Jelena Stanojkovic/iStock through Getty Pictures

At a Look

Delving into Moderna’s (NASDAQ:MRNA) trajectory, my earlier analysis make clear its eclectic venture vary. This spectrum spans from oncology to infectious illnesses, with notable breakthroughs in RSV and flu vaccines. Moderna has since leaped ahead, particularly with mRNA-1083. This vaccine, each progressive and dual-purpose, targets COVID-19 and flu. It is now in Part 3, with approval anticipated in 2025.

Nonetheless, it is not all easy crusing. The previous 12 months noticed income dip and operational bills climb. Nonetheless, Moderna’s monetary well being stays resilient, boasting $12.8 billion in liquid property. But, buyers ought to keep alert. They face hurdles like Pfizer’s (PFE) rival vaccine and the essential want for sharp monetary stewardship to make sure progress.

Regardless of these challenges, the market appears to undervalue Moderna. It overlooks the long-term progress pushed by its wealthy pipeline. This oversight is especially acute within the realms of most cancers remedy and infectious illness management. These areas, brimming with potential, are prone to be key drivers of Moderna’s future income surge.

Moderna’s Double Protection: A Shot at Conquering Flu and COVID Collectively

As a nurse working on the bedside, I’ve been donning numerous isolation robes, gloves, and masks these days. This winter, COVID-19 and influenza are on the rise, with many weak individuals contaminated and experiencing signs. This underscores the necessity for more practical and handy immunizations. Moderna’s mRNA-1083 vaccine takes an enormous step ahead by concentrating on each influenza and COVID-19.

mRNA-1083’s Part 1/2 trials revealed strong outcomes. Their findings demonstrated important immune responses to each viruses, in addition to a security and reactogenicity profile equal to current immunizations.

The trial knowledge for mRNA-1083 revealed spectacular hemagglutination inhibition antibody ranges, rivaling or surpassing these elicited by permitted quadrivalent flu vaccines. Equally, the vaccine generated SARS-CoV-2 neutralizing antibodies at ranges similar to these from the Spikevax bivalent booster. Notably, antagonistic reactions had been usually delicate or average, aligning with these noticed in standalone vaccine trials.

mRNA-1083 is now in Phase 3, with approval anticipated in 2025. This dual-action immunization permits for speedier administration and elevated affected person compliance, doubtlessly lowering the annual burden that these viruses place on people and healthcare programs. As a result of COVID-19 is prone to be a seasonal downside, just like influenza, I consider a mix vaccine is perhaps a extremely profitable funding, and if Moderna’s pandemic efforts from years in the past are any indication, they’re well-positioned for achievement.

Moreover, the massive industrial potential of this vaccine is demonstrated by Moderna’s prediction that gross sales of respiratory merchandise will attain between $8 and $15 billion by 2027. That, in my view, is just not a naive estimate. A mix vaccine might greater than double their present market share. As Moderna observes,

The worldwide influenza market quantity is roughly 500-600 million doses yearly with roughly 150 million doses administered in the US. Moderna estimates the U.S. fall 2023 COVID-19 market measurement as prone to be 50 to 100 million doses, relying on vaccination charges. Over time, the Firm anticipates the COVID-19 market will method the influenza market within the U.S. given the burden of illness.

Moderna

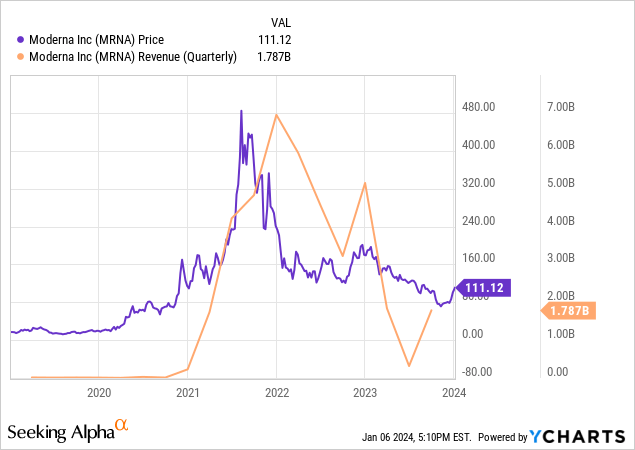

Q3 Efficiency

For the quarter ending September 30, 2023, Moderna revealed a major Y/Y lower in income, with web product gross sales dropping from $3,120 million to $1,757 million as a result of a lower in demand for his or her COVID vaccine. Operational prices, notably in the price of gross sales, elevated to $2,241 million, resulting in a web lack of $3,630 million, a major drop from the earlier 12 months’s revenue of $1,043 million. Share dilution has been average, with fundamental weighted common frequent shares receding from 390 million to 381 million.

