Sakorn Sukkasemsakorn

Montauk Renewables, Inc. (NASDAQ:MNTK) lately delivered EPS in step with expectations, and administration continues to report quarterly web earnings progress. In my opinion, the current announcement about new reactors and manufacturing improve from 2026 make MNTK a purchase. Sure, I did discover a number of dangers coming from modifications in power costs, new regulatory requirements for renewable power, and speedy technical modifications. Nevertheless, even contemplating the dangers, MNTK does look fairly undervalued.

Montauk Renewables

Montauk Renewables is a renewable power firm specializing within the restoration and processing of biogas from landfills and different non-fossil sources for helpful use as an alternative to fossil fuels. It develops, owns, and operates Renewable Pure Fuel or RNG initiatives, utilizing confirmed applied sciences that provide renewable gasoline to the transportation and electrical energy sectors.

It is likely one of the largest RNG producers within the United States, with greater than 30 years of expertise within the trade. It has established an working portfolio with 12 RNG initiatives and three Renewable Electrical energy initiatives via self-development, partnerships, and acquisitions, spanning six states.

The corporate’s main prospects for RNG gross sales embrace giant homeowners or long-term operators of landfills and livestock farms in addition to native utilities and huge refineries within the pure fuel sector. In relation to Renewable Electrical energy, its typical prospects are municipal electrical energy utilities or privately owned utilities.

The income Montauk receives from the sale of renewable power consists of two foremost elements. The primary element is income derived from the commodity worth of pure fuel or electrical energy generated, which it sells via quite a lot of fixed-term agreements. The second element comes from the inducement applications granted to the manufacturing of Renewable Pure Fuel and Renewable Electrical energy offered by the USA.

The corporate identifies secure sources of biogas feedstocks and secures long-term provide rights. It designs, builds, owns, and operates services that convert biogas to RNG or use the processed biogas to supply Renewable Electrical energy. The corporate establishes agreements with transportation corporations and different kinds of corporations that prioritize the consumption of renewable power. Electrical energy gross sales agreements are established on a long-term foundation with respected counterparties, usually via a hard and fast worth with scales.

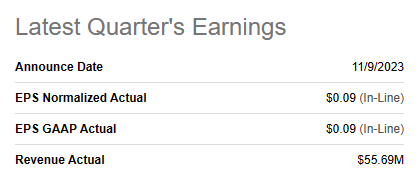

Latest Earnings Have been In Line With Expectations, With Much less Working Bills

