PJ66431470/iStock through Getty Photographs

My thesis

Microchip (NASDAQ:MCHP) owns a stable portfolio combining Microcontrollers, Analogs, programmable processors, and software program options. This whole providing permits for built-in and tailored options. Whereas the acquisition of Microsemi in 2018 was crucial, it elevated Microchip’s leverage place considerably with an ND/EBITDA reaching 5x in 2019. Regardless of a stable cash-flow technology, it took years to cut back such debt burden.

We’re at the moment reaching the tipping level: the leverage ratio went under 1.5X permitting for a big and recurrent distribution to shareholders. On this report, I’ll analyze the enterprise mannequin, talk about the latest outcomes, and supply a valuation evaluation of the MCHP inventory. Whereas the funding case is stable, weak cyclical tendencies and a good valuation make me look ahead to a greater entry level. I fee the inventory as a HOLD.

Funding overview

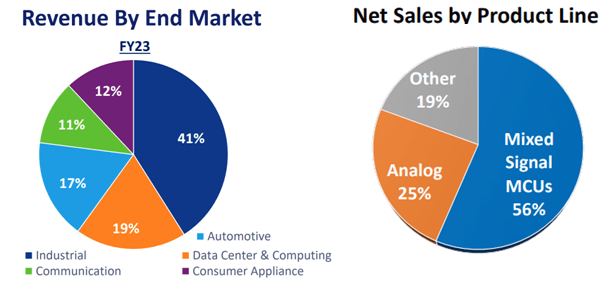

Microchip is a US-based semiconductor firm created in 1989, designing and producing Microcontrollers (MCUs), Analogs, programmable processors (FPGAs), onerous drive controllers, radiofrequency chip units, and different purposes. It focuses on offering Whole System Options (TSS) for its clients: from a whole set of {hardware} to software program and providers. As such, it goals to outgrow its trade due to its improve in common income per consumer. It leverages its large-scale portfolio of greater than 250,000 units. Its consumer pool is nicely diversified, with above 120,000 accounts. Microchip ended final FY2023 with document revenues of $8.4 billion however has since then entered right into a cyclical correction as we’ll talk about afterward.

Microchip

The agency produces 40% of its wafers in-house, principally older applied sciences whereas counting on exterior foundries to provide the remainder. On high of that, it owns packaging and testing amenities. We are able to say it has comparatively good management over its provide chain. To enhance its relations with its shoppers and decrease its enterprise cyclicality, the agency arrange 2011 a Most well-liked Provide Program. The PSP helps its clients to safe stock, by putting 12 months upfront non-cancelable orders and including a deposit. As a consequence of the latest financial slowdown, impacting the agency’s outcomes and creating elevated ranges of inventories, Microchip determined to halt this program. The agency could have the flexibility to revive if the exercise had been to rebound.

