Nikada

Companies that create benchmarks and requirements which might be helpful for whole industries are sometimes capable of construct distinctive aggressive benefits. That is considerably true for MSCI Inc. (NYSE:MSCI). MSCI’s indexes are well-known all through the funding administration world. However MSCI’s success over the previous decade and potential success shifting ahead has extra to do with savvy forward-looking choices than what is mostly considered to be a moat.

MSCI, S&P Dow Jones (SPGI), FTSE Russell (OTCPK:LDNXF), CRSP, and Nasdaq (NDAQ) seize 95% of the index ETF market. This market share dynamic doubtless extends to all cases the place benchmarks are used. Whereas the CEO of Amundi (OTCPK:AMDUF) went so far as calling index providers an oligopoly, that could be a liberal use of the phrase.

Assessing the power of administration groups is commonly not clear-cut, however there might be indicators that administration is pondering like buyers. Throughout info providers, the most effective companies are arguably those who have created proprietary score methods: S&P World, Moody’s (MCO), and Honest Isaac (FICO). Whereas every enterprise is basically totally different, and the jockey cannot make the horse run sooner, MSCI’s newer initiatives present administration has a deep understanding of this dynamic.

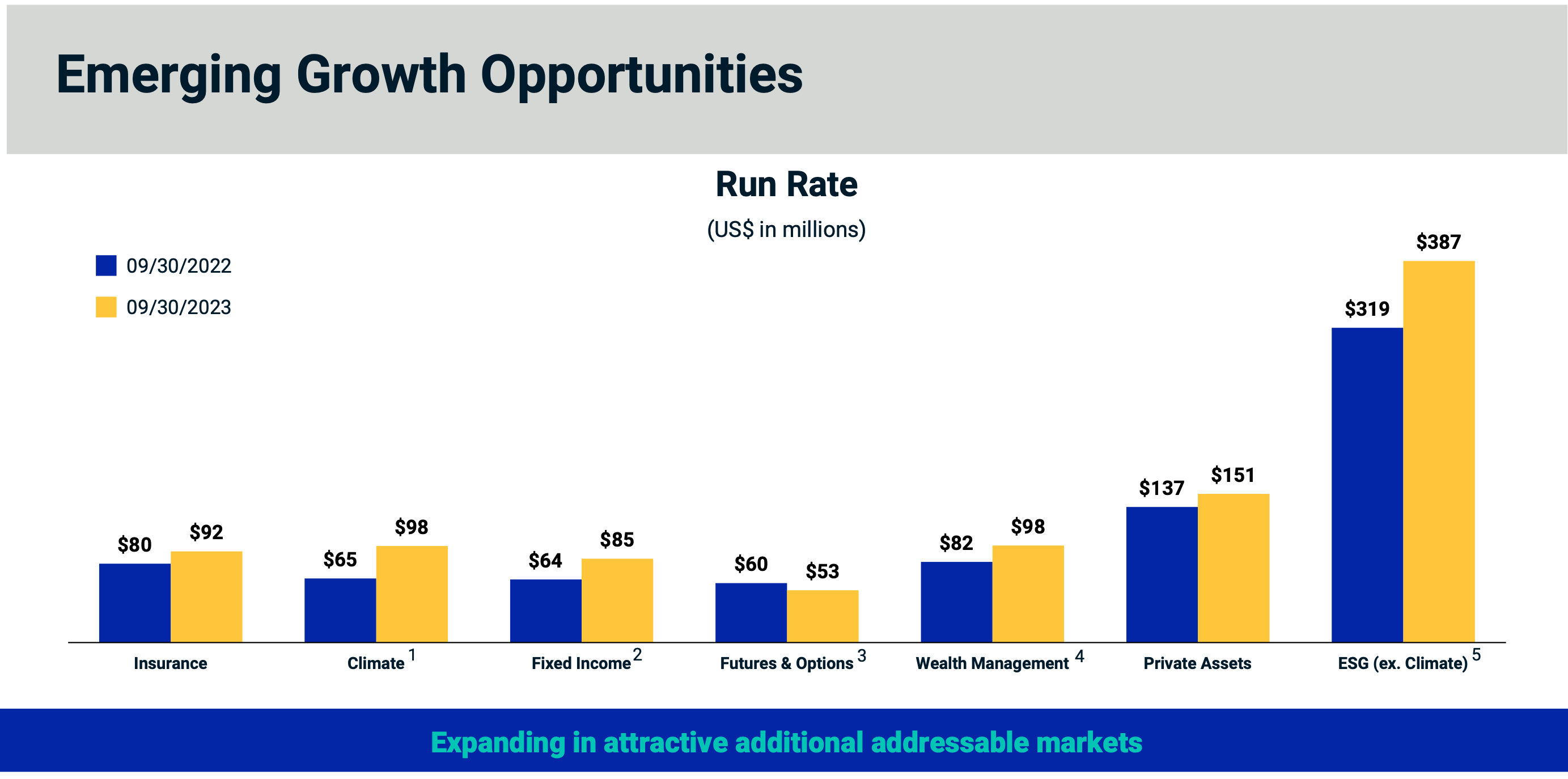

Together with bolstering the prominence of its indices, MSCI is making an attempt to unfold its tentacles into new areas, primarily in ESG and personal belongings. For example:

Our ESG rankings goal to measure an organization’s resilience to long-term ESG dangers. Firms are scored on an industry-relative scale throughout probably the most related key ESG points primarily based on an organization’s enterprise mannequin…Traders use MSCI ESG Rankings for a wide range of functions, together with to help with basic or quantitative evaluation, portfolio building and threat administration, engagement and thought management, benchmarking and customized index design.

Whereas it would not seem to be ESG scores are outstanding in asset administration at present, the income run charge is closing in on $400M. Extra importantly, the considered administration making an attempt to construct deeply ingrained moats proper earlier than our eyes is sort of astounding and uncommon. If MSCI is ready to strike gold on ESG rankings or one other future system, it may very well be a closely moated, decades-long compounding enterprise.

