Morsa Photos

Funding abstract

My advice for Marvell Know-how (NASDAQ:MRVL) is a purchase ranking. I consider the worst of the cycle is over for MRVL, and it ought to begin to enter the upcycle as early as 2H25, which ought to drive sturdy development acceleration in FY26. Over the long run, I’m additionally bullish on MRVL’s capacity to proceed rising its information heart enterprise, because it has a number one place within the 800g PAM4 optics resolution, which has been a key driver in its capacity to win extra AI offers.

Enterprise Overview

MRVL is a provider of a variety of semiconductor-related expertise, equivalent to controllers for arduous disk drives (HDDs) and solid-state drives (SSDs), Ethernet switches, processors, and ASICs for information facilities, and so on. MRVL additionally develops built-in {hardware} platforms together with software program that comes with digital computing applied sciences designed and configured to supply an optimized computing resolution. Like many firms within the semiconductor business, financials have been cyclical, going by way of three cycles over the previous 10 years (the newest downcycle began in FY24). In every down interval, income declined sharply, with the EBIT margin going unfavorable. Within the latest quarter, MRVL reported 4Q24 income of $1.43 billion, the place Knowledge Heart reported income of $765 million, Provider Infrastructure reported income of $170 million, Enterprise Networking reported income of $265 million, Shopper reported income of $144 million, and Auto/Industrial reported income of $82 million. Complete income noticed development of 1% sequentially and yearly, offering hopes for a turnaround in FY25. Adj gross margin additionally noticed constructive acceleration by 330 bps sequentially to 63.9%, with EBIT margin enhancing from 33.1% to 33.8%.

Cloud infrastructure is driving long-term development.

I take the 4Q24 sequential and annual income and revenue development as a constructive indication that the worst is over for this downcycle, and therefore, my focus is on the drivers that can help MRVL’s development within the subsequent upcycle and over the long run. The primary secular tailwind I see in the present day is cloud infrastructure and AI, or, in different phrases, MRVL’s Knowledge Heart enterprise, which has proven great resilience and efficiency in 4Q23, rising 38% sequentially and 54% yearly to $765 million. AI was a key driver within the quarter, led by MRVL’s leading position within the 800G PAM4 resolution, which I anticipate to proceed inserting MRVL’s in a superb place to compete for offers. There are a number of seen development catalysts that help sturdy efficiency within the subsequent 1 or 2 years (notice that each one these will solely begin contributing revenues on the finish of FY25, organising a superb base for FY26):

- The subsequent technology of 200G per lane and 1.6T PAM4 options from MRVL have began to be certified by clients, and first deployments are anticipated to start by the tip of this yr, in response to administration.

- Moreover, the administration plans to extend the implementation of PAM4 DSPs for AECs and anticipates delivery merchandise to numerous Tier 1 cloud clients this yr.

- The subsequent-generation 51.2T change from MRVL is predicted to be shipped later this yr.

- Administration additionally expects to see a constructive uplift from elevated funding in inferencing. Notably, MRVL is experiencing excessive demand for its 800G DCI merchandise, the following technology, and is presently delivery 400G DCI merchandise in massive portions. And with the growth in DCI buyer base with design wins at a number of information heart clients, income contribution from the 800G DCI merchandise will solely doubtless ramp up subsequent yr.

One other method to get a way of the expansion runway for MRVL within the AI house is that AI is at present on the degree of “more than 10%” of FY24 income, up from 3% in FY23. In simply 1 yr, the income combine greater than tripled and has a run charge income of $800 million ($200 million in 4Q24), pushed largely by MRVL’s optics resolution. My view is that the necessity for AI is just not going to see any type of slowdown; in truth, I anticipate to see an acceleration transferring ahead as companies all over the world compete to have the most effective AI capabilities. To realize this, the spine (information storage and administration) should sustain on the similar tempo (or arguably at a quicker tempo to make sure additional growth is feasible). Therefore, I anticipate MRVL to proceed seeing long-term development in its information heart enterprise.

