Wirestock/iStock Editorial through Getty Photos

Funding Thesis

McDonald’s Corp (NYSE:MCD) reported outcomes on the fifth, February. Factset analyst’s anticipated a rise of 4.7% in identical retailer gross sales for the quarter however the firm reported a acquire of solely 3.4%. The share value dropped 3.7% on the closing bell and has since retracted additional to commerce on the 200-day shifting common. The miss on revenues is attributed to a decline in exercise throughout the center east as boycotters dent gross sales because of the firm reportedly giving free meals to the Israeli navy. I imagine it is a good time to start writing on the corporate and have initiated a Maintain on the grounds that the Center East battle will proceed to adversely have an effect on revenues. However the long-term image appears sturdy with the enlargement of the Speed up the Arches technique driving development over the long-term.

Speed up The Arches Technique

Since 2019 MCD has acted upon their Speed up the Arches technique to ship distinctive efficiency, producing 5.3% CAGR development since 2019. The technique has 3 pillars that undermine the latest success of the corporate:

- Maximize Advertising and marketing

- Decide to Core

- Double Down on the 3Ds.

MCD continues to make the most of their advertising and marketing experience to interact with clients and construct a world class model. It was voted by Kantar as one of the top five most precious manufacturers, pushed by culturally related campaigns that clients love to interact with. Their dedication to the core menu that represents 65% of systemwide gross sales is a confirmed success and MCD’s innovation on this essential phase has allowed them to develop market share. Lastly, MCD has targeted on delivering an distinctive digital expertise of their loyalty program. This is among the largest of its sort had homes over 150 million energetic customers, with plans to increase in direction of 250 million customers by 2027. With this distinctive development in energetic customers MCD plan to have meals prepared for arrival by 2025 additional growing effectivity throughout the group.

On the sixth December within the investor update MCD introduced new targets in relation to their Speed up the Arches technique. In abstract it consists of concentrating on an bold 50,000 eating places by 2027, in addition to including 100 million energetic customers to the membership plan by 2027 and integrating Google Cloud know-how to enhance operations. The enhancements are anticipated to drive continued monetary efficiency with the corporate concentrating on 2.5% Systemwide gross sales development past 2024 and a continued enlargement in working margins.

Center East Battle

Whereas I will not contact on the precise state of affairs resulting from Searching for Alpha tips, the Center East battle is affecting MCD revenues! According to data in 2021 MCD had 213 eating places situated in Israel and an additional 1,650 situated throughout the Center East, with the affect of the conflict is taking its toll. Revenues for the 4 months to December elevated solely 0.7% within the IDL phase and administration aren’t very optimistic on the state of affairs. It has been reported that MCD have been handing out free meals to Israeli militants and I worry this might snowball right into a model damaging catastrophe. It’s estimated that 300,000 have taken to the streets of London alone in assist of a Gaza ceasefire and the Israeli authorities have taken no such motion. If the press will get ahold of this data extra totally, world boycotts might ensue placing additional stress on MCD gross sales.

