Nikada

Dear Friends and Investors,

During the second quarter of 2025, the Massif Capital Real Assets Strategy returned 6.2% net of fees, with gross-of- fees gains from the long book of 9.8% and short book losses of 3.3%. Since the end of the second quarter, the portfolio has trended positively. At the time of writing (Wednesday, July 23), the portfolio is up a further 9.2%, bringing our YTD results to up 16.5%.

Top Five Returning Positions During the 2nd Quarter

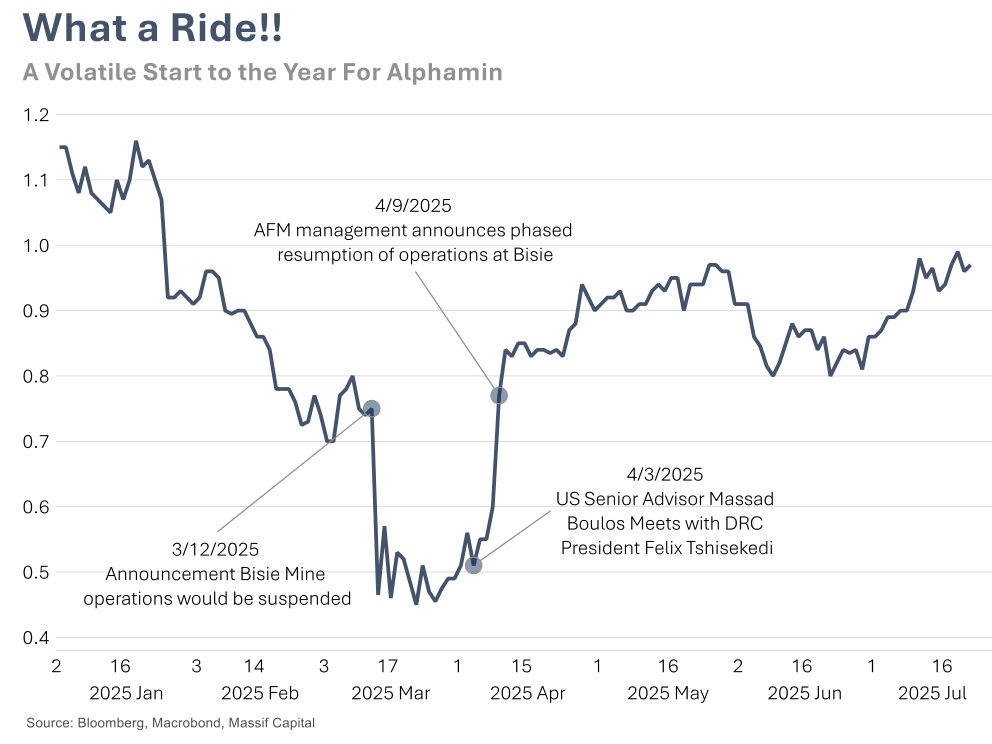

Although Alphamin was our best-performing position during the second quarter (up 68%), we will forgo in-depth analysis. As we explained in our first-quarter letter, the stock sold off due to a temporary shutdown of operations in the context of an ongoing conflict in the DRC. We also discussed our thesis and valuation of Alphamin (OTCPK:AFMJF) extensively in a report published on April 9th.1 It is worth noting that, despite temporary operational interruptions, the quarter ended with contained tin production of 4,106 tonnes, which is below the targeted quarterly production of 5,000 tonnes but only 4% below the first quarter’s production. Output in May and June was in line with the annual target of 20,000 tonnes. The processing facilities performed well and above target – overall plant recoveries averaged 77% during the quarter (Q1: 75%).

The average tin price achieved was in line with the prior quarter at US$32,512/t – the tin price is currently trading around US$33,000/32,000. Q2 2025 AISC per tonne of tin sold was estimated at US$16,500 (Q1: US$16,279), which is higher than under normal operating conditions due to the impact of the operational stop and subsequent restart. Still, even if we did not know about the operational interruptions, we would not have thought twice about that move in the AISC and would be pleased with the quarter.

