LIONEL BONAVENTURE/AFP by way of Getty Photographs

I used to be unsuitable about Meta Platforms (NASDAQ:META).

I bought my shares of the inventory for $186/share in March of final yr, locking in small income.

On the time I used to be happy to make the most of what I assumed is perhaps a short-term rally.

I needed to get out of an organization that I not trusted due to its large metaverse spending. I seen administration as irresponsible and borderline loopy. And due to this fact, I used to be joyful to exit my place since I used to be not within the purple and had the chance to make some cash whereas transferring onto what I assumed have been higher alternate options.

Effectively, with the advantage of hindsight, I could not have been extra unsuitable and my timing right here could not have been worse.

Shortly after I made that commerce, Mark Zuckerberg introduced his plans of a “year of efficiency” which despatched shares hovering.

This announcement triggered META shares to spike by 20%.

On the time, I did not purchase again into the inventory due to belief points.

Speak is reasonable, I informed myself.

It is simple to speak about decreasing capex; nevertheless, it appeared unlikely that we might see a complete pivot after the corporate’s title change and overt concentrate on moonshot concepts surrounding the metaverse.

I wasn’t positive that Zuckerberg had it in him to swallow his satisfaction, backtrack, and concentrate on what the corporate does greatest (digital promoting with its social media platforms).

However, he did not simply speak the speak right here, he walked the stroll.

Kudos to him…and everybody who believed in his messaging.

Meta has an incredible yr in 2023 and I largely missed out.

During the last yr, META diminished its headcount by greater than 22%.

The corporate’s capex continues to fall every quarter.

And but, Meta’s fundamentals proceed to rise.

It is uncommon to see an organization can slash spending whereas nonetheless rising income.

However, META has completed simply that. This resulted in robust margin growth and finally, big income.

These income triggered META’s share value to soar.

In 2023, META generated triple digit whole returns trying forward, I feel META shares will proceed to outperform.

What’s extra, META introduced a brand new dividend throughout its most up-to-date quarter, which meant that these shares at the moment are included on my dividend development compounder screens.

Now, when stacked up towards my different favourite dividend development shares, META’s fundamentals shine.

I feel this firm has the prospect to turn out to be one of many strongest dividend compounders on planet Earth and due to this fact, final week I ate somewhat crow, swallowed my satisfaction, and rebought these shares that I bought final yr (and some extra as effectively) at a value that was greater than 2x the scale.

I initiated a large META place at $476.04 after its This fall earnings and now this firm sits on the prime of my private watch checklist, when it comes to firms I need to add extra of when money turns into out there to speculate.