Financials Level To Lengthy-Time period Purchase

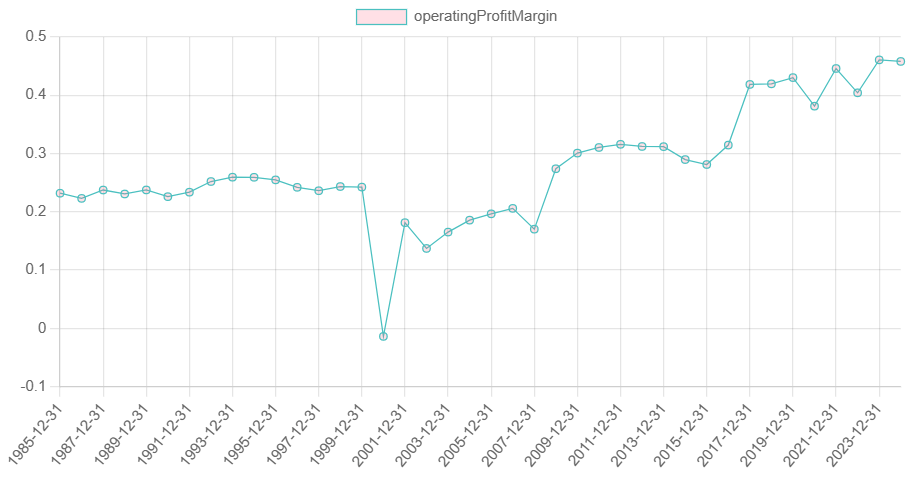

The financials look sturdy and undoubtedly suggest a purchase case for the corporate. Full yr revenues climbed 10% and EBIT Margins expanded 570 foundation factors. Historically MCD was an organization in decline, with revenues falling -2.2% CAGR between 2010 and 2020 however since COVID there was a notable enhance in gross sales with a development fee of seven.3% CAGR during the last 4 years. This development is attributed to the Speed up the Arches technique that was shaped in 2019 and I anticipate this technique to proceed driving success for the group going ahead.

Regardless of the aneamic gross sales development previously, the corporate has efficiently expanded working margins resulting from glorious working leverage pushed by spectacular value reductions. This has resulted in EBIT Margins rating seventh out of 525 firms within the Consumer Discretionary sector.

Supply: Writer’s Calculations

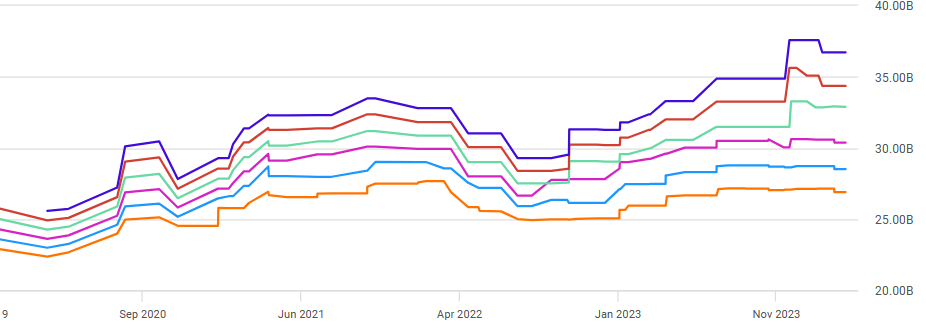

After subtracting curiosity expense and different revenue internet margins present an identical image, with a serious enlargement in profitability between early 2000s and 2024. The growing internet margins and nicely managed working capital has expanded free money move margins which at present stand at 25%. The corporate makes use of its $15 billion share repurchase program introduced in 2019 to return cash to shareholders and in addition pays a dividend yield of two.1%.

Extra just lately, gross sales elevated 3.4% in This autumn, coming in just below estimates pushed by strong development in North America offset by anemic development within the IDL phase. Internet Margins contracted -28 foundation factors however after changes expanded 136 foundation factors to 33.5%. The corporate missed on high line numbers due to the battle within the Center East.

Revisions

For the reason that outcomes revisions have fallen again as anticipated. Additional out income estimates fell instantly following the outcomes and within the continuing weeks the newer years estimates have additionally marginally declined. This lower in revisions is because of the miss on identical retailer sale in This autumn that was pushed by poor efficiency throughout the IDL phase. That poor efficiency is being pushed by battle within the Center East and sure clients boycotting MCD resulting from them delivering free meals to Israeli militants. The battle is a transparent near-term headwind and MCD administration are expressing concerns:

So long as the conflict is happening… we’re not anticipating to see any vital enhancements [in these markets]

