John W Banagan/Stone by way of Getty Photographs

Montage Gold Overview

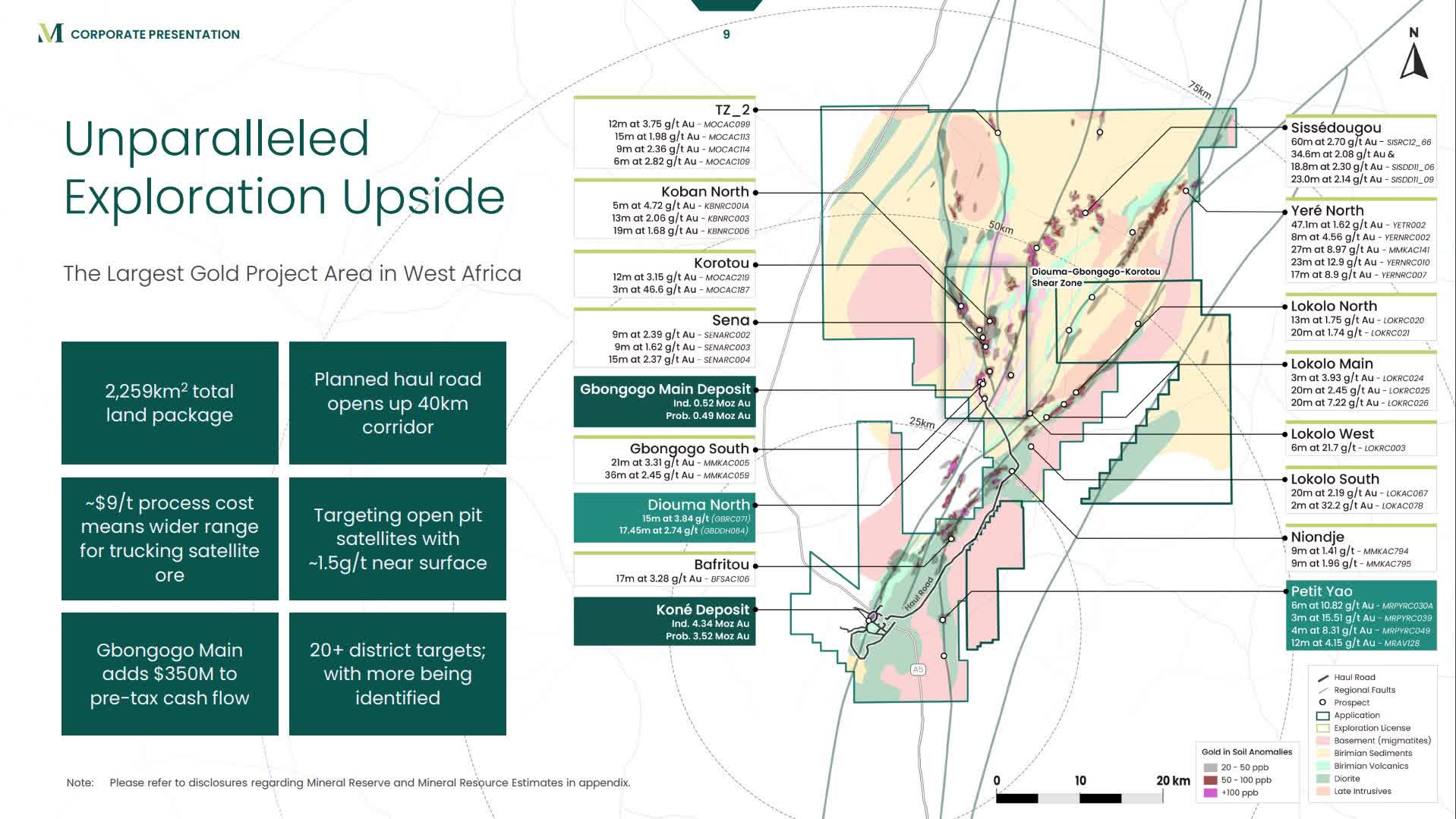

Gold miners – mid-tiers and majors included – have been in search of ever-larger mining tasks. With 4Moz of reserve and a first-three-year anticipated common manufacturing of 349koz, Montage Gold’s (OTCQX:MAUTF) (TSXV:MAU:CA) Koné gold challenge is the biggest undeveloped standalone gold challenge in West Africa. LOM AISC of $998/ouncescompares favorably to the present prices of most mining corporations, and naturally to the present worth of gold at roughly $2000/oz. NPV5 at $1850 gold is estimated to be $1.1B, which provides the challenge a horny NPV5/capex ratio of 1.53. Moreover, the big 2259 km2 land bundle surrounding the primary Koné deposit is extraordinarily potential, with many important preliminary discoveries made ready for follow-up drilling.

Koné gold challenge (Montage Gold)

M&A pattern

M&A is heating up within the house – inside latest months, two builders of African gold tasks have obtained bids from two completely different events. Osino Sources is anticipated to be acquired by “a foreign-based mining company”, outbidding Dundee Treasured Metals, which subsequently declined to make one other bid. The opposite is OreCorp which is anticipated to be acquired by Silvercorp, outbidding Perseus Mining (which additionally owns 18% of Montage Gold). I’ll return to those two related friends later within the article.

