Fed Chair Powell’s Jackson Hole speech on Friday was enough to keep the hopes of a 50bp cut(s) alive.

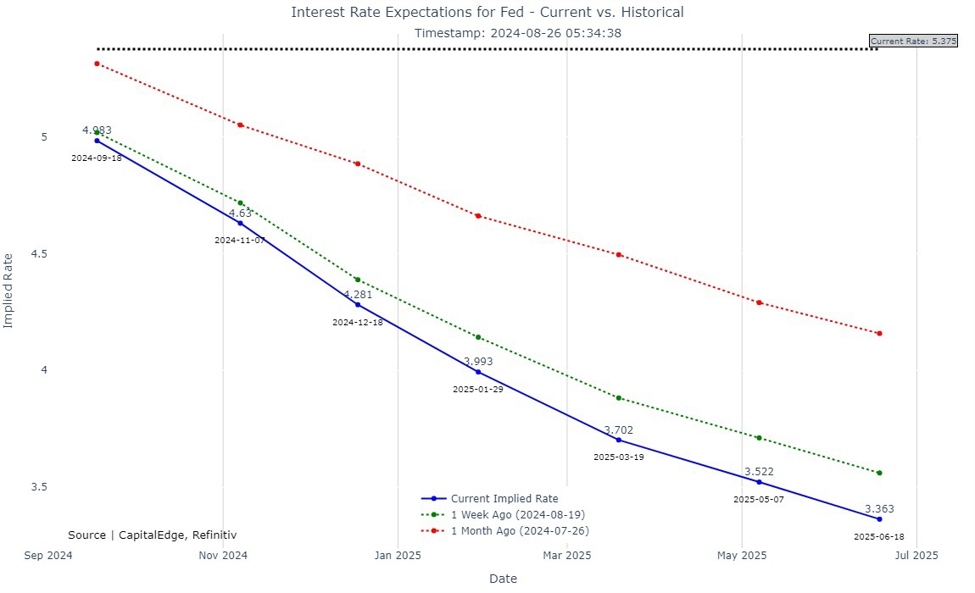

We’ve seen the implied rate path push lower following Friday’s speech, with money markets pricing in close to 200bp of cuts by July next year.

Fed implied rate path

Given the current state of US economic data this view seems too aggressive in my opinion.

Even talking about 50bp cuts when Q2 GDP is close to 3% doesn’t make much sense, but with all the focus turning to the labour market, the bets for whether we get any 50bp cuts this year will largely be based on the remaining NFP prints.

Throughout 2022-2023 markets were gauging how big the Fed hikes based on incoming CPI data, and now the market will gauge how big the Fed cuts based on incoming NFP data.

That means next job’s data will be the deciding factor for whether we get a 25bp or 50bp cut at the September meeting.