Michael Vi

The Federal Reserve pivot that everybody is ready in 2024 has already achieved its magic on the inventory market. Each the S&P 500 and the Nasdaq are flirting with all-time highs as soon as once more, and lots of the development shares that had been all the fad in 2020 and 2021 have drastically appreciated simply within the final couple of months. One nice instance is MongoDB (NASDAQ:MDB): the inventory cratered an astounding 70% since inflation spiked and the Fed needed to elevate rates of interest quickly; the restoration in 2023 was nevertheless wonderful by itself because the inventory has principally doubled within the final 12 months. We are actually in a state of affairs akin to the pandemic days, with shares of MongoDB buying and selling at sky-high valuations and buyers questioning in the event that they missed the boat or whether it is just the start of one thing greater.

My opinion is that MongoDB is a probably fantastic firm buying and selling at a horrible valuation. The inventory will commerce primarily based on the corporate’s development, certain, however will completely observe the market sentiment and can get knocked down if the economic system takes a flawed flip.

An ideal monitor report

MongoDB’s mission is to “empower innovators to create, transform, and disrupt industries by unleashing the power of software and data”. The idea of all the corporate’s work is a normal objective database that’s constructed on a document-based structure, an improved model of SQL. I imagine that there are only a few doubts on the standard and success of MongoDB as a service supplier given their wonderful monitor report for the reason that firm was based in 2006.

Since then, MongoDB advanced into providing a number of enterprise, database-as-a-service options to its clients that remodeled it right into a $28 billion firm with a projected income for FY2023 of $1.65 billion.

The most recent quarter noticed the corporate put up as soon as once more nice numbers: income grew about 30% to $432 million, whereas whole variety of clients grew 19% to 46,400. These are strong numbers, even higher if we solely take into account clients contributing over $100,000 in annual income which grew 28% YoY. For what’s value, a number of Wall Street analysts have expressed a light concern over the deceleration of the corporate’s trajectory, which paired with its insane valuation would possibly probably spell bother on the horizon.

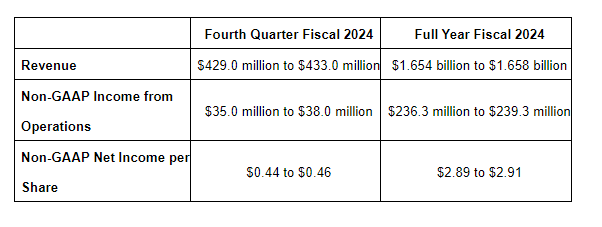

Steerage for FQ24 and full 12 months (MongoDB Q3 FY2024 press launch)

How loopy is the valuation?

MongoDB is a superb firm, rising quick and offering a service that’s cherished by the builders. Nonetheless, buyers must reckon with the truth that shares are presently buying and selling at a valuation that’s removed from cheap, no less than from a basic, value-oriented perspective. There are not any GAAP income to depend on, whereas the corporate solely just lately has been beginning to report constructive free money circulate: these two metrics are subsequently fairly ineffective to worth the corporate. So far as income goes Worth to Gross sales sits at 17.5x, not fairly an insane degree as in the course of the COVID-induced market bubble (when MDB reached highs of 45x) however nonetheless across the prime of market valuations. Does MongoDB deserve this valuation? Does any inventory, truly?

Exhausting to say. Development shares are beasts of their very own, typically buying and selling on momentum, carried by narratives and pleasure. The rock-bottom rates of interest of the final 15 years are a factor of the previous, nevertheless current exuberance concerning a possible interest rate cut by the Federal Reserve has truly pushed MongoDB’s share value not that removed from all-time highs, all issues thought-about.

With development shares for my part it is rather essential to first perceive if there’s truly meat on the bone. I do suppose that MDB has the potential to be the true deal and supply one other decade-plus of comparatively excessive development. However how briskly precisely ought to it develop to justify the present valuation?

Within the trailing twelve months the corporate recorded about $88.7 million of free money circulate, translating to about 5.5% FCF margin. The corporate is barely beginning now to considerably reliably be FCF constructive, nevertheless I feel this may quickly develop into the norm fairly than the exception. Because of wonderful gross income and scale, I feel MDB will almost definitely attain about 20% FCF margin when absolutely optimized, which is within the vary of SaaS companies within the cloud house.

