Torsten Asmus/iStock via Getty Images

Elevator Pitch

My investment rating for Marubeni Corporation (OTCPK:MARUY) (OTCPK:MARUF) [8002:JP] is a Buy.

Previously, I outlined potential catalysts for Marubeni Corporation relating to better-than-expected shareholder capital return and higher-than-expected earnings in my prior update published on March 14, 2024.

This latest article touches on MARUY’s recent acquisition, and provides an update on the company’s shareholder return. I have chosen to stay bullish on Marubeni Corporation with a Buy rating. Marubeni Corporation’s latest purchase of a brand management business bodes well for its Lifestyle business segment’s growth outlook, as this will provide MARUY with a platform to acquire other brands. Also, the company is expected to distribute a bigger percentage of its earnings as share repurchases and dividends in the future, considering its guidance and management commentary.

Readers can deal in Marubeni Corporation’s shares on the Tokyo Stock Exchange and the OTC or Over-The-Counter market. The company’s OTC shares and Japanese shares boasted average daily trading values of $1 million and $100 million (source: S&P Capital IQ), respectively, in the last three months. Investors can buy or sell Marubeni Corporation’s Japan-listed shares with US brokerages like Interactive Brokers.

Recent M&A Deal Has Positive Read-Throughs For Lifestyle Business’ Growth Prospects

Seeking Alpha News reported in the earlier part of this month that Marubeni Corporation’s 100%-owned subsidiary Marubeni Growth Capital US bought over “RG Barry Brands, a multi-brand management platform”, which has brands like Dearfoams and Baggallini.

In its June 10, 2024 press release, Marubeni Corporation highlighted that this latest acquisition of a “lifestyle brand management business” is the company’s “first investment in the consumer sector in the U.S.” and is aligned with its “aim of building businesses that will become new pillars of Marubeni in 2030.”

MARUY’s Lifestyle business segment accounted for 2.1% of the company’s FY 2024 (YE March 31, 2024) net income, and the company projects that the Lifestyle business segment’s earnings contribution as a proportion of its total net profit will increase to 2.3% in FY 2025. The Lifestyle business has a long growth runway ahead, as the bottom-line contribution from this segment is still small with ample room for further growth.

More importantly, the Lifestyle business segment is a key area of focus for the company, as seen with its recent management commentary. At the company’s recent Q4 FY 2024 analyst call last month, Marubeni Corporation emphasized that “we want to develop a solid business pillar for the Lifestyle Division” when it was asked about “businesses with major room for improvement.”