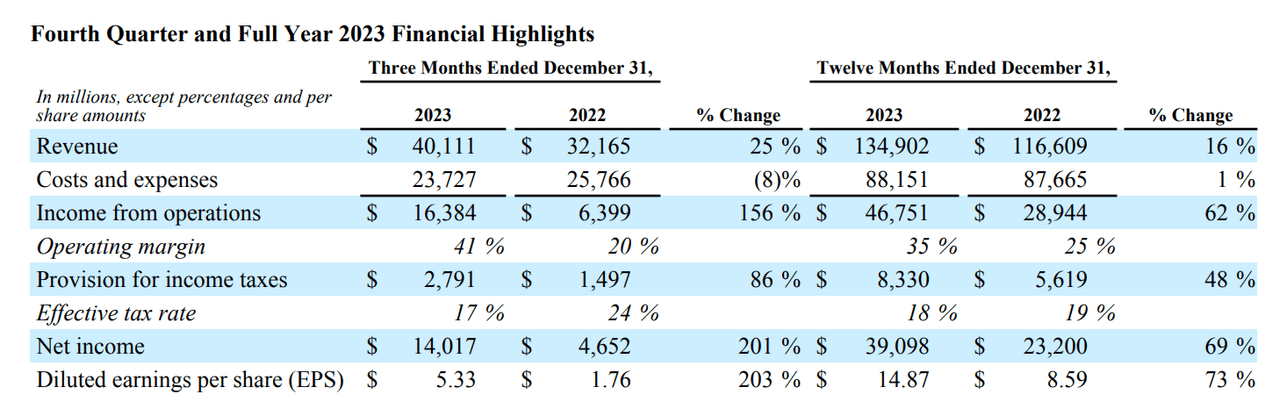

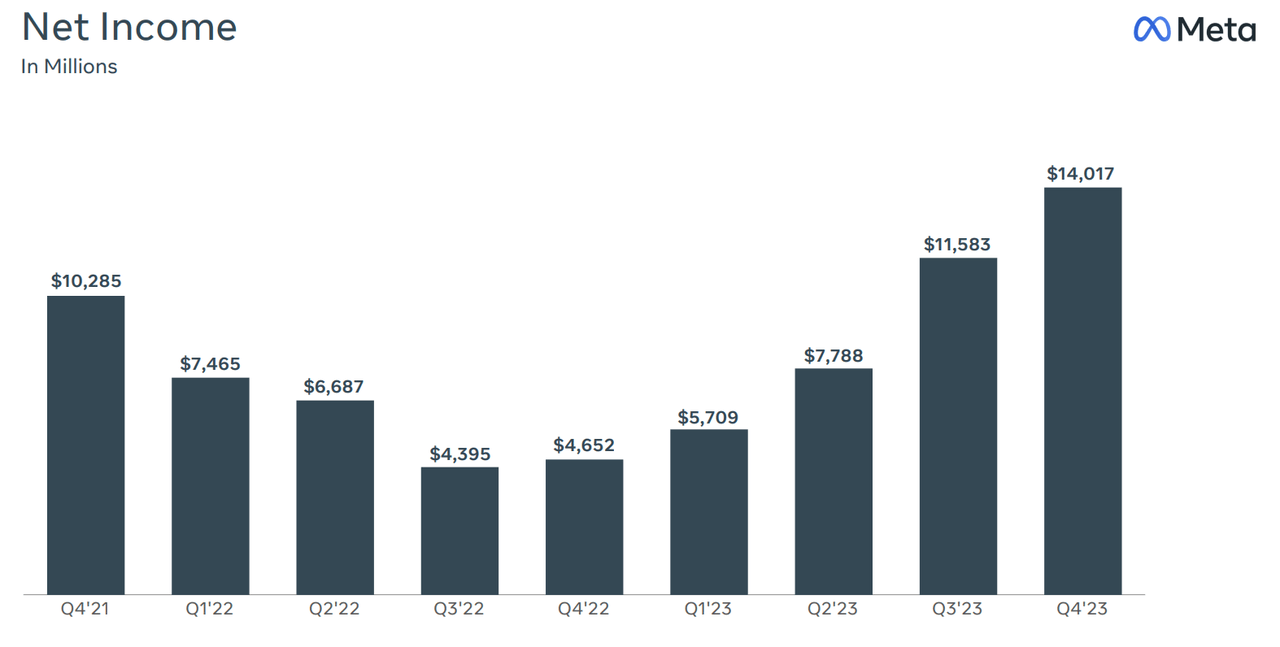

This fall/Full-Yr Outcomes

Through the fourth quarter, META’s revenues got here in at $40.1b, up by 25% on a y/y foundation.

For the full-year, META produced $134.9b in gross sales, up 16%.

As you possibly can see under, META’s bottom-line outcomes accelerated at a tempo far past these income development charges, because of the firm’s concentrate on value reducing and margin growth.

