zimmytws

Do you want a March Insanity replace now that we’re formally into April?

The clock is ticking, the sphere is narrowing, and there is lots to speak about within the NCAA basketball world… together with off the court docket.

Should you learn my final article on the topic – “My ‘Sweet 16’ REITs Revealed” – you already know March Insanity “is an annual opportunity to learn humility.”

I say that as a result of, yearly, tens of millions of individuals put down on paper who they assume will win every match proper as much as the tip. And yearly, they fail.

Most of them fail exhausting.

As I wrote, “People have, of course, correctly guessed the winning team.” However in accordance with the NCAA itself, the percentages of filling out an ideal bracket are:

- 1 in 9,223,372,0326,854,775,808 for these engaged on sheer guesses and likelihood

- 1 in 120.2 billion for many who “know a little something about basketball.”

Both means, I feel we are able to all agree it is just about unattainable. So why even trouble?

Effectively, for one factor, it is enjoyable! For an additional, individuals who decide the perfect brackets can win a pair hundred {dollars} from their office pool. Or a lot, rather more on-line.

Who would not need a piece of that?

Ashtyn Gold from Raleigh, North Carolina, definitely does. And this 11-year-old nonetheless has an opportunity of successful.

Huge.

Should you’re like me, that is not true for you. However I do have eight actual property funding trusts (REITs) that may give you significantly better odds.

A Bracket Price Bragging About

I am actually excited to offer you my Elite 8 REITs in the present day – though the match has really progressed to the Ultimate 4 as I write this. However first, I do assume it is solely honest to provide credit score the place credit score is certainly as a consequence of Ashtyn Gold.

WRAL, which offers information for Raleigh, Durham, and Fayetteville, North Carolina, reported on the little miss simply the opposite day. The outlet wrote how she:

… appropriately picked the Ultimate 4 matchups in ESPN’s Event Problem contest… of the 22.6 million individuals who entered the competition, her bracket is ranked 109 and within the 99th percentile of all brackets.

Nonetheless in elementary faculty, the kid has knowledge past her years. She informed the outlet that she “kept her bracket strategy simple” but studious.

“‘I watched them and I see who can handle the pressure, who can get at least far and who has won more games,'” she stated.

Her father initially wished to make her bracket, however Gold stated she wished to make a special one and picked the red-hot NC State Wolfpack to win the large dance.

Her father’s bracket at present sits in 11 millionth place.

I am not fairly certain if I would really feel extra proud or chagrined if one among my 4 daughters trounced me so badly at such a younger age. In all probability proud, although the “chagrin” ranges can be fairly excessive too.

Since Ashtyn is not my daughter although, I can supply my congratulations and properly needs with completely no hesitation. The truth is, I am going to go as far as to say that, if she needs to show courses after this, I’d simply enroll.

Train me your March Insanity methods!

The REIT Competitors Provides You A lot Extra to Work With

I will not inform you how properly (or how badly) my March Insanity bracket goes. However I’ll inform you that I did not guess the farm on it.

I did not must. Not when I’ve REITs to depend on in a correctly balanced and individually tailor-made portfolio.

And never after I personal the fastidiously chosen REITs that I do.

Once I purchase a inventory, I am going for the win. Like Ashtyn Gold, I wish to maintain my “strategy simple.” I analysis the REIT – or different asset – in query, particulars like its:

- Share worth

- Previous valuations

- Present stability sheet

- Future plans and projections

- Dividend, yield, and dividend historical past

- Administration

- Holdings

- Company statements and objectives.

I then crunch the numbers, analyze the outcomes, and act from there.

It is that course of that is led me to advance eight REITs since final week’s report. To refresh your reminiscence, my Candy 16 picks had been:

- VICI Properties (VICI)

- Agree Realty (ADC)

- Realty Revenue (O)

- Important Properties Realty Belief (EPRT)

- Digital Realty Belief (DLR)

- American Tower (AMT)

- Healthpeak Properties (DOC)

- Alexandria Actual Property (ARE)

- Boston Properties (BXP)

- Mid-America Residence Communities (MAA)

- Solar Communities (SUI)

- Prologis (PLD)

- Rexford Industrial Realty (REXR)

- Further House Storage (EXR)

- Regency Facilities (REG)

- Ladder Capital (LADR).

That is 4 net-lease REITs, two tech, two workplace, two residential, and two industrial, together with one self-storage, retail, healthcare, and mortgage REIT.

Which of them made it via and which of them did not? Let’s examine what we’ll see…

