bluekite

Earlier Thesis

I final coated Medical Properties Belief, Inc. (NYSE:MPW) again in November in an article titled: Don’t Get Cut Being Greedy When You Should Be Fearful. This was an apparent play on phrases referencing traders catching a falling knife within the type of MPW. For the file, I used to be as soon as a shareholder in MPW, however bought out some time in the past at a loss earlier than they minimize the dividend.

I mentioned the dividend minimize of almost 50% to unencumber liquidity through the third quarter. And whereas this did unencumber capital giving the REIT a then 49% payout ratio, the corporate has continued to face points I am going to focus on later within the article. Moreover, the share value has declined farther from almost $5 to $4.25, the place it at the moment trades on the time of writing. On this article, I focus on why I would not contact this REIT with a 10-foot pole and why traders should not both.

Temporary Overview

For these new to Medical Properties Belief, MPW is a REIT that invests primarily in healthcare services all through the world. On the finish of 2023, they’d 439 properties in 9 completely different international locations throughout 50 tenants. A few of their tenants embrace Steward, their largest firm, adopted by Circle Well being. Of word, 40% of their properties are situated exterior of the US, with most situated in Germany & Switzerland.

Dividend Elimination?

I simply wish to say I do not quick shares. As beforehand talked about, I used to be a shareholder in Medical Properties Belief. As a result of their constant tenant points, I made a decision to promote the inventory at a loss and make investments the capital elsewhere.

One factor I’ve discovered is to not turn into emotionally connected to a inventory. That is most likely the largest lesson the inventory market has taught me. As an investor closely weighted within the REIT sector (XLRE), I’ve a number of favorites that present me with steady and dependable revenue. These like Agree Realty Company (ADC), NNN REIT, Inc. (NNN) and VICI Properties Inc. (VICI). However I additionally put money into them due to their dividend security.

Each ADC & VICI had payout ratios of round 75%, whereas NNN had a payout ratio of roughly 69%, very protected for REITs. But when their financials grew to become suppressed for too lengthy, irrespective of how a lot I appreciated them, I might minimize my losses if their fundamentals began to alter. I might additionally take note of how their CEO plans to appropriate their declining fundamentals.

Throughout Q4 earnings again in February, MPW’s CEO addressed the dividend broadly:

The Board will meet later this quarter to debate the dividend. The board’s coverage on the dividend stays unchanged. As has all the time been the case, the Board will assessment all elements of the corporate, together with objects similar to FFO payout ratio, REIT necessities, and liquidity.

Now, some could say he did not say that the corporate was slicing the dividend. And whereas he did not, he did not sound too assured in paying a dividend for the upcoming quarter. This jogged my memory of Walgreens Boots Alliance, Inc. (WBA) once they broadly addressed the dividend throughout an earnings name.

When WBA’s administration workforce failed to handle particularly why they held the dividend and determined to forgo Dividend King standing within the course of, I noticed the basics could be altering and a dividend minimize was prone to happen. A reader instructed me I used to be unsuitable and that they selected to not handle this to present the brand new CEO flexibility. And whereas the minimize was hypothesis on my half, everyone knows what occurred.

And for good purpose. Generally a dividend minimize is required. On this case, I would not be shocked if it was suspended or eradicated altogether. I do not assume it will be a foul transfer on the corporate’s half due to their liquidity points. And I believe it is doubtless priced in already, so the share value will not fall too removed from right here in my view.

