JHVEPhoto

Abstract

Moncler (OTCPK:MONRF) is a luxurious model retailer that serves a world buyer base. The merchandise they provide embody a number of classes, corresponding to outerwear, footwear, equipment, and so on., for each men and women. Presently, MONC has two key manufacturers: Stone Island and Moncler. The monetary contribution between the two differs primarily within the cut up between DTC (direct to shopper) and wholesale. Stone Island is extra weighted in direction of wholesale, whereas Moncler is weighted in direction of DTC. I’m recommending a purchase score for MONC as I count on efficiency forward to comply with the identical energy seen in FY23/4Q23.

MONC MONC

Feedback

MONC goes to report its 1Q24 leads to 2 weeks, and I consider MONC goes to report a robust quarter (and for FY24). My confidence stems from the sturdy momentum that MONC noticed in 4Q23, the place gross sales accelerated sequentially to 16% (900 bps acceleration vs. 3Q23). By numbers, 4Q23 gross sales grew to EUR1.178 billion. This successfully pushed natural gross sales development [OSG] on a 4-year stack foundation (4 years as a result of it compares towards pre-covid in FY19) to 74% (or 18.5% on common). Importantly, the expansion was pushed by MONC’s core model, Moncler, which noticed retail efficiency up 20% in 4Q23 (200 bps acceleration vs. 3Q23). I feel what’s extra vital right here is that development momentum was seen throughout all the expansion drivers within the equation:

- MONC managed to proceed rising retailer area (by 2% in FY23).

- MONC managed to drive double-digit development in visitors in FY23.

- MONC managed to transform this improve in visitors to transactions (with a better worth), each rising double digits in FY23 as nicely.

- In the end resulting in gross sales density reaching a report of EUR38,000/sqm

What I can infer from that is that MONC has the precise set of merchandise for the continued trend development on the proper worth level, which enabled it to seize share within the luxurious market. Primarily based on administration feedback, the place they famous a really strong begin to the yr and are very completely satisfied in all areas, this principally tells us that development momentum has continued into 1Q24 (at the very least). Contemplating that Kering really noticed a 4% decline in sales, pulled down by Gucci, the arrogance in administration’s tone could be very encouraging, which instills confidence that it ought to be capable to develop the quantity of area as guided (the information was for 10–15 new shops in FY24).

Digging deeper into the underlying development drivers, it painted an much more constructive outlook for MONC. The most important debate within the luxurious retail area is that the weak Chinese language economic system will affect discretionary spending, and we will see this within the Gucci efficiency (dragged down by China). Nevertheless, this isn’t the case for MONC. Income from Mainland China grew 21.4% on a continuing foreign money foundation and 22.7% on a reported foundation, a stark distinction vs. the main model Gucci. Much more notable is that administration noticed enchancment in retention of the cohort and that new prospects are repeatedly recruited, supported by a restoration in journey. Do not forget that MONC gave this replace on February 28, 2024, which implies they’d 2 months of 1Q24 knowledge already, successfully telling us that 1Q24 noticed no slowdown in demand.

The identical demand energy was not solely seen in China. Even neighboring nations like Japan, Korea, Indonesia, Singapore, Hainan, and Macau all did nicely; different Asia grew 31.5% in 4Q23 on a continuing foreign money foundation. What’s value mentioning right here is that MONC has managed to diversify its demand away from simply the very rich Chinese language nationals. The apparent implication is that MONC development isn’t much less unstable. The larger implication, I consider, is that it implies MONC has managed to efficiently penetrate a brand new cohort of shoppers (in different phrases, expanded its focused market), offering it extra room to develop.

It began by very wholesome and rich a really rich Chinese language, however now’s broadening additionally, the truth that completely different nations have facilitated the emission of visa is clearly serving to to restart the actions with Chinese language outdoors of China. Source: 4Q23 earnings