Management has released EBITDA guidance for 2Q 2025 of US$75 mil, 21% higher than the previous quarter’s actual of US$62m as a result of additional tin sales during 2Q 2025, which included clearing of the backlog of deliveries experienced during the prior quarter. The Company has a robust US$110 million in cash with a Net Cash position of US$50 million. We await further information from management about the dividend, but are not concerned. Pausing the payment during operational interruptions made sense, and now that the mine is back up and running, we fully expect the dividend to be reinstated.

We remain convinced that Alphamin is well-positioned for the next decade. Currently, our database of mining projects comprises 39 different tin deposits at various stages of production or development globally. Of the 39, 24 are either grassroots exploration or drilling targets, which means they are still being validated for the existence of economic deposits. Seven of the projects are either in a prefeasibility stage or are currently developing feasibility studies, so they are at best three to five years away from production. We are not aware of any projects currently under construction. Within this context, tin demand is growing at a rate of 2% to 3% per annum, while supply is expected to increase at a rate of roughly 1% per annum at best. We are skeptical of even that level of supply growth given declining grades in existing mines (besides Alphamin’s) and political challenges in critical producing countries like Myanmar.

Our second-best performing position was our unfortunately undersized investment in Chemring (OTCPK:CMGMF), a UK-based defense contractor in which we initiated a position during the first quarter.2 Chemring was up 49% during the second quarter. Currently, the firm is within roughly 25% of our target price. We began building a position with the intention of increasing it to 6% to 8% over the course of the year, but the market quickly recognized the underpriced nature of this manufacturer of “energetics” (explosives) and electronic warfare kits.

We are still assessing the path forward for this position. We are carefully evaluating the possibility that we may have underappreciated this company’s potential, given that EU defense spending is set to rise by more than €100 billion by 2027, and the UK is targeting 2.5% of GDP. Chemring’s positioning in niche market areas, including energetics and electronic warfare, creates a potentially solid investment case for the multi-decade rearmament cycle.

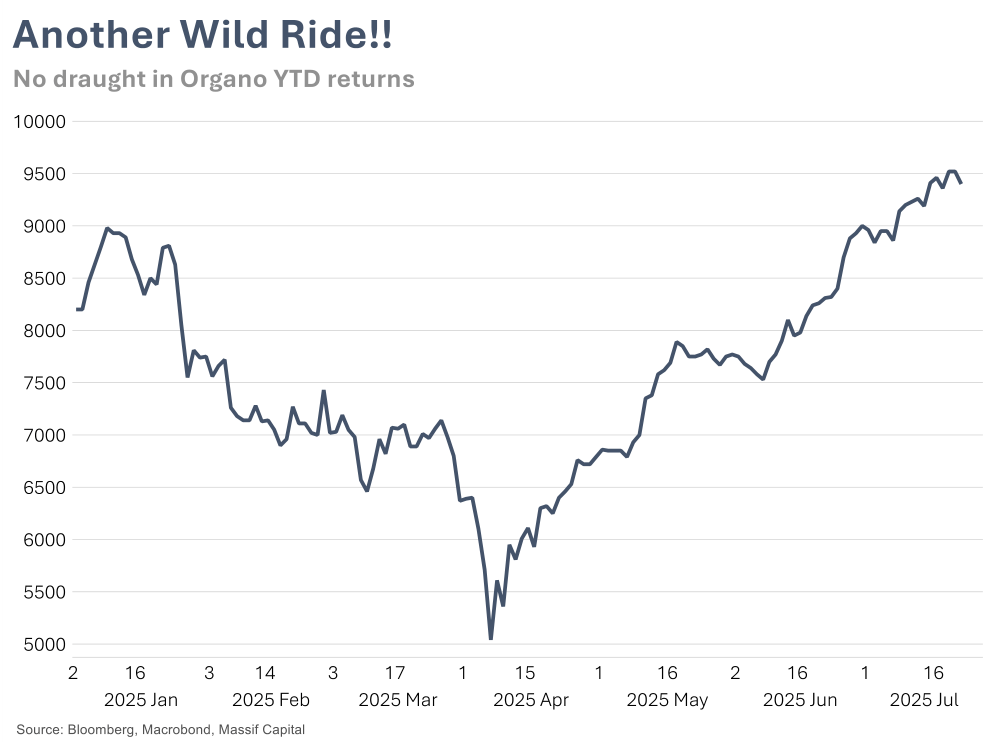

Within the context of the EU defense landscape, Chemring’s specialist energetics capabilities are in high demand. The group holds a duopoly with France’s state-owned Eurenco in European advanced high explosives. As is the case with Alphamin, being one of a few producers of a highly sought-after product is always a good position to be in. This thought process leads us to our third-best-performing stock of the 2nd quarter, Oragano, another firm we initiated a position in during the first quarter, only to see it appreciate significantly during the second quarter.

