sshepard

My newest article on Medical Properties Belief (NYSE:MPW) was issued again in October 2023 earlier than the Firm circulated its Q3, 2023 outcomes and supplied some attention-grabbing insights to the market.

In this article, I outlined a number of basic points, which have made MPW a gorgeous funding:

- Multiples buying and selling at a deep worth territory warrants a positive floor for experiencing an enormous bounce again supplied that constructive information factors emerge.

- Strong debt administration as a result of a mix of dividend cuts and asset gross sales, MPW has largely neutralized main refinancing danger by 12 months 2026.

- Properly-structured lease expiration profile places away stress on lease rollovers that might doubtlessly impose a further layer of danger throughout instances of steadiness sheet optimization, when money stream stability is important.

With that being mentioned, your entire funding case must be caveated by two tenants – Prospect Medical Holdings and Steward Well being Care – which collectively account for ca. 25% of the Q3 2023 leases. As a lot of you recognize, MPW has been pressured to step in right here to keep away from submitting Chapter 11, present its personal financing, and defer lease collections (on a money foundation). Whereas monetary prospects appear to be bettering for each of those tenants, they each are nonetheless working in speculative territory with a notable likelihood of additional misery. Within the case of such a situation, the affect on MPW’s money era and extra danger premiums on the Firm’s capital could be dramatic.

Now, because the publication of my article, the full returns have landed at 3.9%, whereas the S&P 500 is up by 9.1%, and, most significantly, the broader REIT index advancing by 15.1%.

Within the meantime, MPW has printed recent quarterly outcomes and the assumptions of financial coverage have modified in favour of such entities as MPW, which must refinance and embark on notable asset monetization transactions.

Synthesis of the prevailing state of affairs after Q3

Let’s now take a fast have a look at the underlying financials and the state of MPW’s steadiness sheet.

In my view, essentially the most regarding situation is related to MPW’s capacity to efficiently refinance and accomplish that in a way, which doesn’t destroy the FFO era.

In Q3, 2023, we might lastly discover how part of the rapid debt maturities has been efficiently retired – primarily because of the sale of Australian services.

Kind 10-Q for Medical Properties Belief

Presently, MPW has to refinance solely ~$440 million by the tip of this 12 months and never fear about extra debt rollover till 2025. The excellent quantity in 2024 which is mirrored within the desk above, has been already paid down proper after the publication of the Q3 report (by utilizing the proceeds from prior transactions of Australian properties).

Contemplating the quarterly money retention after dividend distribution of ~$135 million (primarily based on Q3, 2023 information), acquiring short-term financing for 2023 maturities or tapping into a number of the current revolver capability shouldn’t be an issue for MPW.

Plus, we should always not count on a significant affect on the curiosity value element though this 2023 maturity is predicated on a comparatively low mounted price. The constructive results from a full neutralization of the 2024 quantity ought to present an offsetting increase by way of the curiosity value place.

All in all, these enhancements shouldn’t be that shocking since that was already communicated earlier than. A constructive aspect on this context is that we are able to see a sensible realization of the communicated technique {that a} notable de-leveraging focus will happen.

Within the latest earnings call, Edward Aldag, CEO of MPW, additionally confirmed that getting steadiness sheet in examine stays the important thing precedence for the administration:

Our present major focus is on executing a capital allocation technique that can present the liquidity to fulfill our debt maturities even debt that does not mature for a number of years.

On high of this, Steven Hamner, CFO of MPW, said that there’s a plan to draw ~$ 2 billion of capital over the course of 2024:

I can say that we’re focusing on roughly $2 billion of liquidity transactions over the following three to 4 quarters.

Which means MPW will be capable to refinance 2025 debt properly prematurely of its official maturity and to some extent additional optimize the underlying danger profile by bringing down a number of the excessive yielding debt. Right here we have now to notice that we have no idea how a lot of those proceeds will stem from debt financing (i.e., mortgages) and the way a lot will come from fairness akin to monetization of JVs or direct asset gross sales.

Lastly, the efficiency of each struggling tenants appears to be getting higher and exhibiting first indicators of restoration. For instance, throughout Q3, 2023, MPW began to obtain lease funds from Prospect Medical Holdings. It’s projected that Prospect will provoke new lease funds of $3.5 million per 30 days early subsequent 12 months (associated to earlier direct finance/assist from MPW).

Steward has additionally managed to strengthen its profile because the reported EBITDARM hire protection landed at 2.7x.

Granted, the state of affairs for these two tenants nonetheless stays troublesome and MPW has not but materialized its investments and precise money flows haven’t began to stream in a full/full method.

Approach to play it

Whereas from the aforementioned points, MPW’s fairness story appears somewhat stable, there’s nonetheless a excessive likelihood of experiencing additional difficulties down the highway.

For my part, there are 4 main issues on why to keep away from fairness publicity:

- Trying on the latest historical past, we had a number of cases which might be just like this one, the place the MPW’s fundamentals have seemed very sound, however in the long run (largely as a result of tenant points), the inventory worth has simply continued to go south.

- Regardless of the latest information and a beneficial recalibration of near-term rate of interest outlook from excessive and unsure to regularly declining and clear by way of the height degree, MPW has responded poorly, particularly if in comparison with the opposite REIT friends. This sends a transparent sign that it will likely be somewhat troublesome for MPW to get the inventory worth increased with out important enhancements on the tenant facet.

- We lack transparency of the underlying monetary positions of Steward and Prospect to make justified conclusions pertaining to their capacity to service their lease obligations, which in MPW’s case account for ~25% of the top-line.