META This fall ER

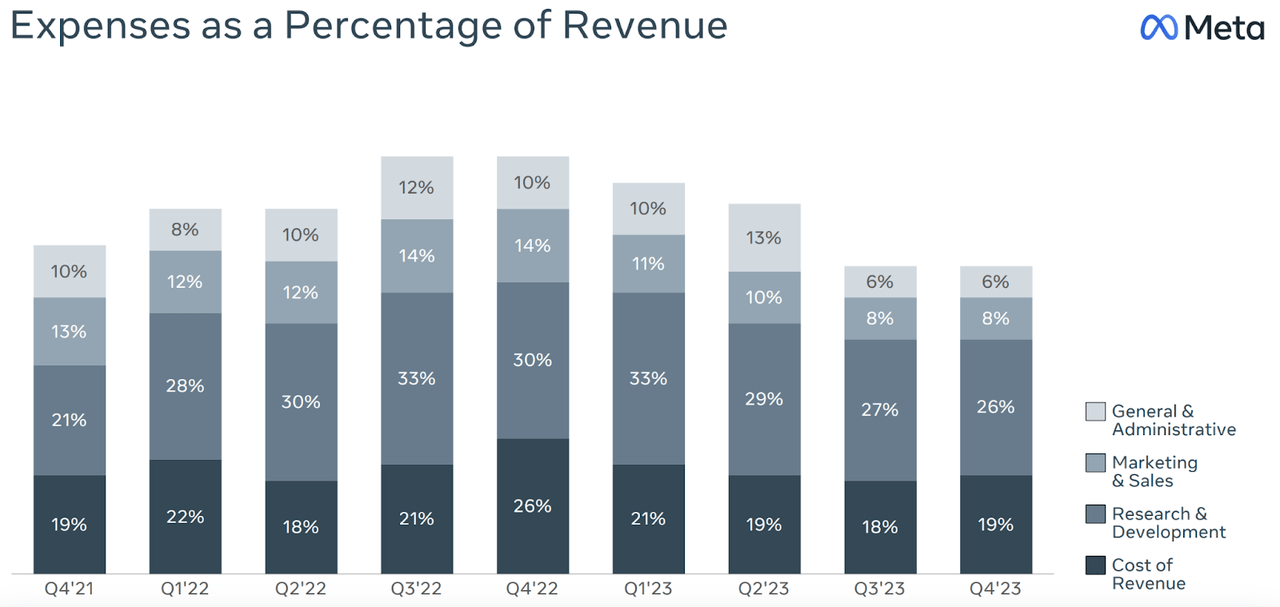

This chart clearly exhibits the success of the “Year of Efficiency” that Zuckerberg highlighted final yr.

META This fall ER Presentation

As you possibly can see, capex is falling and that is resulting in monumental money flows.

META This fall ER Presentation

META diminished its annual capex by roughly $4b throughout 2023, or roughly 12%.

And but, this does not seem to have damage the corporate’s merchandise.

META’s household of app’s day by day common consumer development remained in place throughout This fall and 2023 total.

Through the fourth quarter, greater than 3.1 billion folks estimated to go to its ecosystem.

On a month-to-month foundation, practically 4b individuals are estimated to have visited this firm’s ecosystem.

Take into consideration that. There’s an estimated 7.89b folks on Earth proper now. That signifies that Meta’s platforms are utilized by greater than half of the human inhabitants on a month-to-month foundation.

This demand leads to robust pricing energy for the corporate when promoting adverts.

