EvgeniyShkolenko/iStock by way of Getty Pictures

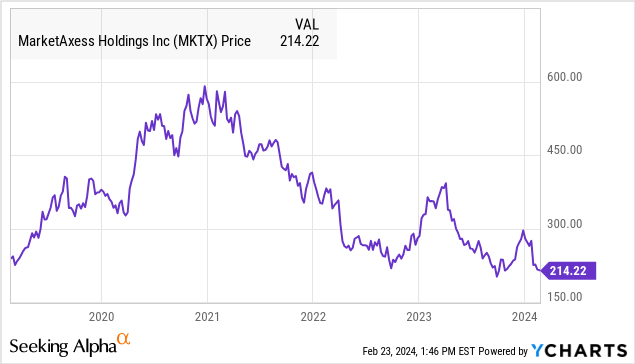

MarketAxess Holdings Inc. (NASDAQ:MKTX) reported its This fall earnings which beat estimates though it wasn’t sufficient to stem a pointy selloff in shares which are down greater than 25% YTD and at present close to a five-year low.

We final coated the inventory again in early 2022 citing what was then anticipated to be a “transitional year” for progress which seems to have uncovered some deeper structural challenges. As we see it, the story right here for the institutional-level fixed-income buying and selling platform has been an ongoing reset of expectations in comparison with what was possible exuberance throughout a pandemic-era increase.

Latest information suggesting a decline in market share and in any other case delicate profitability have labored to strain sentiment towards the inventory. The issue with MKTX in our opinion is that shares sit in a grey space as not fairly delivering distinctive progress whereas additionally falling in need of compelling worth. We anticipate the volatility to proceed.

MKTX Earnings Recap

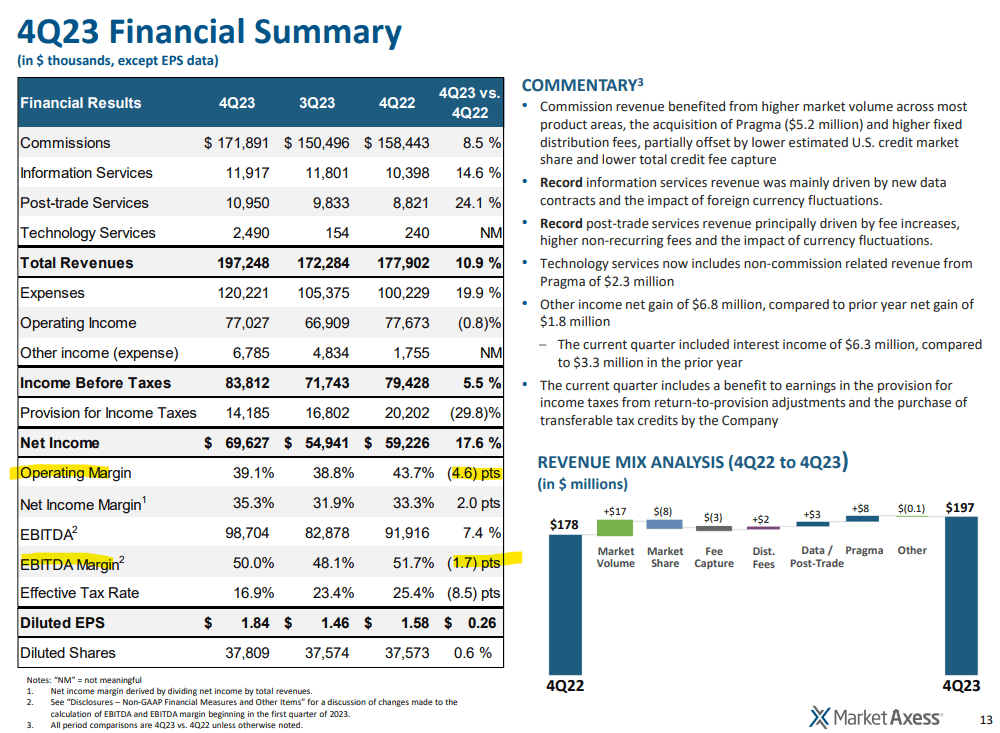

MKTX Q4 EPS of $1.84 was $0.12 above the consensus and in addition up 16% year-over-year. Income of $197 million climbed by 11% y/y benefiting from an ongoing worldwide enlargement in addition to momentum from smaller segments like data companies, post-trade analytics, and the expertise group.

Alternatively, the core commerce charge income progress of 8.5% in This fall, or 3.4% for the total yr stands in distinction to the height 37% progress achieved in 2020.

Needless to say the outcomes this quarter additionally included an $8 million income contribution from the 2023 acquisition of “Pragma” as algorithmic buying and selling and AI-powered execution answer. By this measure, the “organic” progress this quarter was nearer to six% y/y.

supply: firm IR

So whereas the top-line momentum has at the least rebounded in comparison with a weaker 2022, the opposite facet to the equation has been an ongoing enhance in whole bills, up 20% y/y in This fall.

The hassle to spend in the direction of progress together with including headcount in addition to on the R&D facet is mirrored in a decrease working margin of 39.1% in This fall, down from 43.7% within the interval final yr. Equally, the EBITDA margin can be decrease.