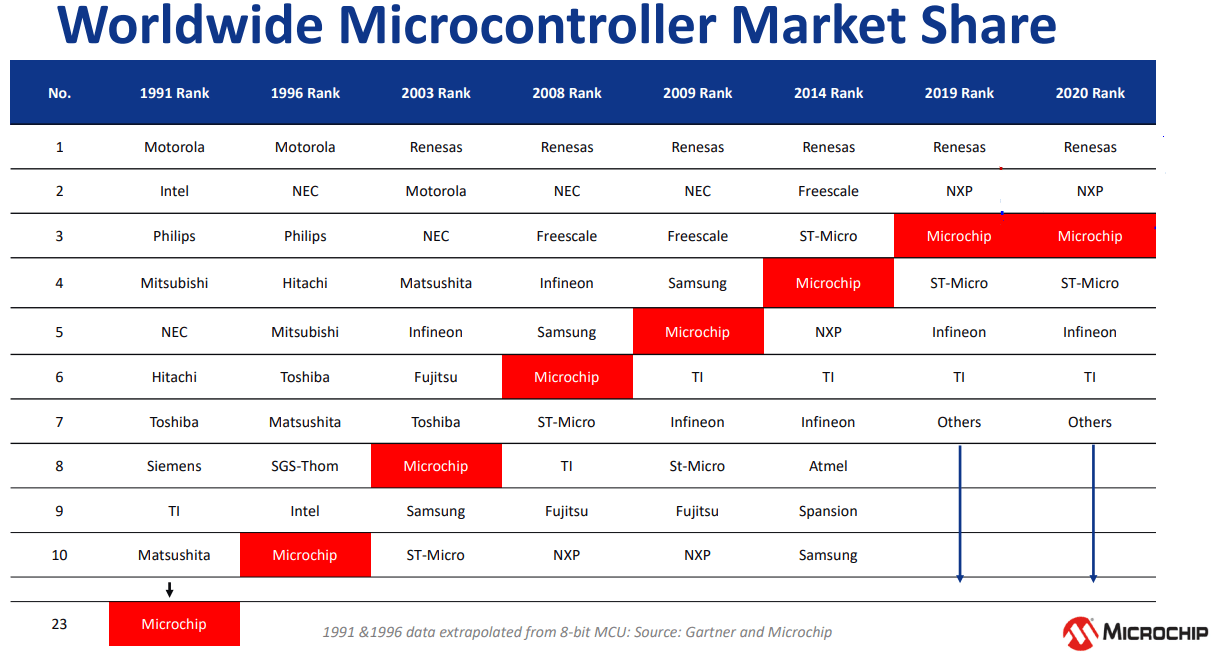

Microchip turned a powerhouse by buying a number of firms. Probably the most notable ones had been the takeover of Atmel in 2016 for $3.6 billion and Microsemi for $10 billion in 2018. Atmel strengthened its portfolio in RF chips, Analogs, and reminiscence units, whereas the latter helped to extend its scale in MCUs by including new segments comparable to FPGAs and storage/networking chips. By way of natural progress and inorganic consolidation, the agency went from the highest 10 positions in Microcontrollers to the highest beginning in 2020.

Nonetheless, its MCU portfolio just isn’t on the highest finish of the spectrum and nonetheless importantly depends on manufactured 8 and 16-bit buildings. As compared, NXP (NXPI), STMicroelectronics (STM), and Infineon (OTCQX:IFNNY) have a extra dominant place in probably the most superior 32-bit chips. Microchip is step by step altering that scenario by investing in 32-Bits and has already made good progress. Certainly, whereas in 2021 solely one-fourth of its MCU portfolio was associated to this newest know-how, this rose to 50% in 2023.

