Ake Ngiamsanguan/iStock by way of Getty Photographs

Mistras Group (NYSE:MG) gives asset safety options. MG posted Q3 FY23 outcomes, which I’ll analyze on this report. I believe MG is just not a purchase proper now. On account of rising debt, stagnant income progress, and due to the technical chart. It will be dangerous to guess on MG proper now. Therefore, I assign a maintain score on MG.

Monetary Evaluation

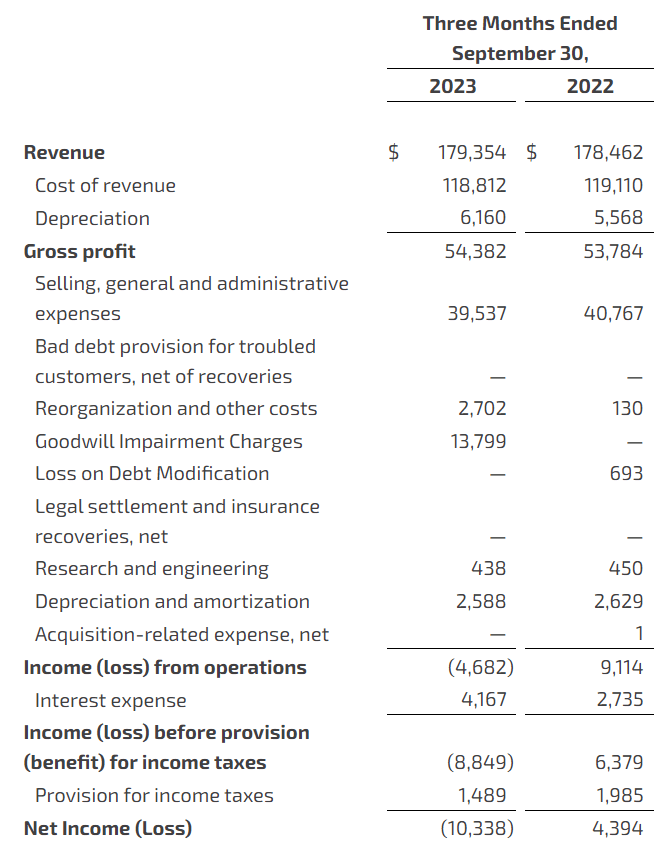

MG introduced Q3 FY23 results. The income for Q3 FY23 was $179.3 million, a slight enhance of 0.5% in comparison with Q3 FY22. The explanation for the stagnant income progress was the underperformance in its companies section. The income from the companies section declined by 2.6% in Q3 FY23 in comparison with Q3 FY22. The main cause for the drop was a decline in energy distribution because of venture timing. The gross margin for Q3 FY23 was 30.3%, which was 30.1% in Q3 FY22. The rise was primarily because of low healthcare bills and a positive gross sales combine.

MG’s Investor Relations

The corporate needed to incur a $13.8 million non-cash impairment cost. On account of this, it reported a internet lack of $10.3 million in comparison with a internet earnings of $4.4 million. Truthfully, I don’t see something noteworthy within the outcomes. The income progress was stagnant, and the administration has reduce down its gross sales and EBITDA steering for FY23, which could create a detrimental sentiment and have an effect on its share worth. Its gross sales steering for FY23 is now round $700 million, beforehand $710 million, and the EBITDA steering is now at $66 million from $69 million. Nonetheless, there have been two positives for them on this quarter. First, the continued aerospace progress is boosting its gross sales and is predicted to proceed to learn them. Second, the optimistic preliminary impact of the venture Phoenix. Its gross margin expanded, and the administration attributed this to the Phoenix venture; it’s an initiative to scale back the corporate’s bills and increase profitability by way of environment friendly pricing and lowering SG&A bills. This venture is new, and the administration talked about that it has seen some success, which is a optimistic signal as a result of, with time, the margins of the corporate will proceed to enhance. Nonetheless, stagnant income progress is a matter, and the steering suggests softness will proceed within the fourth quarter. The opposite challenge that I see is the rise within the long-term debt. Its long-term debt elevated 1% in September 2023 in comparison with December 2022 to $185.4 million. Though the rise is just not vital contemplating its low profitability, the excessive debt turns into a problem.