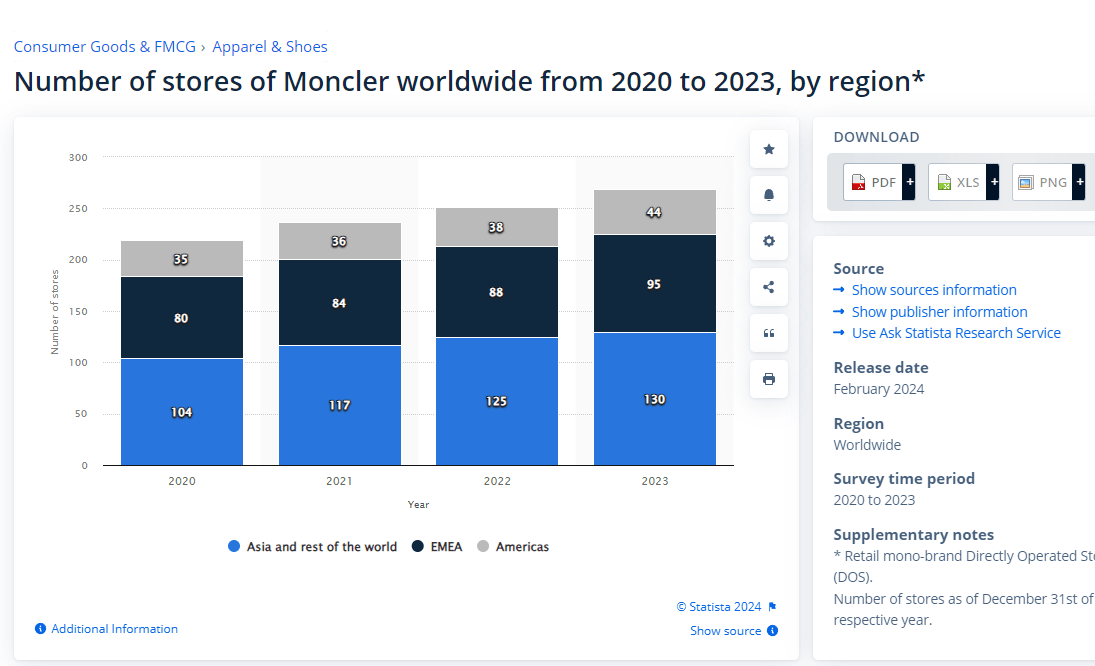

Shifting focus to the western area, each the European and American areas additionally noticed enchancment, organising nicely for 1Q24 efficiency. For Europe, MONC noticed elevated spending by the cohort, and for America, whereas it was flattish within the quarter, volumes had elevated, which I consider can proceed to develop forward given the low penetration of its Moncler model. For context, America has $25.44 trillion in GDP whereas Europe has $19.35 trillion in GDP, however by way of shops, Europe has greater than twice the variety of shops vs. America. The expansion runway is lengthy forward for MONC within the Americas.

Statista

Nevertheless, whereas I’m constructive on top-line development, margins ought to be flat in FY24 as administration technique shifting ahead is to proceed reinvesting into development – retailer openings, product assortment, and so on. throughout each manufacturers. Given the present development momentum in Asia and the lengthy runway forward for the Americas, I feel investing within the enterprise is the precise resolution.