Microchip

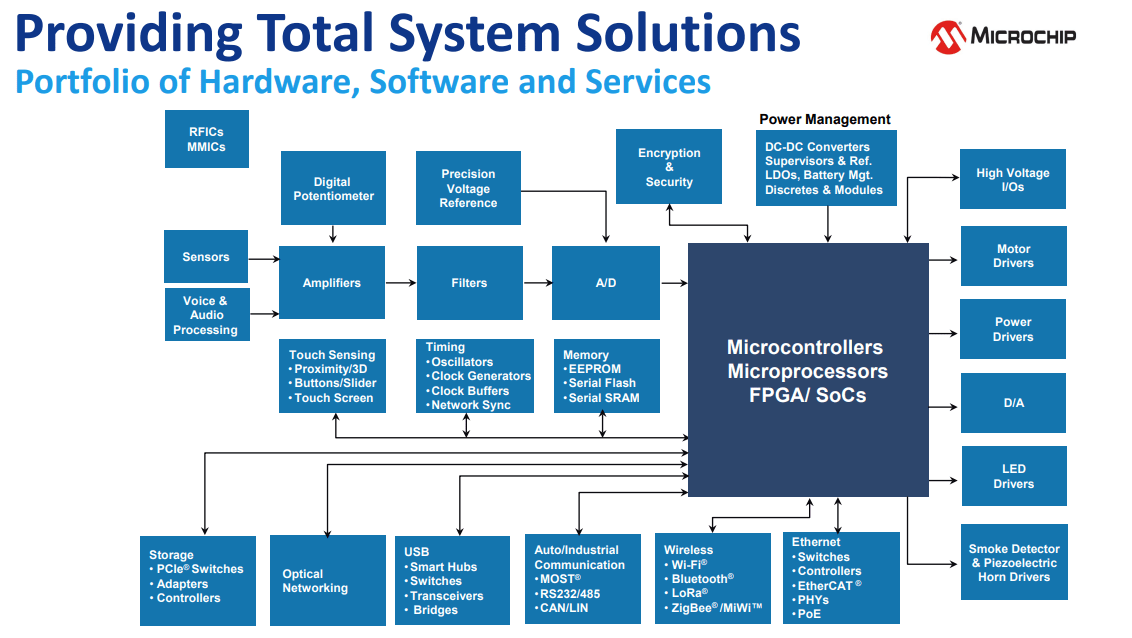

Microchip’s TSS may be mapped within the image under. It offers a one-stop store for its shoppers and interprets right into a stable switching value. On account of elevated cross-selling, the agency’s margins and money circulate conversion are excessive. Certainly, Microchip can generate larger income per consumer whereas holding its SG&A bills beneath management.

Microchip

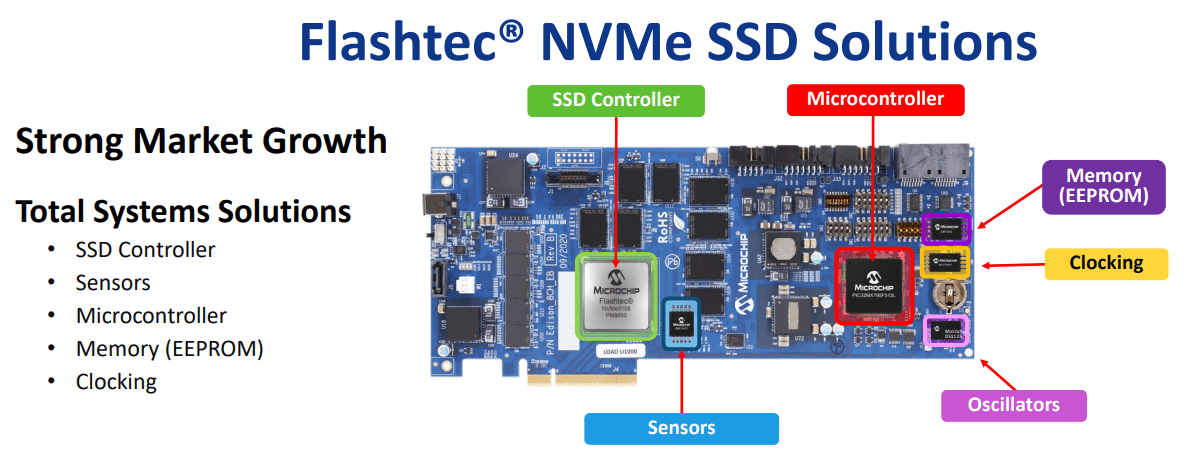

If we take one concrete instance of an answer for an SSD storage drive, we see that Microchip offers a set of chips, from the controller, and MCU to sensors. Drive controllers discover the situation the place the requested information is saved, learn the information, and switch it to the server. Such options are a part of the information heart and computing section. In that section, Microchip is in a quasi-duopoly, with Marvell (MRVL) as the principle competitor.

Microchip

In automotive, the agency ranks primary with contact screens and buttons. Contemplating larger worth gadgets, it additionally offers chips for ADAS and infotainment the place it may well place its microcontrollers. Lastly, it offers full options for EV chargers together with MCU, SiC diodes, contact display controllers, or power metering.

