Leonidas Santana

Introduction

If somebody requested me to clarify why I believed MercadoLibre (NASDAQ:MELI) was an important firm in only one sentence, I might say “it’s the Amazon of Latin America.” Then once they ask how the Amazon River was capable of generate internet revenue and money move, I might inform them I’ve already used up my one sentence and need them good luck.

However utilizing two sentences (or extra), I might go into depth concerning the range of MercadoLibre’s enterprise mannequin, how sticky it’s to current clients (which in flip attracts new clients) and naturally its progress charges and profitability. The No. 1 e-commerce participant in Latin America has executed nothing however execute at a excessive stage over the previous decade and for my part, will solely proceed to take action going ahead. Additionally, the cherry on high is that it is an effective way to diversify a portfolio exterior of the USA. I’ve taken a deep dive into this enterprise mannequin and estimated the intrinsic worth of the inventory to be $1,980.70. Let’s get into it.

What’s MercadoLibre’s alternative?

For starters, MercadoLibre is not a carbon copy of Amazon – nevertheless it’s a straightforward start line to conceptualize what they do and the way they earn a living. There are six components to their enterprise mannequin, with 5 of them having comparable similarities to what Amazon supplies: MercadoLibre MarketPlace vs Amazon’s e-commerce platform, Mercado Pago vs Amazon Pay, Mercado Envios logistics vs Amazon Prime/Logistics, Mercado Advertisements vs Amazon advertisements and Mercado Retailers vs Amazon Shops. The one outlier is Mercado Libre Classifieds service, which does not have an Amazon counterpart that is comparable sufficient to match.

Beginning with the MercadoLibre MarketPlace alternative, it is estimated that MercadoLibre currently controls around 21.6% of the Latin American e-commerce market. The three main gamers within the Latin American e-commerce market are Brazil, Mexico, and (arguably) Argentina – and these three nations make up 95.4% of MercadoLibre’s income. Now, the true great thing about the Latin American market is that it is nonetheless in its growth stage and facing rapid growth prospects forward. Brazil is anticipated to develop from $36.6 billion e-commerce gross sales in 2022 to $77.2 billion by 2027, representing a 111% progress. Mexico can be anticipating speedy progress with a projection from $34.2 billion e-commerce gross sales from 2022 to $68.2 billion by 2027, which is a 99% improve. Argentina is the smallest e-commerce market dimension of the three, because it’s at the moment estimated at round $7 billion in 2022. Nonetheless, the expansion charge is not any much less speedy, as that is projected to develop 111% by 2027 to achieve 109% by 2027.

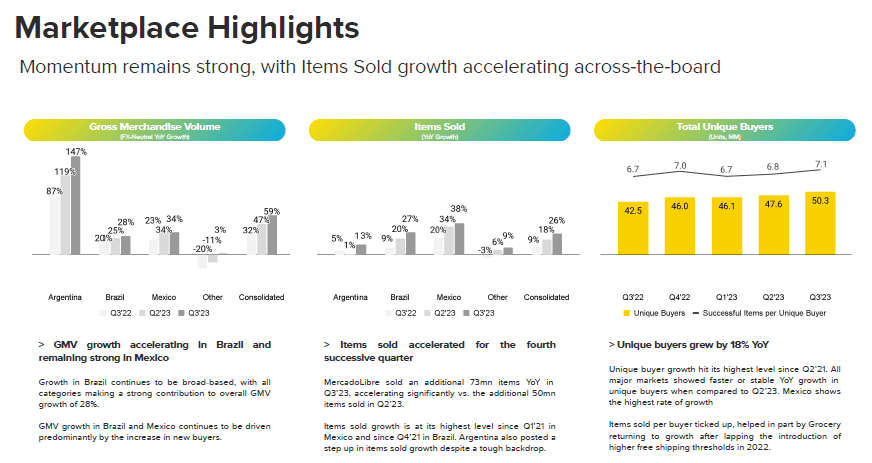

As per the beneath screenshot from MercadoLibre’s Q3 investor presentation, they’re exhibiting that they are consolidating extraordinarily effectively in these three markets. Each Gross Merchandise Quantity (GMV) and the quantity of things bought are growing quickly on a q/q foundation. The quantity of distinctive consumers has additionally elevated 18% y/y, exhibiting that they’re attracting new clients at a quick tempo.