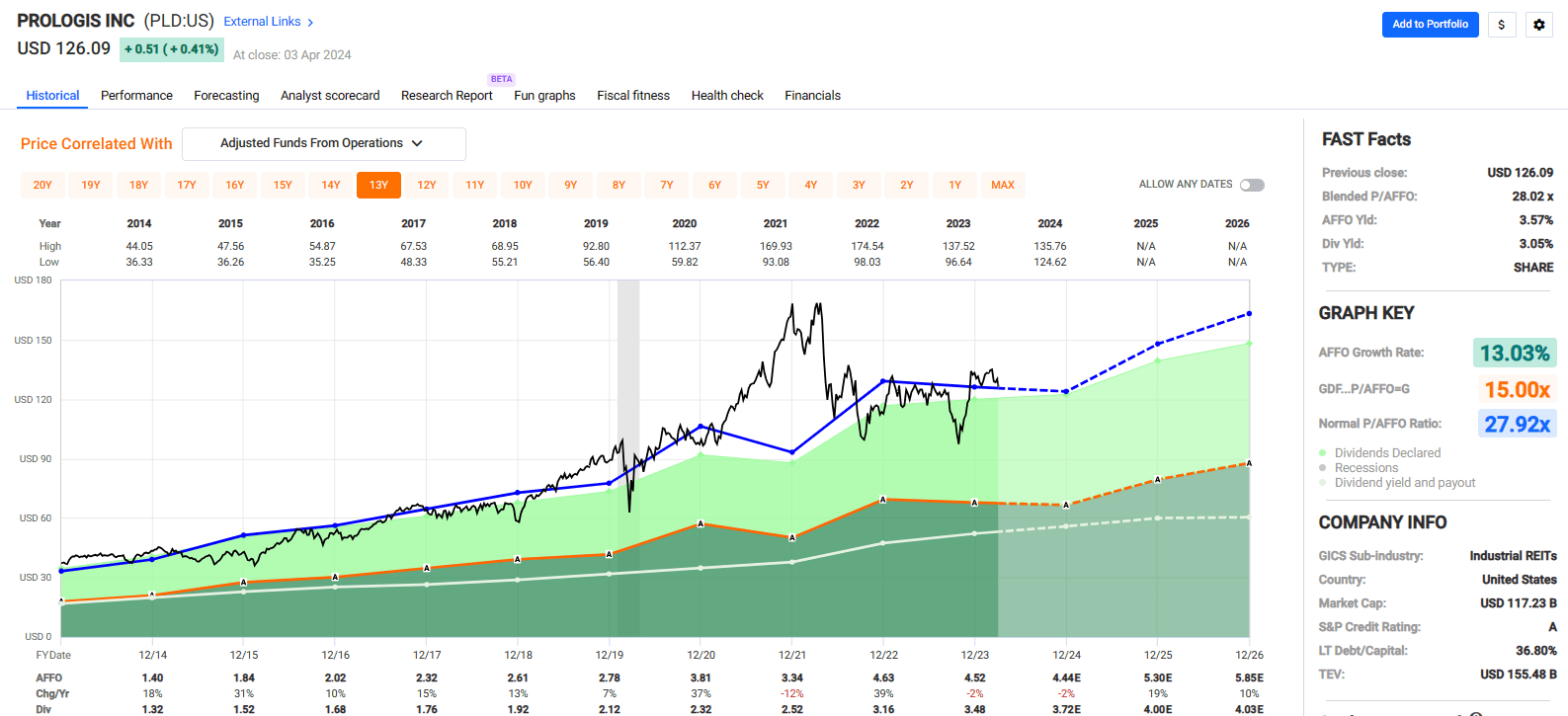

Prologis (PLD)

With a market cap of roughly $118.3 billion Prologis is a juggernaut within the industrial sector. PLD is an industrial REIT that has a worldwide portfolio spanning throughout 19 international locations and on 4 continents with over 5,600 properties encompassing roughly 1.2 billion SF.

The corporate has round 6,700 tenants that embrace top-tier companies resembling Amazon, FedEx, Residence Depot, DHL, UPS, Tesla, and Pepsi. Its prime tenant is Amazon which makes up 5.0% of the corporate’s lease, adopted by Residence Depot and FedEx which make up 1.5% and 1.4% respectively.

In complete, PLD receives 14.5% of its lease from its prime 10 tenants and 20.5% of its lease from its prime 20 tenants.

PLD has an investment-grade stability sheet and an A credit standing from S&P World. The corporate has wonderful debt metrics resembling a debt to adjusted EBITDA of 4.6x, a long-term debt to capital ratio of 36.80%, and a hard and fast cost protection ratio of seven.9x.

Since 2014 PLD has delivered a median AFFO development charge of 13.03% and a median dividend development charge of 12.14%. Analyst anticipate AFFO per share to fall by -2% within the present yr, however then enhance by +19% in 2025 and by +10% the next yr.

The inventory pays a 3.05% dividend yield and trades at a P/AFFO of 28.02x, in comparison with its 10-year common AFFO a number of of 27.92x.

We charge Prologis a Purchase.

FAST Graphs

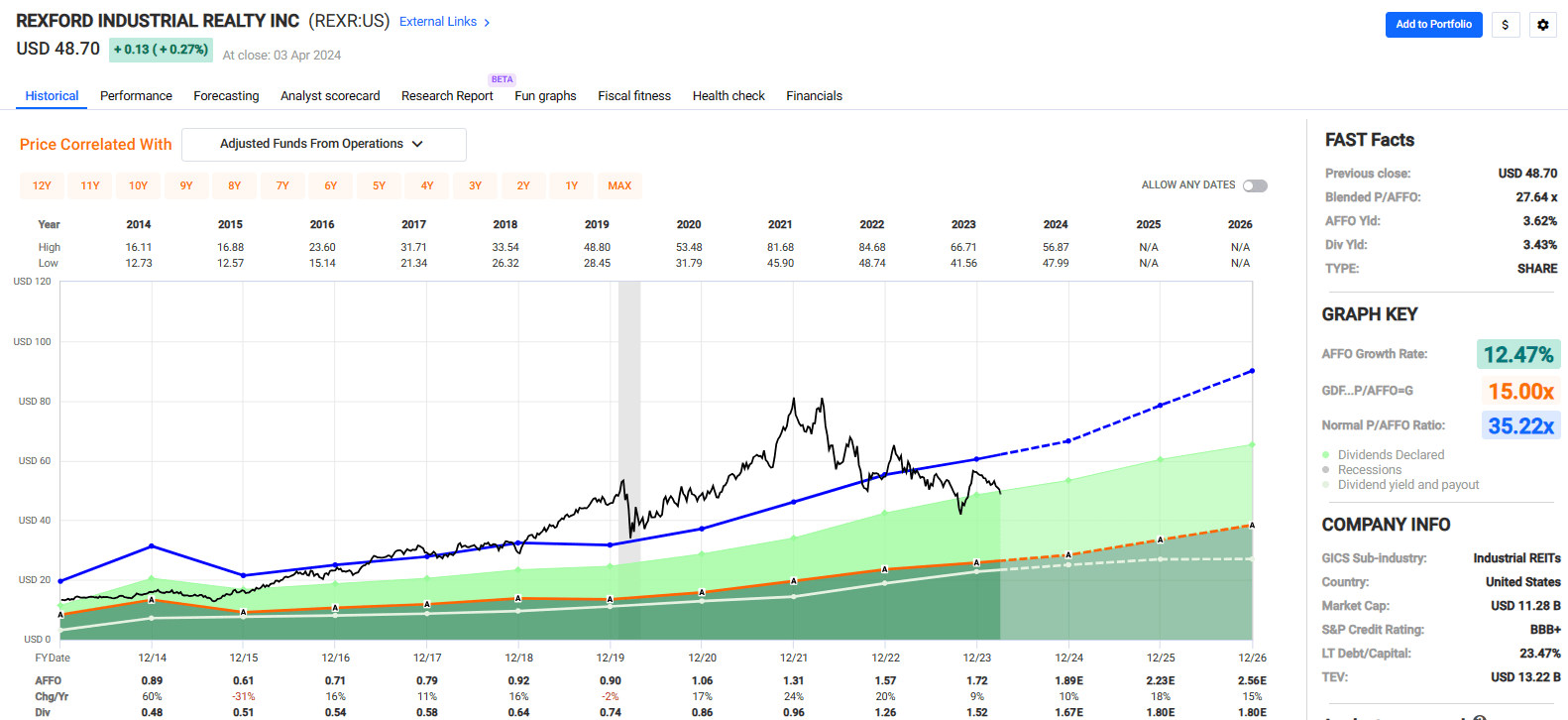

Rexford Industrial Realty (REXR)

The 2nd industrial REIT to make the lower is Rexford Industrial Realty. By way of high quality this firm is on par with Prologis, however by way of funding technique the two REIT’s are polar opposites.