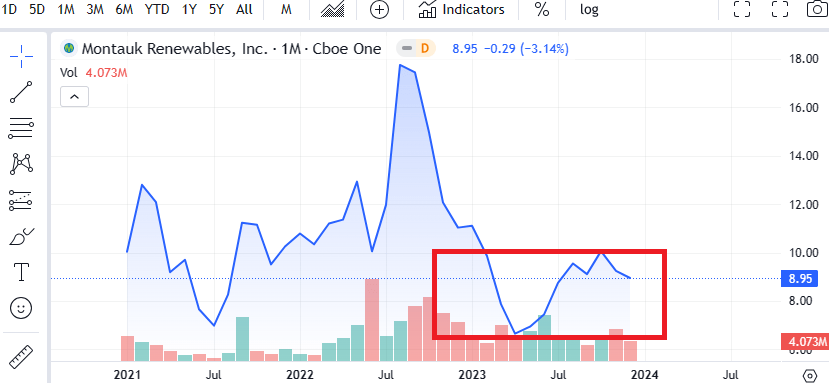

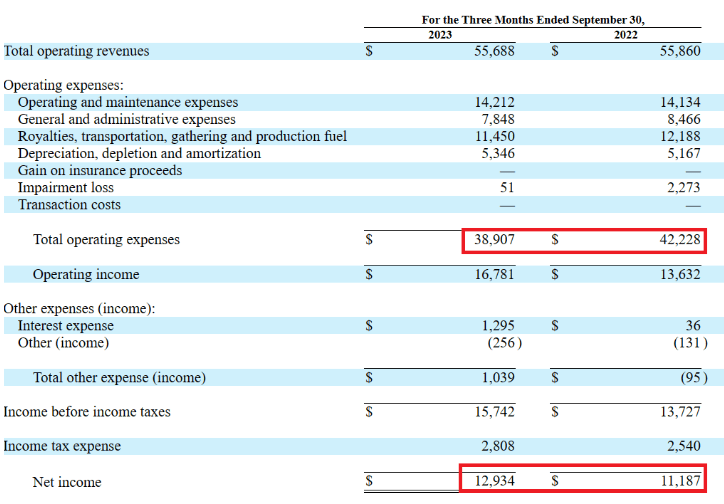

With the corporate delivering EPS in step with expectations, near $0.09, and quarterly income of about $55.69 million, I don’t suppose the market is paying plenty of consideration to Montauk Renewables. The corporate is buying and selling at multi-year lows.

Supply: SA

Supply: SA

With that concerning the current modifications within the inventory worth, I imagine that the numbers lately delivered by Montauk Renewables have been very helpful. The corporate famous lowering quarterly working bills y/y in addition to rising quarterly net income growth.

Supply: 10-Q

Steadiness Sheet

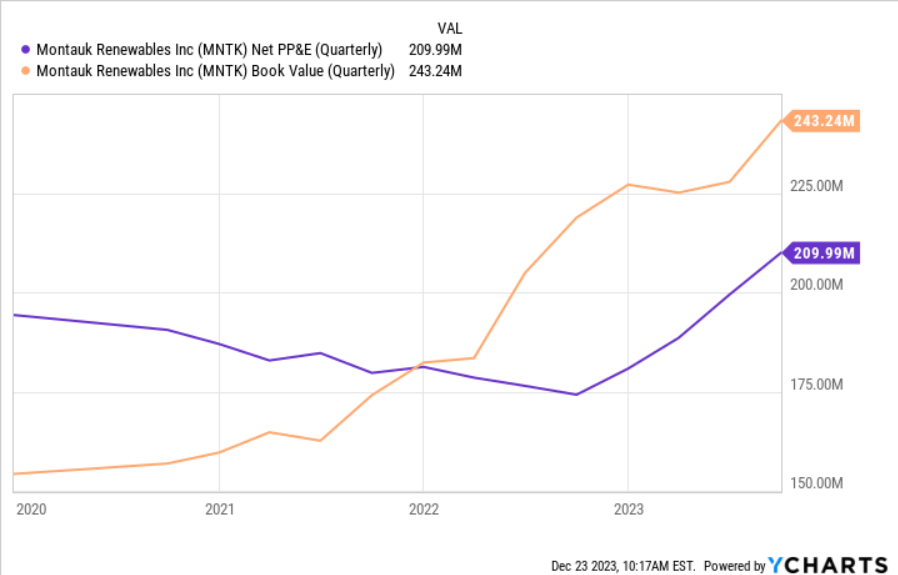

Montauk Renewables experiences a stability sheet with little working capital wants, a major amount of money, and a few debt that’s used to finance new property and tools. Given the current improve in ebook worth, will increase in property and tools, and the overall quantity of debt, plainly there are a couple of shareholders which can be investing a significant quantity of {dollars} to extend the corporate’s capability.