Now we do a little bit of an creativeness train. Let’s think about that MongoDB is absolutely optimized at present, and already boasts a terrific FCF margin of 20%. Based mostly on $1.5 billion of TTM Income, the present imaginary FCF can be about $317 million. With a purpose to justify the present valuation of $28.2 billion, whereas assuming a reduction price of 10% the corporate would want to realize about 29% of FCF development yearly. Naturally, as at present MongoDB is barely reaching about 5.5% of FCF margin, the true development price wanted to justify the present valuation is definitely a lot increased than that, however it’s unimaginable to know the way rapidly MongoDB will be capable of absolutely optimize their operation, reign in bills and function at most profitability.

I personally wouldn’t advocate investing into something at such valuation. At these ranges anticipating any extra return coming from multiples growth appears silly, subsequently any future return should come straight from the enterprise efficiency; nevertheless, MongoDB has to knock it out of the park merely to realize an anticipated annual return of 10%, no less than primarily based on the hypothetical money circulate mannequin outlined above. Too arduous for me at these costs.

Slowly changing into worthwhile

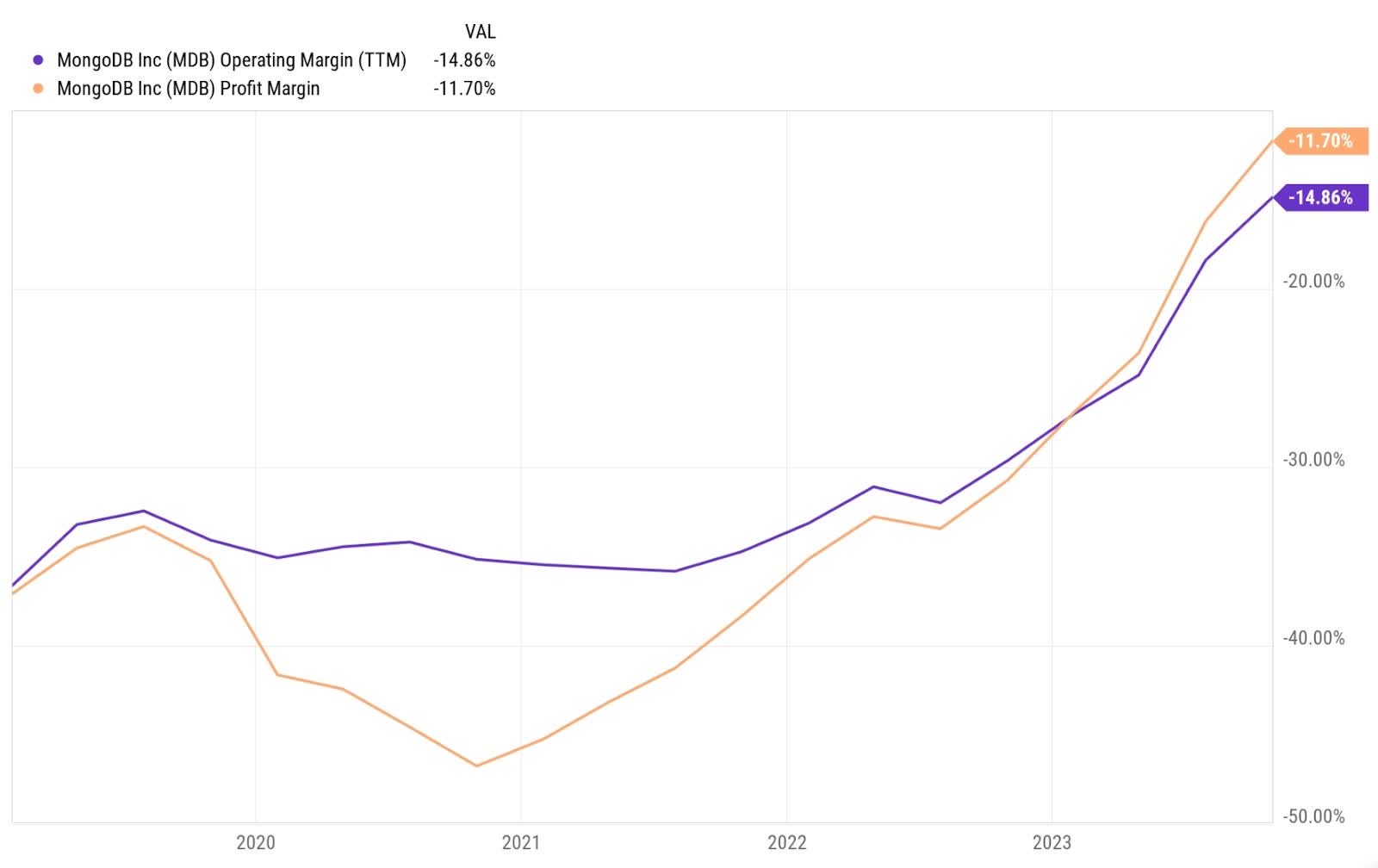