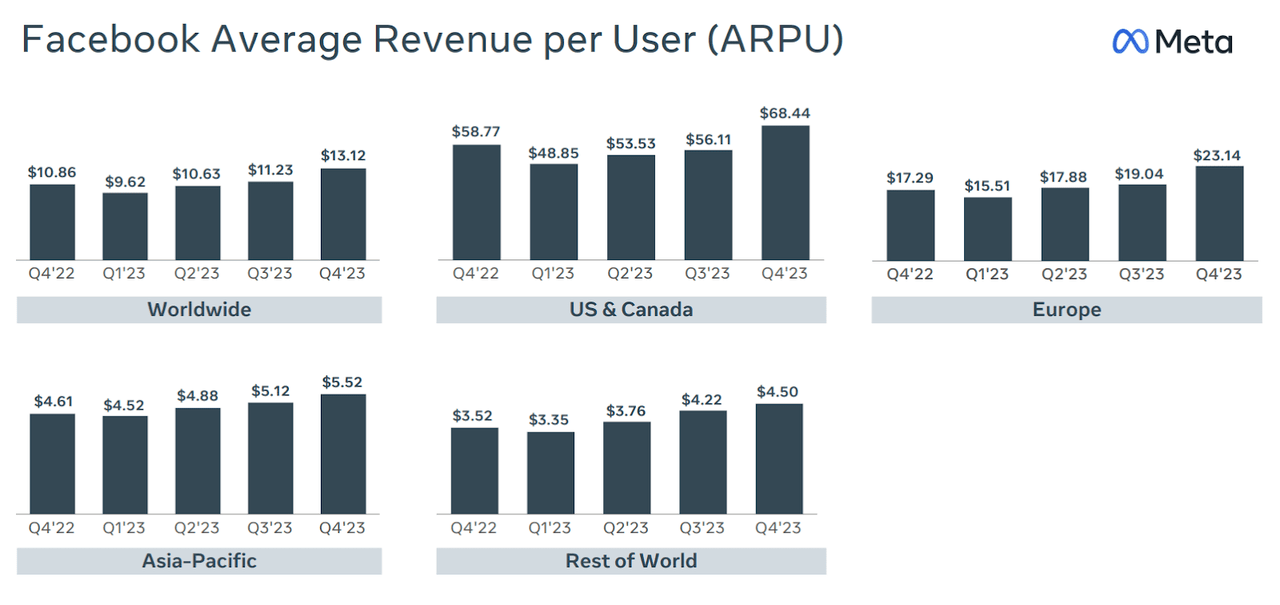

Meta’s common income per consumer (ARPU) posted optimistic development in each geographic area in each quarter throughout 2023.

The consistency of that development/execution is superb.

META This fall ER Presentation

Sure, this 2023 success units up powerful 2024 comps for the corporate within the coming quarters; nevertheless, as long as Meta stays disciplined with its capital spending, I feel it may proceed to extend margins and generate rising income even when we see consumer development stagnate.

This expectation for continued margin growth, alongside the potential advantages of economic engineering by way of META’s large buyback (the corporate licensed an extra $50b of share repurchases through the This fall consequence), leads to robust bottom-line development expectations in 2024.

And rising earnings and free money flows ought to lead to rising shareholder returns as effectively.

To me, this turned META from a considerably speculative development play right into a sleep effectively at night time dividend development inventory (actually, over night time).

And now I am a cheerful shareholder with plans to purchase & maintain over the long-term.

Shareholder Returns

I would be mendacity if I mentioned that META’s new dividend wasn’t the driving power behind my current buy.

To some, this measly dividend yield won’t appear essential. However to me and my investing technique, it is all the things.

Positive, the corporate’s fundamentals are implausible, however they have been that approach all yr.

Frankly, I did not really feel the necessity to personal META once I already had chubby positions in high-growth, big-tech performs like Alphabet (GOOGL), Amazon (AMZN), and Nvidia (NVDA) which do not actually issue into my passive revenue stream (sure, NVDA pays a dividend, however even with a really giant place, its 0.02% yield signifies that these shares do not play a major position in my dividend snowball).

Nevertheless, the brand new dividend modified that calculus.

For some time now, I’ve mentioned that firms like Meta, Alphabet, and even Amazon may turn out to be main gamers within the dividend development house. Nevertheless, trying on the firms’ fundamentals, thought that Alphabet would the primary one to make that transfer. I used to be unsuitable about that too, however this is to hoping that Alphabet’s administration sees the market’s response to META’s earnings and adopts a yr of efficiency-like mindset as effectively.

Positive, proper now, META’s yield can also be fairly low (simply 0.43%). However, this buy is not in regards to the yield within the current. It is about my expectations for META to persistently develop that dividend over time – at an above common fee – placing this firm into very uncommon air in relation to its shareholder returns profile transferring ahead.

To me, META now falls into the identical fantastic class as blue chip shareholder return performs similar to Apple, Microsoft (MSFT), Visa (V), Mastercard (MA), and MSCI (MSCI).

Shares like these are at all times excessive precedence buys for me, anytime they’re buying and selling at or under honest worth, due to the power of their compounding potential.

Clearly META hasn’t had time to determine a dividend development observe file, however now that administration has initiated its dividend, I consider that cat is out of the bag and I’ve excessive hopes for dividend development transferring ahead.

I think that they’ve seen the success that different very beneficiant development firms have had with regard to adopting disciplined capital constructions, returning money to shareholders, and nonetheless having robust sufficient money flows to spend large quantities of cash on R&D and different growth-oriented capex, to maintain the compounding machines working.

I additionally would not be stunned if this transfer can set META aside from different development tech performs in relation to engaging human capital as a result of the brand new dividend differentiates their share from most different silicon valley firms in relation to share primarily based comp.

I noticed a slew of articles final week noting that Mark Zuckerberg can be making roughly $700m per yr from META’s new dividend.