Supply: Ycharts

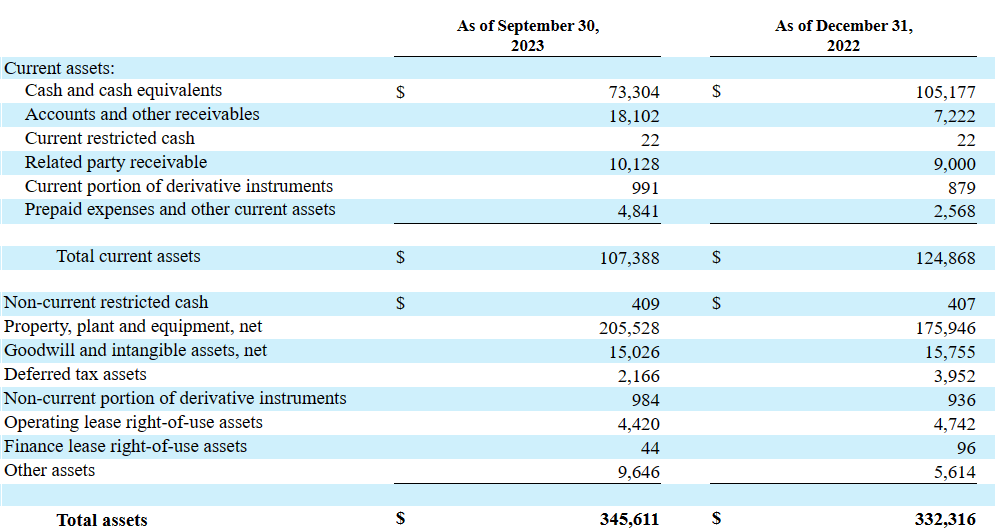

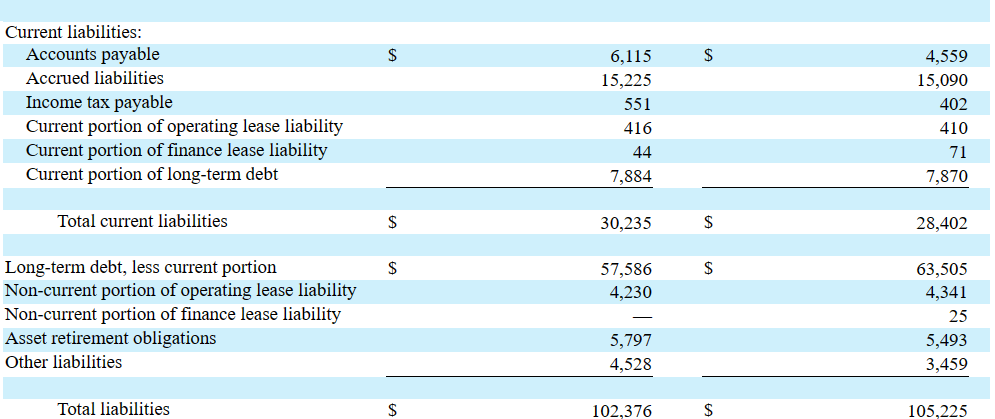

Extra specifically, as of September 30, 2023, Montauk Renewables reported money and money equivalents of about $73 million, accounts and different receivables value $18 million, and complete present property value $107 million. The present ratio is bigger than 3x, so I’m not actually involved concerning the complete quantity of liquidity.

Property, plant, and tools stands at near $205 million, with goodwill and intangible property value $15 million, deferred tax property of $2 million, and complete property value $345 million. The asset/legal responsibility ratio is near 3x, so I might say that the stability sheet seems fairly secure.

Supply: 10-Q

With accounts payable near $6 million and accrued liabilities of about $15 million, present portion of long-term debt stands at about $7 million, with long-term debt value $57 million. The corporate additionally reported asset retirement obligations value $5 million, which I didn’t embrace for the calculation of the web debt and complete liabilities of $102 million. Given the FCF projections by different traders and the present EBITDA ranges, I’m not involved concerning the complete quantity of debt.

Supply: 10-Q

Debt Agreements, Curiosity Price, And Price Of Capital Assumed

I’m not involved concerning the complete quantity of debt, nonetheless I might be operating a reduced money move mannequin. I imagine that learning the price of debt and value of capital would assist in the evaluation of the WACC.

Previously, I noticed administration signing debt agreements with rates of interest starting from 4% to 2%. Nevertheless, extra lately, the corporate famous rates of interest shut to six%. With this in thoughts, I assume {that a} price of capital near 2% and seven% would make sense.