- Based mostly on the recent news, it appears that evidently there could possibly be extra tenant issues brewing in MPW’s portfolio. If this danger begins to materialize, I feel it’s for certain that extra market cap will probably be worn out.

On the identical time, wanting on the progress on steadiness sheet optimization in addition to some preliminary indicators of bettering state of affairs with Steward and Prospect going quick could be additionally a dangerous concept.

In search of Alpha

The chance of “short squeeze” is particularly related after we see fully depressed valuations at the side of constructive tailwinds within the financial coverage area.

Because of this, in my humble opinion, a place in MPW’s bonds appears essentially the most engaging option to seize returns from MPW.

It is dependent upon which bond we take, however sticking to USD foreign money and a maturity profile that may give buyers time to gather coupons, MPW 5.250% 01Aug2026 Corp bond (US55342UAG94) could possibly be thought of optimum.

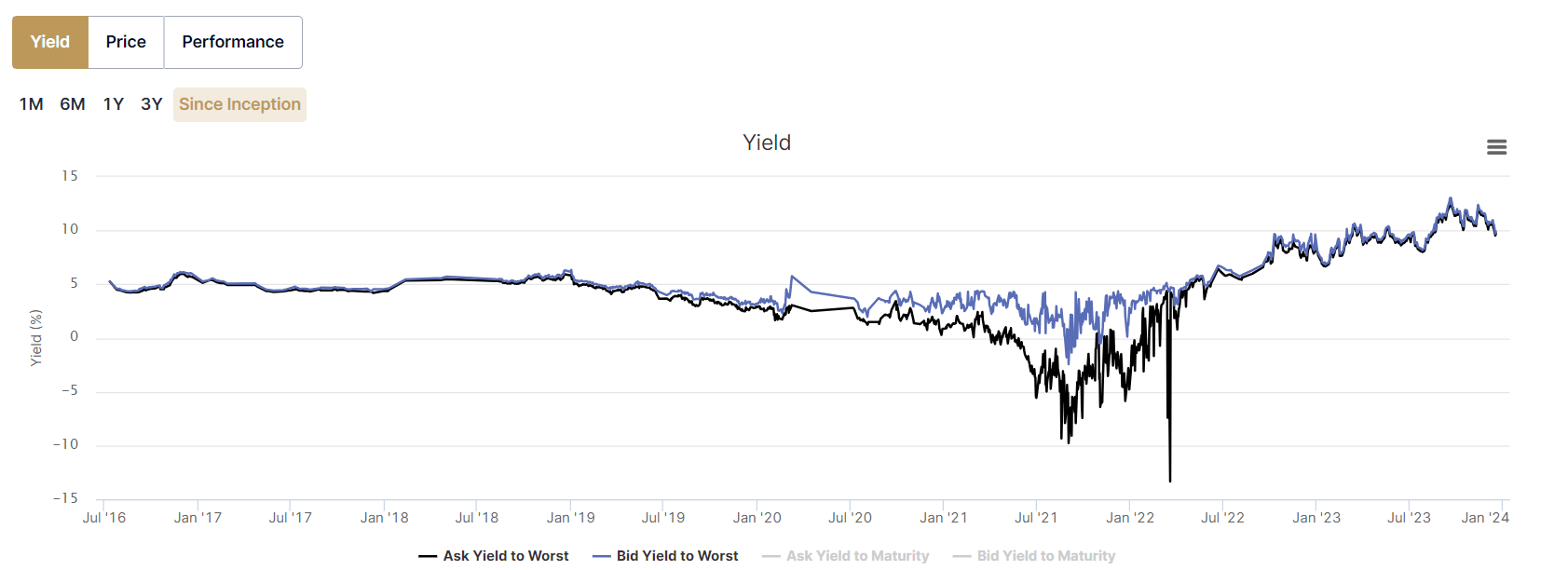

Bondsupermart Ltd

As we are able to see within the chart above, at present MPW’s bond yields are near their peak ranges, yielding ~10%. The YTM of the USD 2026 bond at present stands at 9.8%, which is simply ~220 foundation factors beneath the prevailing dividend yield.

Contemplating the chance and reward ratio between MPW’s fairness and bonds, it’s clear that a further 200 foundation factors don’t justify the incremental danger, which is related to fairness publicity.

Adjusted for one-offs, MPW distributes ~60% of its AFFO, which leaves an ample quantity of inner money that could possibly be put to work on both decreasing debt or making accretive acquisitions. This suggests additionally a capability for MPW to soak up new shocks with out having to faucet into debt financing sources. Within the worst case, MPW carries additionally an optionality to make additional dividend cuts to avoid wasting $100 – 150 million per quarter.

Bonds are additionally extra protected provided that the Administration has set targets to cut back leverage within the books and doubtlessly retire parts of the at present excellent debt though their maturities are fairly far sooner or later.

Lastly, within the context of normalizing rates of interest, publicity to period issue (e.g., bonds) per definition ought to reply properly. Versus MPW’s fairness, which has not reacted to extra dovish information, the bond positions have truly adjusted accordingly by growing in worth; so the YTM degree has dropped by ~150 foundation factors previously month.

The underside line

Whereas MPW’s fairness appears to be somewhat engaging because of the depressed valuations and bettering fundamentals, the important thing dangers stay considerably unclear, which within the case of materialization would likely additional destroy shareholder worth.

But, given the strengthening of underlying fundamentals (e.g., no materials debt maturities by 2025) and the comparatively engaging yield that’s provided by MPW’s bonds, taking a protracted place within the fixed-income element of MPW is way extra optimum option to seize a double-digit yield.