Regardless of the very steep valuation the inventory is buying and selling at, the corporate appears nonetheless removed from constant profitability. On a GAAP foundation, Working margin and Revenue margin are nonetheless very a lot destructive however the image is slowly enhancing. The newest studying exhibits TTM working and revenue margins at roughly -11.7% and -14.8%, translating to a web lack of $235 million within the trailing twelve months.

MongoDB is enhancing their working effectivity (YCharts)

Nonetheless, as with many different tech friends that is hardly the entire story. The corporate depends closely on Inventory-Based mostly Compensation (”SBC”) to reward its staff, which isn’t a money expense. By stripping out SBC and different non-cash changes, the corporate within the final 4 4 quarters managed to be free money circulate constructive in three of them, possibly proving that they lastly turned a nook and began to reliably earn constructive money from their operations.

One other indication that they may have turned a nook is the speed of development of their operational bills. For the previous 4 quarters, each price of income and whole working bills have constantly grown a lot slower than whole income. That signifies that the corporate has began to be extra environment friendly of their operations, and any of the long run development will accrue an increasing number of in the direction of their backside line. I absolutely anticipate free money circulate to be constantly constructive any longer, whereas for the web revenue to show constructive would require a for much longer time because of the excessive nominal worth of the SBC issued by the corporate yearly.