Each REITs put money into industrial properties and each have fortress-like stability sheets, however REXR focuses solely on industrial properties in Southern California (“SoCal”) infill markets, whereas PLD has a worldwide portfolio with properties in 19 international locations.

REXR has a market cap of roughly $10.6 billion and a forty five.9 million SF portfolio made up of 374 properties which might be leased to roughly 1,600 tenants with a same-property portfolio occupancy of 97.5%.

REXR has such a powerful concentrate on the SoCal infill area as a result of sheer measurement of its industrial market and the favorable provide and demand dynamics. Southern California is the 4th largest industrial market on the planet, behind solely China, Japan, and the complete U.S.

The SoCal infill market has a persistent imbalance between provide and demand as a consequence of pure obstacles (mountains / ocean) that restrict the provision of developable land, mixed with the excessive demand within the area that’s house to roughly 24 million residents and greater than 600,000 corporations.

REXR is investment-grade with a BBB+ credit standing from S&P World. The corporate has wonderful debt metrics together with a web debt to adjusted EBITDA of three.6x, a long-term debt to capital ratio of 23.47%, and an EBITDA to curiosity expense ratio of 8.25x.

Since 2014 Rexford has delivered a median AFFO development charge of 12.47% and a compound dividend development charge of 21.89%. Analyst anticipate AFFO per share to extend by 10% in 2024, after which enhance by 18% and 15% within the years 2025 and 2026 respectively.

The inventory pays a 3.43% dividend yield and trades at a P/AFFO of 27.64x, in comparison with its 10-year common AFFO a number of of 35.22x.

We charge Rexford Industrial Realty a Sturdy Purchase.

FAST Graphs

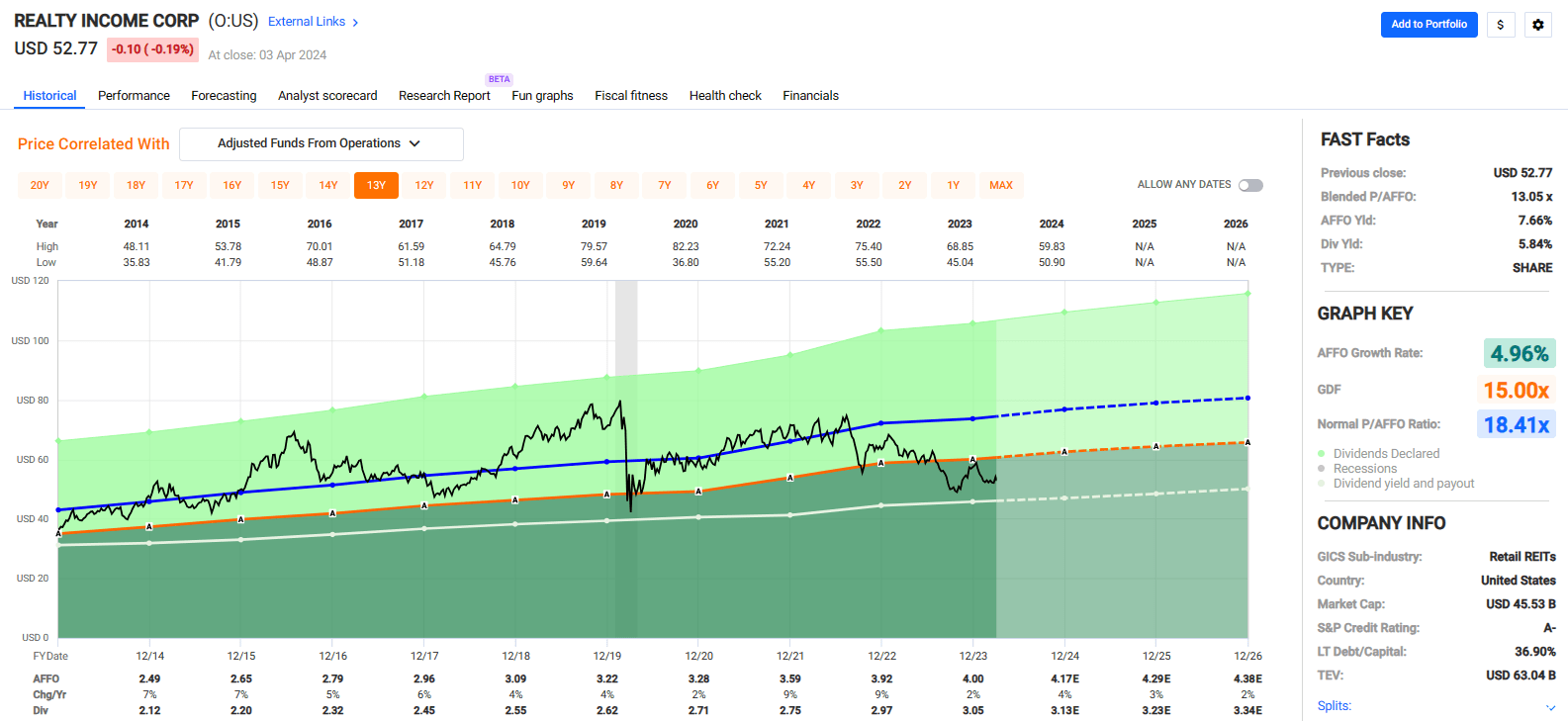

Realty Revenue (O)

For our first web lease REIT we went with the standard-bearer within the area which has been paying month-to-month dividends since its formation in 1969. Realty Revenue specializes within the acquisition and administration of portfolio of web leased properties which might be primarily single-tenant, free-standing buildings.