MercadoLibre’s Q3 Investor Presentation

That is unbelievable to see as e-commerce is a really aggressive business, so it is clear that MercadoLibre is making all the fitting strikes to develop its buyer base in such an atmosphere. Buyer retention, nevertheless, is one other matter totally, which is the place MercadoLibre actually shines with its sticky enterprise mannequin.

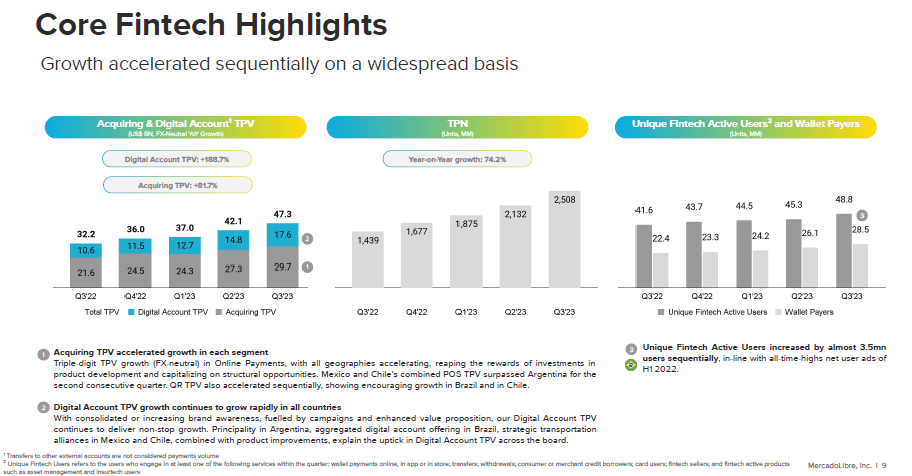

The primary aspect of that is Mercado Pago, which is MercadoLibre’s digital funds platform, however deeply built-in throughout the MercadoLibre ecosystem. Sticking with the comparability theme, it is fairly just like PayPal (PYPL) (which I beforehand wrote an article on here), however particular to MercadoLibre and the Latin American market. Clearly, this can be a draw back because it means that it’ll have difficulties being adopted exterior of Latin America – however its weak point can be its energy. Individuals who need to purchase objects on MercadoLibre MarketPlace will determine to make use of Mercado Pago. Then again, individuals who need to use Mercado Pago will purchase issues on MercadoLibre MarketPlace. Each of those act in flip to draw and retain clients, and due to this fact enhance income and revenue. Nonetheless do not simply take my phrase for it, see the beneath screenshot from MercadoLibre’s Q3 investor presentation. Complete Cost Quantity (TPV) for my part is an important metric used to measure the success of a digital fee platform and has been quickly growing every quarter. In Q3 of 2022, this was measured at $32.2 billion and has now grown to $47.3 billion in Q3 of 2023 – a rise of 46.9% y/y. This could proceed to extend because the Latin American market continues to develop. One other fascinating level is the quantity of distinctive customers which might be on the fintech platform rose to 48.4 million in Q3. Contemplating that Latin America at the moment has round 300 million on-line purchasers, Mercado Pago accounts for round 16% of the market, which isn’t dangerous in any respect.

MercadoLibre’s Q3 Investor Presentation

The second a part of their sticky enterprise platform is Mercado Envios logistics. As soon as a buyer buys a product by way of Mercado Libre MarketPlace and pays with it by way of Mercado Pago, they’ll then have it delivered to them by MercadoLibre’s logistics community. This community can be extraordinarily aggressive throughout the Latin American Market. As of Q3, Mercado Libre accounts for 48% of all shipments throughout its jurisdiction. Additionally, its complete managed community penetration reached a report stage of 94.2%, which is nice to see them holding every thing in-house and sustaining a stage of management.

