Just_Super/iStock by way of Getty Pictures

Medtronic PLC (NYSE:MDT) is a worldwide developer and producer of medical gadgets for continual illnesses. Based in 1949, Medtronic is now a $111 billion (by market cap) healthcare behemoth that employs 95,000 individuals. The corporate experiences outcomes throughout 4 segments: Cardiovascular, 37% of FY 2023 income; Neuroscience, 29%; Medical Surgical, 27%; and Diabetes, 7%.

Medtronic’s product portfolio is comprised of quite a lot of life-saving and life-improving medical gadgets that embrace implantable defibrillators, coronary heart valves, insulin pumps, glucose monitoring methods, pacemakers, stents, and surgical instruments.

Not solely is Medtronic’s product portfolio broad, nevertheless it’s additionally dominant. Morningstar places it like this: “Medtronic has historically held roughly 50% share in its core heart devices. It’s also the market leader in spinal products, insulin pumps, and neuromodulators for chronic pain.”

Healthcare is one in every of my favourite areas of the economic system to spend money on. That’s as a result of healthcare demand is uncorrelated with financial cycles. One’s demand for healthcare is uniquely tied to at least one’s well being. If one has a critical well being problem, rectifying the difficulty is all that issues to that individual at that time limit – it doesn’t matter what’s happening with the economic system. Since well being points are a standard function of the human situation – human our bodies slowly deteriorate as they age – there’s a continuing base stage of demand for healthcare purely from a human existence standpoint.

Plus, healthcare services often function inelastic demand. The spending on these merchandise is often non-discretionary in nature, particularly if it’s a life-or-death circumstance that doesn’t lend itself to cost sensitivity or on-the-spot negotiation. If one thing like emergency surgical procedure is immediately known as for, one is of course way more involved with survival than the precise pricing of the medical gadgets wanted to avoid wasting one’s life.

One other facet of healthcare that’s extremely interesting for long-term funding? Demographic tendencies. First, our international inhabitants is rising. Second, persons are, on common, dwelling longer than ever earlier than. Third, the wealth of the typical individual continues to rise.

A higher variety of older and wealthier human beings strolling round practically ensures extra demand for high quality healthcare, on the whole, and Medtronic’s industry-leading merchandise with inelastic demand, particularly.

All of this is the reason Medtronic ought to proceed to develop its income, revenue, and dividend for years to return, simply because it’s been doing for years already.

Dividend Progress, Progress Price, Payout Ratio and Yield

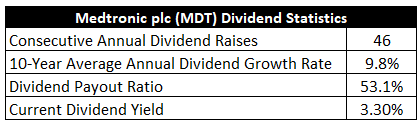

To this point, Medtronic has elevated its dividend for 46 consecutive years. That prolonged and spectacular monitor file simply qualifies Medtronic for its standing as a vaunted Dividend Aristocrat. In actual fact, it’s practically a Dividend Aristocrat twice over.

The ten-year dividend progress charge is 9.8%, and that’s fairly sturdy, though newer dividend raises have been within the mid-single digit vary.

However, the inventory’s yield has been recalibrated by the market and adjusted upward with a purpose to compensate for that slower progress charge.

The yield is now at 3.3%. If you happen to’ve been following Medtronic for some time, you’ll discover how unusually excessive that yield is for this inventory. For perspective on that, it’s 90 foundation factors larger than its personal five-year common. Much less progress however extra yield. And for buyers who lean extra towards earnings, that is perhaps a really acceptable trade-off.

Furthermore, as I’ll delve into later, I don’t assume this slowdown is everlasting in nature, and the next progress charge within the close to future could drive the market to readjust the yield again right down to its historic norm. That type of adjustment would require the inventory value to go larger, and that’s the place the near-term alternative may very well be.

With a payout ratio of 53.1%, primarily based on midpoint steerage for FY 2024 adjusted EPS, the dividend seems to be as safe as ever. For buyers looking for an above-average dividend from a Dividend Aristocrat, it is a fairly attention-grabbing setup.

