NYCstock

Fast Overview

With banks making headlines this week once more, I wished to the touch upon a subsector of the financials phase that’s typically under-covered however typically presents an fascinating investing alternative as I’ve written about within the final yr, and that’s insurance coverage. Although it will not be the mainstream media’s hip and funky startup from Silicon Valley, what it lacks in media hype it makes up in fundamentals, which we predict is extra vital.

The truth is, it’s possible you’ll bear in mind the opening scene of the Nineteen Eighties film Wall Avenue, the place the skilled dealer tells the youthful of us to “stick to the fundamentals.. that’s how IBM and Hilton were built. Good things sometimes take time.”

Right now’s insurance coverage decide of the week buying and selling now for beneath $70 is MetLife (NYSE:MET), a inventory I covered in August and since calling it a maintain its share worth has gone up practically 5% since then.

MetLife – worth since final score (In search of Alpha)

This time round, our thesis on this inventory is to reaffirm its maintain score, and that is pushed by strong YoY progress in income, earnings, and fairness, but additionally analyst estimates of future EPS progress, and an rate of interest surroundings favoring this agency’s asset portfolio.

On the similar time, its dividend yield in comparison with key friends is unremarkable, and regardless of first rate valuations it is also buying and selling at a major premium to its shifting common and has publicity to workplace loans, a identified danger being talked about quite a bit recently.

Methodology

This text will make use of our Investing Stream under which relies on waterfall methodology from the world of mission administration.

Right now’s article goals to reply questions like why this particular inventory and sector, what are the dangers and advantages we are able to plan for, whether or not the present share worth and valuation is smart, what metrics matter to this particular sector, and what might be a long-term exit technique for this inventory?

The solutions to those questions, holistically, ought to result in a enterprise resolution of whether or not we purchase, promote, or maintain this inventory right this moment.

MetLife – investing movement (creator)

Initiating: Why this Inventory & Sector?

First, let’s begin with the general sector of financials. We all know from key market data on In search of Alpha that this phase has grown properly from 3 years in the past, to the tune of +32% progress in 3 years, but additionally +6% progress within the final yr.

It should be stated that it’s a massive sector that encompasses banks, asset managers, and insurance coverage. What I like about insurance coverage is that it doesn’t have sure points that banks have. For instance, it takes in a ton of money from buyer coverage premiums, and after paying out bills and coverage claims it invests plenty of the additional money into an asset portfolio, earning money on that too, largely from curiosity. Therefore, a excessive fee surroundings is sort of a gold rush for this agency.

On the similar time, not like banks, it doesn’t have the legal responsibility of buyer deposits, worry of financial institution runs, or paying curiosity on conventional financial institution depositor funds. Insurance coverage insurance policies, in our opinion, additionally are typically “sticky” particularly life insurance coverage.

With that stated, we like to investigate MetLife as a result of it’s a main life insurer, but additionally has diversification amongst different traces of enterprise. A few of its friends and rivals could be Prudential Monetary (PRU), and Canada’s Solar Life Monetary (SLF).

From its profile on SA, we all know that it has been round for +100 years, trades on the NYSE, has a world attain, and moreover insurance coverage it additionally offers in mounted and variable annuities, pension merchandise, and capital markets funding merchandise.

These of us who grew up within the New York Metropolis space additionally know the way sturdy of a model MetLife is, and never simply from having its identify on an enormous constructing in Manhattan but additionally from a number of generations having watched MetLife adverts on TV, print, and later on-line. It’s a model constructed over generations, and like we stated generally good issues take time.

Planning: What are Dangers & Advantages?

Now that we all know why we have an interest on this sector and this inventory, let’s speak about planning for the dangers and advantages of proudly owning this inventory.

First, let’s contact on its most up-to-date earnings results which are nonetheless recent after their Jan. thirty first launch.

This seems to us a critical firm, with YoY income rising to +$19B within the quarter ending December, vs $16.3B in December 2022.

We are able to see from the income statement what drove this income was progress in each its core enterprise of insurance coverage premiums but additionally progress in interest-income on its asset portfolio.

Nonetheless, we additionally see from that very same assertion that there was YoY progress in coverage profit payouts, with +$14.7B paid out in advantages in This fall, and this clearly impacting earnings with internet revenue falling to $607MM vs $1.3B in Dec. 2022.