Current quarterly tendencies

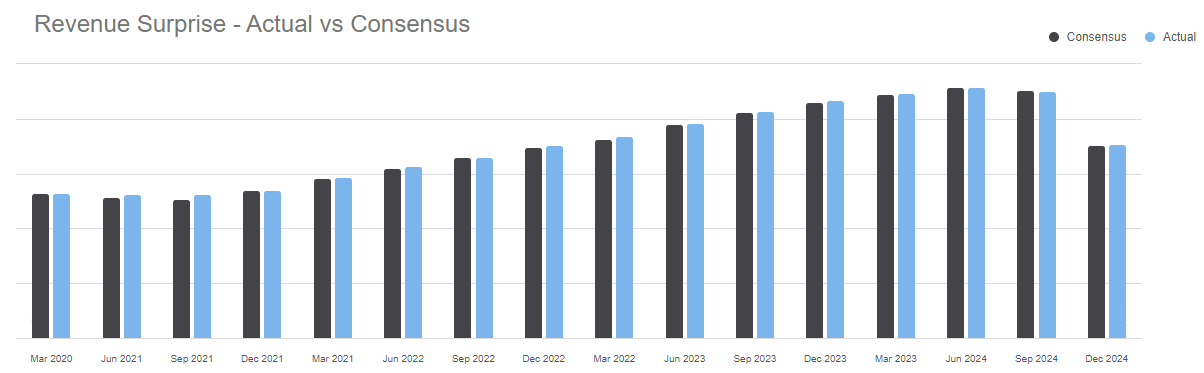

Microchip simply revealed its Q3 FY2024 results on February 1, 2024. Revenues fell off a cliff, down 22% QoQ to $1.77 billion and down 19% YoY, whereas non-GAAP gross margins stood nicely at 63.8%. Stock remained elevated, above $1.3 billion for the fourth consecutive quarter. Days of inventories reached 185 and elevated by 10% from the final quarter. In the conference call, the corporate acknowledged “We were not able to make as much progress as we would have liked“. All segments aside from protection and aerospace suffered a correction.

Searching for Alpha

What was notable in administration’s remark was that its finish markets had been a lot weaker than anticipated round all areas. It acknowledged that: “many customers implemented extended shutdown in December” and that Microchip was “able to push out or cancel backlog” to assist clients higher deal with their stock ranges. The administration added that such a scenario was the results of a just-in-case coverage set in place post-COVID disruptions, changing just-in-time stock administration. Additionally, overly optimistic views of enterprise CEOs throughout 2023, anticipating robust financial progress would proceed in 2024.

Microchip reacted to such a troublesome scenario by reducing utilization charges of its factories world wide and implementing cost-cutting measures comparable to wage cuts round all its organizations. The subsequent and fourth quarter of FY2024 ought to proceed to fall, with revenues seen near $1.3 billion implying a minus 27% decline whereas gross margin ought to resist near 60% due to manufacturing facility optimization. The agency CEO concluded by saying: ” We don’t know how and when the upcycle will play out“. As a consequence, no steerage past the subsequent quarter was given. The one constructive level for my part was the indication of the income decline) is especially volume-related resulting from under-shipping and never price-driven because the administration stated: “pricing is stable“.

What valuation can we anticipate?