Monetary Well being

Moderna’s whole liquid property are $12.8 billion, consisting of $2.9 billion in money and equivalents and $9.9 billion in investments. The corporate has $5.9 billion in liabilities, divided between $4.4 billion in present and $1.5 billion in non-current. The present ratio is 2.46, indicating a strong liquidity place.

Nonetheless, Moderna skilled a web money depletion of $3.7 billion in working actions over the 9 months ending September 30, 2023. This negatively impacts the corporate’s monetary runway, with an estimated (historic) money runway of 31 months.

Moderna’s money reserves and lengthy money runway recommend minimal want for extra financing throughout the subsequent 12 months, assuming a constant money burn price and no main surprising bills or income slumps. Nonetheless, the corporate’s long-term monetary well being is unsure as a result of important money burn and the potential want for strategic monetary stewardship for sustainability.

Market Sentiment

Based on Searching for Alpha, Moderna’s market capitalization is pegged at $42.37 billion, marking a significant presence within the biotech panorama. Nonetheless, progress prospects seem restricted, with gross sales anticipated to drop from $6.42B in 2023 to $4.45B in 2024, then rebound to $5.57B in 2025. This gross sales volatility factors to fluctuations in income streams. By way of inventory efficiency, (MRNA) has trailed behind SPY, dipping 35.96% over the past 12 months, in opposition to SPY’s 23.35% uptick. This underperformance displays a scarcity of investor confidence. Then again, buyers might profit from zooming out and contemplating the long-term story.

The inventory’s brief curiosity stands at 6.36%, with 21.88 million shares brief, signaling average investor skepticism. Institutional ownership is excessive at 64.21%, however a shift in new (2,051,730 shares) versus sold-out positions (3,680,455 shares) suggests a gradual retreat from the inventory. Key gamers like Baillie Gifford & Co. and Blackrock show various changes of their holdings. Insider trading patterns present a discernible unfavorable development, with important web gross sales over the previous 12 months (-2,346,233 shares), presumably hinting at inner doubts relating to Moderna’s future trajectory. Thus, the market sentiment surrounding Moderna might be characterised as fragile.

My Evaluation and Suggestion

Buyers are drawn to Moderna’s inventory as a result of it’s each interesting and dangerous. mRNA-1083, a vaccine that combats each COVID-19 and influenza. This innovation represents Moderna’s prowess. It’s vital for buyers as a result of it suggests a reversal within the near-term income development. Presently, the market seems to be underestimating the importance and immediacy of this catalyst. As COVID-19 turns into an endemic, just like the flu, demand for a mix vaccine is anticipated to rise. Right here, Moderna stands poised to use.

Past COVID-19, Moderna’s mRNA expertise shines. Their pipeline, replete with potential most cancers therapies and different infectious illness cures, foretells constant progress. Such diversification bolsters the agency’s outlook, reaching previous pandemic-centric vaccines.

Pfizer’s comparable vaccine, which is barely forward in growth, is poised to seize a major market share. This competitors might restrict Moderna’s market penetration and income progress. Moreover, Moderna’s funds are presently being strained by important R&D expenditures. Buyers ought to maintain an in depth eye on these. Any medical setbacks might have a major affect on the inventory.

Buyers’ technique? Diversify holdings, discover hedging choices. Vigilance in monitoring medical trials and vaccine market shifts is vital for knowledgeable choices.

In conclusion, regardless of fiscal challenges and Pfizer’s shadow, Moderna’s vibrant pipeline and anticipated approval for mRNA-1083 mark it as a viable long-term biotech funding. The corporate’s strong fiscal footing, underscored by ample money reserves, reinforces this view. Amid inventory fluctuations and medical unknowns, Moderna stays a “Strong Buy” for forward-looking buyers. The pandemic-induced revenues solely scratched the floor of Moderna’s medical potential. Though revenues have declined because the pandemic, the expertise stays, and affected person buyers could also be rewarded in the end.