On the finish of 2023 the corporate had a 272.1 million SF portfolio consisting of 13,458 industrial properties situated in all 50 states, the UK, Spain, Italy, Puerto Rico, Portugal, Eire, France, and Germany. Roughly 82% of its portfolio consisted of retail properties, ~13% consisted of business properties and ~4% consisted of gaming properties at yr finish.

In January the corporate closed its merger with Spirit Realty, which is predicted to extend its property rely to over 15,000 and its industrial publicity to over 15%.

The web lease REIT primarily focuses on retail industries which might be resilient to recession and proof against e-commerce. Its largest business is grocery shops which made up 11.4% of its 2023 lease, adopted by comfort and greenback shops which made up 10.2% and seven.1% respectively.

Realty Revenue is a S&P 500 Dividend Aristocrat and has elevated its dividend for 29 consecutive years. It has been in a position to accomplish such a feat as a consequence of its conservative and regular enterprise mannequin that has generated optimistic AFFO per share development in 27 out of the final 28 years.

For the reason that firm’s public itemizing in 1994 it has delivered a 13.9% compound annual complete return with half the volatility of the broader market as measured by its beta of 0.5.

Since 1996 it has achieved a median AFFO per share development charge of ~5% and has a compound annual dividend development charge of 4.3% since 1994.

Extra lately, during the last 10 years the corporate has had a median AFFO development charge of 4.96% and a median dividend development charge of three.92%.

The corporate has an A- credit standing from S&P World and a powerful stability sheet with a web debt to professional forma adjusted EBITDAre of 5.5x, a long-term debt to capital ratio of 36.90%, and a hard and fast cost protection ratio of 4.7x.

At the moment the inventory pays a 5.84% dividend yield and trades at a P/AFFO of 13.05x, in comparison with its 10-year common AFFO a number of of 18.41x.

We charge Realty Revenue a Purchase.

FAST Graphs

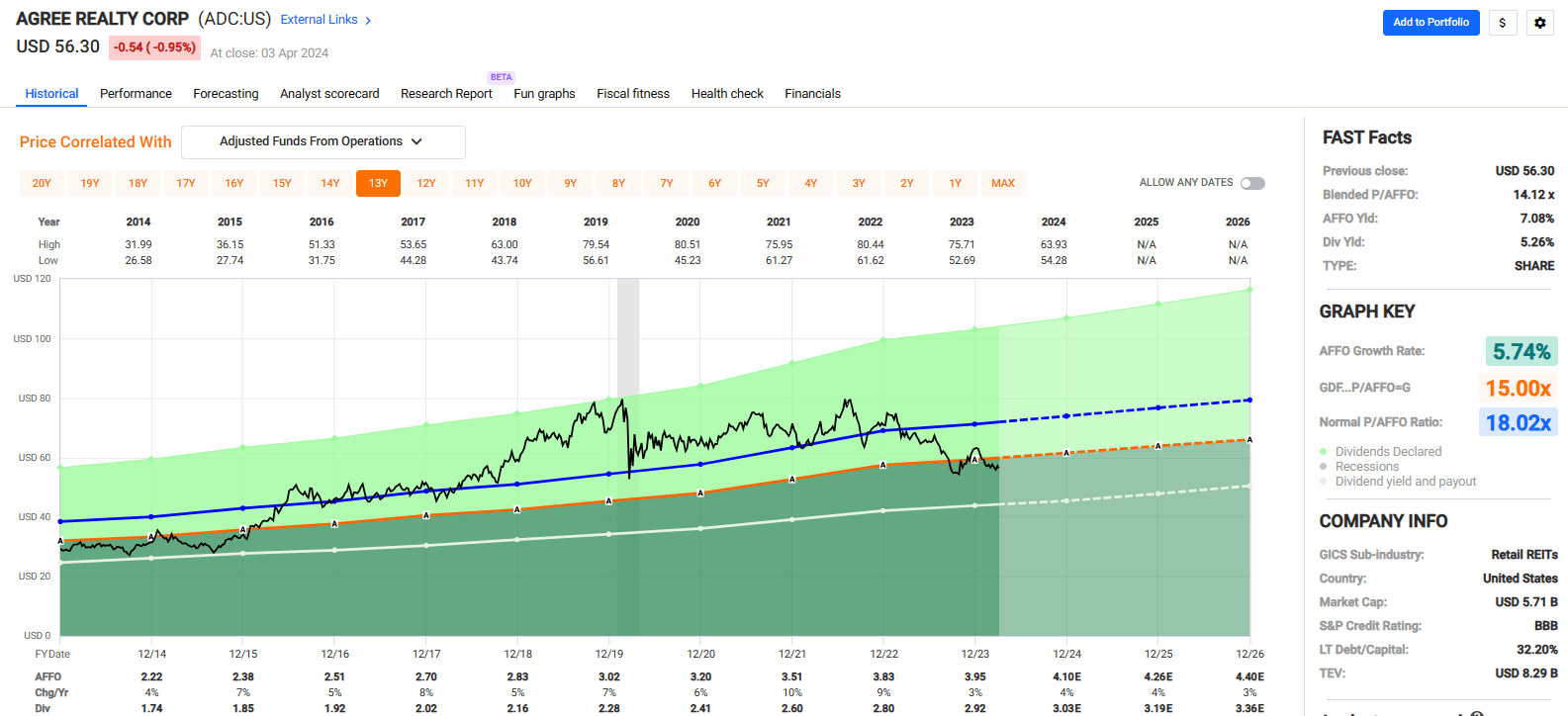

Agree Realty (ADC)

In some ways Agree Realty is sort of a smaller model of Realty Revenue in that they’re each web lease REITs that maintain high-quality portfolios and pay month-to-month dividends.

ADC has a market cap of roughly $5.7 billion and 44.2 million SF portfolio made up of two,135 industrial properties situated throughout 49 states. Its portfolio was 99.8% leased and had a W.A. remaining lease time period of roughly 8.4 years on the finish of 2023.

Agree Realty invests in free-standing retail properties that fungible in nature. The corporate avoids specialised properties resembling automotive washes or golf driving ranges since discovering a brand new tenant would require an operator in the identical business. As a substitute, ADC seems for fundamental, 4×4 packing containers that can be utilized throughout a number of industries.

ADC seems to amass free-standing properties leased to high-quality tenants resembling Tractor Provide, Sherwin Williams, Residence Depot, Chick-fil-A, 7-Eleven, Lowes and Costco. As of the tip of 2023, the corporate reported that 69.1% of its annualized base lease (“ABR”) was obtained from investment-grade tenants.