Technical Evaluation

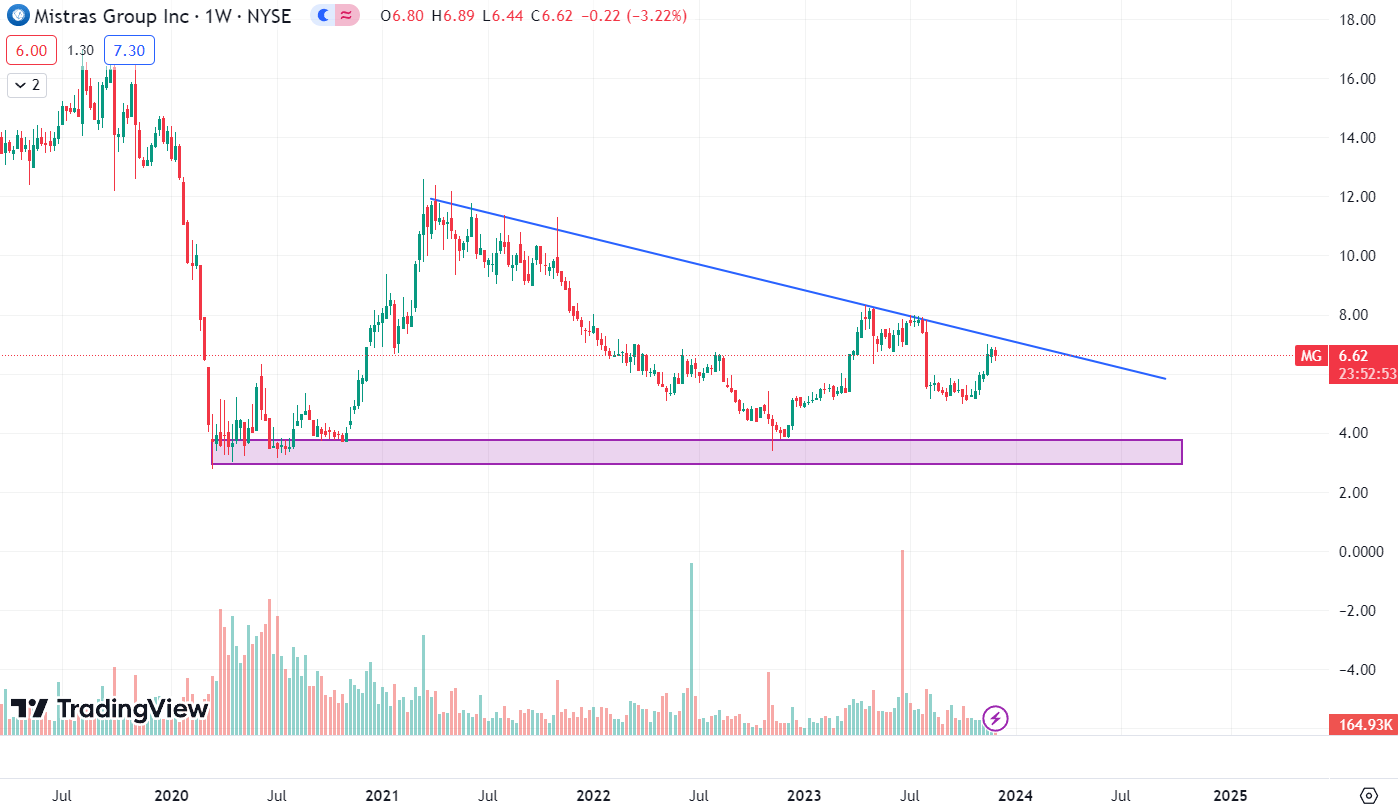

Buying and selling View

MG is buying and selling at $6.6. Within the final two years, the inventory has corrected greater than 40%, and proper now, it’s at an important stage as a result of it’s close to a trendline. This trendline has been a barrier for the inventory since 2021. The worth has didn’t cross the trendline and has reversed each time it touches it. So if the inventory fails to cross the trendline, which is at $7.3, it’d reverse and fall as much as $4. The $4 stage has been sturdy help for the inventory since 2020, so if the inventory faces resistance from the trendline, the draw back that I see is at $4. Now, speaking about what if the inventory breaks the trendline, which is at $7.3, then we’d see a strong upside. So, for now, I might say one ought to wait, and if the inventory breaks the trendline, then one can provoke a shopping for place, and if it fails to take action, it could be higher to keep away from it.

Ought to One Make investments In MG?

MG has an EV / EBIT [FWD] ratio of 15.75x in comparison with the sector median of 15.31x. MG doesn’t appear overvalued, however there isn’t any alternative that we are able to capitalize on. It nonetheless wants various work to do. The excessive debt appears to be an issue. The corporate’s curiosity expense elevated considerably on this quarter in comparison with the earlier 12 months. So, the rise in debt turns into a problem as a result of its income progress has been stagnant, and softness is predicted within the fourth quarter as nicely. Moreover, its share worth is close to an necessary stage. So, contemplating these elements, I believe MG is just not a purchase proper now.

Threat

A lot of their earlier earnings have come from their prospects within the oil and fuel sector. Particularly, for the years ending December 31, 2022, 2021, and 2020, they constituted roughly 56%, 54%, and 54% of their revenues, respectively. Although they now serve a wider vary of sectors apart from the oil and fuel sector, this sector nonetheless accounts for almost all of their earnings. The operators of vegetation, refineries, and pipelines rely on their companies, which they’ve elevated by including mechanical and in-line inspection companies to their portfolio. Nonetheless, contracts for his or her companies have been diminished prior to now and will proceed to be so because of financial downturns or low oil costs. Moreover, low oil costs could discourage new development and exploration, which might harm their market potential. Their money flows, earnings, and revenues would possibly all decline if the value of oil dropped. The supply of inspection companies to purchasers within the oil and fuel sector could also be delayed or postponed if the value of oil hits document highs, as occurred in 2022.

Backside Line

The continued progress within the aerospace market and the Phoenix venture are optimistic for the corporate. Nonetheless, I believe it isn’t a purchase proper now due to the stagnant income progress and rising debt. Moreover, its share worth is at an important stage the place we are able to see a reversal from the present stage. Therefore, it could be dangerous to speculate on the present stage. Therefore, I assign a maintain score on MG.