There may be additionally an important alternative with MercadoLibre advertisements and Mercado Retailers. Whereas I do not anticipate both of those two to take over the world anytime quickly, they undoubtedly can have a spot throughout the Latin American Market. Contemplating the present inhabitants of Latin America is 650 million (practically double the inhabitants of the USA), there needs to be an honest slice of income they will seize. Nonetheless, it’s arduous to measure how a lot this will probably be contemplating Amazon, Meta and Google virtually dominate the promoting business worldwide. Mercado Retailers then again I anticipate to carry out effectively, because it integrates effectively inside their enterprise mannequin. Clients will purchase objects by Mercado Pago from shops arrange on Mercado Retailers and have them delivered by way of Mercado Envois logistics.

General, MercadoLibre has a robust ecosystem that may entice and retain clients and in flip will probably be tough to disrupt. It’s because as soon as a shopper has been uncovered to the system, it will likely be very tough for an additional firm to persuade them the grass is greener elsewhere, which exhibits up within the spectacular double-digit progress charges.

What about MercadoLibre’s administration crew?

MercadoLibre’s administration crew has confirmed they’re able to executing their enterprise mannequin. There was a current shakeup with Martín de los Santos taking up as the brand new CFO from Pedro Arnt in August 2023. There may be each good and dangerous information with this transformation. The excellent news is that Martín has been with MercadoLibre since 2007 as a board member, which exhibits loyalty. The dangerous information is that MercadoLibre has been executing extraordinarily effectively, so seeing a possible change in how they carry out is not precisely excellent. I consider Martín will do effectively, nevertheless, we’ll have to double-check his efficiency in each the upcoming quarter and Q1 of 2024.

In any other case, Marcos Galperin (the CEO) has executed a beautiful job constructing this firm up from scratch and working it in the present day, so hopefully he’ll keep round for so long as he can.

What about MercadoLibre’s monetary place?

MercadoLibre’s financials are in an excellent place. For the complete 12 months 2022, they printed over $2.49 billion in FCF and $9.54 in EPS. These numbers have already been crushed within the first 3 quarters of 2023, as they’ve up to now reported $2.88 billion in FCF and a whopping $16.29 in EPS. Whereas no steering has been offered for This autumn, I might anticipate this to be a report quarter for MercadoLibre because of their confirmed progress technique and all the primary consuming holidays being positioned on this quarter (together with Black Friday and Cyber Monday).

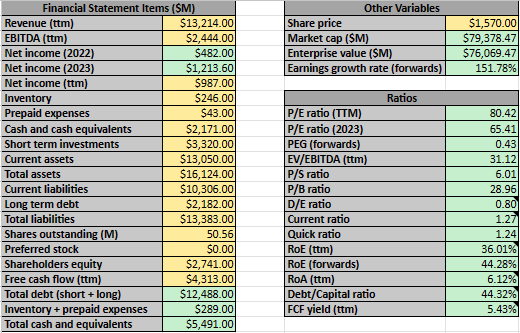

Concerning their stability sheet, MercadoLibre at the moment has $5.49 billion in money and money equivalents and $2.14 billion in long-term debt. This implies in the event that they wished to, they may repay all their debt comparatively rapidly and nonetheless have money to burn. Please see my beneath abstract of MercadoLibre’s key metrics:

Writer’s Calculations

At first look, this inventory appears extraordinarily overvalued, however appears will be deceiving. MercadoLibre usually trades with a trailing P/E within the 40 to 90 vary. Given the present TTM P/E of 80 we’re undoubtedly in the direction of the higher finish of the vary, nevertheless be mindful the expansion charge this firm is experiencing – which is demonstrated by the exceptionally low PEG ratio of 0.43

MercadoLibre additionally usually trades with a trailing EV/EBITDA of 30 to 90 – so at the moment TTM EV/EBITDA of 31.12 we look like buying and selling low cost – not in absolute phrases a minimum of, however in relative phrases. The business median trailing P/E and EV/EBITDA ratios are roughly 14.5 and 11.1 respectively, which MercadoLibre is clearly buying and selling above. General, these are clearly blended outcomes.