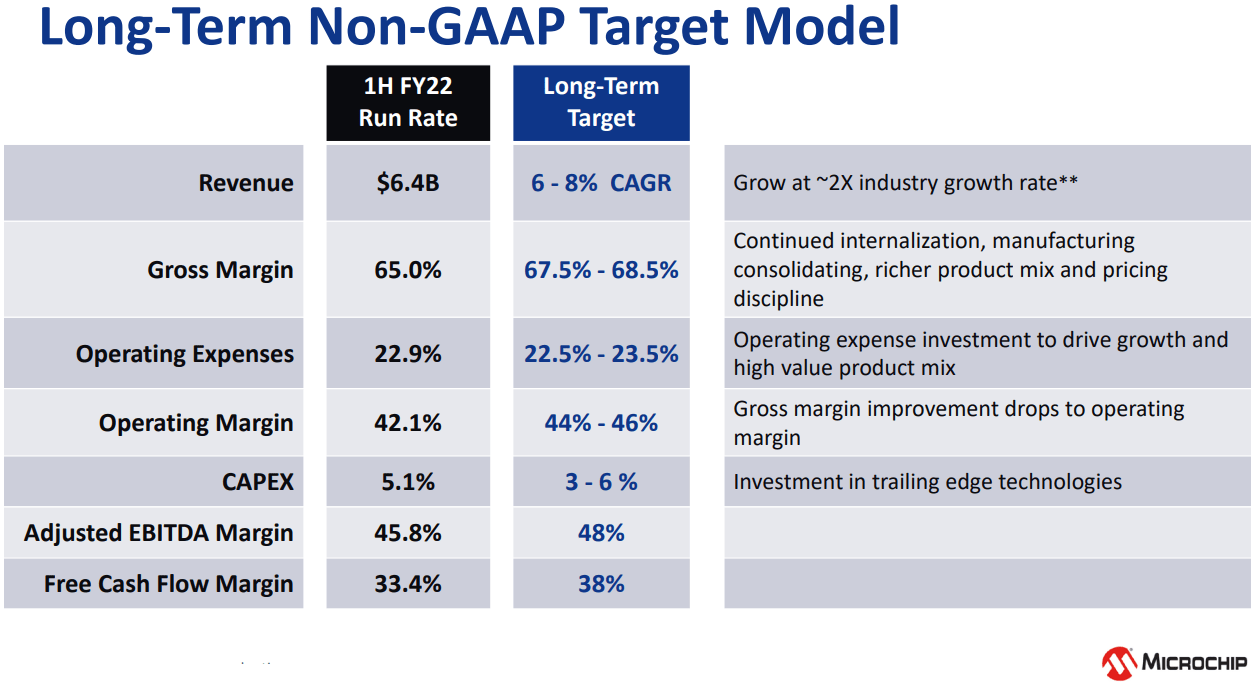

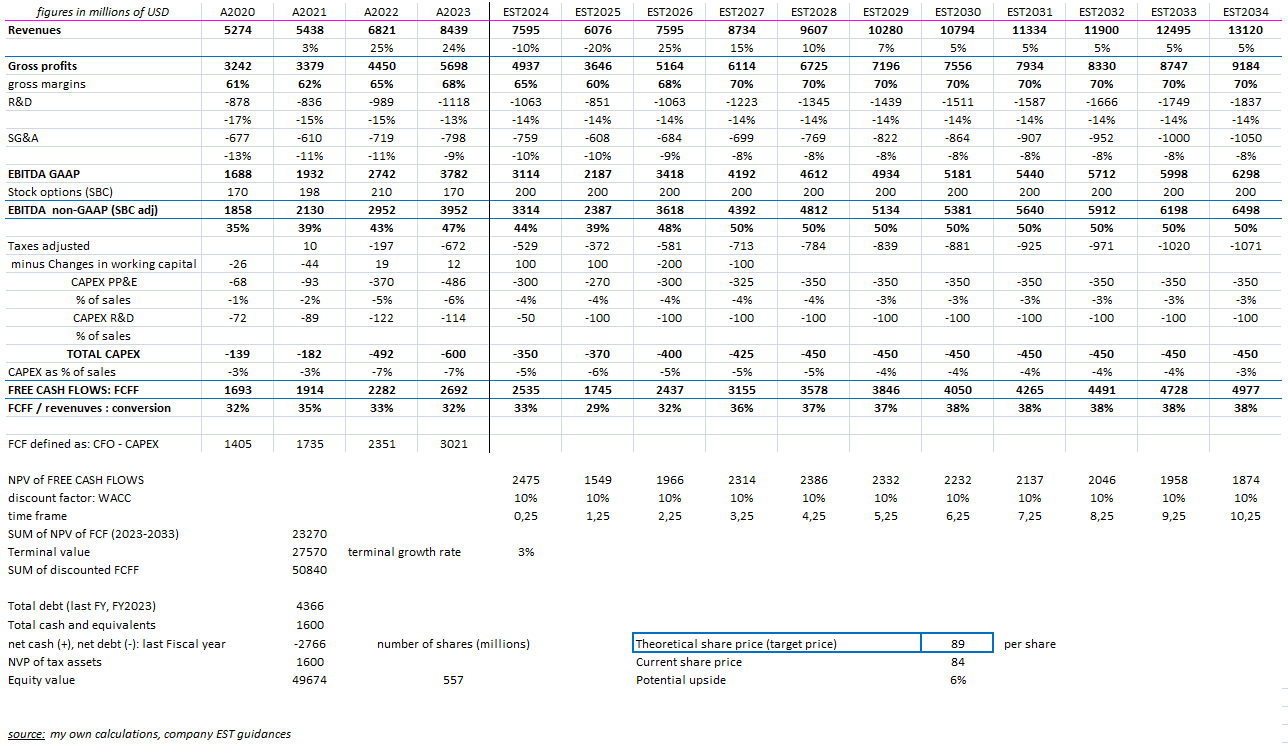

Throughout the 2021 Investor Day, Microchip set a long-term goal mannequin. I took under consideration a few of its hypotheses in my following DCF mannequin.

Microchip

As income progress began a cyclical correction final quarter (Q3 FY24), an enormous a part of the downturn might be felt in FY2025 (finish Match 2025). I, due to this fact, mannequin Microchip will hit the underside in the course of the subsequent fiscal yr. The rebound may very well be fast and huge hereafter as has been the case traditionally in Industrial MCUs. Within the medium-term (FY2028-2034), I see a CAGR of 6%, on the backside of the vary of the Lengthy-term mannequin offered by the administration.

Microchip Whole System Options assist stabilize the agency margins, even throughout a downturn as we witnessed within the newest quarterly consequence. As a consequence, I do not see gross margins to compress under 60% regardless of the anticipated income decline. It’s spectacular that pricing is steady regardless of an ongoing quantity correction. This may very well be the brand new regular, post-supply-chain disruption.

When macro tendencies enhance, I imagine the working margin may hit 50%, larger than the 2021 administration estimates. Certainly, semiconductor firms (MCU and Analogs friends) have seen a transparent sustainable development of their working leverage.