The corporate is concentrated on defensive retail industries which might be proof against e-commerce. ADC’s prime retail sector is grocery shops which made up 9.6% of its ABR, adopted by house enchancment and auto service which made up 8.7% and eight.6% respectively.

The web lease REIT has a BBB credit standing from S&P World and a fortress-like stability sheet with a web debt to EBITDA of 4.7x, a long-term debt to capital ratio of 32.20%, and a hard and fast cost protection ratio of 5.0x.

Moreover the corporate has no important debt maturities till 2028 and a W.A. time period to maturity of virtually 7.0 years.

Agree Realty began paying month-to-month dividends in 2021. Previous to the change the corporate paid a quarterly dividend and paid 107 consecutive quarterly dividends between 1994 and 2020. Since shifting to a month-to-month dividend the corporate has paid 38 consecutive month-to-month dividends.

Since 2014 the corporate has had a median AFFO development charge of 5.74% and a median dividend development charge of 5.94%. The inventory pays a 5.26% dividend yield and trades at a P/AFFO of 14.12x, in comparison with its 10-year common AFFO a number of of 18.02x.

We charge Agree Realty a Purchase.

FAST Graphs

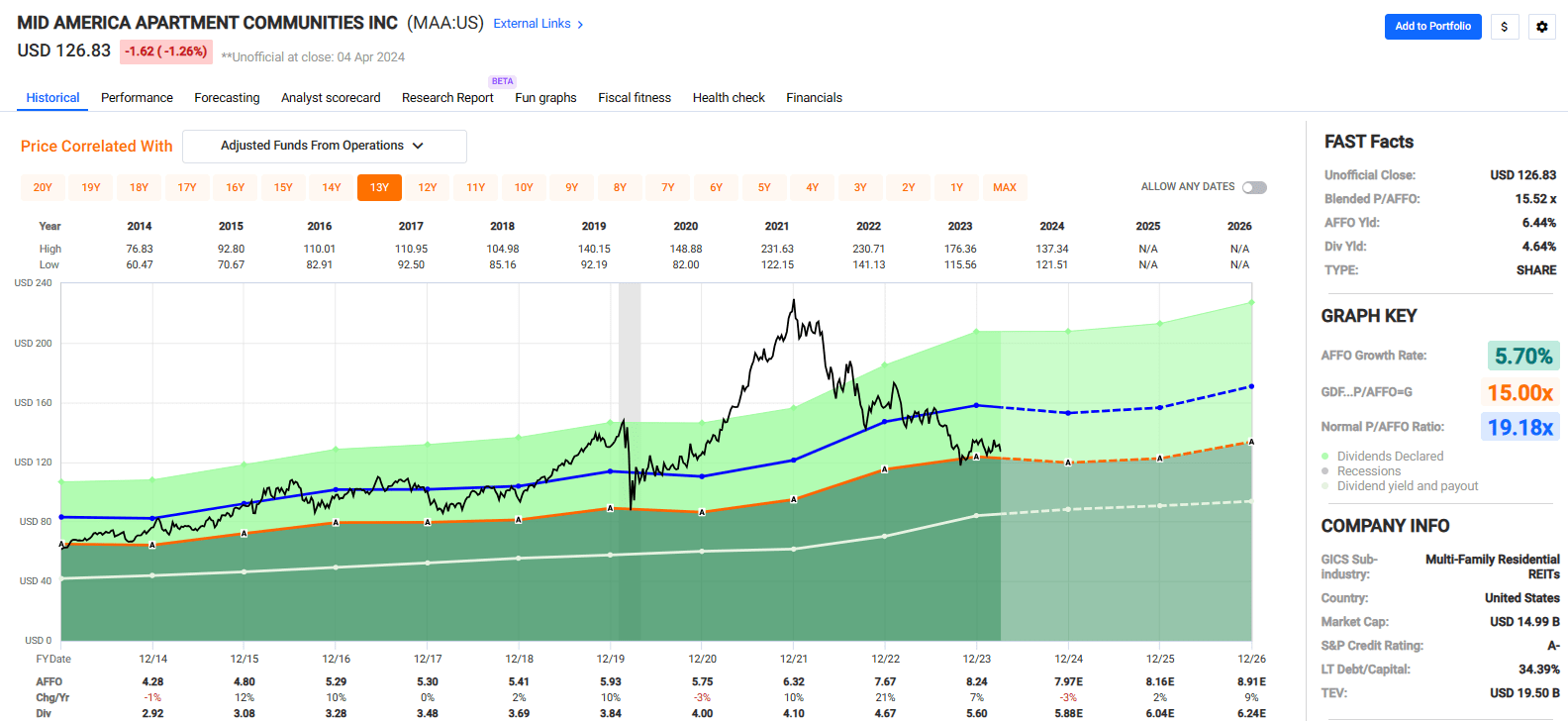

Mid-America Residence Communities (MAA)

Mid-America is a multifamily REIT that’s targeted on the acquisition, improvement, and administration of house communities which might be strategically concentrated within the Sunbelt area.

The S&P 500 firm has a market cap of $14.7 billion and a portfolio that consists of virtually 103,000 house houses situated in 16 states and Washington, D.C.

The corporate seems to generate a secure money stream and pay dividends to its shareholders via all financial cycles and has diversified its portfolio throughout worth factors, house kinds, markets, and submarkets to realize this goal.

MAA has a powerful concentrate on the Sunbelt and most of its prime markets reside on this area. As a proportion of 4Q-23 web working earnings (“NOI”) its prime market was Atlanta at 12.7%, adopted by Dallas and Tampa at 9.6% and seven.2% respectively.

By market measurement 70% of its portfolio is situated in massive markets whereas 30% is situated in mid-tier markets and by submarket, 47% of its portfolio is situated within the internal loop, 42% is situated in suburban areas, and 11% is situated in downtown enterprise districts.

By property class, 51% of its portfolio is designated as class A- to B+, 38% is designated class A+ to A, and 11% is designated class B to B-.

And by property sort, 63% of its portfolio consists of backyard type flats which have 3 tales or much less, 33% of its portfolio consists of mid-rise, whereas the remaining 4% is made up of high-rise house buildings.