Oragano, much like Chemring, is undersized in the portfolio, and while not operating in a duopoly, it operates in a segment of the water market that is functionally a triopoly. We initiated a position before the tariff announcement, after which it sold off 30%, a sell-off we took advantage of. However, the stock rapidly turned, like much of the rest of the market, and rallied in roughly a straight line, gaining 87%. As a reminder, Oragano is one of three companies globally that specializes in the manufacture and operation of facilities for the production of Ultra-Pure Water, a type of water so pure that impurities in an Olympic swimming pool of the stuff would be less than a teaspoon.3 Oregano specializes in equipment for purifying water used in semiconductor manufacturing and is the sole supplier of water purification equipment for TSMC.

Unlike Chemring, for which we feel confident in evaluating the future, we are less confident in our ability to assess Organo’s future from here. Much like the Uranium industry, in which we have watched the market for more than a decade and done very little, but invested successfully (have made four investments, with three successful exits and one yet to be resolved situation), we have followed the water industry for a while but find very few opportunities. We have not followed the semiconductor industry in the same way, and Organo at these prices is a second derivative semiconductor opportunity. While the value of Organo at the time we initially bought the stock was obvious, all that was necessary was an accurate outlook on semiconductor demand.

At the current time, the stock is approaching a value that makes a precise and accurate read on the future of semiconductor manufacturing demand necessary, and we are less confident in our ability to make that kind of judgment call. As such, we have exited the position with a quick 34% return.

Our fourth-best-performing position is also our best-performing position of the year thus far, Enovix (ENVX), which was up 39% during the second quarter and has increased by a further 57% in the first 17 days of the third quarter. Unlike Organo and Chemring, Enovix is sized correctly in our portfolio, having built a position over the last two years at an average price of $6.98. The stock is now trading at approximately $14/$15 and is our largest position, accounting for 14% of the portfolio.

Enovix remains a volatile stock and a business that still has a few things to prove, so it could fall again, perhaps even more than once, before it reaches our probability-weighted value of $27. Still, we are confident that some of the initial operational growing pains are behind us. On July 7th, the firm released its AI-1 silicon anode smartphone battery platform. Enovix believes the 900WH/L capacity makes AI-1 the “highest energy density battery” commercially available on the market, complemented by fast charging (i.e., 50% in 15 minutes) and cycle rates of 900+ based on internal testing of initial units. Although we are aware of specialty batteries that have a higher energy density, specifically those from drone battery-focused producer Amprius (AMPX), we believe Enovix’s claim holds up for the most part. Most competitors are in a similar situation to Samsung (OTCPK:SSNLF), which has a road map for a 900 Wh/L cell phone battery but does not expect it to be available before 2027.

Although we believe the stock has appreciated somewhat on a positive read-through from incremental disclosure regarding battery specs, coupled with the earnings beat (which it seems investors care about, but in these early days is meaningless), we suspect that the stock’s rapid rise this time around has been facilitated in part by the unwinding of the firms persistently high short interest. The stock remains a favorite punching bag of the investing commentariat on twitter who are skeptical of everything from management’s ability to manufacture the battery to skepticism of the potential of a silicon anode, or just doubt about the willingness of anyone to pay a premium price for a more energy dense battery, we expect the first purchase orders later this year to a be key de-risking event for the final unwinding of the prominent short position, which was still 30% of the stocks float at the end of the 2nd quarter.