The time period mortgage amortizes in quarterly installments of $2,000 via December 2024, quarterly installments of $3,000 from 2025 via the maturity, with a ultimate cost of $32,000, of December 21, 2026 with an rate of interest of 4.12% and a couple of.91% at December 31, 2022 and 2021, respectively. The revolving and time period loans beneath the Amended Credit score Settlement bear curiosity on the BSBY Margin or Base Price Margin based mostly on our Whole Leverage Ratio (in every case, as these phrases are outlined within the Amended Credit score Settlement). Supply: 10-k

Borrowings of the time period loans and revolving credit score facility bear curiosity on the Bloomberg Quick-Time period Financial institution Yield Index Price plus an relevant margin. Rates of interest as of September 30, 2023 and December 31, 2022 have been 6.38% and 4.12%, respectively. Supply: 10-Q

Underneath My Monetary Mannequin, I Assumed That New RNG Demand, New Worth-added Providers, And Additional Diversification Of Actions Might Carry FCF Development

In my opinion, the enterprise technique is centered on three precedence areas. The primary is to proceed diversification within the vary of agricultural uncooked supplies used for RNG manufacturing. On this sense, funding in third-party know-how can also be thought of to extend productive efficiency.

Then again, Montauk considers the necessity to optimize property and its portfolio of current initiatives in addition to to develop new initiatives as applicable. Specifically, it’s proposed to detect circumstances by which it’s doable to transform renewable electrical energy demand into RNG demand.

In the end, it’s thought of helpful to supply value-added providers. That is what the corporate has achieved all through its historical past because it has at all times targeted on the excellent improvement of the manufacturing course of contemplating engineering, development, administration, operation, and supervision of human assets.

Montauk Renewables Promised New Income Producing Actions Starting In 2025 And New Reactors In 2024.

I imagine that probably the most minimal significant communication made lately is the brand new addition of seven new reactors which is able to happen in 2024. Additionally it is value contemplating that income producing actions are additionally anticipated to happen from 2025. With all this in thoughts, I imagine that we might see an accelerating web gross sales from 2024 and 2025 and free cash flow growth in these years.

Supply: Buyers Presentation

The corporate additionally made a major variety of guarantees with respect to will increase in annual manufacturing to start in 2026. In two years, administration famous that manufacturing might attain 45 to 50 thousand MWh equivalents.