Searching for Alpha

Valuation

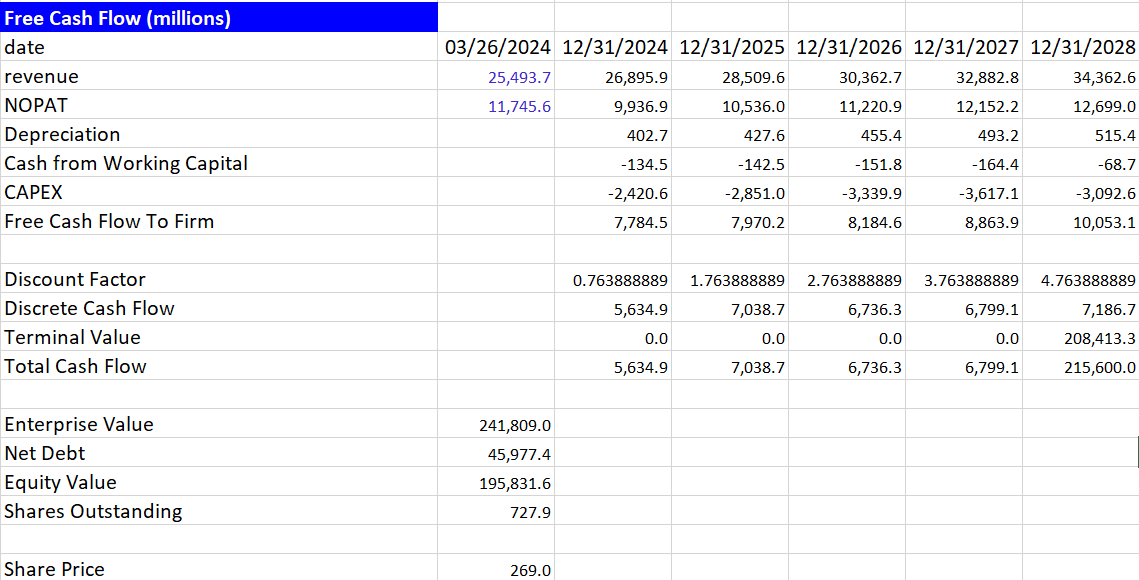

Supply: Writer’s Calculations

When valuing MCD I’ve used a a number of of 29x to get a share value goal of $269 and a draw back of -4.6% from in the present day’s value. The median a number of during the last 5-years is 30x however because of the ongoing battle and up to date destructive press I’ve used a barely decrease a number of to account for this.

Supply: Writer’s Calculation

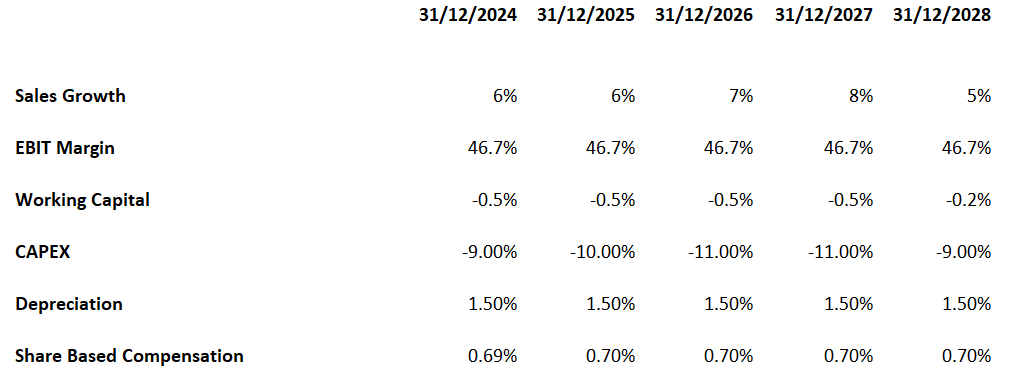

During the last 6-years MCD has invested closely into working capital and I’ve the investments lowering going ahead as I do not suppose the present degree might be sustained so have rolled out a -0.5% incremental change. When it comes to CAPEX the corporate has a fairly sturdy enlargement undertaking deliberate so I’ve CAPEX growing in direction of 11% by 2027 to account for the 55,000 new shops deliberate.

Dangers

The main problem to my thesis is the battle within the Center East. To date the UN Safety Council has ordered an immediate ceasefire however Israel responded with extra assaults. If a ceasefire does happen that will warrant a change in my advice as different MCD markets are rising, and adjusted revenue metrics are increasing.

Conclusion

The long-term outlook for MCD stays sturdy, the financials are glorious, and the corporate maintains its standing of getting a robust moat however the present battle within the center east might lead to unhealthy press and additional boycotts. That’s the reason I’m initiating a Maintain on the corporate with a share value goal of $269. I think about MCD will deal with the issue within the coming quarters however for now the very close to time period outlook would not look promising.