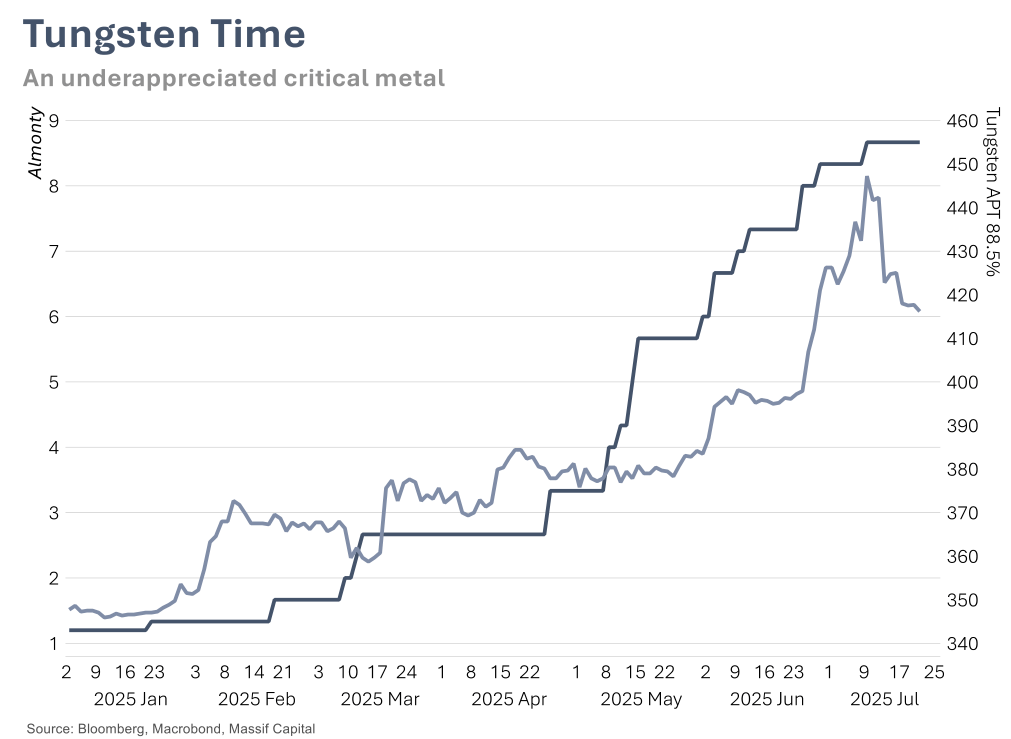

Rounding out our top five is a position in a yet-to-be-disclosed Tungsten miner, and no, it is not Almonty Industries (OTCQX:ALMTD), although we expect, in the fullness of time, a similar move in our investment. Fund investors are welcome to reach out to learn the name of the company. The investment was our first private investment at the time we started our position, the company is now public.

Tungsten is often described as one of the world’s most indispensable industrial metals. It reminds us a little of tin, critical to the economy, but generates no headlines comparable to those of rare earth minerals. We tend to believe that problems that attract attention, such as those related to rare earths, tend to get solved; issues that don’t attract attention rarely do. Tin and Tungsten shortages attract no attention; as such, they are unlikely to be solved. At the same time, unlike rare earths, which appear to require significant government involvement to create businesses that may not be sustainable without government support, our investments can generate profits in the market independently of government largesse.4

Tungsten’s value stems from a unique combination of physical and chemical qualities: it possesses the highest melting point of any metal, exceptional density, and remarkable hardness and durability. These characteristics explain why tungsten is essential for a vast range of applications in industries as diverse as defense, aerospace, electronics, energy, and manufacturing. Yet, despite this broad industrial necessity, tungsten is in short supply—a situation exacerbated by rising global demand and pronounced risks in its highly concentrated supply chain.

To understand why tungsten is considered critical, it is essential to examine its extraordinary physical properties and the degree to which modern industry relies on them. Its melting point (a staggering 3,422°C5 ) allows it to remain stable in environments where most metals would fail. Tungsten’s density is close to that of gold, and its hardness is exceeded only by diamonds when alloyed as tungsten carbide. This hardness makes it invaluable for cutting, drilling, and machining tools that must withstand relentless wear and extreme conditions, especially in manufacturing, mining, and petroleum industries. Tungsten’s resilience also makes it irreplaceable in the production of military and defense equipment, such as armor-piercing projectiles and kinetic energy penetrators. When choosing between materials, the military often selects tungsten for its penetrators—not only for its unrivaled density and strength, but also because it presents a safer and more environmentally acceptable alternative to depleted uranium.