www.montagegoldcorp.com

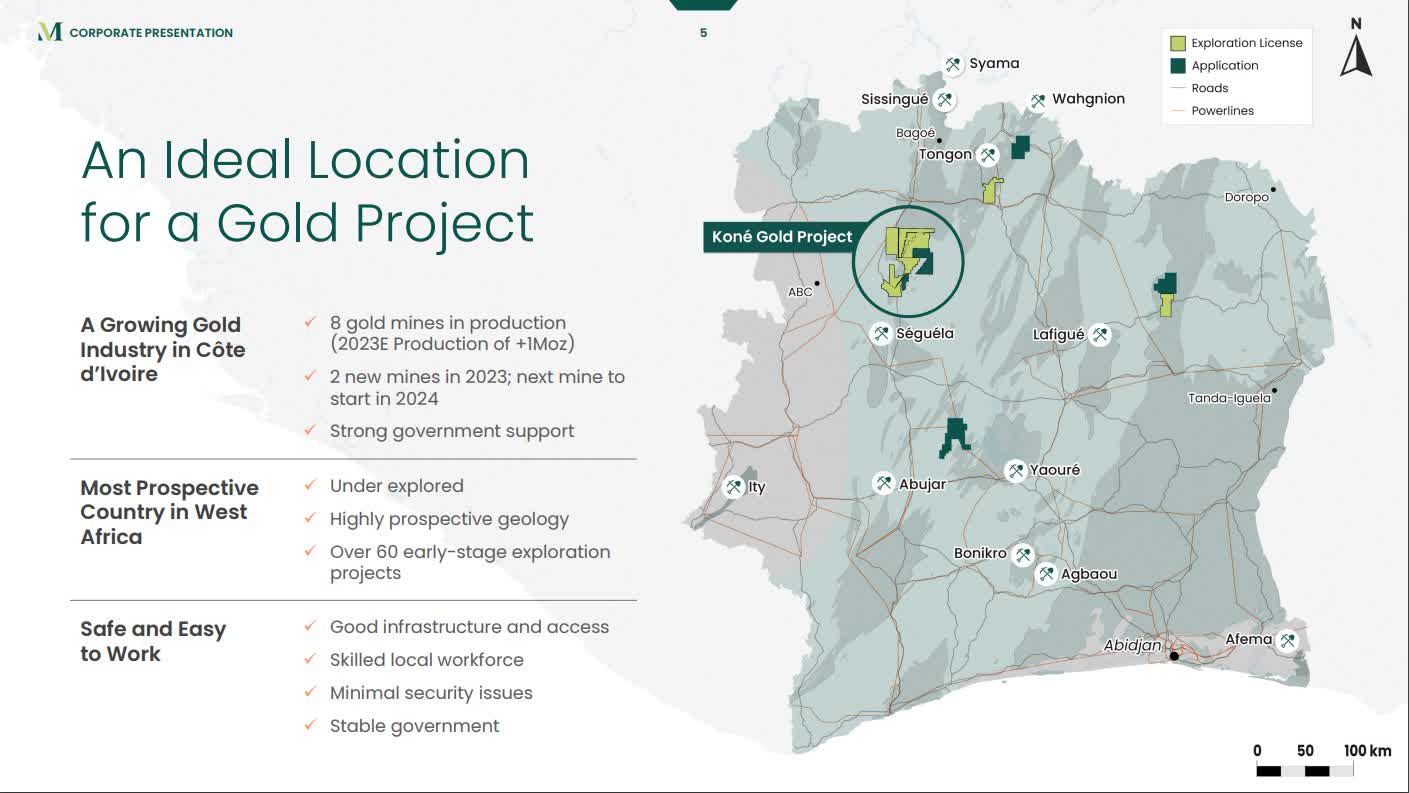

The challenge location of Côte d’Ivoire is not precisely a low-risk jurisdiction, however I might argue that it’s a prime jurisdiction amongst its African friends. Its northern neighbours, Mali and Burkina Faso, have, for instance, skilled growing issues with extremist Islamist teams destabilizing the Sahel area, on prime of a number of latest coups. Côte d’Ivoire has been comparatively steady for many years, and had two new mines getting into manufacturing final yr with one other one coming on-line this yr, indicating continued investor confidence within the nation.

