MattZ90/iStock through Getty Photographs

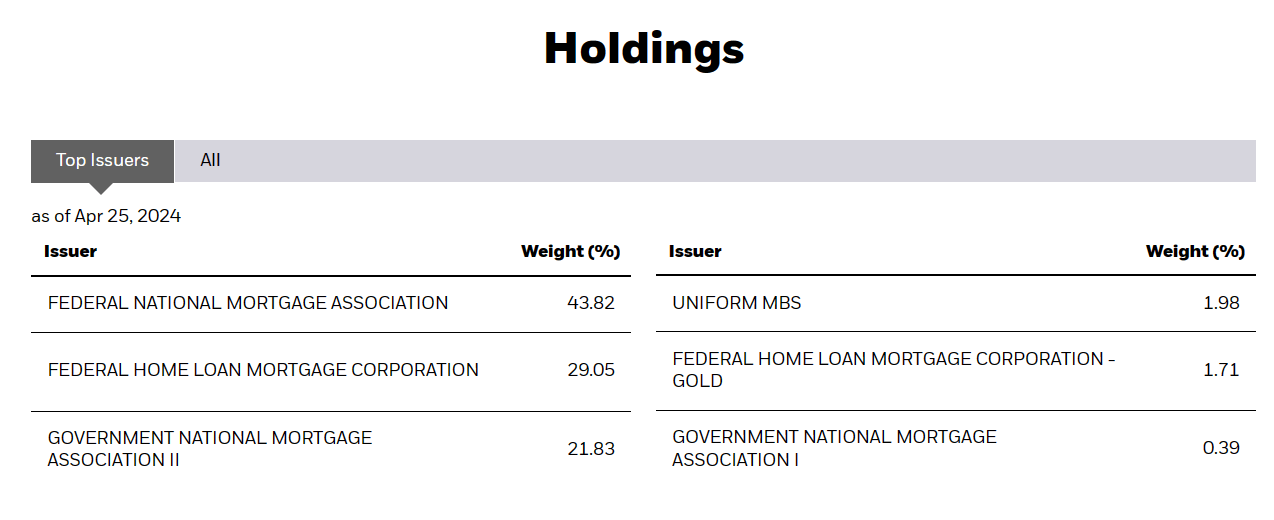

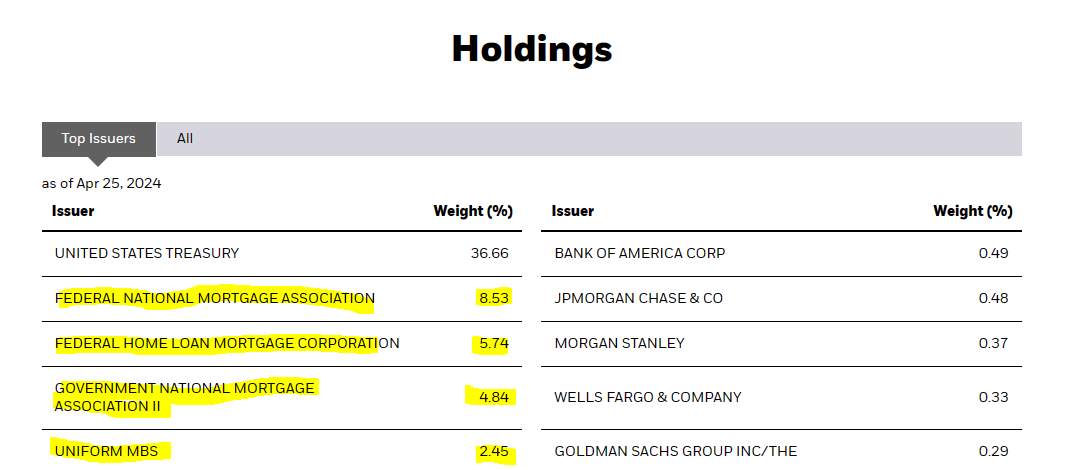

The iShares MBS ETF (NASDAQ:MBB) serves as a one-stop store for U.S. mortgage-backed securities, primarily issued by Ginnie Mae, Fannie Mae and Freddie Mac. The latter two entities are sponsored by the federal government, versus Ginnie Mae, which is owned by them. The holdings corroborate the preponderance of the terrific trio within the ETF’s portfolio.

MBB

This revenue searching for, alternate traded fund is passive by nature. Which implies that its goal is to trace the funding outcomes of an index, making no effort to outperform it or react to the altering market circumstances. The index in query for our protagonist is the Bloomberg U.S. MBS Index. The securities included on this index are issued by the aforementioned enterprises and have maturities of 15, 30 or 20 years. To be eligible for inclusion within the index, the safety must have not less than a yr left to maturity.