MAA has an investment-grade stability sheet with an A- credit standing from S&P World. The corporate has wonderful debt metrics together with a web debt to adjusted EBITDAre of three.6x, a long-term debt to capital ratio of 34.39%, and a debt service protection ratio of seven.8x.

Moreover, the corporate has a superb dividend observe document with no dividend suspensions or cuts since 1994. MAA pays a quarterly dividend and in January it paid its one hundred and twentieth consecutive quarterly dividend.

Since 2014 the corporate has had a median AFFO development charge of 5.70% and a median dividend development charge of seven.37%. The inventory pays a 4.64% dividend yield and trades at a P/AFFO of 15.52x, in comparison with its 10-year common AFFO a number of of 19.18x.

We charge Mid-America Residence Communities a Sturdy Purchase.

FAST Graphs

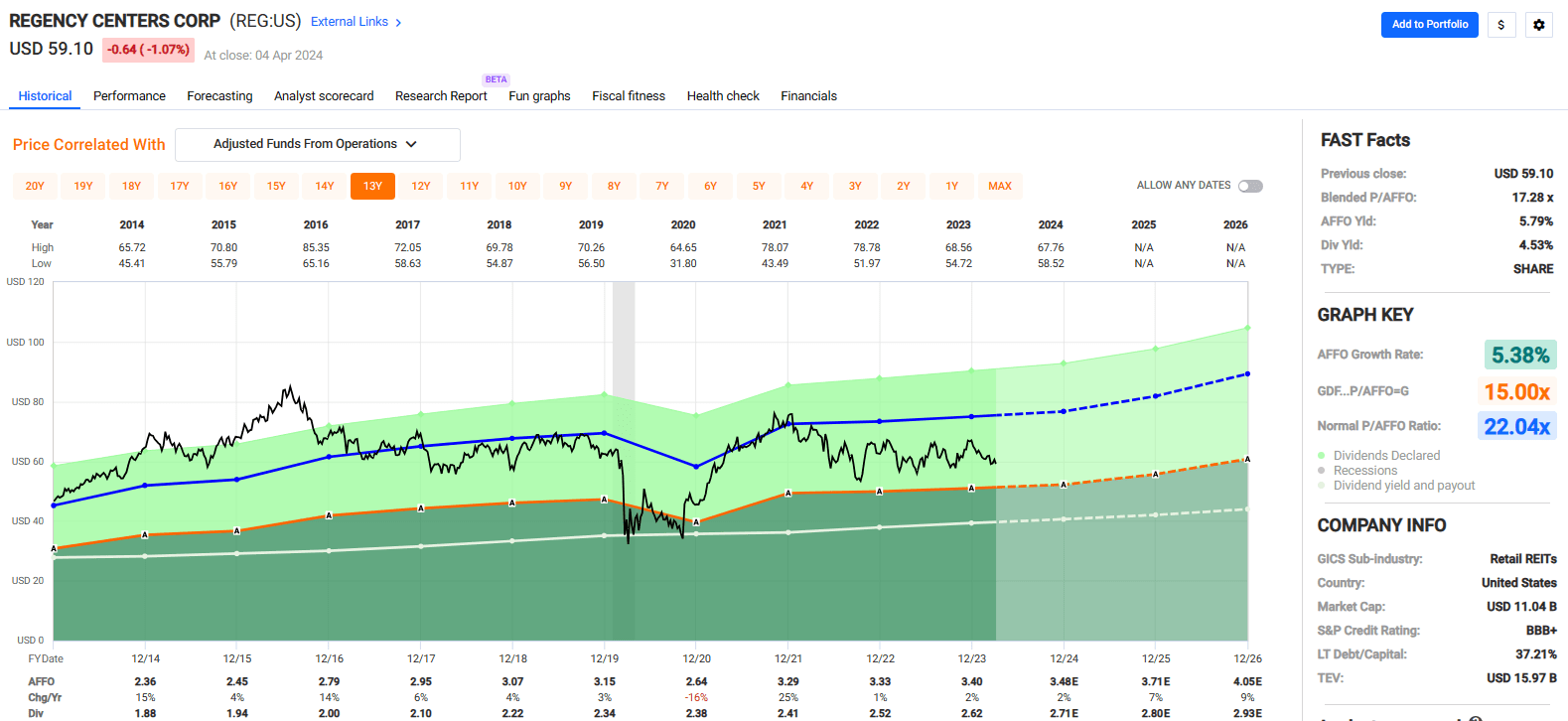

Regency Facilities (REG)

For our first and solely purchasing middle REIT we went with Regency Facilities. This firm focuses on creating and managing a portfolio of open-air, grocery anchored purchasing facilities which might be situated in prime markets throughout the USA.

The corporate’s portfolio is properly diversified throughout the U.S. with a powerful presence in Northeast and Mid-Atlantic, in addition to Texas, Florida, and California. As a proportion of its ABR, the Northeast makes up 23%, the Mid-Atlantic makes up 8%, whereas Texas, Florida and California make up 7%, 19%, and 23% respectively.

The corporate targets properties with enticing surrounding demographics. Inside a 3-mile radius of its commerce areas there may be a median inhabitants of 124,000, a W.A. family earnings of $152,000, a median house worth of $585,000, and 54% of the inhabitants surrounding its purchasing facilities has a bachelor’s diploma or increased.

Greater than 80% of REG’s portfolio is grocery-anchored by main grocers resembling Publix, Kroger, and Complete Meals. The corporate locations a excessive emphasis on grocers and appears on the business as a cornerstone of its working technique.

By retailer rely, Regency is the highest landlord for lots of the top-tier grocers within the U.S. together with Publix and Complete Meals. Moreover the corporate is the 2nd largest landlord for Kroger. Together with grocery shops the corporate seems for tenants that supply necessity-based companies and items.

6 out of its prime 10 tenants are main grocers and embrace Publix, Albertsons, Kroger, Complete Meals, Ahold Delhaize, & Dealer Joe’s and seven of its prime 10 tenants have an investment-grade credit standing from S&P World.

Regency Facilities has an investment-grade credit standing of BBB+ from S&P World and was simply upgraded to A3 by Moody’s in February 2024. The corporate has a powerful stability sheet with a web debt plus most popular to EBITDAre of 5.1x, a long-term debt to capital ratio of 37.21%, and a hard and fast cost protection ratio of 4.7x.