Beyond defense, the aerospace industry relies on tungsten for critical components that must endure extreme heat and stress, such as rocket engine parts, counterweights for aircraft, and shielding for radiation. Its excellent electrical and thermal conductivity has made tungsten a staple in the electronics industry, where it is used in microprocessors, electrical contacts, filaments for lighting, and the fabrication of chips for advanced computing. Moreover, tungsten’s applications are expanding rapidly with the proliferation of electric vehicles, renewable energy technologies, and the relentless pace of high-tech manufacturing.

Despite the essential nature of these uses, global tungsten supply faces severe risks. The root of the problem is extreme geographic concentration—China alone is responsible for over 80% of global tungsten mine production and holds nearly 60% of known reserves. The robustness of the Chinese resource base is fading though, with mining quotas for 2025 cut by over 6%, reflecting diminished ore grades and a government push to conserve resources for high-tech domestic sectors. Other producers, such as Russia and Vietnam, along with a handful of Western countries, are minor by comparison; many potential mines remain undeveloped or have ceased operations due to economic or regulatory barriers. Most of the United States and Europe rely entirely on imports for their tungsten requirements. This lopsided distribution of supply gives one country disproportionate leverage over a resource vital to economic stability and national defense.

China has not hesitated to use its supply dominance strategically. In recent years, it has imposed tariffs and export restrictions on tungsten to prioritize domestic users and as part of broader geopolitical calculations. These controls have intensified trade tensions and compelled Western governments and manufacturers to search urgently for alternative suppliers and secure new sources of ore. Yet, developing new tungsten mining projects is both slow and costly. Regulatory challenges, environmental concerns, and economic uncertainties have delayed or stalled such efforts in countries beyond China, and recycling, while helpful, cannot provide enough supply to meet rising global demand.

The demand side is no less pressing. As new technologies proliferate—from the increased use of tungsten in electric vehicle batteries and precision automotive parts to its integration into high-performance electronics and renewable energy systems—requirements for the metal are surging. Modern militaries are also increasing their allocations for tungsten-based ammunition and components, responding to heightened security needs worldwide. At the same time, the manufacturing sector’s dependence on hard metal tools and robust wear-resistant parts continues to fuel demand.

With global output stuck in a handful of countries and most of the Western world dependent on a single supplier, tungsten’s supply chain is unusually fragile. Disruptions have already been felt from export controls, trade policy shifts, and supply chain bottlenecks. Recent logistical challenges, including pandemic-era closures and conflict in major mining regions such as Myanmar, have only exacerbated the scarcity. As a result, market prices for tungsten have experienced notable volatility, and manufacturers are finding themselves pressed to secure contracts and build stockpiles in anticipation of future shocks.

The growing demand combined with supply constraints has triggered a sharp increase in tungsten prices throughout 2025. Prices for key products—such as ammonium paratungstate (APT) and tungsten concentrates—are up more than 32%, reaching historic highs and causing downstream prices of tungsten carbide and alloys to surge as well.

Market liquidity remains low, with many buyers securing stockpiles or entering long-term contracts to hedge against ongoing uncertainty.

In response, Western governments and industries are accelerating efforts to diversify their sources. Policies such as the US REEShore Act and direct government grants for new mining projects are aimed at reducing dependency on China. However, true supply chain independence is hampered by slow mine development, limited refining capacity outside China, and the time required to build robust upstream and downstream infrastructure.

In sum, tungsten is not only a linchpin of modern industry but also a growing flashpoint in the politics of resource security. It’s rare combination of properties ensures it will remain pivotal to emerging technologies in defense, energy, transportation, and information systems. Unless new sources are developed and supply chains diversified, the risk of sustained shortages—and the attendant economic and strategic vulnerabilities—will remain high for years to come. The story of tungsten is, therefore, not just about the wonders of modern metalworking, but about the mounting challenge of securing the building blocks of 21st-century progress.

Our investment is a low-cost producer with assets located in friendly western countries, has a small producing asset (with expansion potential), and is developing a second asset. The firm also has an existing offtake agreement with the largest smelter of tungsten in the western world and a critical supplier for the US DOD.