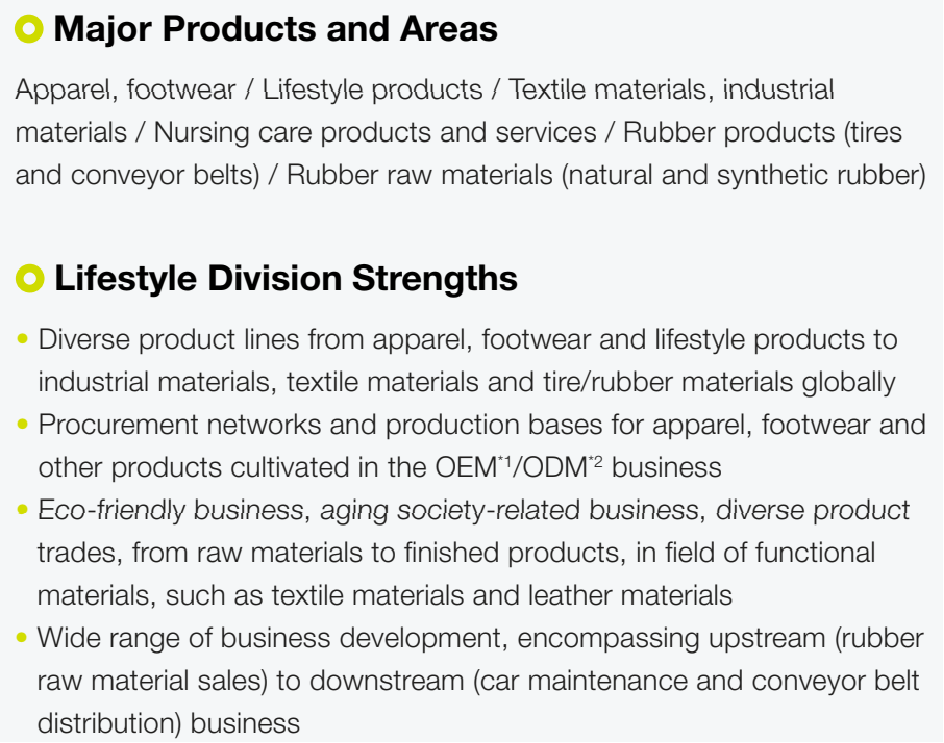

A Description Of Marubeni Corporation’s Lifestyle Business Segment

Marubeni Corporation’s 2023 Integrated Report

There are synergies between Marubeni Corporation’s Lifestyle business segment and the newly acquired brand management business RG Barry. Dearfoams (slippers) and Baggallini (bags) are apparel brands. MARUY has an existing Asian apparel business known as “Marubeni Fashion Link” which is engaged in the “manufacturing and sale of apparel and goods” as indicated in its 2023 Integrated Report.

It is realistic to think that MARUY’s Lifestyle segment will become a key growth business for the future with rising earnings contribution over time, as the company utilizes RG Barry as a platform to execute on further acquisitions. RG Barry cited Marubeni Growth Capital US President’s comments in its June 10 media release indicating that MARUY is looking to “add additional brands under the RGB (RG Barry) umbrella.”

In a nutshell, Marubeni Corporation’s recent M&A transaction with RG Barry has favorable read-throughs for the long-term growth prospects of its Lifestyle business segment and the company as a whole.

Positive Update On Shareholder Capital Return Outlook

With my previous mid-March 2024 write-up, I mentioned that Marubeni Corporation “has the potential to pay out a larger proportion of its net profit as dividends and also allocate more capital to buybacks.” It is encouraging to note that there have been positive developments pertaining to MARUY’s shareholder capital return.

As indicated in its FY 2024 results presentation slides, the company is guiding for a +5.9% increase in its dividend per share to JPY90 in FY 2025. This implies that Marubeni Corporation’s dividend payout ratio is expected to rise from 30.3% in the prior fiscal year to 31.3% for the current fiscal year.

Marubeni Corporation also set its full-year FY 2025 target for share repurchases at JPY50 billion. As a comparison, the company allocated a much lower JPY20 billion to share buybacks in FY 2024.

MARUY’s shareholder capital return guidance suggests that the company’s proportion of capital returned (dividends and buybacks) as a percentage of earnings could potentially increase from 34.5% for FY 2024 to 41.7% in FY 2025.

At its Q4 FY 2024 results briefing in May, Marubeni Corporation stressed that even though “our shareholder return policy targets a range of around 30%–35%, we are aware that investors have expectations for it to rise closer to 40%.” MARUY also added at the most recent quarterly earnings call that it “will have to shift to 40% due to pressure from the market” going forward, and noted that this is achievable after “we took a good look at the (company’s financial) figures.”

In summary, MARUY’s current capital return policy states that the company will distribute between 30% and 35% of its earnings as buybacks and dividends every year. But Marubeni Corporation’s FY 2025 guidance already points to a 41.7% total capital payout ratio, so the company is likely to formally raise its capital payout ratio to 40% or better in time to come.

Key Risk Factors

The major downside risks for Marubeni Corporation are related to the company’s capital allocation.

Investing in brands with poor prospects or overpaying for the brand acquisitions will hurt MARUY’s future performance. This is a key downside risk for the stock.

Another downside risk pertaining to Marubeni Corporation is that the company doesn’t change its shareholder return policy involving a higher total capital payout ratio.

Final Thoughts

Marubeni Corporation is deserving of a Buy rating based on my updated valuation analysis.

In my December 13, 2023 initiation piece, I noted that a fair “P/B ratio is derived by dividing [ROE minus the Perpetuity Growth Rate] by [Cost Of Equity minus the Perpetuity Growth Rate]” as per the “Gordon Growth Model.” My prior assumptions were “a 15% ROE, a 10% Cost of Equity, and a 0% Perpetuity Growth Rate.”

My updated assumptions are a 15% ROE (unchanged), a 9% Cost of Equity and a 2% Perpetuity Growth Rate. I have raised my Perpetuity Growth Rate assumption, taking into account MARUY’s latest growth initiatives like acquiring RG Barry. At the same time, I have lowered my Cost of Equity assumption to reflect a lower discount rate justified by the company’s improved capital return outlook.

My new target P/B multiple is 1.86 times, and this is 30% higher than Marubeni Corporation’s current trailing P/B ratio of 1.43 times (source: S&P Capital IQ). The undervaluation of Marubeni Corporation’s shares supports my Buy rating.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.