Since 2014 the corporate has had a median AFFO development charge of 5.38% and a median dividend development charge of three.55%. The inventory pays a 4.53% dividend yield and trades at a P/AFFO of 17.28x, in comparison with its 10-year common AFFO a number of of twenty-two.04x.

We charge Regency Facilities a Purchase.

FAST Graphs

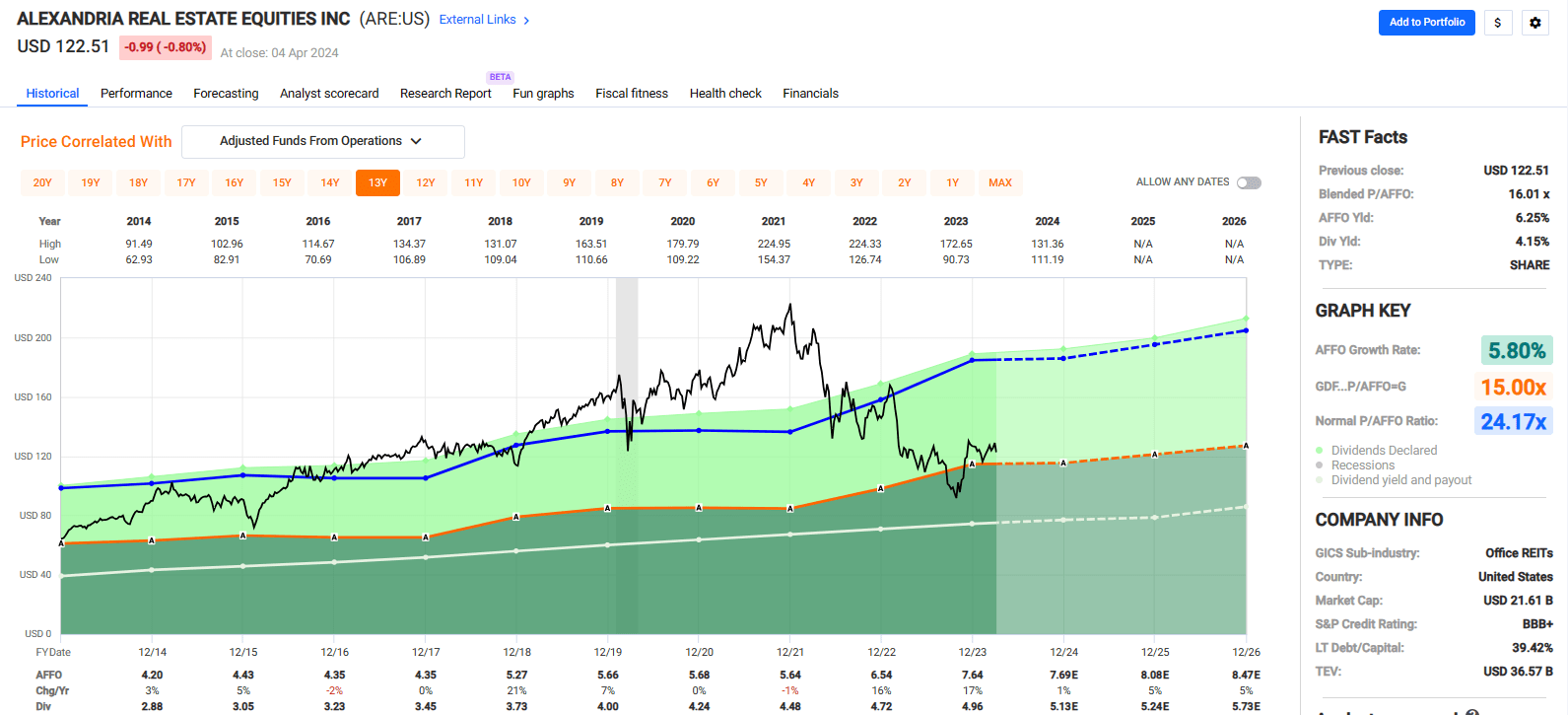

Alexandria Actual Property (ARE)

For our first and solely “office” decide we went with Alexandria Actual Property. I put workplace in quotes as a result of though ARE is technically within the workplace sector, the corporate is mostly a life science REIT.

The corporate pioneered the life science specialty area of interest since its formation in 1994. It specializes within the improvement and administration of life science properties which might be situated in innovation cluster areas in Boston, New York Metropolis, San Diego, San Francisco, Seattle, Maryland, and the Analysis Triangle.

Alexandria has a market cap of roughly $21.8 billion and an asset base in North America totaling 73.5 million SF which incorporates ~42.0 rentable sq. ft (“RSF”) of working properties, virtually 6.0 million RSF of properties below development, 2.1 million RSF of near-term improvement, and 23.9 million SF allotted for future improvement.

As of the tip of 2023, the corporate’s working properties had been 94.6% leased and had a weighted common remaining lease time period of seven.4 years.

ARE leases its laboratory area out to main pharmaceutical and biotech corporations in addition to prime medical and academic establishments. It has a really diversified tenant base and solely receives 35.5% of its annual income from its prime 20 tenants.

A number of the firm’s prime 20 tenants embrace Moderna, Eli Lily, Bristol-Myers Squibb, Roche, Alphabet, Harvard College, Pfizer, New York College, and Boston Youngsters’s Hospital. Its largest tenant is Moderna which has a remaining lease time period of 13.2 years and makes up 5.7% of the corporate’s annual income.

ARE has an investment-grade stability sheet with a BBB+ credit standing from S&P World. The corporate has excellent debt metrics together with a web debt and most popular to adjusted EBITDA of 5.1x, a long-term debt to capital ratio of 39.42%, and a fixed-charge protection ratio of 4.7x.

Moreover the corporate’s debt has a W.A. rate of interest of three.72% and a W.A. remaining debt time period of 12.8 years with no debt maturing earlier than 2025.

Since 2014 the corporate has had a median AFFO development charge of 5.80% and a median dividend development charge of 6.64%. Analysts anticipate AFFO per share to extend by 1% in 2024, after which enhance by 5% in each 2025 and 2026. The inventory pays a 4.15% dividend yield and trades at a P/AFFO of 16.01x, in comparison with its 10-year common AFFO a number of of 24.17x.

We charge Alexandria Actual Property a Sturdy Purchase.