Financials / Valuation

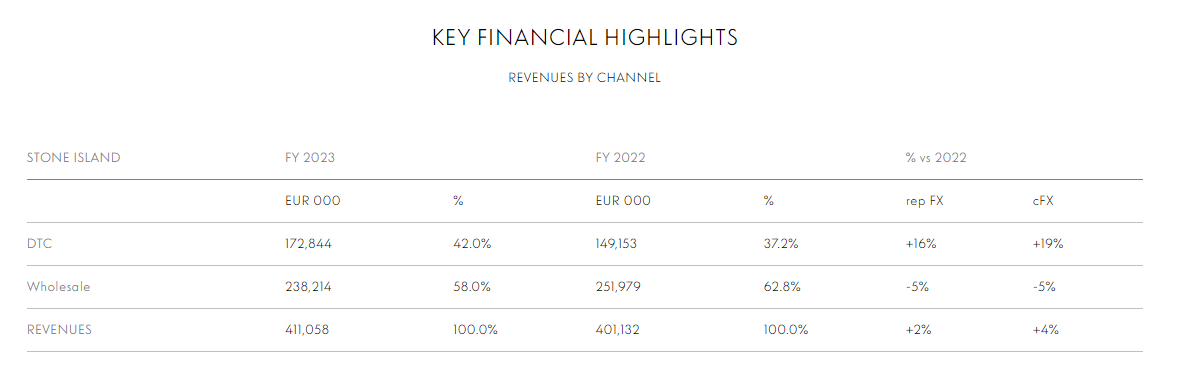

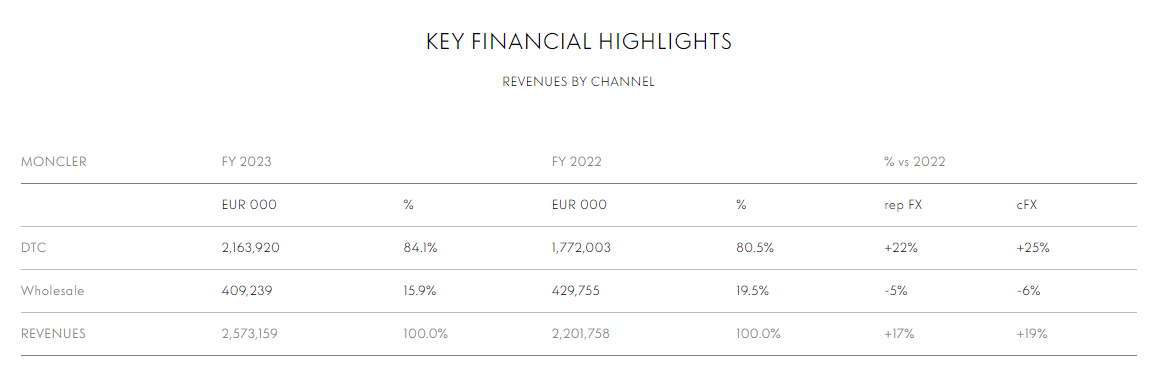

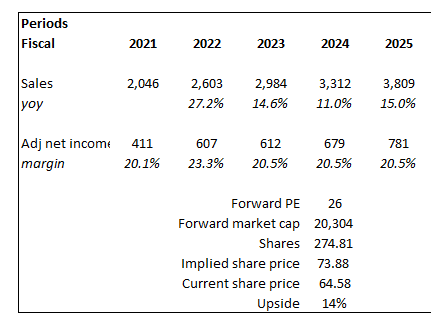

MONC reported a really sturdy FY23 lead to late February, rising income by 14.7% to EUR2.98 billion and EBIT of EUR893.8 million, representing a margin enchancment of 19bps to 30%, largely pushed by the development in gross margin (which noticed 69bps enlargement to 77.1%). The important thing reason for the development in gross margin is the income combine shift in direction of DTC, which now accounts for 84.1% of gross sales. By way of the stability sheet, MONC continues to take care of a internet money place, ending FY23 with ~EUR1 billion in money and no debt (besides working leases).

Primarily based on writer’s personal math

Primarily based on my view of the enterprise, MONC ought to proceed to see double-digit development for FY24 and FY25, with FY24 dipping again barely under the historic common of mid-teens development given the excessive base in FY22/23, adopted by a reversion to the historic imply. As I mentioned under, margins are unlikely to broaden as administration goes to reinvest extra income again into the enterprise to drive development, which I consider is the precise resolution. The important thing comps for MONC are Hermes Worldwide, LVMH, Prada, Kering, and Capri, which is buying and selling at a mean of 23.5x ahead PE at present. On common, friends are anticipated to develop excessive single-digits. Given my view that MONC ought to see low to mid-teens development forward and the sturdy relative efficiency vs. the main model, Gucci, I modeled MONC to proceed buying and selling at this premium (26x) vs. friends’ common.

Danger

On the flip aspect of MONC, figuring out the precise trend development is the important thing threat. Trend developments have a lifecycle that’s hard to predict, and if MONC is unable to increase this streak of determining the precise development, development might be closely impacted. Margins would see an analogous destiny, as MONC will doubtless must rely extra on wholesale to cut back inventories (that are unable to promote given they don’t feed customers’ preferences).

Conclusion

I’m recommending a purchase score for MONC. This previous quarter noticed continued momentum throughout all gross sales metrics, together with retailer area, visitors, and transaction worth. Importantly, administration feedback on a robust begin to the yr instills confidence because the timing of that remark was in finish February. Notably, the efficiency in China was a significant spotlight when in comparison with Gucci. MOC enlargement into new buyer segments additionally supplies additional development alternative. Though margins could not improve within the quick time period attributable to reinvestment plans, I feel it’s the proper resolution to take a position for development.

Editor’s Word: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please concentrate on the dangers related to these shares.