Clearly he owns essentially the most shares and albeit, does not want the cash both approach, however I’ve to consider that I am not the one one that sleeps effectively at night time whereas my shares present passive revenue and due to this fact, I feel the money flows and relative stability that comes with shares that present rising shareholder returns will assist to engaging (and keep) prime expertise.

META’s new dividend is not the one similarity that I am seeing in comparison with Apple.

For years, META was recognized for its pristine stability sheet. This firm was flush with money and had zero long-term debt. Effectively, in 2022 that started to alter.

The corporate ended 2022 with $9.92b in long-term debt.

That determine rose to $18.39b by the tip of 2023.

And whereas I liked META’s former stability sheet, I am truly joyful to see them make the most of leverage, alongside their rising shareholder return applications, as a result of even in as we speak’s rate of interest surroundings, META generated very robust ROIs final yr with debt-fueled buybacks and over the long-term, I think that this can proceed to be the case whereas its rising is EPS/FCF’s at such a powerful fee.

To me, it seems to be like META is taking a web page out of Apple’s “cash neutral” playbook. META’s money place is not practically as giant as Apple’s, however proper now, it is sitting on $65b of money/money equivalents (and $43b of annual free money flows), which provides it a whole lot of monetary flexibility in relation to rising leverage with out placing its stellar AA- credit standing in danger.

With all of that in thoughts, I count on to see META proceed to purchase again tens of billions of {dollars}’ value of shares every year whereas additionally elevating the dividend.