www.montagegoldcorp.com

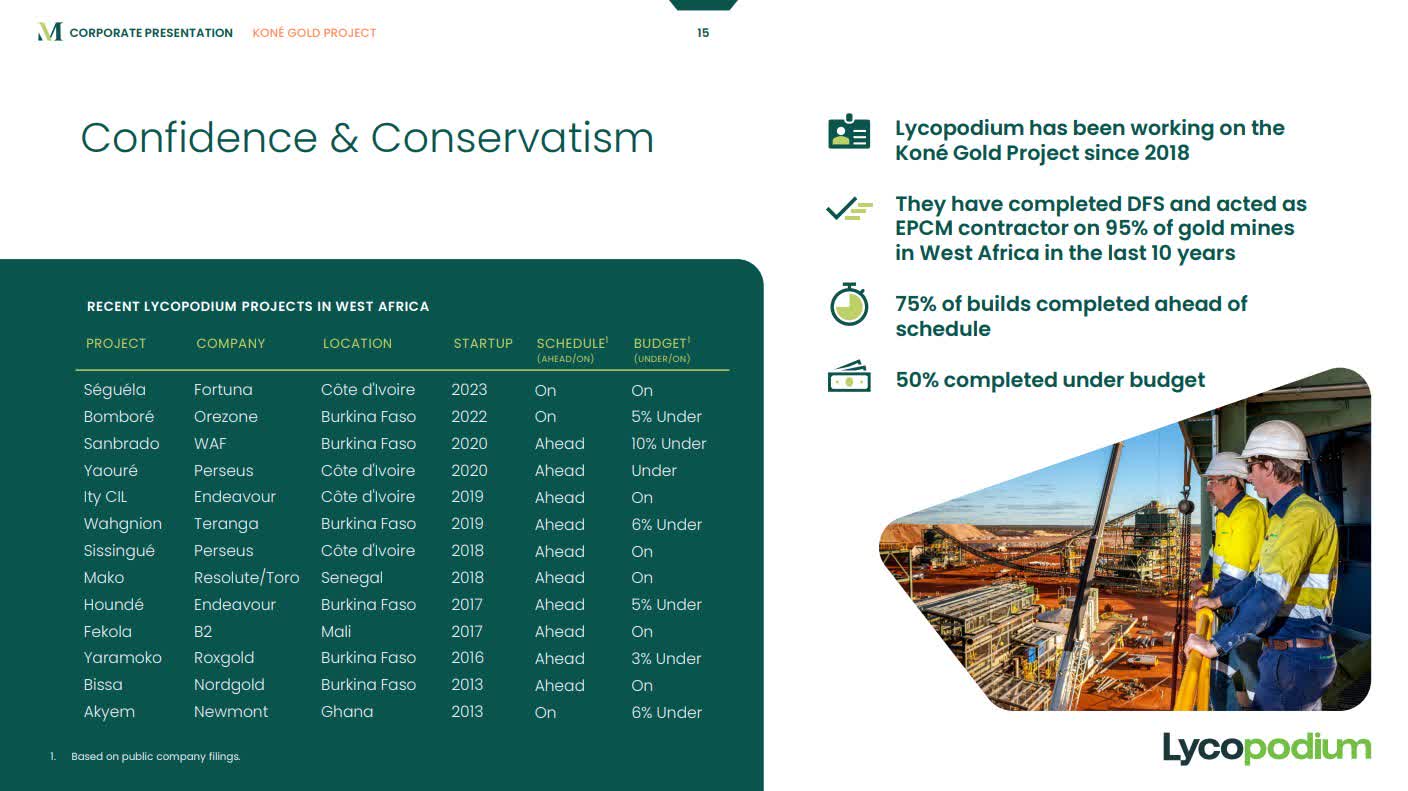

Earlier than delving additional into the small print of Montage’s Koné challenge, I want to level to the extraordinarily spectacular monitor file of Lycopodium, the corporate that produced the Koné feasibility research and is anticipated to construct the mine as effectively.

One thing you be taught after following the mining sector for some time is that particularly PEAs, but in addition PFS and FS research, oftentimes don’t maintain up in the actual world. Personally, I add at the least 20% to price estimates utilized in PEAs, except issued by a senior producer. I’m wondering if there has ever been a mine that ended up with decrease prices than was estimated in its PEA. Having the ability to trust within the financials laid out is, in fact, crucial.