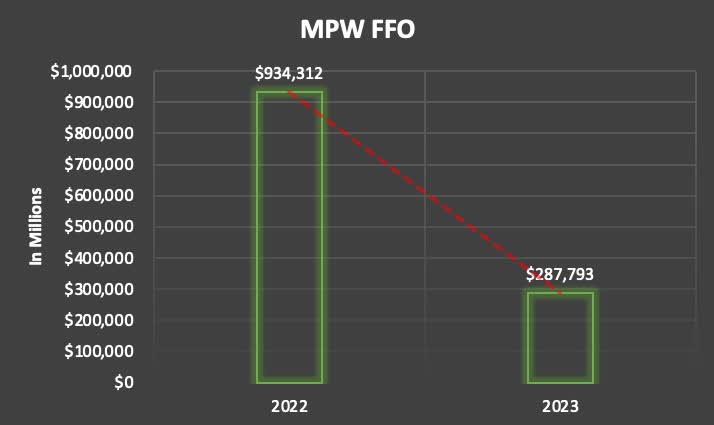

Utilizing their CEO’s phrase and their FFO payout ratio, you possibly can see within the chart beneath that this declined considerably from 2022. In accordance with their 10-K, FFO declined roughly 69% year-over-year, an enormous drop. And the corporate paid out $615,390 in dividends for the complete 12 months. This provides them a payout ratio above 100% at the moment. And whereas some REITs do function with elevated payout ratios, one has to marvel how lengthy earlier than the dividend is minimize or eradicated? And what are they going to do to proper the ship?

Creator creation

MPW’s revenues additionally declined considerably year-over-year, dropping from roughly $1.5 billion to $871.8 million in 2023. In This autumn income of -$122 million was down from $306.6 million in Q3. I do not find out about you, however this does not seem like an organization I wish to make investments my cash in.

And regardless of the challenges over the past two years for REITs particularly due to greater rates of interest, many have carried out nicely, even rising their financials over the identical interval. Living proof, VICI Properties and Agree Realty.

The nice factor is FFO did are available above the steerage administration set in Q3 of $1.56 – $1.58. FFO of $0.36 within the fourth quarter beat estimates by $0.07 however nonetheless fell from the prior quarter and This autumn ’22’s $0.43. Bringing the entire to $1.59 for the complete 12 months. 12 months-over-year this fell almost 13% from $1.82 in 2022.

Enhancing Liquidity

MPW has been attempting to enhance its liquidity, making efforts by promoting off a few of its property. However once more, who needs to put money into an organization that has to unload vital property to enhance liquidity? This tells me the corporate’s stability sheet is just not in fine condition, nevertheless it additionally places the dividend at excessive danger of a minimize if an organization has to promote property.

Administration has expressed they wish to use the liquidity to pay their off debt for years to come back. However the query it’s a must to ask your self is, what’s going to they do when that debt is paid? What property will MPW have offering money stream to maintain firm progress and dividend funds sooner or later? What accretive acquisitions does administration see themselves making to maintain their enterprise? From their earnings name, it appears fairly imprecise to me.

The corporate’s largest and most troubled tenant, Steward recently agreed to promote its managed care enterprise to behemoth UnitedHealth Group Included (UNH) due to their monetary points. Moreover, they closed on the sale of 4 of their Australian services for proceeds of $305 million and in addition bought 5 of their hospitals at a cap charge of seven.4%.