The corporate was capable of keep constructive cash flow, and from the stability sheet we see a major YoY decline in long-term company debt, which helped in the direction of YoY fairness progress with whole fairness now at +$30.25B.

One other constructive to notice is that analysts are estimating further EPS growth for the following few years at MetLife, with practically +23% YoY progress in EPS anticipated for the quarter ending Dec. 2024.

By way of liquidity danger, the corporate in its full-year 2023 results indicated “holding company cash and liquid assets of $5.2B at December 31, 2023, which is above the target cash buffer of $3.0 – $4.0B.”

We additionally know that the excessive rate of interest surroundings has benefitted this agency. In keeping with their Q4 commentary, progress in internet funding revenue was “driven by higher interest rates and increases in the estimated fair value of certain securities.”

With current headlines within the monetary press speaking about danger publicity of banks to workplace loans, resembling The Financial Times reporting on shares plunging at New York Group Bancorp (NYCB) after the financial institution reported mortgage losses ” which emanated from loans tied to office buildings,” we care about what sort of publicity MetLife has to workplace actual property and the way it can have an effect on this agency going ahead.

From MetLife’s financial supplement, we see that their $19.65B of workplace mortgage publicity is sort of +38% of their whole industrial mortgage loans which make about $52.1B of the internet mortgage mortgage e book of $84.1B. So, places of work are round 23% of the web mortgage loans MetLife is uncovered to.

MetLife – publicity to workplace (firm monetary complement)

Our outlook, due to this fact, is one in all constructive warning on this agency as a result of on the one hand it has grown income, fairness and earnings in addition to having future EPS progress estimates nonetheless on the similar time virtually 1/4th of its mortgage mortgage publicity is tied to places of work. Even when these are high quality loans, our concern is the market turning into more and more jittery about proudly owning firms with quite a lot of proportion factors of publicity to places of work, particularly if extra banks begin reporting vital mortgage losses.

Holistically, the danger/profit situation for us right here to this point is one in all a maintain reasonably than a purchase or promote, however we are going to want some extra knowledge earlier than making a choice.

Executing: Is the Worth & Valuation Justified?

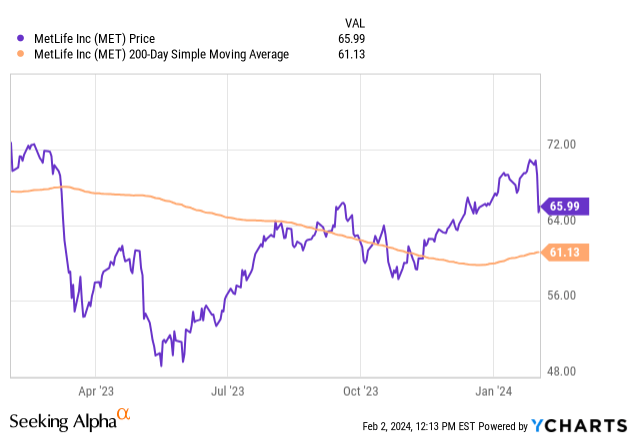

An element we think about is share worth in relation to its 200-day shifting common, in addition to valuations on this inventory.

First, let’s pull the yChart:

We see from the chart that the inventory has recovered fairly properly from its lows final spring when many financials had been taking a dip within the wake of regional financial institution failures, and proper now MetLife is buying and selling at practically +8% vs its 200-day SMA.

From valuation metrics we all know that the ahead P/E is 7.98, whereas the sector common is 10.88. Additional, it’s a higher valuation than the 16.6x earnings a number of at insurance coverage peer Prudential Financial.

In comparison with my summer coverage of MetLife when it had a ahead P/E of 13.7, now it presents a greater valuation at practically 8x ahead earnings, contemplating that analysts are estimating +23% YoY EPS progress by December, as I discussed earlier. So, it seems the market is holding again a bit though analysts are bullish. We see this as a worth alternative.

Personally, we predict the continued excessive rate of interest surroundings will proceed to profit this agency’s earnings, particularly after the late-January Fed assembly didn’t end in a fee reduce and in keeping with a CNBC article it appears much less seemingly {that a} March fee reduce will occur both.