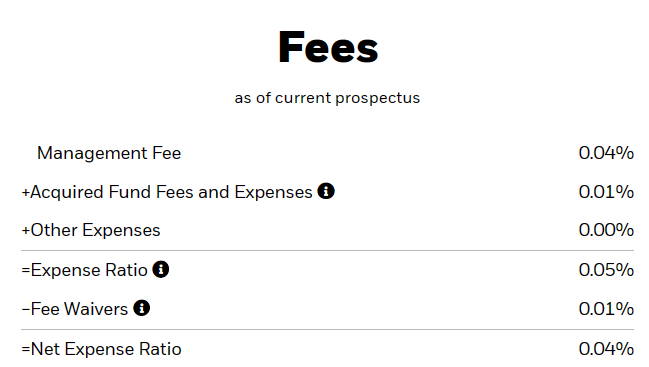

MBB makes use of the consultant sampling indexing technique in its endeavor to reflect the outcomes of the benchmark. This entails holding a portfolio of securities which have funding and elementary traits just like that of the index elements. The ETF goals to speculate not less than 90% of its property in forms of securities which are included within the index. MBB has annual bills of 0.04%, whereas the index has none.

MBB

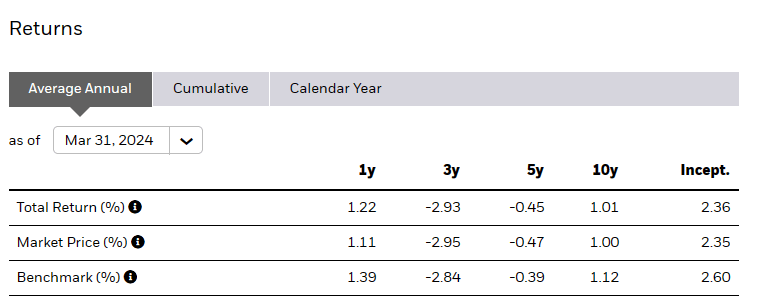

The ETF’s beneath efficiency vis a vis the benchmark in virtually all time frames is greater than what could be accounted for by its bills. We’ll observe right here that the bills have been larger beforehand and have now been diminished to a rounding error.

MBB

The place This Suits In Your Allocation?

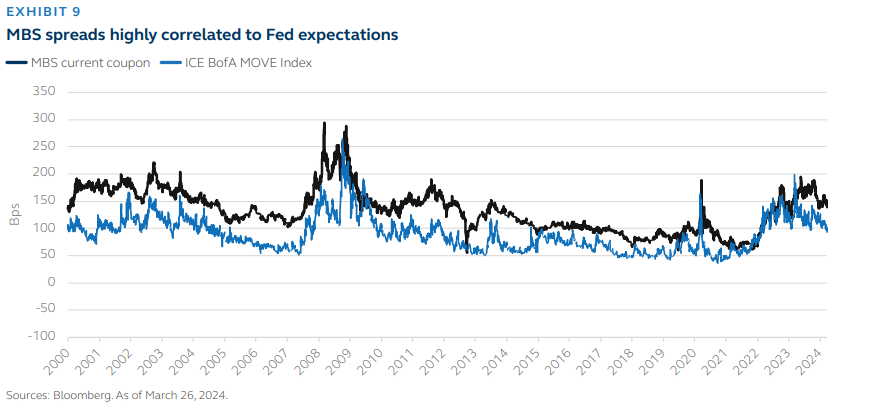

Mortgage Backed Securities have continuously been a speaking level on In search of Alpha. The rationale they’ve come up so typically is as a result of many like to chase mortgage REITs, they usually personal, primarily, Mortgage Backed Securities. The latest dialogue has centered round the truth that these are low cost and those making that declare are usually not incorrect. You may see within the chart under, that the unfold is often about 50 foundation factors relative to comparable Treasuries.

Bloomberg

The phrase “usually” refers to in quiet instances. Because the above chart additionally reveals, when bond volatility index or MOVE spikes, the unfold spikes as nicely. Right this moment we’re getting a wider unfold and that’s the reason for all the joy. Notice that the chart runs until March 26, 2024.

Now, this unfold is, in a method, a risk-free unfold. These securities are government-guaranteed, so you’re getting the identical implied credit score as that of the US Treasuries. So why does everybody not make investments each single greenback in these versus US Treasuries? The reply is that whereas their credit score threat is similar, their length threat may be very uncommon. If you happen to purchase a 10-12 months Treasury and maintain until maturity, you may have your return profile setup at first. The worth might actually transfer within the interim, however you realize what you’re getting. With Mortgage Backed Securities, you may have a can of worms, and it’s arduous to foretell precisely what you’ll get. The largest challenge is that their length is an estimate. Whereas these are 15 and 30 yr securities to start out off with, the common funds of principal scale back the length. There’s flexibility to additionally pay extra principal in lots of circumstances with out penalties. Extra importantly, there’s a enormous threat if charges fall and these get refinanced at decrease charges. So Mortgage Backed Securities have an enormous destructive convexity. That in easy phrases implies that they admire quite a bit lower than related (non-callable) bonds when charges drop.