Marvell Know-how, Inc. a pacesetter in information infrastructure semiconductor options, in the present day introduced Spica Gen2-T, the business’s first 5nm 800 Gbps transmit-only PAM4 optical DSP. Designed for transmit retimed optical modules (TRO modules), Spica Gen2-T can cut back the facility consumption of 800 Gbps optical modules by greater than 40percent1 whereas sustaining interoperability with standard optical modules and IEEE 802.3 compliant host gadgets. MRVL

Other than AI and information facilities, I’m additionally optimistic about MRVL’s cloud customized silicon enterprise, the place MRVL is beginning to ramp for 2 buyer wins (expects preliminary shipments in 1Q25) and can exceed the $800 million goal run charge by the tip of CY2024. There ought to be no points for MRVL to hit this provided that these designs are on monitor for a considerable ramp in 2H25 and administration has a transparent view of demand for each FY25 and FY26.

Different enterprise outlook

As for the remainder of the enterprise, whereas the 1Q25 steering suggests very dangerous efficiency, I took it very positively. Administration guided for enterprise networking to be down 40% sequentially (1Q25 to be ~58% beneath peak); provider to be down 50% sequentially (1Q25 to be ~73% beneath peak); and shopper to be down 70% sequentially (1Q25 to be 74% beneath peak). For reference, these anticipated declines are the larger sequential decline that MRVL is predicted to see over the previous 4 years, which tells me the unfavorable demand/provide state of affairs is coming to an finish, and MRVL ought to see a powerful restoration in demand quickly. One good information level of a turnaround is that storage has already began to see a powerful restoration.

We additionally benefited from larger sequential demand for our storage merchandise as that portion of our information heart finish market continues its restoration. Income from our Teralynx Ethernet switches additionally grew sequentially within the quarter. 4Q24

Valuation

Redfox Capital Concepts

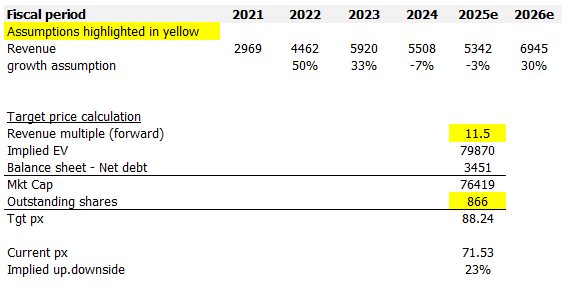

I mannequin MRVL utilizing a ahead income a number of strategy, and utilizing my assumptions, I consider MRVL is price $86.34. In my view, MRVL goes to see huge development acceleration forward because it goes into the following upcycle, largely doubtless in FY26, as FY25 continues to be going to see lingering impacts from the downcycle in a few of the enterprise items in 1Q25 (as talked about above). It’s arduous to pinpoint the precise restoration trajectory, however my assumption is that FY25 will see a 3% decline, which is a decline of a small magnitude (2H25 begins to see some type of restoration, offset by the weak efficiency in 1Q25). FY26 ought to see a powerful acceleration, which I estimate to be ~30% primarily based on the common previous few cycles efficiency (FY11 noticed 28% development, FY19 noticed 19% development, FY22 noticed 50% development). In an upcycle, MRVL ought to commerce at an elevated a number of given the stronger development charges. On the present 11.5x ahead income a number of, that is ~2.5x off the height in FY21 and ~3x above the common. My considering is that multiples might surge to the earlier peak if MRVL reveals stronger than anticipated development, however I feel the present 11.5x higher displays my 30% development expectation as consensus is anticipating the identical too (FY25 development of 29.9%).

Threat

Though I anticipate a restoration within the close to time period, the precise timing of the inflection and the tempo of restoration shall be troublesome to pinpoint. Whereas historic information factors do assist in forecasting, they aren’t assured to be correct. MRVL might very properly see a number of extra quarters of slowdown, particularly if the worldwide macroeconomy sees additional pressure from charges staying larger for longer, growing the price of capital for companies, thereby restraining funds capability for investments.

Conclusion

My view for MRVL is a purchase ranking. MRVL seems to be nearing the tip of the present downcycle, and I anticipate MRVL’s main place to proceed positioning it properly to capitalize on the long-term development in AI and cloud computing (the Knowledge Heart enterprise). Whereas the near-term outlook for some enterprise items stays weak, I’d anticipate a powerful rebound within the latter half of FY25. The chance lies within the actual timing and tempo of the restoration, which might be impacted by macroeconomic components.