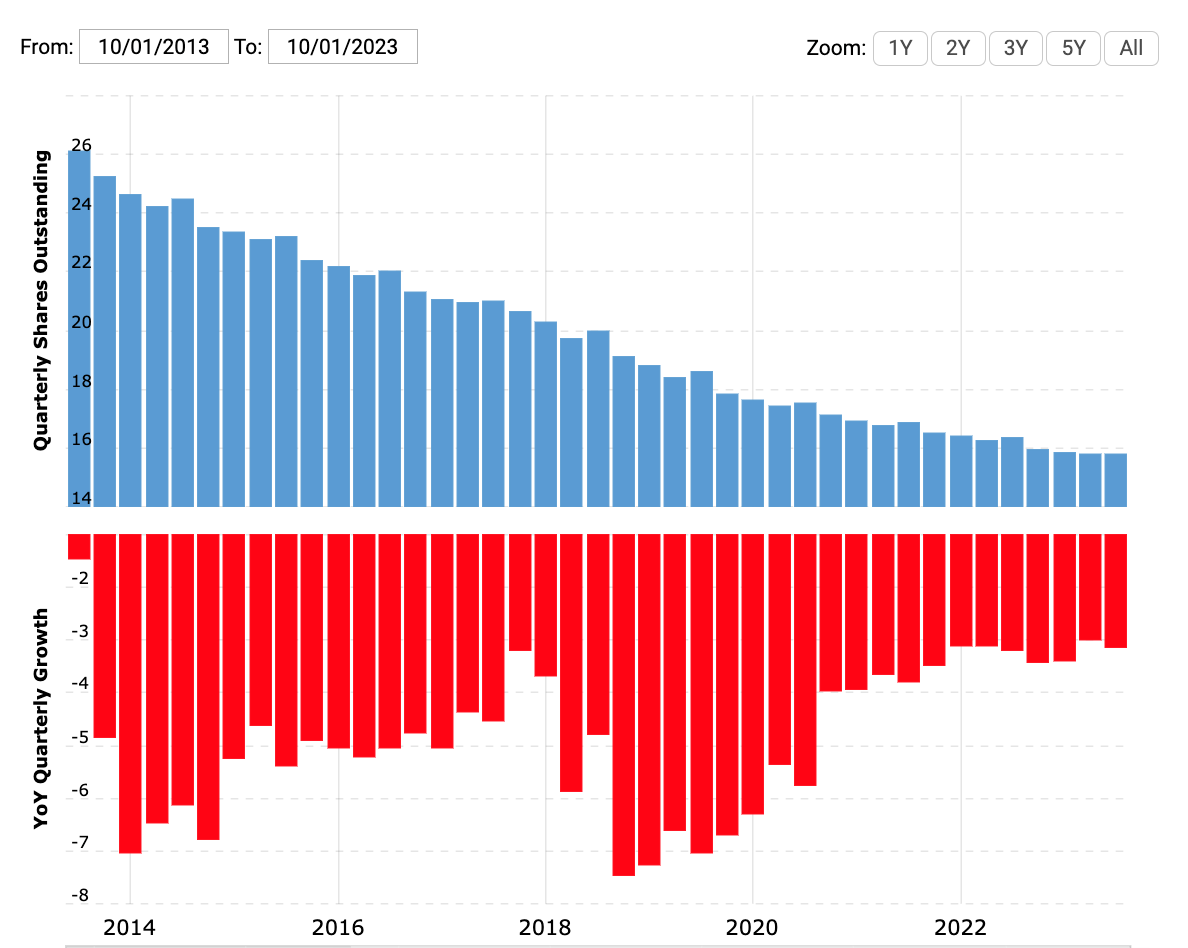

As META’s self-discipline, with regard to headcount and share-based comp discount continues, these buybacks will turn out to be increasingly environment friendly, with regard to decreasing the corporate’s excellent share counts.

Now {that a} dividend is in play, I think that decreasing its excellent shares will turn out to be increasingly of a precedence as a result of each share retired by a buyback program reduces the burden of the general dividend on the corporate’s money flows.

In brief, I consider that META has what it takes to observe in Apple’s footprints in relation to a mature, big-tech title with large money flows…

During the last 10 years, AAPL has diminished its excellent share rely by 39.4%.

Macrotrends

Throughout this similar time period, on a split-adjusted foundation, AAPL’s dividend has elevated from $0.1089/share to as we speak’s $0.24/share degree on a quarterly foundation.

In different phrases, AAPL’s dividend has elevated by greater than 120%.

I may simply see META’s share rely and dividend development in an identical route over the approaching decade as effectively. Due to this fact, I felt compelled to get into this firm on the floor flooring (with regard to its just lately initiated dividend). Clearly META and APPL aren’t an ideal apples to apples comparability right here, however I see too many similarities between the 2 capital return tales to keep away from META any longer.

Investing in AAPL shortly after it initiated its dividend was top-of-the-line selections I’ve ever made available in the market. If I’ve even half that a lot success with these META shares, it’ll speed up my journey in direction of monetary freedom in a giant approach.