FAST Graphs

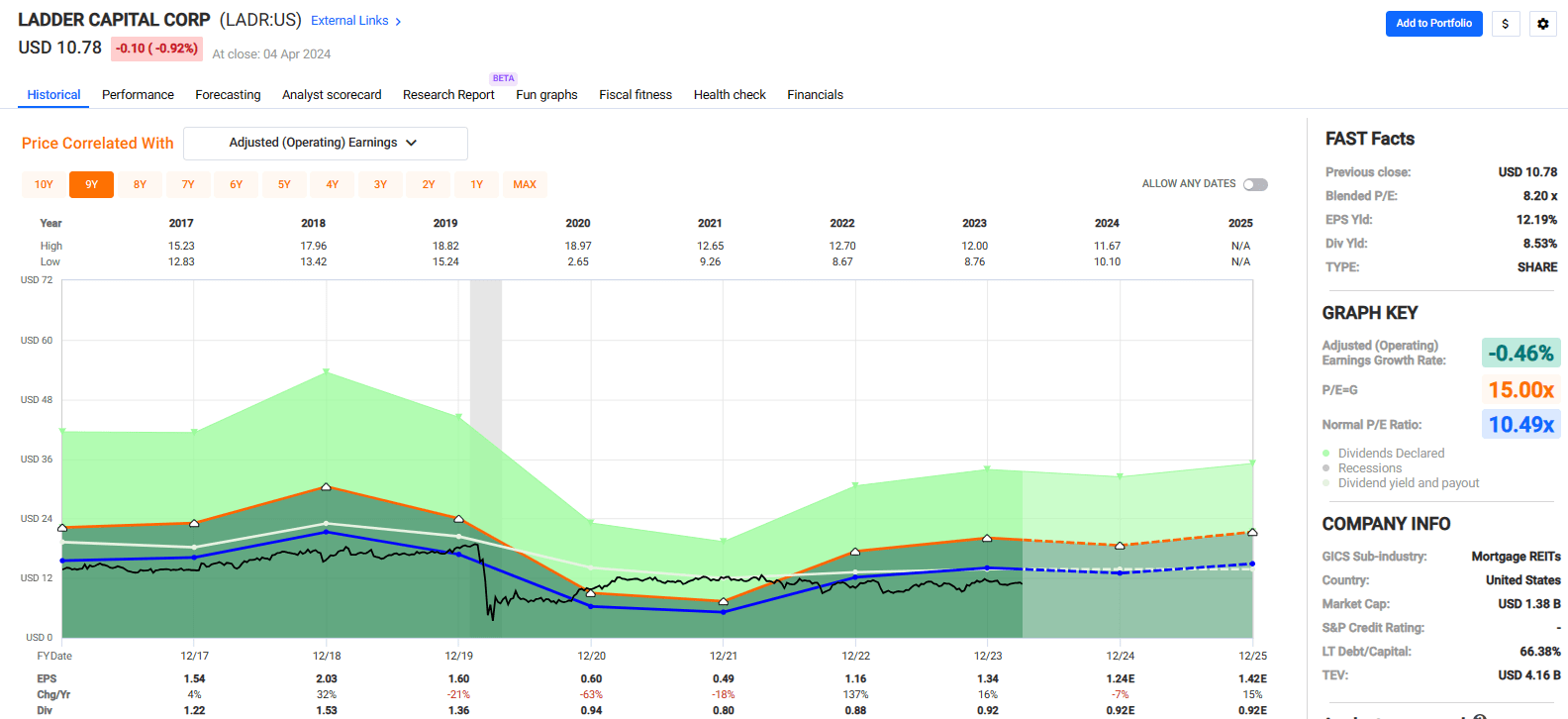

Ladder Capital Corp (LADR)

This firm operates as an internally managed mortgage REIT that focuses on originating senior first mortgage loans with fastened or variable rates of interest which might be backed by industrial actual property (“CRE”).

Along with its core enterprise of mortgage origination, the corporate acquires possession curiosity in web leased industrial properties and invests in debt securities which might be investment-grade and secured by industrial actual property.

LADR has a market cap of roughly $1.4 billion and a $3.1 billion mortgage portfolio that’s primarily made up of senior secured first mortgage loans, which account for greater than 99% of its mortgage portfolio. Moreover, the corporate takes a conservative method in lending as they don’t concern development loans and have a portfolio with a W.A. loan-to-value (“LTV”) ratio of 66%.

The corporate had a complete asset base of $5.6 billion on the finish of 2023 which consisted of $3.1 billion in CRE loans, $947.0 million in CRE fairness investments, 486.0 million of CRE securities, and over $1.0 billion in money.

As a part of its lending operations LADR originates conduit loans that are then pooled and securitized and offered as industrial mortgage-backed securities (“CMBS”). The corporate’s $3.1 billion mortgage portfolio consists of $3,123 million in stability sheet first mortgage loans and $27 million in conduit first mortgage loans.

By property sort, 37% of the corporate mortgage portfolio is secured by multifamily properties, 28% is secured by workplace, and 18% is secured by mixed-use properties. Along with its 3 largest classes, the corporate additionally has loans secured by retail, resort, and industrial properties.

The mortgage REIT isn’t investment-grade and is junk rated by S&P World with a credit standing of BB-. It focuses on financing its operations with long-term debt that’s unsecured, non-recourse, and non-mark-to-market.

41% of the corporate’s debt consists of unsecured company bonds and LADR reported a complete leverage ratio of two.5x as of the tip of 2023.

Since 2017 LADR has had a median adjusted working earnings development charge of -0.46%. Analysts anticipate earnings per share (“EPS”) to fall by -7% in 2024, however then return to development the next yr with EPS development estimates of +15% in 2025.

The inventory pays an 8.53% dividend yield and trades at a P/E of 8.20x, in comparison with its common P/E ratio of 10.49x.

We charge Ladder Capital Corp a Purchase.

FAST Graphs

In Closing

In Males’s faculty basketball, the Ultimate 4 is on Saturday (April 6) with NC State matching up in opposition to Purdue and Alabama set to play UConn. The finals will probably be held on Monday (April 8).

At this level, my favourite is NC State.

SportingNews has Purdue successful by 6 factors, however I’ve at all times appreciated Cinderella tales, so I am rooting for the Wolfpack. UConn seems robust, as at all times, so I am pretty assured we’ll see the Huskies within the finals on Monday evening.

As at all times, thanks for studying and commenting. I look ahead to listening to your ideas on March Insanity beneath.