Income and Earnings Progress

As attention-grabbing as these metrics is perhaps, although, lots of the numbers are wanting into the rearview mirror. Nevertheless, buyers should all the time be wanting by the windshield, because the capital of as we speak is placed on the road and risked for the rewards of tomorrow. Thus, I’ll now construct out a forward-looking progress trajectory for the enterprise, which can be of nice assist when the time involves estimate truthful worth.

I’ll first present you what the enterprise has achieved over the past decade when it comes to its top-line and bottom-line progress. And I’ll then reveal an expert prognostication for near-term revenue progress. Lining up the confirmed previous with a future forecast on this method ought to give us the data essential to make a judgment name on the place the enterprise may very well be going from right here.

Medtronic superior its income from $17 billion in FY 2014 to $31.3 billion in FY 2023. That’s a compound annual progress charge of seven%. I’m often searching for a mid-single digit top-line progress charge from a mature enterprise like this. Medtronic greater than delivered.

However it’s vital to remember that a significant chunk of this income progress resulted from the acquisition of Covidien PLC in 2015 for nearly $50 billion. This complementary addition to the corporate (with Covidien specializing in endomechanical devices, including to Medtronic’s cardiovascular and orthopedic choices) gave a big increase to the enterprise in absolute phrases.

Relative revenue progress, on a per-share foundation, ought to higher inform us, particularly since Medtronic used fairness to assist finance the acquisition. Earnings per share grew from $3.02 to $5.29 (adjusted) over this era, which is a CAGR of 6.4%. Even throughout a tricky stretch, Medtronic nonetheless put up respectable numbers.

This enterprise may have achieved higher, if not for 2 critical headwinds (one in every of which isn’t the corporate’s fault). First, Medtronic’s excellent share depend elevated considerably because of that giant acquisition, making progress on a per-share foundation tougher. Second, the pandemic negatively affected Medtronic in a significant method.

The overwhelming deal with the pandemic by the worldwide healthcare advanced led to the delaying of something that may very well be delayed (reminiscent of elective surgical procedures). Worse but, key product launches coincided with the onset of the pandemic and the lessened demand. As well as, the pandemic made it troublesome to convey new provide to market. What this implies is, Medtronic has confronted challenges each on provide and demand.

However there are silver linings right here. Surgical procedures that might not be carried out beforehand are nearly definitely demand deferral, not demand destruction. These delays may very well be inflicting pent-up demand, which might be a robust driver of accelerated progress for the enterprise over the subsequent few years. Moreover, the arrival of recent merchandise to the market exactly concurrently rising demand may very well be a potent combine for the enterprise, turning a former headwind into a brand new tailwind.

Trying ahead, CFRA believes that Medtronic will compound its EPS at an annual charge of 4% over the subsequent three years. CFRA appears to be assuming that results from the pandemic will linger for a bit longer. Certainly, CFRA states: “We also see growth around 4% in FY 25 with pandemic disruptions to supply and demand finally ending, in our view.”

I suppose the important thing query for long-term buyers is that this: What sort of progress is Medtronic able to delivering over the subsequent 10+ years? That is clearly a really troublesome query to reply, however I don’t see why the enterprise can’t do no less than in addition to the final decade – a really troubled and difficult interval for the enterprise that features a international well being disaster which is unlikely to repeat once more over the subsequent decade. Seeing as how the final decade was actually fairly respectable, despite the pandemic, that truly bodes fairly effectively, in my opinion.

All that stated, near-term catalysts (pent-up demand and new merchandise) are current. CFRA dives into this a bit: “We expect strong results from [Medtronic] as its health care provider customers serve pent-up demand for procedures that had to be postponed due to the pandemic and then subsequent staffing shortages at medical facilities. [Medtronic] also stands out from medical device peers because of its product innovation and new launches, which drove market share gain during the pandemic and should continue to do so over the long term. One product line that has particularly immense potential is [Medtronic’s] robotic assisted surgery platform, which we see ultimately being adopted worldwide, up from around 13 countries using the technology in FY 23.” The robotic-assisted surgical procedure platform CFRA is referring to is Hugo, and it’s fairly a promising launch.