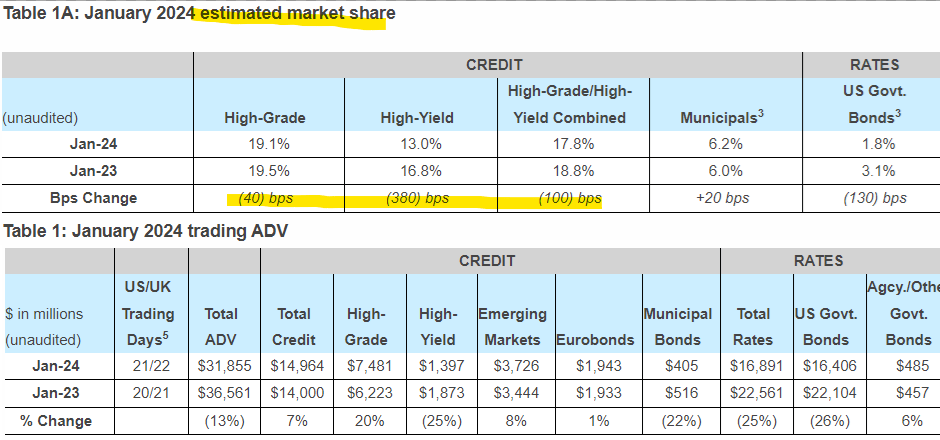

In trying to know the continuing inventory value weak spot, the metric that stands out to us is the decline in market share with the monthly update for January into Q1 2024 displaying an ongoing contraction. Inside credit score buying and selling, high-grade and high-yield market share mixed at 17.8% is down from 18.8% within the month final yr.

Administration is focusing extra on “record” whole common day by day quantity inside credit score as a key market phase reaching $15.0 billion, up 6.9% though the ADV for different segments is down.

supply: firm IR

The corporate believes that tighter credit score spreads and diminished general market volatility clarify among the drop, with an expectation that an eventual Fed charge minimize will assist enhance the market backdrop.

When it comes to 2024 steerage, MarketAxess is concentrating on full-year 2024 income progress of round 12% which features a “mid-single digits” contribution from Prama. An estimate of whole bills of round $490 million for 2024, if confirmed, would signify a 12% enhance y/y implying in any other case flat margins in opposition to related progress.

supply: firm IR

What’s Subsequent For MKTX?

Our takeaway when MKTX is that the corporate is basically sound with the current operational and monetary turbulence roughly reflecting rising pains in what stays a fast-moving market phase.

On the identical time, it’s value wanting again at among the expectations the share value carried when the inventory traded as excessive as $600 in late 2020 when the platform was seen as “disruptive” or a sport changer in comparison with the trade stand the place bonds, loans, and credit score securities are historically traded over the cellphone.

For context, the full market cap of credit score buying and selling with information from January at 17.8% is down from as excessive as 19.5% in 2020. Any expectation that the corporate would attain a stage above 30% or past seems more and more unlikely within the foreseeable future. There’s additionally a way that the aggressive panorama has labored to strain charges and a headwind on profitability.

Gamers on this phase embody Tradeweb Markets Inc. (TW), in addition to “Bloomberg” and S&P World Inc. (SPGI) which every over alternate options with strengths and weaknesses in sure classes. Our interpretation is that the trade has moved to implement lots of the options that made MarketAxess stand out 4 or 5 years in the past.

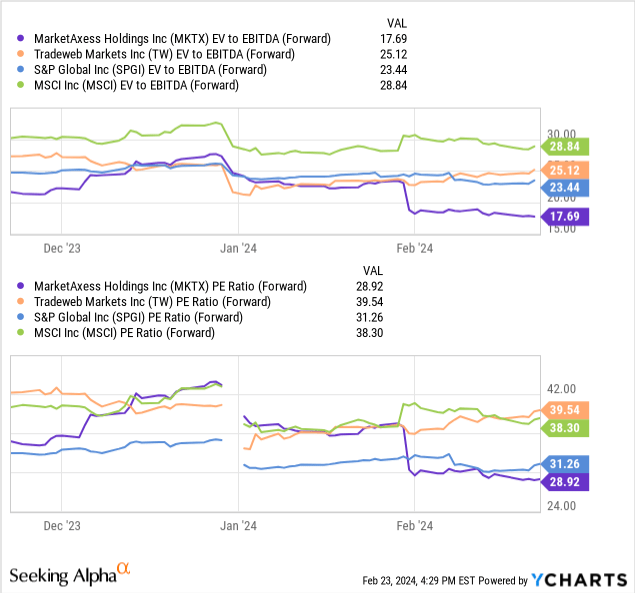

Shares buying and selling at an 18x EV to ahead EBITDA a number of or 29x ahead P/E are at a reduction to Tradeweb and SPGI, as a monetary information chief, which we imagine is justified given the current traits.

The bullish case for MKTX is that the corporate can handle a re-acceleration of natural progress whereas additionally displaying indicators of stabilizing or gaining market share. The chance is that the information continues to underperform and the inventory might face a re-pricing decrease because the market reassesses the long-term alternative.

Closing Ideas

2024 shall be a essential yr for MarketAxess to ship a turnaround with a watch on monetary effectivity and stronger working momentum. The excellent news is that the corporate stays worthwhile with in any other case stable free money circulation that at the least buys it time to make the platform work.

Whereas leaning bearish, we’ll charge shares as a maintain, balancing what we imagine to be ongoing challenges whereas additionally recognizing that the steep selloff has possible already included lots of the negatives. A break within the inventory under $200 would sign a extra regarding deterioration of the outlook that shareholders ought to control. Our base case is for volatility to proceed.