Supply: Buyers Presentation

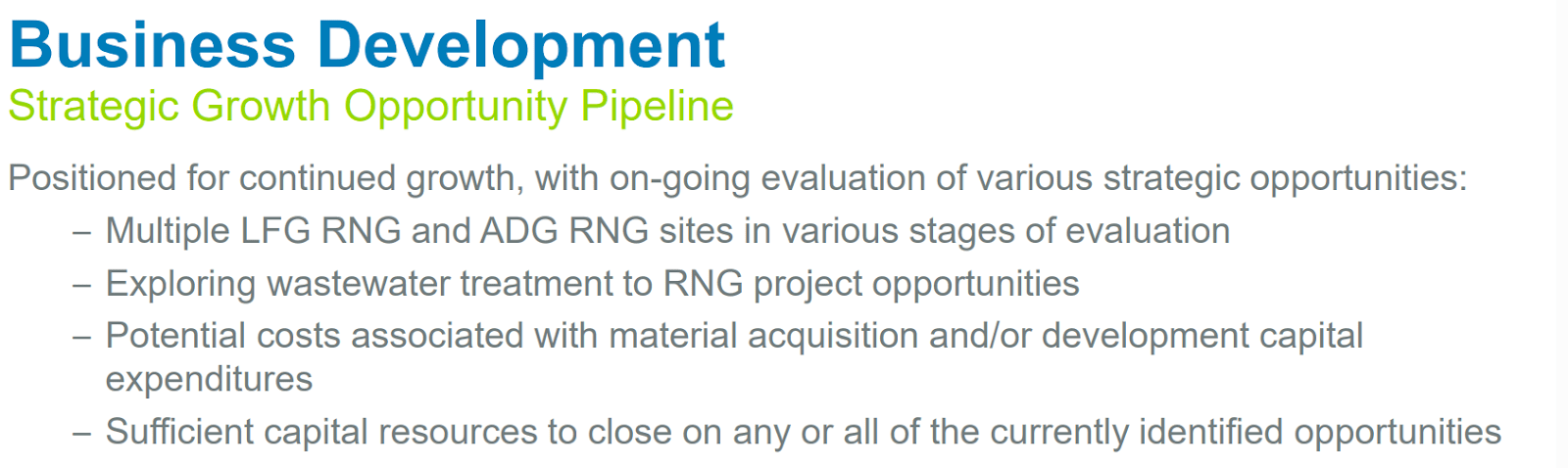

Montauk Renewables Seems To Have Enough Sources And A number of Strategic Alternatives, Which Might Be Introduced In The Future.

Given the present state of the stability sheet and the overall amount of money accrued, it’s honest to say that the corporate is properly outfitted to think about new alternatives. Within the final presentation to traders, the corporate offered an inventory of potential initiatives that included new LFG RNG and ADG RNG websites, water remedies initiatives, and different associated acquisitions. In my opinion, any improve in new capability will almost certainly result in will increase in FCF expectations. Consequently, we may even see new traders within the firm’s inventory.

Supply: Buyers Presentation

My Expectations Embody Conservative Internet Earnings Development And FCF Development

My monetary expectations are primarily based mostly on the expectations of different analysts, who lately delivered helpful EPS revisions and my very own assumptions. I imagine that my figures are very conservative.

Supply: SA

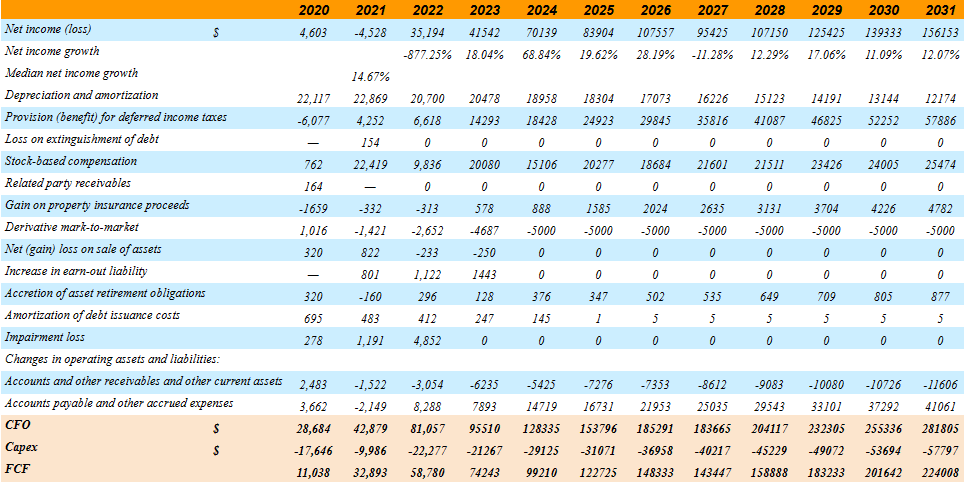

2031 web earnings stands at near $156 million, with 2031 depreciation and amortization of $12 million, provision for deferred earnings taxes value $57 million, and 2031 stock-based compensation near $25 million.

In addition to, with acquire on property insurance coverage proceeds near $4 million, by-product mark-to-market changes and settlements of about -$5 million, and modifications in accounts payable and different accrued bills of about $41 million, 2031 CFO could be near $281 million. Additionally, with 2031 capex of -$58 million, 2031 FCF could be about $224 million.