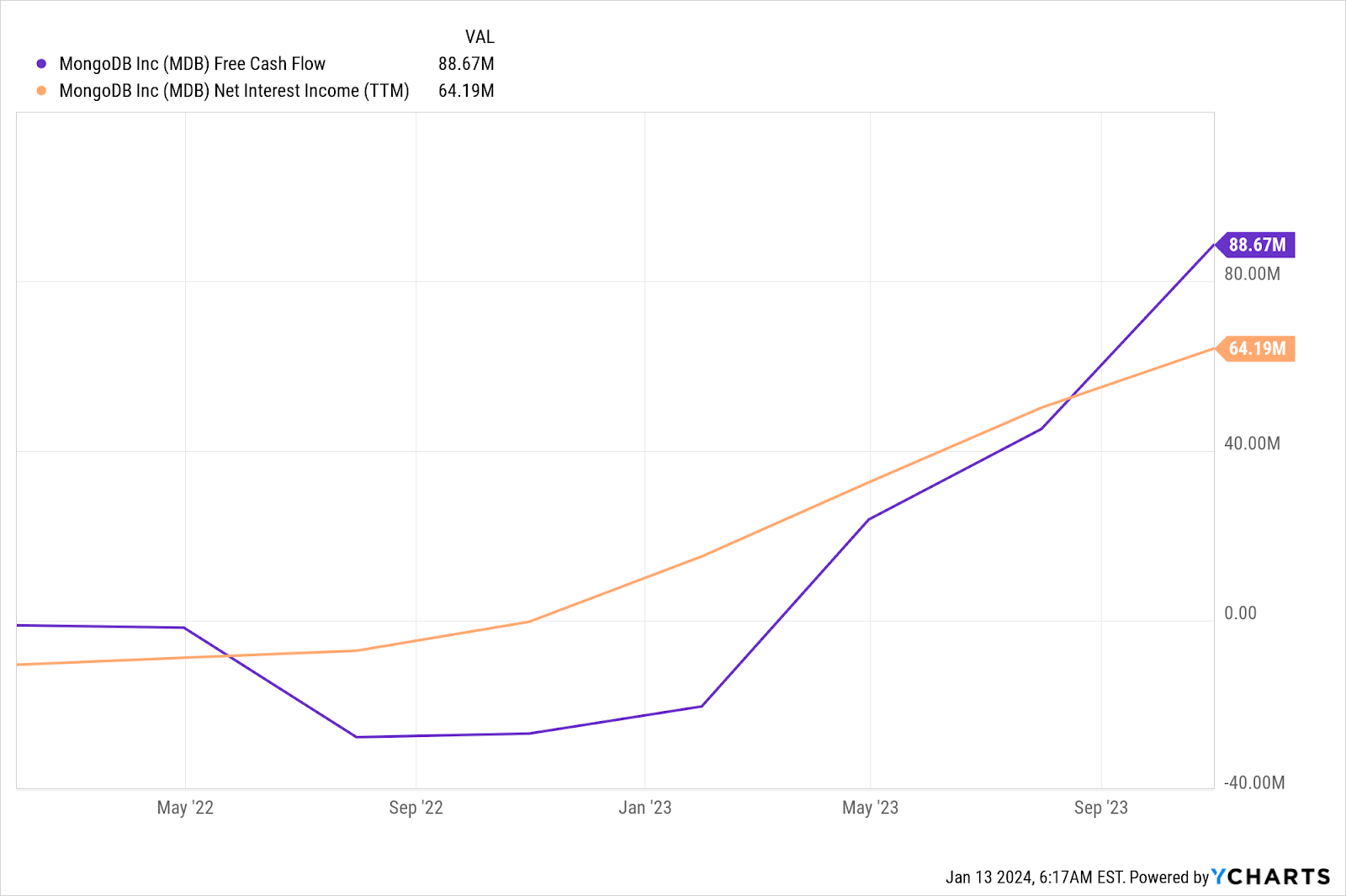

Funnily sufficient, the world the place MDB extra constantly income is from the curiosity earned on their $1.4 billion invested in marketable securities, almost definitely short-term Treasuries or cash market funds. That’s fairly ironic contemplating that rising rates of interest has been an important motive that brought about a development inventory massacre throughout 2022, however now truly permits MongoDB to earn fairly good returns reliably: after taking into account their minor debt obligations, within the final 12 months the corporate earned $64 million from pursuits on their investments, an quantity similar to their precise free money circulate however arguably even higher because it’s extra dependable and predictable.

YCharts

In any case, an inescapable drag when firms extensively depend on SBC is shareholder dilution. Over the last 4 full years (2020 to 2023) MDB has elevated the variety of shares excellent by a yearly common of 6%. One may argue that that is irrelevant on condition that the inventory value greater than doubled in the identical time-frame, nevertheless this will expose buyers to actual ache if the market stops buying and selling exuberantly, or if MDB makes some mistake alongside the best way that both adjustments the narrative round them or straight impacts their outcomes. On the very least dilution is one thing that buyers ought to pay attention to, and take it into consideration when assessing how dangerous an funding is.

Conclusion

MongoDB is a superb firm and has the potential to develop into an exquisite one sometime. That is likely to be sufficient for some buyers to provoke a place, possibly even at any value. For me nevertheless, I simply can not justify an funding at this valuation in just about something.

I like how MDB is displaying vital enhancements of their profitability and I’d be shocked if they will not be constantly FCF worthwhile already subsequent 12 months. The numbers clearly say that they supply companies that clients love, and are in a position to do it constantly above 70% gross revenue margin which is an incredible indication of doubtless excessive profitability in future.

The chance nevertheless of shopping for one thing at 17.5 occasions gross sales is that any bump on the street would possibly push your place within the pink for a few years. I feel it’s too nice of a danger for me, which makes MDB only a fantastic addition to a not so thrilling watchlist.