Valuation

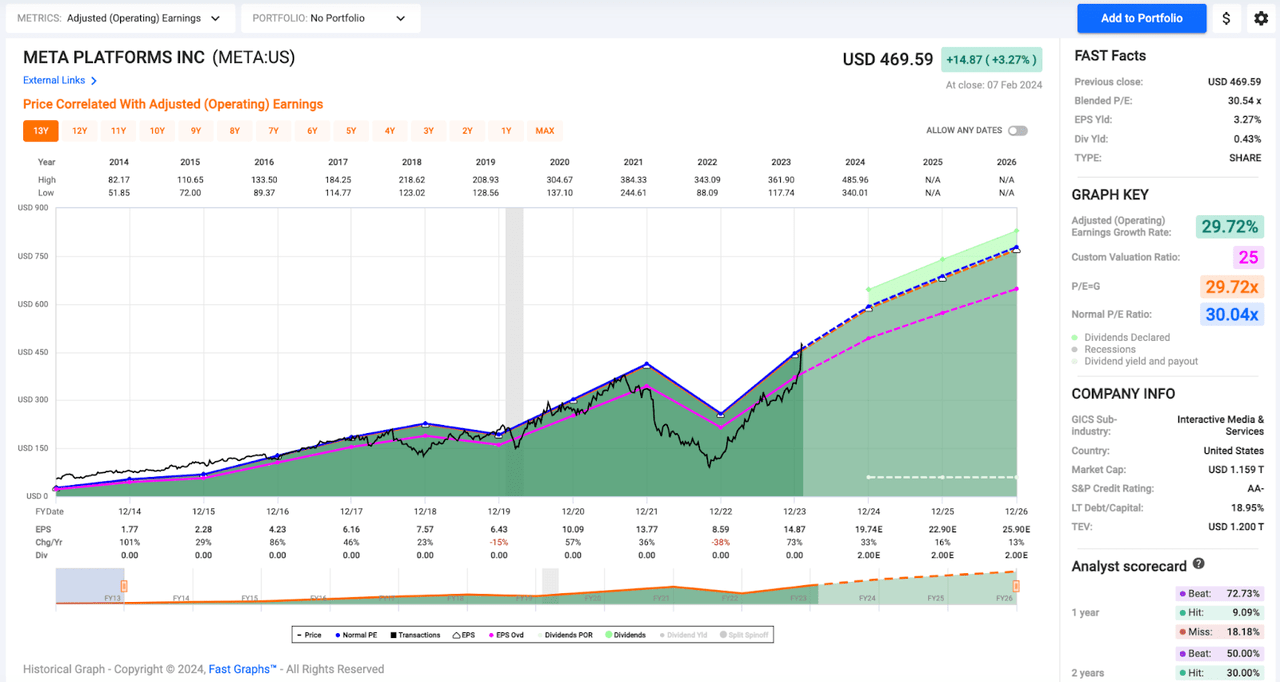

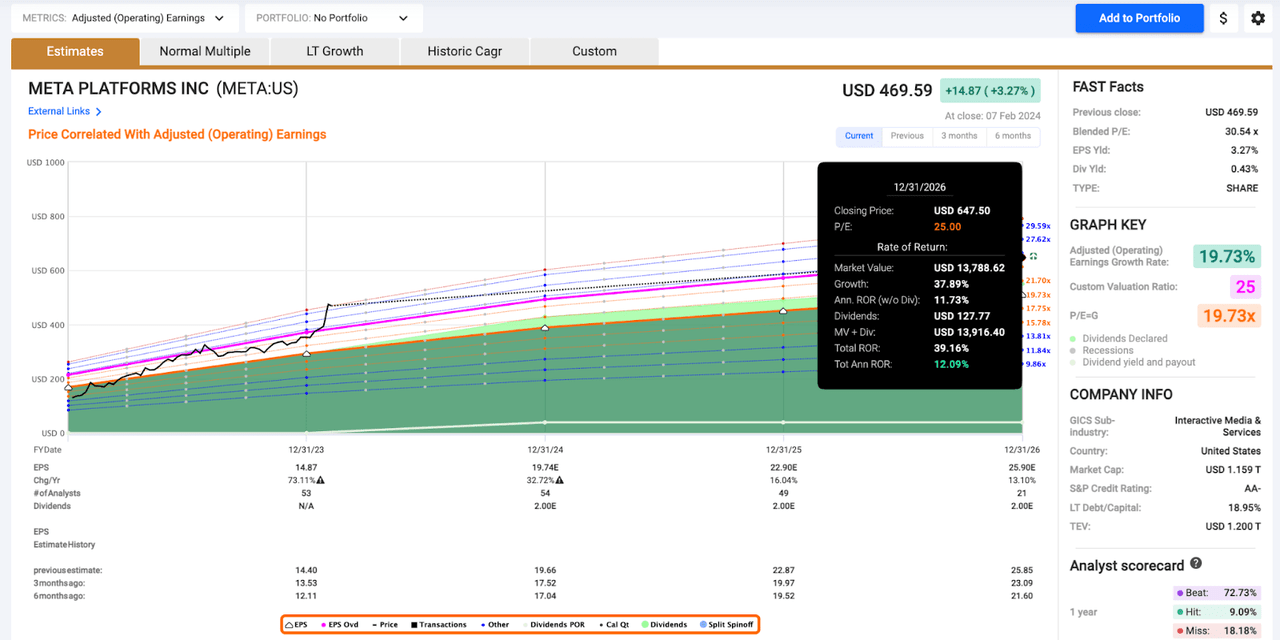

I consider {that a} ~25x ahead P/E a number of represents a conservative honest worth for META.

This degree is marked on the chart under by the pink line, which, you may discover, represents a major low cost to META’s historic common P/E of ~30x.

FAST Graphs

At that degree, META would nonetheless be cheaper than all the firms I in contrast it to earlier than…

- Apple at the moment trades with a ahead P/E a number of of 28.8x

- Microsoft at the moment trades with a ahead P/E a number of of 35.7x

- Visa at the moment trades with a ahead P/E a number of of 28.1x

- Mastercard at the moment trades with a ahead P/E a number of of 32.1x

- MSCI at the moment trades with a ahead P/E ratio of 39.8x

Effectively, not solely is META buying and selling at a reduction to its friends – it is buying and selling at a reduction to that concentrate on honest worth a number of.

