0.29% which is on the excessive aspect. The ETF has been available on the market since April final 12 months and though it stays small with a market cap of $149mn, it has seen a parabolic rise in inflows in current months reflecting the rising optimism surrounding these shares.

MAGS ETF Market Cap Vs Worth (Bloomberg)

Inventory-Based mostly Compensation Is A Big Hidden Price

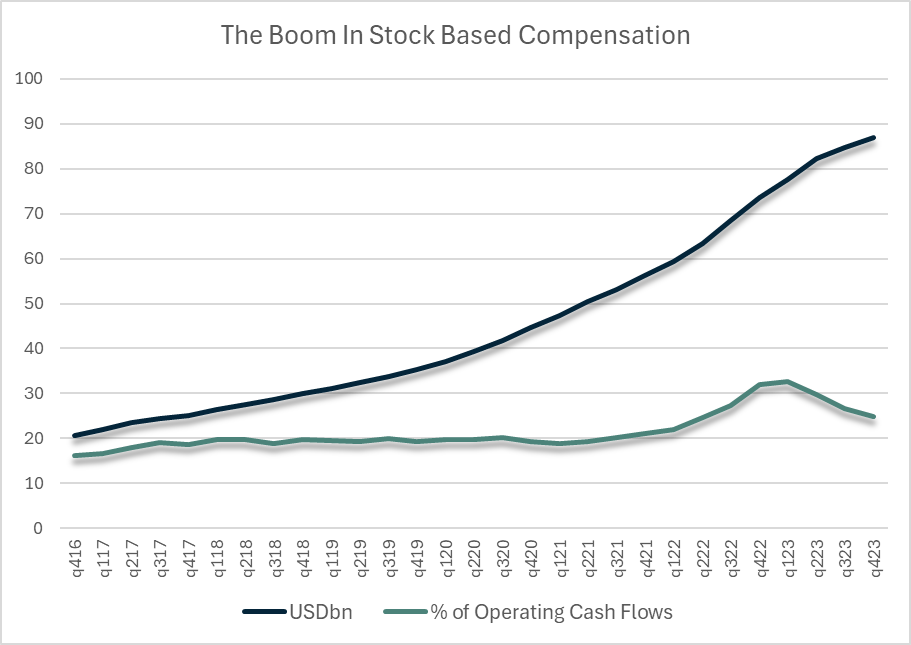

The Magnificent 7 paid out $87bn in stock-based compensation (SBC) over the previous 12 months amid rising competitors for expertise because the AI increase heats up. Such funds are up 18% y/y, and have doubled in simply 4 years. These 7 corporations now make up 62% of all stock-based compensation of Nasdaq 100 corporations.

Annual Inventory Based mostly Compensation Of Magnificent 7 Shares (Bloomberg)

By paying staff in shares quite than wages, this has allowed free money flows to be inflated, as this money shouldn’t be actually free. The equal amount of money have to be used to purchase again shares so as to stop share dilution when these shares are bought. Inventory-based compensation ought to subsequently be thought of as a value when calculating the Magnificent 7’s valuations. As Warren Buffett mentioned about stock-based compensation:

If inventory choices aren’t compensation, then what’s it? If compensation isn’t an expense, then what’s it?”

Over the previous 12 months Magnificent 7 free money flows amounted to $351bn, and with a mixed market cap of $13.3tn this ends in a value to free money circulation ratio of just about 38x. If we add again SBC, then this free money circulation determine falls to $264bn and the worth to free money circulation ratio rises to 50x.

The Larger They Are, The Slower They Develop

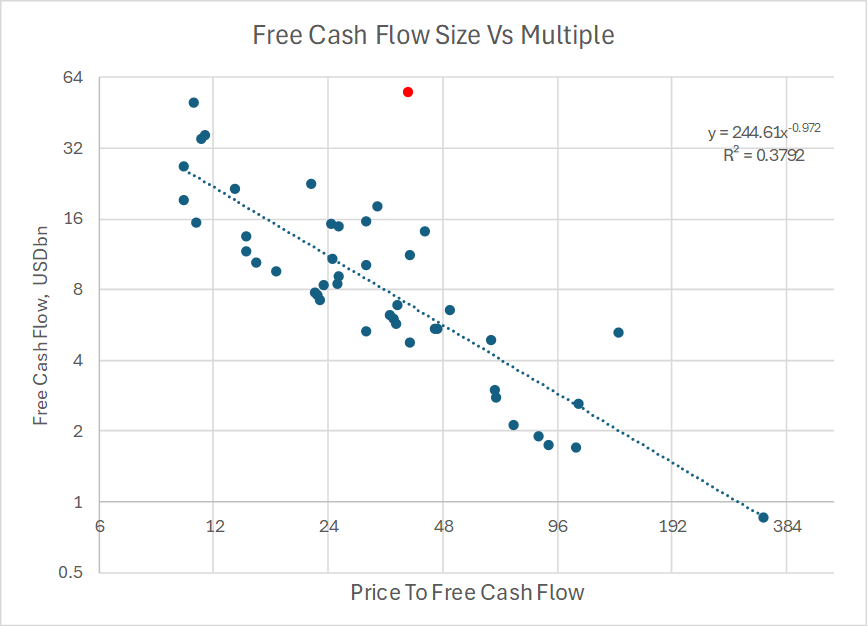

Buyers sometimes don’t worth giant corporations at excessive valuations. The chart under exhibits value to free money circulation ratio versus absolutely the measurement of free money flows for the 50 largest US shares. As market share will increase, buyers apply a decrease a number of in anticipation of slower progress. The pink dot is the common of the Magnificent 7, which stand out as commanding excessive multiples given its measurement.