Concerning the stability sheet ratios, practically all of those are good with some being fairly wonderful which might be extremely uncommon to see. A TTM RoE of 36% is unquestionably high tier and there’s a robust FCF yield. The present and fast ratios above 1.0 additionally point out there’s a low monetary threat to the corporate. The P/B ratio is extraordinarily excessive at 28.96, nevertheless, the one arduous belongings they actually have are their warehousing/storage models – and their PP&E marks up roughly 7% of their complete belongings for reference. General, MercadoLibre has positioned itself ready of energy.

What’s MercadoLibre’s intrinsic worth?

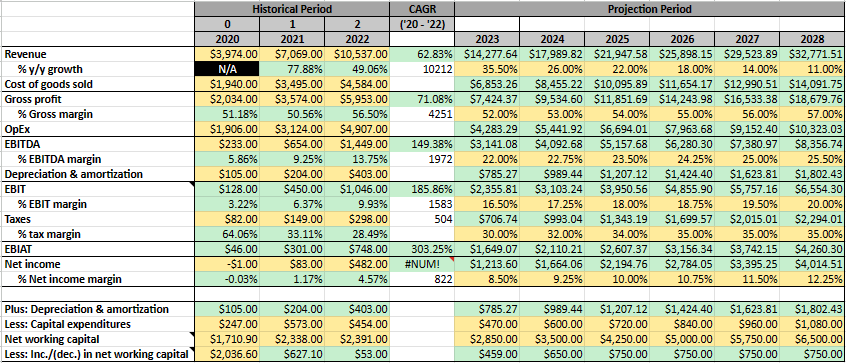

As per my final article, I’ve additionally determined to undertake 3 totally different approaches to find out the truthful worth per share of MercadoLibre’s inventory. I’ve additionally put collectively the beneath monetary projections primarily based on the place I consider MercadoLibre is headed:

Historic financials and projections

Writer’s Calculations

As talked about earlier, no official steering has been offered. I do consider nevertheless that MercadoLibre will proceed to develop income quickly primarily based not solely on their confirmed previous efficiency but additionally as a result of quickly rising Latin American markets, the penetration they’ve developed inside these markets, and naturally, the standard companies they supply to their clients. Nonetheless, to be on the protected aspect, I’ve quickly decreased their y/y progress percentages to achieve 11% by 2028.

I might additionally anticipate margin growth to proceed at a continuing charge, as MercadoLibre expands and cost-cutting measures come into play – boosted by the everyday advantages of getting an built-in ecosystem working together with an financial system of scale.

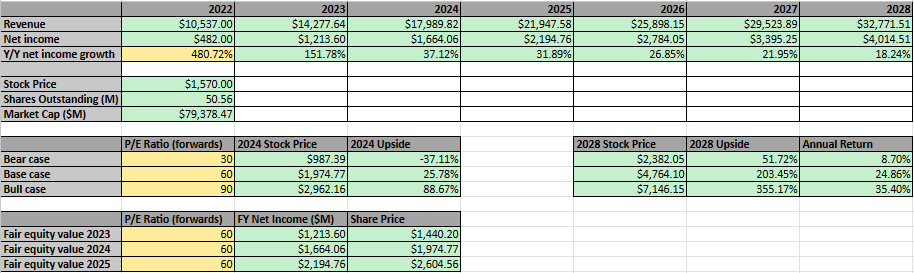

Internet revenue evaluation

Writer’s Calculations

I’ve determined {that a} present truthful P/E for MercadoLibre is round 60. Whereas that is undoubtedly fairly excessive, I consider that their robust monetary place and progress charges demand this premium. As compared, Amazon is at the moment buying and selling with a ahead P/E of round 55, which is near the 60 I selected. Bear in mind, with the expansion charges they need to be placing up, this time subsequent 12 months their present 67 P/E will drop to round 45.