FY2024 CAPEX is anticipated to succeed in $305 million and it was stated over the last convention name that the FY2025 spending degree needs to be decrease. My mannequin makes use of a 4.5% CAPEX/gross sales ratio for the medium time period. All-in-all, the FCF conversion I obtained mid-term is near 38%. Utilizing a WACC of 10% and my estimates, I do discover the inventory is broadly pretty valued.

personal calculations

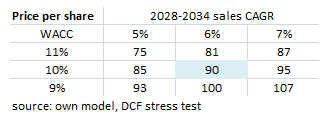

To present extra perspective, I applied a sensitivity evaluation, various medium-term (2027-2034) progress fee and the low cost fee:

personal calculations

Steadiness sheet evaluation

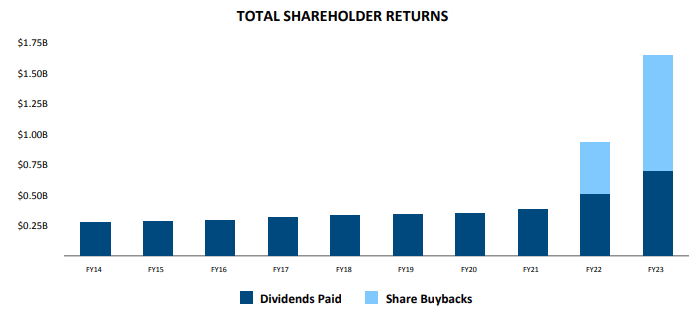

Over the past quarter, the ND/EBITDA declined to 1.3X permitting the agency to additional improve its money distribution to shareholders to 82.5% for the subsequent quarter and go to 100% by March 2025. This dedication is legitimate except the leverage ratio rises above 1.5x. Throughout the 9 months of FY2024, the agency distributed $1.3 billion money to shareholders, roughly half dividend and half buybacks. I anticipate the full annual money yield to succeed in $1.8 billion for FY2024 resulting in a yield of 4% over the market cap.