Bloomberg

The Magnificent 7’s big free money flows will make it extraordinarily tough to proceed rising at double-digit charges. As an illustration, free money flows already make up 52% of the Nasdaq 100, 23% of S&P500, and 9% of the complete FTSE International All Cap index. With the US and international financial system rising at round 4%, if the Magnificent 7 can proceed rising at 10% yearly for the subsequent decade, this is able to enhance these percentages to 90%, 40% and 15% by 2034. It’s laborious to think about a world the place simply 7 corporations dominate the worldwide financial system to such an extent.

Let’s assume that they can generate 10% progress for the subsequent decade, however after that, their progress charges will inevitably sluggish to the speed of the US and international financial system of round 4%. To be able to be valued to return 10% yearly consistent with the long-term common, the Magnificent 7 must have a free money circulation yield (together with SBC) of 6%, assuming it pays out all its money to shareholders. In 10 12 months free money flows would rise to $685bn leading to a yield of simply 5.1%. To be able to yield 6% their inventory worth must fall by 14%, and when that’s discounted to the current day it might require a 67% decline to succeed in truthful worth.

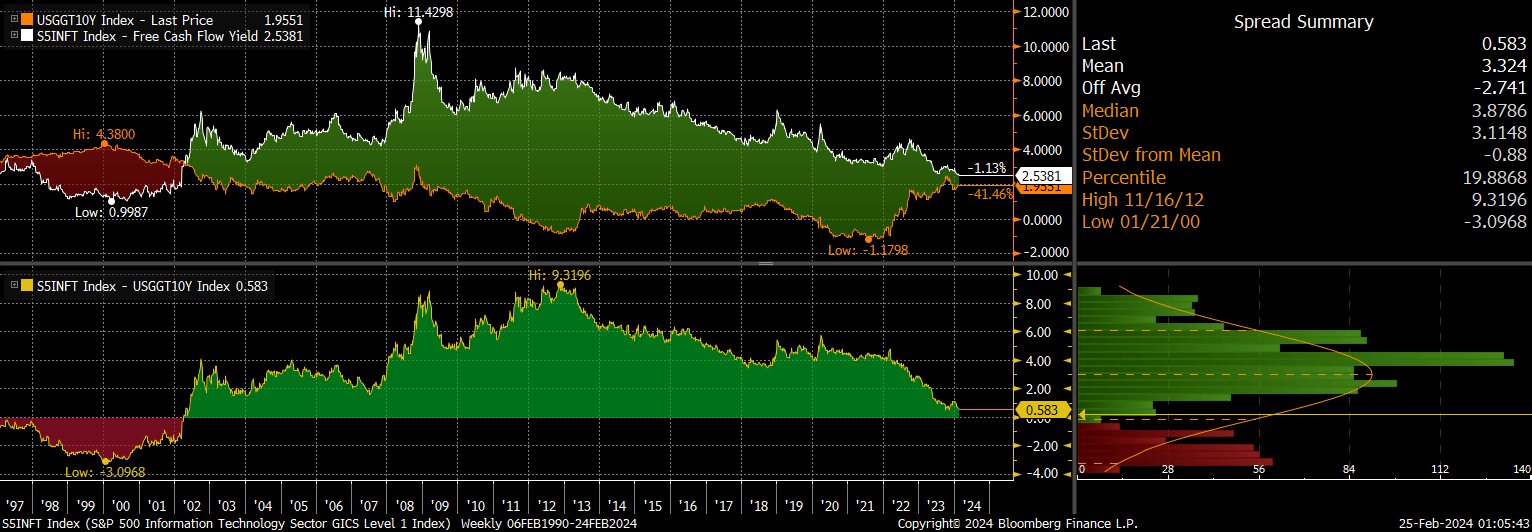

If this sounds loopy, simply keep in mind that tech shares yielded greater than 6% as not too long ago as 2019, and simply 12 years in the past they yielded 9 share factors greater than 10-year actual yields. If the identical threat premium over and above Treasuries had been to occur once more at present elevated charges, it might require their market cap to fall by 82%.

10 12 months Actual UST Yield Vs SPX Data Tech FCF Yield (Bloomberg)

It is All About The Required Threat Premium

It’s not altering assumptions about future progress that drive shares as a lot as it’s adjustments within the threat premium. Though the marginal investor could not essentially actually have a required fee of return in thoughts when making a inventory buy, it’s this enhance in buyers which might be shopping for for short-term speculative causes which have pushed up valuations to those excessive ranges.

JMP, QDS

The surge in retail shopping for over the previous few months exhibits that this development chasing behaviour is just like that seen on the earlier market prime in 2021. As soon as just a few days of consecutive weak point ensues, these buyers are prone to throw within the towel in a short time inflicting devastating losses as investor focus shifts to stopping losses quite than maximising features.

Abstract

The MAGS ETF faces critical headwinds after its speedy advance, because the Magnificent 7 commerce at a a number of of 50x free money flows when the surge in stock-based compensation is added again to replicate its true value to shareholders. With complete free money circulation already exceeding half of the complete Nasdaq 100, future progress charges for the Magnificent 7 will probably be compelled to converge to that of the general financial system, exposing the extent of overvaluation.