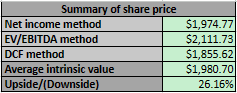

Assuming they hit my projected internet revenue of $1.66 billion in 2024, the truthful value of MercadoLibre at the moment needs to be round $1,974.77 – giving us a 25.78% upside from the present value.

As well as, this 60 P/E implies that the share value will attain $4,764.10 if my projections are appropriate – which suggests a 203.45% return.

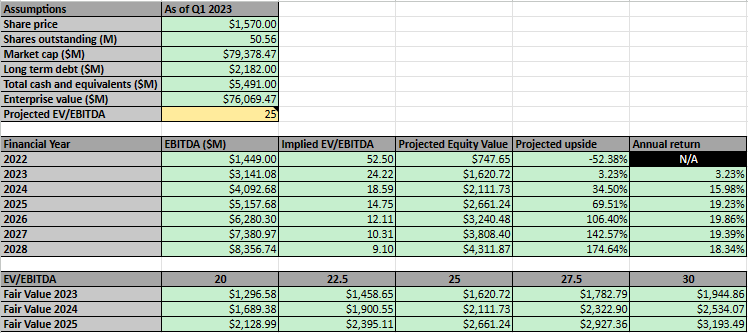

EV/EBITDA evaluation

Writer’s Calculations

I’ve determined that MercadoLibre ought to have a base case EV/EBITDA of 25. Once more, that is comparatively excessive, however for a similar causes as above, I feel that this premium is deserved. As well as, that is truly decrease than their present projected ahead EV/EBITDA of round 28.5, which implies this is not out of the working.

Utilizing this, the truthful worth for MercadoLibre needs to be round $2,111.73 per share primarily based on the EBITDA they need to be printing for 2024. I’ve additionally offered calculations for EV/EBITDA ratios increased/decrease than 25 if you would like this adjusted.

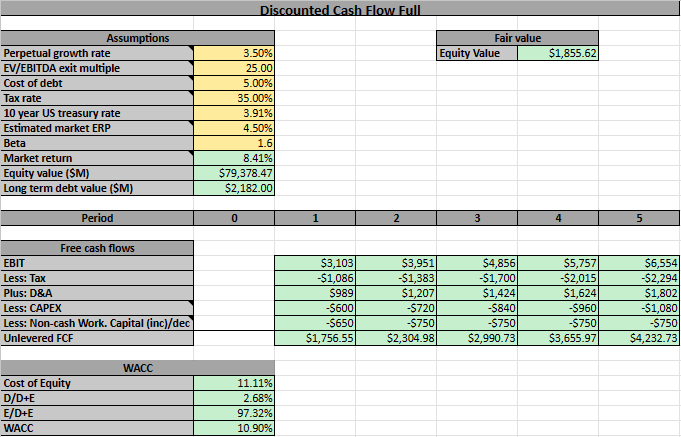

DCF evaluation

Please see the beneath DCF evaluation, the place I calculated the terminal worth utilizing the common of the EV/EBITDA exit a number of technique and WACC technique:

Writer’s Calculations Writer’s Calculations

I consider an acceptable perpetual progress charge for MercadoLibre is 3.5%. This isn’t solely as a result of quickly rising industries this firm operates in but additionally that they are particular to the Latin American market that’s anticipated to undergo a speedy growth cycle. I feel 3.5% is greater than truthful.

Their price of debt was estimated utilizing their newest 10-Q and I used an efficient tax charge of 35% primarily based on what they’ve traditionally paid. For the risk-free charge, I’ve selected utilizing the 10-year US treasury charge, which was 3.91% on the time of writing.