Microchip

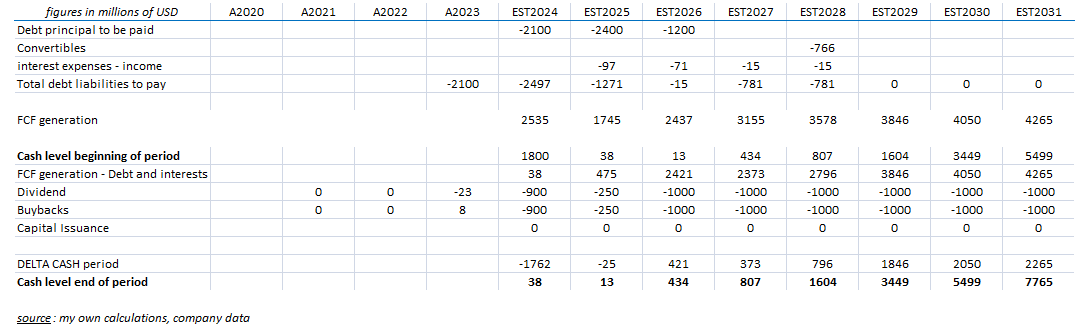

Regarding FY2025 (ending March 2025): my calculations present that money distribution might be modest in quantity because the FCF needs to be compressed and the agency has to repay $2.4 billion of bonds maturing throughout CY2025. Nonetheless, beginning FY2026 and past, Microchip may handle to distribute greater than $2 billion money payout, equal to a yield shut to five% which I discover interesting.

personal calculations

Technical evaluation

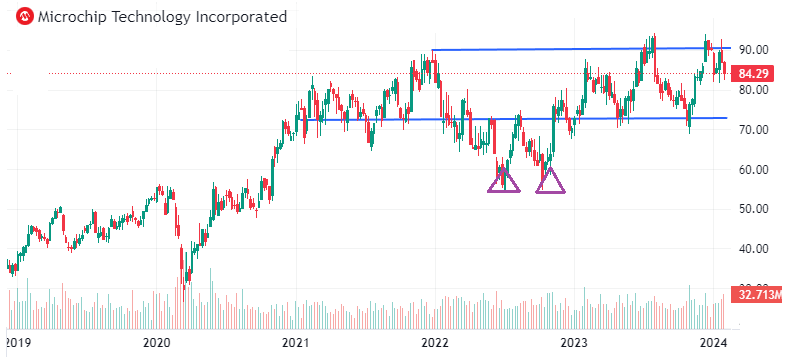

The inventory rebounded strongly from mid-2022 lows through a double backside at $55/share after which step by step reached latest highs near $90/share. The continued cyclical correction of Microchip ends markets, with no clear rebound seen by the administration within the close to time period, just isn’t coherent with all-time excessive value ranges. Given the weak Q3 and steerage, the inventory deserves a correction. I might wait on the backside of the higher vary, trying on the help close to $70-75/share, for a greater entry level.

Searching for Alpha

Dangers and alternatives

The principle threat is see is said to the very fact Microchip is competing with greater firms in three of its markets. In microcontroller MCUs, it’s NR4 with 14% market share after STMicroelectronics, Renesas (OTCPK:RNECF), and NXP. Inside Analog, it’s a relatively small player if we examine it with Texas Devices (TXN) and Analog Units (ADI). Lastly, in FPGA processors, I estimate its revenues are actually near $500m because it generated close to $400m annually in 2021. That is a lot smaller than Xilinx from (AMD) and Altera from (Intel).

One other secondary threat comes from the very fact its industrial section is kind of massive, near 40% of its gross sales, and is topic to excessive swings. Subsequently, the P/E ratio has to low cost such cyclicality.

Conclusion

Essentially, it might be the time to purchase the inventory Microchip administration has constructed an organization having a whole portfolio of semiconductors, software program, and providers, serving as a full resolution for its shoppers. Within the meantime, the debt degree is now beneath management whereas the stable FCF technology permits for growing money distribution. Nonetheless, it’s troublesome to disregard the present cyclical downturn of its finish markets, and the administration simply stated no clear rebound is foreseen. It might be extra rational to attend a bit extra earlier than including to the inventory. I fee the funding as a Maintain.