So far as ahead P/B ratio, it’s now 1.62, simply above the sector common of 1.04. This tells us the market is bullish on future fairness progress, seemingly resulting from anticipated earnings progress and the YoY fairness progress and decrease debt the corporate reported in This fall outcomes. We like this valuation as it’s backed by confirmed fairness progress and excessive chance of future fairness progress, so it justifies bullishness on the share worth.

At this level in our “waterfall” strategy to this inventory, it may nonetheless be both a maintain or a purchase, and we see today’s consensus (SA analysts, Wall Avenue, quant system) all are calling for a purchase.

The deciding issue will probably be dividend yield and dividend progress, and we are going to cowl that within the subsequent part.

Monitor & Management: What Metrics Matter to this Sector?

We’re caught between whether or not to purchase shares in MetLife on the present elevated worth or maintain on (assuming we had already purchased on the earlier decrease costs in spring).

Two metrics we monitor on an ongoing foundation (as they’re topic to alter) are dividend yield and dividend growth, but additionally the soundness of quarterly dividend payouts.

We all know that MetLife up till now has been a dividend grower over 10 years, with the annual dividend going from $1.18 in 2014 to $2.06 in 2023, a +74% progress in a decade. This tells us it’s a critical agency capable of return capital again to shareholders. Contemplate that the current mortgage loss from New York Group Bancorp led to that agency reducing its quarterly dividend, and affecting yield as effectively.

We expect the continued anticipated profitability progress at MetLife, and constructive money movement scenario, will increase chance of dividend hikes in 2024. It’s now already at $0.52/share, which we predict just isn’t dangerous for a inventory buying and selling at beneath $70, because it affords a +3% yield. Though history doesn’t assure future payouts, it does improve our confidence as this agency has had uninterrupted quarterly payouts for years.

Lastly, we wish to examine the trailing yield vs friends, to seize the most effective yield for our capital invested.

The comparables we are going to use are Prudential, Solar Life, and Aflac (AFL). We are able to see that Prudential leads the way in which with 4.87% yield, so in an interest-rate surroundings the place buyers are sometimes leaving shares for high-rate CDs and cash market funds paying +5% yield and better, we’ve to say that MetLife comes brief in its yield.

Prudential, regardless of its $125 share worth right this moment, affords a quarterly dividend of $1.25/share, and likewise has a history of regular payouts and 10 yr dividend progress, so that will be our selection by way of the most effective yield supply.

MetLife – dividend yield vs friends (In search of Alpha)

So, we argue for a agency maintain on MetLife reasonably than a purchase or promote at this level, and imagine the proof helps this case.

Closing: When do I Exit This Funding?

Now that we decided to carry on to MetLife and never purchase shares or promote them, what’s our portfolio technique and the way can we exit from this place?

Our technique is that MetLife could be an anchor inventory in our portfolio, giving us publicity to massive, well-established and extremely liquid insurance coverage firms like this one, so we might be trying to maintain it for 30+ years as a part of a dividend-income portfolio, reasonably than trying to obtain short-term capital positive factors.

By holding on, we all know it exposes our portfolio to draw back but additionally upside danger. The draw back danger we predict may come from jittery buyers fleeing financials general within the occasion of additional workplace mortgage complications within the system, however we additionally assume there’s upside potential as opportunistic buyers will acknowledge the “future value” of this inventory and also will maintain on to it like we’re, significantly dividend-oriented buyers who need the regular dividend revenue from a safe firm. The draw back danger of workplace mortgage defaults should subside, we predict, after rates of interest come down once more as it can make borrowing cheaper. Proper now the excessive value of borrowing to put money into places of work is solely not a fantastic funding, however finally that ought to change since charges all the time come down once more as we have watched this cycle time and again.

In different phrases, we think about MetLife a “safety” inventory to maintain our palms on, and we additionally acknowledge the “value” of the insurance coverage business as a necessity as an business that helps individuals and companies switch danger to a 3rd -party.

On this case, MetLife is heavy into life insurance coverage, and that may be a life occasion that may develop into fairly pricey and financially impeding to any household, so we predict MetLife gives a crucial necessity economically to switch that monetary danger to an insurer, and as buyers we additionally see the worth of the continual faucet of coverage premiums coming into the corporate every year, and thru environment friendly actuarial /danger administration this agency has made a 100+ yr enterprise out of insuring what we may name somebody’s most vital asset.. their life and that of relations.