MercadoLibre’s present beta is 1.6 and I used a market return of 8.41%, which I calculated primarily based on the present estimated market ERP (round 4.5%)

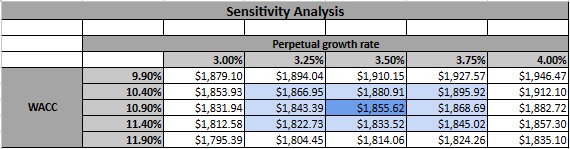

I’ve run the calculations and located a justifiable share value of roughly $1,855.62. Similar to in my earlier article, I’ve offered the beneath sensitivity evaluation, for those who suppose I have been too aggressive/conservative.

Writer’s Calculations

Common share value

Taking the averages from these 3 strategies, I’ve discovered an intrinsic worth for MercadoLibre’s share value of $1,980.70, which is a 26.16% upside from the present share value.

Writer’s Calculations

What are the dangers to MercadoLibre?

Like all firm, there are in fact dangers to MercadoLibre’s enterprise mannequin which can have an effect on my projections

Firstly, as I hinted at earlier, competitors is extremely robust in each the e-commerce and fintech house. MercadoLibre goes to be competing of their market towards the likes of Alibaba, Sea Restricted and naturally, Amazon. MercadoLibre is at the moment holding its personal and has grown market share since 2020, nevertheless in the event that they drop the ball or corporations like Alibaba and Amazon determine to shovel their hundreds of thousands of {dollars} into attacking the Latin American market – it might spell huge bother for MercadoLibre.

Secondly, there’s financial threat usually. After all, MercadoLibre has proven they will nonetheless carry out effectively even in a troublesome financial atmosphere, because the South American financial system has been doing poorly since 2020, so I consider this threat is low general. Nonetheless, inflation has additionally been a scorching matter lately and Argentina has been hit closely – reporting inflation charges of over 100%. Whereas that is clearly dangerous for Argentina’s financial system, MercadoLibre does get a constructive aspect from this. Mercado Pago turned a approach to combat towards inflation by buying and selling the Argentine Peso for safer belongings and defending their clients’ internet value. In flip, this elevated the adoption charge of Mercado Pago.

Thirdly, political/regulatory dangers. Counties exterior of the West aren’t usually recognized for working free and truthful democracies – and South America is not any exception. If a number of the nations MercadoLibre operates in begin to develop into extra aggressive on the political stage, or they begin to unfairly push by rules – then there could also be downstream (or maybe even purposeful) results on MercadoLibre’s efficiency.

Conclusion

Primarily based on the evaluation I’ve performed, I consider MercadoLibre is at the moment undervalued and due to this fact a purchase. The corporate has a powerful historical past of confirmed outperformance in addition to a promising future with lifelike progress and revenue ventures forward.

I feel the one actual dangers to MercadoLibre are competitors and the overall financial atmosphere they function in. Competitors clever, they’re going to want to make sure they maintain tabs on what the likes of the massive boys are doing, equivalent to Alibaba and Amazon. In the future, a minimum of one among them will probably determine to open the floodgates and strike arduous on the Latin American market – a day that MercadoLibre must be anticipating and ready for. Concerning the financial threat, they’ve confirmed they will execute in poor financial environments after exhibiting their efficiency post-2020. Nonetheless, a weaker financial system usually isn’t excellent for e-commerce or fintech corporations. That is very true if occasions happen in Latin America that trigger an general slowdown in how they develop their financial system/infrastructure, equivalent to a change in management that pushes political instability or regulatory frameworks.

All in all, the factor that I like most about MercadoLibre is that it is a unbelievable maintain for the long run. We now have numerous examples of how buyers profit from shopping for unbelievable corporations whereas they’re nonetheless of their progress part and are actually reaping the rewards 10 years later. After I take into consideration the place MercadoLibre will probably be in in the event that they proceed executing for the following 10 years, then it will simply develop into one other instance of individuals wishing that they had purchased in.