www.montagegoldcorp.com

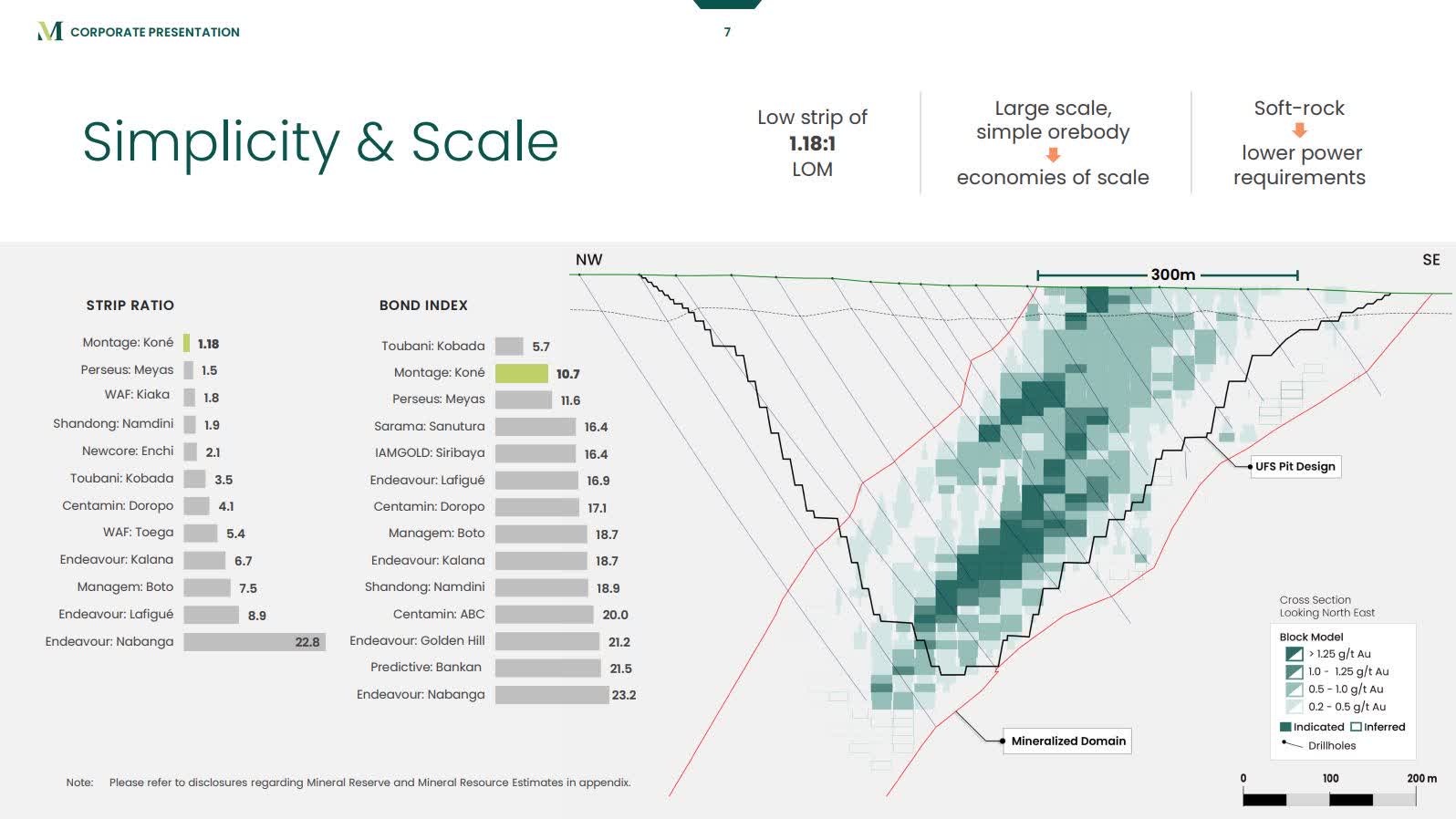

The primary Koné deposit is a straightforward 0.7 g/t low-grade orebody, that might be mined at a low strip of 1:1. Which means the optimistic financial affect of satellite tv for pc deposits with higher-grade ounces could be very massive, even when the strip ratio is considerably larger, like is the case for the just lately added 475koz Gbongogo deposit (3.77 strip, 1.43 g/t). Contemplating the standard and scope of discoveries already made within the district, it appears possible, for my part, that there are at the least a couple of extra Gbongogos.

With preliminary capex estimated to be $712M, the capital depth of $178/reserve ouncescompares favorably to latest open pit tasks accomplished in Canada. These embrace Equinox’s Greenstone mine at $221/reserve oz, Argonaut’s Magino mine at $317/reserve oz, and IAMGOLD’s Cote Gold mine at a towering $366/reserve ouncesspent in preliminary capex.

www.montagegold.com

The administration workforce at Montage is similar that efficiently grew the West African-focused Crimson Again Mining, earlier than selling it to Kinross in 2010 for US$7.1B. So, management seems to be extremely competent.