With all that mentioned, they these bonds ought to nonetheless kind a part of investor’s portfolio as that additional unfold (50 foundation factors in regular instances, and far more at present) does add some juice to a portfolio.

Does MBB Match Your Portfolio?

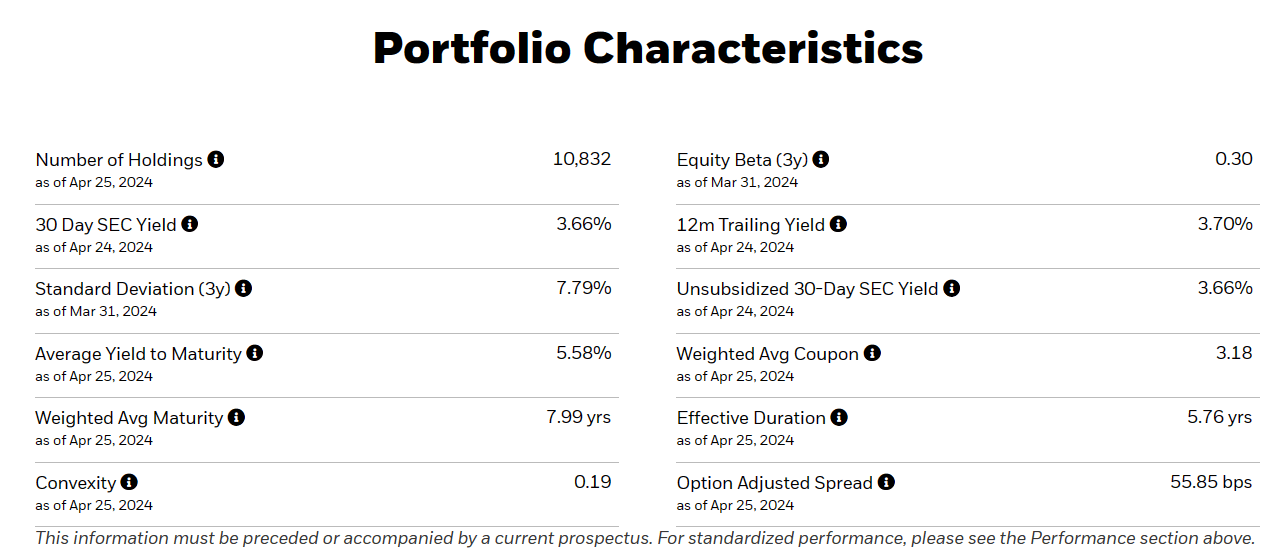

The primary challenge with MBB is that it holds loads of classic low coupon bonds, that are a part of the index. So if you happen to have a look at the portfolio traits, there’s a huge hole between the weighted common coupon and the common yield to maturity.

MBB

Because of this, the funds are nowhere close to the yields that may you get on newer bonds. MBB’s distribution is yield is 3.77% and it seemingly rises over time. However this will likely be little solace to the revenue investor getting 5.0% plus on Treasuries and as much as 5.5% on 1 yr CDs. As a standalone, they are often disappointing. Plus, it’s possible you’ll have already got publicity to this space with out figuring out. Most 60:40 and goal date retirement funds allocate handily to those securities. For instance, we use iShares Core Progress Allocation ETF (AOR), as our primary benchmark in our Marketplace Service. That fund reveals the next holdings.

In search of Alpha-AOR

Okay, so it’s possible you’ll assume that there aren’t any Mortgage Backed Securities there. However if you happen to look deeper in to the second holding, iShares Core Complete USD Bond Market ETF (IUSB), you see these as the first holdings.

IUSB

So in case you are investing through any whole market ETFs on the bond facet, chances are high that you’re getting your fill. In case you are an investor that’s doing the heavy lifting through particular person allocations, and revenue will not be crucial factor to you proper now, an allocation to MBB would possibly make sense for you. We do not personal MBB at current, however we now have our eyes on a few different related funds that we’d pull the set off on and challenge an alert for our subscribers. Our place has to date been that longer dated yields on bonds are usually not compensating you for the dangers, and to date, we now have been proper to remain away. However the second to go “all-in” on Treasuries is drawing shut, and the additional unfold on Mortgage Backed Securities is one we’d get behind.

Please observe that this isn’t monetary recommendation. It might look like it, sound prefer it, however surprisingly, it’s not. Buyers are anticipated to do their very own due diligence and seek the advice of knowledgeable who is aware of their aims and constraints