Extended Discussion of Energy Investments

The portfolio is currently 25.8% invested in energy stocks, of which 100% are oil and natural gas producers. The vast majority of this investment is in three northern European oil and gas producers, two of which we have written reports on during the first half of the year (Var Energie (OTCPK:VARRY), with a TSR of 11.2% since publication, and Harbour Energy (OTCPK:PMOIF), with a TSR of -28.9% since publication). The other long-term holding is Equinor (EQNR); these three positions account for roughly 23% of the portfolio. The remainder of our energy exposure is to Iraq-focused E&P Gulf Keystone (OTCPK:GUKYF) (approximately 3% of the portfolio).

Harbour Energy and Var Energie both straddle the divide between high capital appreciation stocks and high dividend stocks. Both have an expected return from capital appreciation of at least 100%, and both currently offer dividend yields exceeding 10%. Equinor lacks the same punchy capital appreciation return. Still, with share buybacks executed at a price below our expectation of intrinsic value, a net cash balance sheet, a 4%-6% dividend yield, and a capital appreciation potential of more than 70%, it is well-deserving of a place in our portfolio.

The combined total shareholder return from oil and natural gas positions during the second quarter was 0.20%, with dividends contributing a positive 0.76% and capital depreciation offsetting the results. The vast majority of capital depreciation occurred from April 2nd to April 10th, after which the stocks rose throughout the second quarter to settle at roughly the same level as they started. YTD, this group of stocks remains down slightly, as even the war in the Middle East has not managed to save oil equities this year.

Our positions have generated a positive return for the portfolio YTD, despite the weak performance of the sector, with both price improvement and dividend returns across the board. The sole exception is Harbour Energy, which is one of our poorest performing positions YTD, down ~21%.

The current challenge for oil and natural gas equities remains a tension between long-term structural underinvestment and short-term economic headwinds. This creates a complex investment landscape where traditional valuation metrics break down, leaving investors grappling with conflicting signals about the sector’s future. While immediate economic headwinds suppress demand and sentiment, years of systematic underinvestment are creating conditions that will lead to future supply constraints and price volatility. To this mix is added geopolitical tensions. The tension has created a paradox where oil companies, especially those in the US with shorter cycle fracking operations, must simultaneously manage near-term cash flows and shareholder demands while potentially facing a supply crisis that could dramatically alter the industry’s economics.

This environment requires a nuanced approach that considers both the timing of economic cycles and the structural changes reshaping the global energy system. Trading into and out of stock based on such variables is as challenging as it gets. It is rarely done successfully, making the importance of the dividend to help blunt the significance of timing all the more crucial in our opinion. The sector’s future will likely be determined by how successfully companies and policymakers navigate this fundamental tension between short-term financial pressures and long-term energy security needs.

This challenging environment leads us to believe that domestic European producers deserve a premium for several structural, geopolitical, and market reasons. The challenges for the EU start with its near-complete dependency on imports to meet domestic demand. Leaving the European economy acutely exposed to external shocks, price volatility, and geopolitical leverage by suppliers.

Nor has the rapid pivot away from Russian oil after 2022 reduced overall dependency; it has merely shifted it to other suppliers, such as the US and the Middle East, often at a higher cost and with new logistical risks. To this, you add a patchwork of national and EU-level regulations, often with conflicting objectives. In a region facing extreme import dependency, chronic underinvestment, and rising geopolitical risks, the scarcity and flexibility of domestic oil and natural gas production command a justified premium in both market and policy terms. When stocks trade at a discount to their fundamental value and have a total shareholder return in excess of 10%, the decision to overweight exposure is even easier.

Our exposure is also very gassy. This is a choice as well. Like the global oil markets, European natural gas markets stand at a critical juncture in mid-2025, with significant structural shifts resulting from Russia’s invasion of Ukraine and the rapid adoption of renewable energy sources. The fundamental transformations currently underway create a stark contrast between the 2020-2025 period and the projected 2025-2030 timeframe. The earlier period was defined by crisis, emergency responses, and supply disruptions, while the latter will be characterized by either:

- A structural demand decline arising from the spread of renewable energy and systematic decarbonization, or

- A continued struggle to meet demand, in the presence of an energy transition that does not live up to expectations.

Once again, conflicting signals. Given the history of renewable energy supplanting hydrocarbons, especially in energy- intensive industrial applications, we will bet on the latter, not the former. The current European energy strategy hinges on the assumption that renewable energy deployment will successfully replace fossil fuels while maintaining grid stability and economic competitiveness. Emerging challenges suggest that this transition may face significant obstacles.