The close to time period is shaky, whereas the long run nonetheless seems good. I wouldn’t anticipate a lot in the best way of dividend raises over the subsequent yr or two, and that’s okay. If Medtronic can merely get again to the place it was earlier than the pandemic hit, that might arrange the enterprise for high-single digit dividend progress over the subsequent decade or so.

Beginning off with a 3%+ yield, which pays buyers to attend for that turnaround to play out, shortly paints an image the place ~10% annualized complete returns are realistically achievable – earlier than factoring in any type of a number of rerating from bettering operations. That’s not unhealthy in any respect.

Monetary Place

Transferring over to the steadiness sheet, Medtronic has monetary place that ought to strengthen over the approaching years (because the enterprise normalizes). The long-term debt/fairness ratio is 0.5, whereas the curiosity protection ratio is almost 9.

Medtronic ended final fiscal yr with practically $8 billion in money available, whereas the long-term debt load of roughly $24 billion shouldn’t be overly regarding for a enterprise of this dimension.

Profitability is barely so-so, and I’d actually wish to see pronounced enhancements on this division. Return on fairness has averaged 8.4% over the past 5 years, whereas web margin has averaged 14.1%. I just like the margins.

Nevertheless, Medtronic has been placing up single-digit ROE and ROIC for many of the final decade, and that’s mainly proper within the vary of WACC – making it troublesome to generate extra returns. Medtronic has a variety of wooden to cut right here.

Medtronic has undoubtedly misplaced a few of its shine, however a firming of demand from catch-up procedures may shortly return the enterprise again to a few of its former glory. And with IP, R&D, switching prices, economies of scale, a worldwide distribution community, excessive boundaries to entry, and a diversified portfolio of entrenched merchandise, the corporate does profit from sturdy aggressive benefits.

After all, there are dangers to contemplate.

Regulation, litigation, and competitors are omnipresent dangers in each {industry}. All three of those dangers are elevated for this enterprise mannequin compared to many different enterprise fashions, in my opinion.

Any modifications in the best way healthcare spending is managed, particularly in the USA, would nearly definitely affect the corporate.

Medtronic sometimes remembers merchandise, which includes prices and potential harm to fame.

Demand for medical gadgets is pretty disconnected from financial cycles, however a recession may trigger individuals to delay or cancel elective surgical procedures.

Any main technological modifications in medical gadgets can alter the aggressive panorama, which pressures Medtronic to continually innovate and keep forward of the tech curve.

The rise of GLP-1s could cut back and even get rid of a variety of well being points, and this might result in much less demand for a lot of medical gadgets throughout the board.

There are some dangers to significantly think about. However the valuation, which seems engaging after a 35%+ fall within the inventory’s value from its all-time excessive, also needs to be critically thought of…

Valuation

The inventory is buying and selling palms for a ahead P/E ratio of 16.5, primarily based on midpoint steerage for this yr’s adjusted EPS. That isn’t egregious in any respect for a enterprise of this stature, high quality, and market positioning.

The gross sales a number of of three.5 is effectively off of its personal five-year common of 4.3. And the yield, as famous earlier, is considerably larger than its personal current historic common.

So the inventory seems low cost when primary valuation metrics. However how low cost may it’s? What would a rational estimate of intrinsic worth seem like?

I valued shares utilizing a dividend low cost mannequin evaluation. I factored in a ten% low cost charge and a long-term dividend progress charge of seven%. To be sincere, it is a powerful one to gauge.

If we go by Medtronic’s longer-run numbers, a high-single-digit dividend progress charge isn’t an unreasonable expectation in any respect. If something, 7% is promoting the Medtronic of outdated brief. Nevertheless, for the reason that massive acquisition and the pandemic, Medtronic has been struggling. And the brand new weight-loss medication throw a wrench into issues. I’m giving Medtronic the advantage of the doubt right here, assuming the enterprise can return to some (however not all) of its former glory.