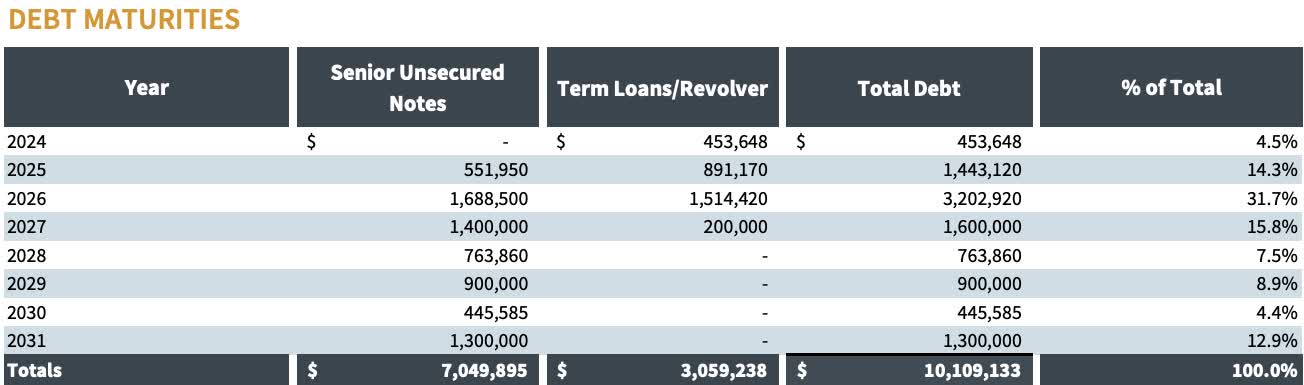

That is all in the direction of their capital allocation plan to generate not less than $2 billion this 12 months. And a few of that is anticipated to go towards the REIT’s upcoming debt. In Might, MPW has $300 million maturing and an extra $130 million on the finish of the 12 months in December. Subsequent 12 months they’ve greater than double that quantity with $1.4 billion due. So, within the subsequent two years, MPW has almost 20% of its $10 billion in debt due.

MPW supplemental

Moreover, the corporate’s leverage degree continued to extend over the 12 months, up from 6.4x in This autumn ’22 to six.9x on the finish of the fiscal 12 months. For REITs, I prefer to see them function within the 5x – 5.5x vary. After they begin getting nearer to 6x and up, that is when issues can get difficult.

Moreover, this additionally speaks to the corporate’s administration workforce. A wholesome leverage degree and well-laddered stability sheet give an organization flexibility to not solely make accretive acquisitions, but in addition unencumber capital to speculate again into the enterprise to develop organically. Among the finest REITs with the most effective stability sheets proper now’s Agree Realty, who had a professional forma web debt-to EBITDA of simply 4.3x.

For comparability functions, CareTrust REIT, Inc.’s (CTRE) web debt-to EBITDA was simply 1.4x on the finish of their fiscal 12 months. And I’ve covered this stock here on Looking for Alpha earlier than. So, for those who’re trying to make investments into the medical REIT area, CTRE is the most suitable choice in my view. Evaluating them to Sabra Well being Care REIT, Inc. (SBRA) whose web debt-to-adjusted EBITDA was a wholesome 5.74x on the finish of their newest quarter.

Valuation & Dangers

I get it. On the present value of a bit of over $4 a share, some traders could also be saying how a lot can I lose? Most of their points are already priced in and whereas I agree the inventory will not doubtless fall a lot farther, I do not assume it’s going to see any vital upside anytime quickly.

Nevertheless, you probably have a longgggg time period outlook, then perhaps, simply perhaps, MPW is an efficient inventory to carry. At a price-to-book worth of simply 0.33x, your draw back danger is probably going restricted. It does provide some upside to its excessive value goal of $7 however the query is when will the inventory attain that value? I do not see it transferring previous $5 within the foreseeable future. MPW’s administration workforce has a number of work minimize out for them and in my view, will probably be a very long time earlier than traders see some upside.

Looking for Alpha

In the case of dangers, Medical Properties Belief has too many to call. Moreover their largest and most troubled tenant, Steward, many could have forgotten about their tenant points with Prospect Medical Holdings. The REIT entered right into a recapitalization plan to defer lease funds till June.

Whereas they had been present on all lease and curiosity as of the fourth quarter, with rates of interest doubtless remaining greater for longer, this may occasionally proceed to place stress on Prospect, making it more durable to stay present on lease funds. If that’s the case, it will actually influence MPW’s financials within the coming quarters, and in the end power them to chop or remove the dividend within the foreseeable future. This, together with their tenant troubles is one thing I will likely be conserving a detailed eye on going ahead.

Backside Line

MPW confronted a number of headwinds in 2023 with tenants Steward Well being and Prospect Medical Holdings. Right here we’re in 2024 and these proceed on. The REIT has been making a concerted effort to enhance its liquidity to fulfill upcoming debt maturities and plans to achieve $2 billion of allotted capital in 2024. One option to obtain this can be to make the choice to remove the dividend or minimize once more which I believe is a excessive likelihood.

Moreover, their web debt-to-EBITDA has continued to climb year-over-year to six.9x, and with charges prone to stay greater for longer, it will solely proceed to position extra downward stress on the corporate going ahead. As a result of their continued headwinds, vagueness from administration on the corporate’s future going ahead, and extremely leveraged stability sheet, I proceed to charge the REIT a robust promote and one traders ought to keep away from.