Our analysis indicates a generally bullish outlook for European natural gas prices over the medium term, characterized by price stability at heightened levels, driven by continued reliance on LNG imports amid declining domestic production and the cessation of Russian pipeline flows through Ukraine. Admittedly, this bullish sentiment is tempered by several bearish factors, including potential oversupply in global LNG markets post-2027, accelerating renewable energy deployment, and demand destruction in price-sensitive industrial sectors.

Within this context, the European gas market will continue to be characterized by weather patterns, geopolitical developments, and infrastructure constraints playing crucial roles in determining prices. LNG is likely to remain the marginal source of power supply, making Europe increasingly vulnerable to global market dynamics and competition from Asian buyers. Furthermore, the dependency on LNG makes domestic production all the more appealing, as LNG boosts the market’s clearing price.

As of mid-2025, the European Gas market remains in a state of tight balance, with LNG imports playing the crucial role in meeting demand. Following the cessation of Russian gas transit through Ukraine at the end of 2024, Europe has become even more dependent on LNG imports, which now account for approximately 43% of the region’s gas supply mix. This structural shift has fundamentally altered Europe’s gas security paradigm, making the continent more vulnerable to global LNG market dynamics. As LNG supply ramps up (starting this year and continuing through the end of the decade), the marginal price of gas in Europe is expected to decline. However, the level of global demand is sufficient to keep natural gas prices elevated relative to the pre-Russia/Ukraine war price paradigm.

At the same time, domestic production continues its inexorable decline, with output from the Netherlands and the UK falling faster than anticipated. Norway remains Europe’s most reliable pipeline supplier; however, production has plateaued and is expected to decline gradually after 2027. Meanwhile, pipeline imports from North Africa have remained relatively stable, though political instability in the region poses ongoing risks to supply security. The squeeze is just beginning, especially if economic activity in either Europe or Asia picks up, both of which will increase the cost of LNG.

While not all the natural gas challenges faced by the continent arise from electricity markets, many do, and the first quarter of 2025 demonstrated several concerning trends. The biggest challenge is the rush to electrify everything on a renewable-powered grid that faces significant intermittency challenges. The share of electricity generated from renewable sources in the EU fell to 42.5% from 46.8% in the same period in 2024, marking the first notable decline in recent years.6 This 4.3% drop signals the fragility of Europe’s energy transformation, particularly as hydroelectric power and wind farms experienced sharp declines, from 260.5 TWh to 218.5 TWh, year-over-year. At any moment, a massive amount of backup power is needed in Europe.

The loss in hydropower is as much a weather and climate-related issue as the loss of wind, but somewhat less concerning given its infrequency. At the same time, climate change issues are increasing the likelihood of water volume issues. Weather regime analysis also demonstrates that European wind power generation can vary significantly, with mean generation ranging from 22 GW to 44 GW, depending on atmospheric conditions.7 These fluctuations, which can last several days to weeks, are more challenging to address than short-term variations. In both cases, backup Natural Gas power is needed at a minimum.

Although problems of this nature can be addressed in multiple ways, Europe’s preferred response is likely battery storage. Unfortunately, the current 35 GWh of battery storage will need to increase to 780 GWh by 2030 and 1.8 TWh by 2040 to fully support the EU’s renewable energy system.8 The massive gap between current capacity and requirements suggests that storage solutions are unlikely to scale quickly enough to address renewable energy intermittency, making natural gas increasingly important.

Given the significant investment in natural gas infrastructure and LNG import capacity (currently, 16 new terminals are under construction) that Europe is making, we suspect that everyone is aware that renewables are likely to fall short, and a backup plan (natural gas) is needed. The Global Energy Monitor estimates that European countries are developing 248.7 billion cubic meters per year (bcm/y) of new LNG import capacity, as well as 16,491 kilometers (km) of new gas transmission pipelines, including several cross-border pipelines capable of importing a further 46 bcm/y of gas. One-fifth of the LNG capacity noted above is currently under construction, and one-tenth of the gas pipeline lines are also under construction. The expected cost of all this infrastructure is € 84.1 billion. This level of infrastructure investment leads us to believe that there will be robust demand for many years to come.