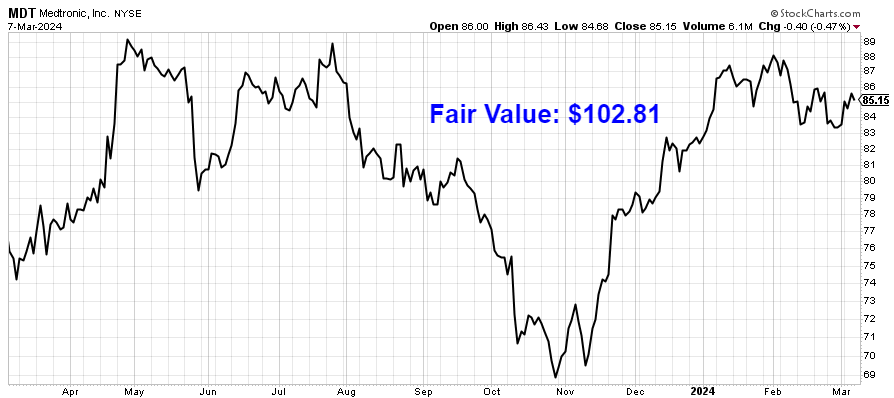

The DDM evaluation provides me a good worth of $98.44. The explanation I take advantage of a dividend low cost mannequin evaluation is as a result of a enterprise is in the end equal to the sum of all the long run money movement it might probably present.

The DDM evaluation is a tailor-made model of the discounted money movement mannequin evaluation, because it merely substitutes dividends and dividend progress for money movement and progress. It then reductions these future dividends again to the current day, to account for the time worth of cash since a greenback tomorrow shouldn’t be value the identical quantity as a greenback as we speak. I discover it to be a reasonably correct solution to worth dividend progress shares. From my vantage level, the inventory seems no less than modestly undervalued.

However we’ll now evaluate that valuation with the place two skilled inventory evaluation corporations have come out at. This provides steadiness, depth, and perspective to our conclusion.

Morningstar, a number one and well-respected inventory evaluation agency, charges shares on a 5-star system. 1 star would imply a inventory is considerably overvalued; 5 stars would imply a inventory is considerably undervalued. 3 stars would point out roughly truthful worth. Morningstar charges MDT as a 4-star inventory, with a good worth estimate of $112.00.

CFRA is one other skilled evaluation agency, and I like to check my valuation opinion to theirs to see if I’m out of line. They equally charge shares on a 1-5 star scale, with 1 star which means a inventory is a Sturdy Promote and 5 stars which means a inventory is a Sturdy Purchase. 3 stars is a Maintain. CFRA charges MDT as a 4-star “Buy”, with a 12-month goal value of $98.00.

I got here out very near CFRA’s quantity. Averaging the three numbers out provides us a closing valuation of $102.81, which might point out the inventory is presumably 17% undervalued.

Backside line

Medtronic PLC is a good healthcare enterprise benefiting from favorable demographic tendencies, secular progress, and pent-up demand. With a market-beating yield, high-single digit dividend progress, a reasonable payout ratio, greater than 45 consecutive years of dividend will increase, and the potential that shares are 17% undervalued, this Dividend Aristocrat is a primary funding candidate for long-term dividend progress buyers seeking to up their healthcare publicity.

Notice from D&I: How protected is MDT’s dividend? We ran the inventory by Merely Secure Dividends, and as we go to press, its Dividend Security Rating is 99. Dividend Security Scores vary from 0 to 100. A rating of fifty is common, 75 or larger is superb, and 25 or decrease is weak. With this in thoughts, MDT’s dividend seems Very Secure with a impossible danger of being reduce.

Disclosure: I’m lengthy MDT.

Editor’s Notice: The abstract bullets for this text had been chosen by Searching for Alpha editors.