As we speak, Wall Road consensus for META’s earnings in 2024 is $19.74. As I write this, META’s share value is $468.65. Due to this fact, we’re speaking a few ahead P/E a number of of simply 23.7x.

25x that $19.74/share earnings estimate is $493.50.

That is the place my honest worth lies (and albeit, I would not be stunned to see this determine rise because the yr strikes on as a result of would not be stunned to see META proceed to beat earnings).

With that in thoughts, META’s present share value represents a ~5% low cost to honest worth.

Even with my comparatively conservative 25x goal a number of, META nonetheless provides robust upside whole return prospects.

If the corporate meets analyst EPS development estimates over the subsequent 3 years, then we’re taking a look at a complete annualized return CAGR of ~12% from right here.

FAST Graphs

And, if META does see a number of growth by way of imply reversion again as much as that 30x degree, then we’re speaking a few whole return CAGR north of 19% per yr between now and the tip of 2026.

I am content material with 12%, however I feel life like upside to the 20% vary ought to be thought of when serious about shopping for shares.

Dangers To Think about

The first danger to this bullish thesis is solely administration execution.

I am basing my bullish outlook and honest worth goal on Meta technology practically $20.00 in EPS throughout 2024 and if that does not come to fruition then I can be pressured to cut back my honest worth estimate.

If administration decides to backtrack and aggressively allocate capital towards low ROI capex then it is like that Meta is not going to meet its goal.

Nevertheless, it appears clear that they’ve totally purchased into the yr of effectivity mantra and this disciplined administration will proceed transferring ahead (I can be monitoring issues like headcount, share primarily based comps, and share primarily based comp as a proportion of free money move, transferring ahead).

The promoting market is economically delicate. Buyers ought to perceive this and settle for a possible slowdown if we enter right into a deep recession. Nevertheless, even on this occasion, I nonetheless consider that the digital advert house has secular tailwinds and even in a down promoting market, leaders within the digital advert house like Meta, Amazon, and Alphabet will proceed to take market share away from legacy avenues like print and cable tv.

What’s extra, there can be a ton of political advert spending in 2024, so that ought to bolster the advert surroundings within the short-term. This may create powerful comps in 2025; nevertheless, my present honest worth is not primarily based upon outsized development subsequent yr. To justify my 25x P/E goal, Meta would solely must develop at a 12-15% clip in 2025 (which, as you possibly can see on the chart above, is effectively under their long-term historic common), assuming that they hit consensus development estimates of practically 35% in 2024.

Conclusion

It wasn’t way back that I used to be promoting shares right here due to worries round capital self-discipline and misguided investments.

Effectively, what a distinction a yr makes.

I have been amazed by administration’s self-discipline over the last yr or so.

Now, when taking a look at META’s valuation, development prospects, stability sheet, and shareholder return insurance policies this can be a very simple firm to purchase and maintain at as we speak’s ranges.

With the advantage of hindsight, I want I hadn’t bought META a yr or so in the past. However, I haven’t got entry to a working time machine.

Residing in a puddle of remorse is not going to do anybody any good in relation to their funding portfolios.

So, as an alternative of trying mournfully on the previous, I am trying in direction of the longer term with pleasure.

I consider that META has the potential to proceed to outperform the broader market – and even a lot of its big-tech friends – and now that the corporate is paying a dividend, it is a very simple inventory for me to carry.

This dividend helps me to keep away from fearful impulses with regard to promoting into damaging volatility, or grasping ambitions of making an attempt to time the market and promoting into power.

That is why I concentrate on dividend growers. Their passive revenue retains me grounded and reduces anxiousness whereas I maintain over the long-term.

I am very joyful to have established a ~1% place at $473 and this inventory stays close to the highest of my watch checklist transferring ahead.

I would wish to construct this place as much as the 2-3% vary, which might make it a prime 10 place inside my portfolio.

It is troublesome to seek out dividend growers with 15-20% long-term EPS development prospects.

It is particularly troublesome to seek out these firms buying and selling for under 25x earnings.

META falls into that class, making it one of the engaging quick compounders that I observe proper now.