Orders for natural gas turbines similarly suggest that demand for natural gas in Europe has no end in sight. GE Vernova (GEV), Siemens (OTCPK:SIEGY) Energy, and Mitsubishi Power (OTCPK:MSBHF), who together serve over 75 percent of projects under construction. Booming demand for turbines has led each of these companies to report extended delivery timelines. Mitsubishi states that turbines ordered today will not be delivered until 2028–2030. Siemens reports a record backlog of €131 billion (approximately US$148 billion), with Europe accounting for 52% of Siemens’ Natural Gas business. And GE Vernova has announced that new turbines will not be available until late 2028 at the earliest.

Despite its renewable ambitions, natural gas remains essential for maintaining European grid stability and supporting the European economy. Gas-fired power plants offset fluctuations in wind and solar energy production, providing flexible power during periods when renewable energy sources cannot meet demand. Research indicates that including small amounts of dispatchable natural gas drastically reduces the cost of a renewable grid, with overall system costs falling by 31% when just 1% of total generation comes from natural gas.9 The ramp-up in LNG supply, especially in the context of a theoretically weak future Asian demand, might cause European natural gas prices to fall, but the long-term trend seems clear.

As always, we appreciate the trust and confidence you have shown in Massif Capital by investing with us. Should you have any questions or concerns, please do not hesitate to reach out.

Best Regards,

William M. Thomson

|

Opinions expressed herein by Massif Capital, LLC (Massif Capital) are not an investment recommendation and are not meant to be relied upon in investment decisions. Massif Capital’s opinions expressed herein address only select aspects of potential investment in securities of the companies mentioned and cannot be a substitute for comprehensive investment analysis. Any analysis presented herein is limited in scope, based on an incomplete set of information, and has limitations to its accuracy. Massif Capital recommends that potential and existing investors conduct thorough investment research of their own, including a detailed review of the companies’ regulatory filings, public statements, and competitors. Consulting a qualified investment adviser may be prudent. The information upon which this material is based and was obtained from sources believed to be reliable but has not been independently verified. Therefore, Massif Capital cannot guarantee its accuracy. Any opinions or estimates constitute Massif Capital’s best judgment as of the date of publication and are subject to change without notice. Massif Capital explicitly disclaims any liability that may arise from the use of this material; reliance upon information in this publication is at the sole discretion of the reader. Furthermore, under no circumstances is this publication an offer to sell or a solicitation to buy securities or services discussed herein. Footnotes 1 If you have bought AFM at the time we published our report, you would have a return of ~26%. 2 Chemring was an idea we found via Conor Maquire’s Value Situations substack. We think Conor’s work is excellent, his substack is worth the money. 3 We published a report on the Ultra-Pure Water equipment industry during the first quarter that can be found on our website: Thirsty for Returns. In that report, we noted that Organo was our favorite of the three primary producers of Ultra-Pure Water equipment; if you had bought the stock on our suggestion, you would have earned a return of 42%. 4 Note that we are not opposed to taking advantage of government support when offered, or investing in companies that benefit from it. Our current investment in Global Atomic (OTCQX:GLATF) is competing for a critical government loan, but the level of government involvement differs significantly from the DOD’s investment in MP Materials. As we noted recently in a historical review of US trade policy between the Revolutionary War and the Civil War, successful industrial policies must be temporary and performance- based, with clear metrics for success and include sunset provisions that prevent the creation of permanent dependence. The support for MP appears to lack all of the above. Link: From Colonial Grievances to Modern Industrial Strategy 5 For context, on re-entry, the surface of the now retired Space Shuttle reached temperatures of 1,600°C; steel smelting occurs at around 1,500°C; lava is between 700–1,200°C; the surface of the sun is roughly 5,500°C. If you dropped a cube of tungsten into a pool of liquid steel, the tungsten would remain a solid cube. 6 https://luxtoday.lu/en/technology-innovation-energy/the-share-of-electricity-from-renewable-sources-decreases-at-the- beginning-of-2025 8 https://api.solarpowereurope.org/uploads/Mission_Solar_2040_mr_V02_54b6a037a2.pdf 9 Natural Gas Peaking Plants: Types, Pros, & Cons | Diversegy |

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.