Supply: Writer’s Work

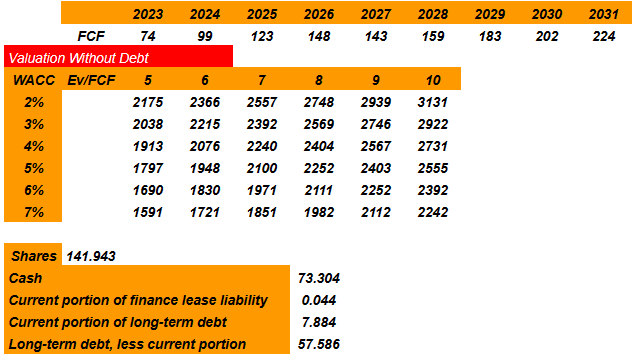

Contemplating a FCF of about $74 million and $224 million from 2023 to 2031, a WACC between 2% and seven%, and EV/FCF of 5x-10x, I obtained an implied valuation with out debt of $1.5-$3 billion. With a WACC of 4%-5% and EV/FCF of 7x, the implied valuation could be near $2.2-$2.4 billion.

Observe that my exit a number of seems to be near median Price/Cash Flow reported in the sector of 7x. As talked about earlier, I imagine that my assumptions are fairly conservative.

Supply: Writer’s Work

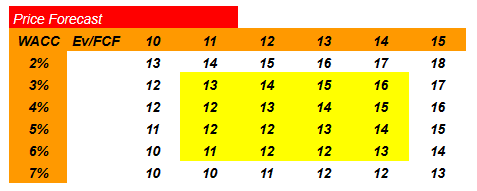

Dividing by the share depend, I obtained a valuation of near $10-$18 per share, however the median valuation resulted in near $12-$14 per share.

Supply: Writer’s Work

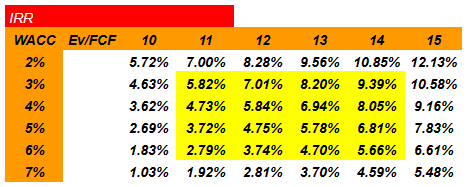

Lastly, the interior charge of return would come with a most valuation of 12% and a median IRR of 4.7%-7%. With these figures, I might say that there’s a sure undervaluation.

Supply: Writer’s Work

Competitors

Competitors within the renewable power enterprise ranges from different venture builders to service or tools suppliers, however the principle competitors comes from different corporations or options searching for to entry biogas from waste.

The biogas market is very fragmented, however Montauk maintains that its dimension in comparison with many different related corporations in addition to its capital construction put it in a robust place to compete for brand new venture improvement alternatives or acquisitions of current initiatives.

The corporate’s foremost rivals are Archaea Vitality, Morrow Renewables, OPAL Fuels (OPAL), U.S. Acquire, Brightmark, and AMP Vitality in addition to corporations with biogas-to-energy services as a phase or subsidiary of their operations, together with DTE and Ameresco. Moreover, sure landfill operators, equivalent to Waste Administration (WM), have additionally chosen to selectively pursue biogas conversion initiatives at their websites. Lastly, Republic has partnered with Archaea Vitality to develop sure of its places.

Dangers

The focus of revenues in a couple of main prospects and the geographic focus of its initiatives expose the corporate to higher manufacturing dangers. Additionally it is doable that a number of landfill homeowners might search to put in their very own biogas manufacturing initiatives on their websites, which would scale back the variety of alternatives for brand new venture improvement.

Moreover, the achievement of economic aims is tied to the projected demand for renewable power. Then again, the opportunity of a discount or elimination of presidency financial incentives for the renewable power market have to be thought of.

The corporate can also be uncovered to commodity costs, regulatory requirements for renewable power, and the speedy technical modifications that happen in relation to the renewable power manufacturing course of.

My Takeaway

With rising quarterly web earnings y/y and helpful EPS revisions for the brand new quarter, Montauk Renewables additionally introduced new reactors, capability will increase, and manufacturing improve from 2026. I don’t suppose that market individuals had a have a look at the expectations of administration and potential FCF era within the coming years. All put collectively, for my part, makes Montauk Renewables a purchase. Sure, there are apparent dangers from modifications within the worth of power and pure fuel, decrease capability enlargement than anticipated, or modifications in environmental legal guidelines and rules. With that, I believe that Montauk Renewables stays undervalued.