A short have a look at financials

Montage Gold had C$6.6M in money on the finish of final yr and no debt. Spending is comparatively low now that the feasibility research is full, with some ongoing exploration of potential satellite tv for pc deposits. They may most likely want to lift capital in a couple of quarters, however I do not see this as a big concern as Montage appears to have had easy accessibility to capital markets thus far, with the newest financing being on April twelfth of final yr, executed at a worth near market with no warrants, which is uncommon for builders of this measurement. With bills being low till building begins, I might count on any potential fairness elevate previous to building financing or take-out to be minor.

www.montagegold.com

Progress with Koné challenge might invite bids

2024 is shaping as much as be a giant yr for Montage Gold. Often, producers wait till a challenge is shovel-ready, or near it, earlier than making a bid, as was the case with the 2 different African gold tasks that had been just lately bid on. So, with the Koné challenge anticipated to be shovel-ready by Q3, we’re getting into the interval the place bids are probably to return.

Presently, Montage Gold has a market cap of US$100M, which interprets to $25/reserve oz. Compared, OreCorp’s most up-to-date bid from Silvercorp values the corporate at $184M, or $71/reserve oz. OreCorp’s challenge has reserves of two.6Moz, common manufacturing of 242koz over the primary ten years, a capital effectivity of $182/reserve ouncesin preliminary capital, and an AISC of $954/oz. These figures are similar to these of the Koné challenge, and it is price noting that the OreCorp research was launched 17 months earlier, so, adjusting for inflation, OreCorp’s prices can be barely larger in an apples-to-apples comparability.

Osino Sources’ acquisition bid from this week valued Osino at $273M, or a excessive $127/reserve oz. The Osino challenge has reserves of two.15Moz, anticipated manufacturing of 162koz over the primary ten years, a capital effectivity of $127/reserve oz, and an AISC of $1011/oz. The challenge has a powerful capital effectivity, however it’s additionally the smallest of the three by way of manufacturing.

Going by the numbers, I might say Koné compares effectively towards these two tasks that had been just lately bid on, particularly contemplating that Koné is considerably bigger than the opposite two. So, will Montage Gold get purchased out, and at what worth? Taking all the pieces into consideration, I believe there’s a good likelihood an acquisition bid will come earlier than Montage begins constructing the mine themselves, which is the present plan. Within the case of no take-out supply, I believe the corporate remains to be strongly positioned to have the ability to discover building financing, given the, for my part, general attractiveness of the Koné challenge, the jurisdiction, and administration’s expertise in constructing and working mines in West Africa. With capex of $712M and a present market cap of $100M, it is clearly not going to be simple although, and there may be actually a threat of the corporate not with the ability to discover building financing, particularly if the gold worth weakens.

Valuation

Valuing small builders like Montage is all the time a problem, as you’ll be able to simply change assumptions that drastically alter the valuation. As issues stand right this moment, I believe a valuation of $200M, or double the present market cap at 70c/share, is affordable. It will translate to $50/reserve ouncesand nonetheless go away room for a take-out premium, earlier than reaching the valuation degree of OreCorp and Osino at $71/reserve ouncesand $127/reserve oz. I due to this fact charge Montage Gold a Robust Purchase.

One final argument that I believe additional helps the Robust Purchase on Montage, is that an financial downturn, which I believe is probably going contemplating how stretched the financial cycle is, might decrease the price of fundamental supplies and thereby scale back preliminary capex. This impact might have a really important affect on the valuation of Koné, as a ten% discount in capex would translate into $71M in financial savings, which is the same as round 70% of Montage Gold’s present market cap.

Dangers and Conclusion

Montage Gold being a micro-cap inventory, it is all the time necessary to maintain threat in thoughts. The primary threat for Montage, other than decrease gold costs, might be not getting the challenge allow. I believe it is unlikely, but when it had been to occur, it might clearly lead to a cratering of the inventory worth, as a mining challenge just isn’t price a lot, if something, if it could actually’t get permitted.

As a last observe, I’ll remind any potential investor that Montage is a micro-cap inventory and has poor liquidity, so all the time use restrict orders. Additionally, needless to say the inventory has a lot better liquidity on the Canadian alternate in comparison with the American. As all the time, I might be joyful to speak within the remark part beneath.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a significant U.S. alternate. Please pay attention to the dangers related to these shares.