MSCI Investor Presentation

MSCI has additionally made some fascinating M&A strikes, most notably the current acquisitions of Burgiss and Cloth. Burgiss supplies indexes for personal belongings, which might help funding managers to raised bogey efficiency versus true friends, as a substitute of merely public market comps. Burgiss provided this case study for the South Carolina Retirement Funding Fee.

With the Fabric acquisition, MSCI is leaning into the expansion of the wealth managers {industry}. MSCI deeply understands the shifting winds of funding administration, as evidenced by this assertion of their 10-k:

the development and administration of funding portfolios have gotten more and more outcome-oriented, rules-based and technology-driven.

MSCI has already been an enormous beneficiary of passive indexing, and it’s persevering with to lean into the tendencies taking up funding administration to seek out further avenues for development.

Aggressive Benefit:

Simply over a decade in the past, MSCI’s indexes were dropped by plenty of funds from Vanguard, the world’s second-largest asset administration agency, in an effort to decrease prices for buyers. This precipitated fairly a stir amongst MSCI buyers, sending the inventory down greater than 25% in a day. Not solely did MSCI lose $24M of income from an essential buyer, it appeared just like the moat had been breached.

Given this piece of knowledge, a twentyfold rally over the subsequent decade could be extremely sudden, however that is precisely what occurred. There’s an fascinating dialogue available across the grey space of aggressive benefit. Whereas solely 5 firms command a majority of the market share, we see from historical past that they’re comparatively interchangeable.

MSCI’s moat is not a lot of a moat in any respect, it is model recognition and relationships. That is the place most companies of all sizes and styles really win. It’s extremely uncommon to seek out companies which have some sort of regulatory benefit that indefinitely stifles competitors, or have constructed some asset that’s inconceivable to duplicate. However these companies do exist within the public markets and have a lot stronger moats than MSCI. MSCI has executed flawlessly over the previous decade, a requirement to proceed to aggressively compound the inventory given the marginal aggressive benefits.

Capital Allocation & Valuation:

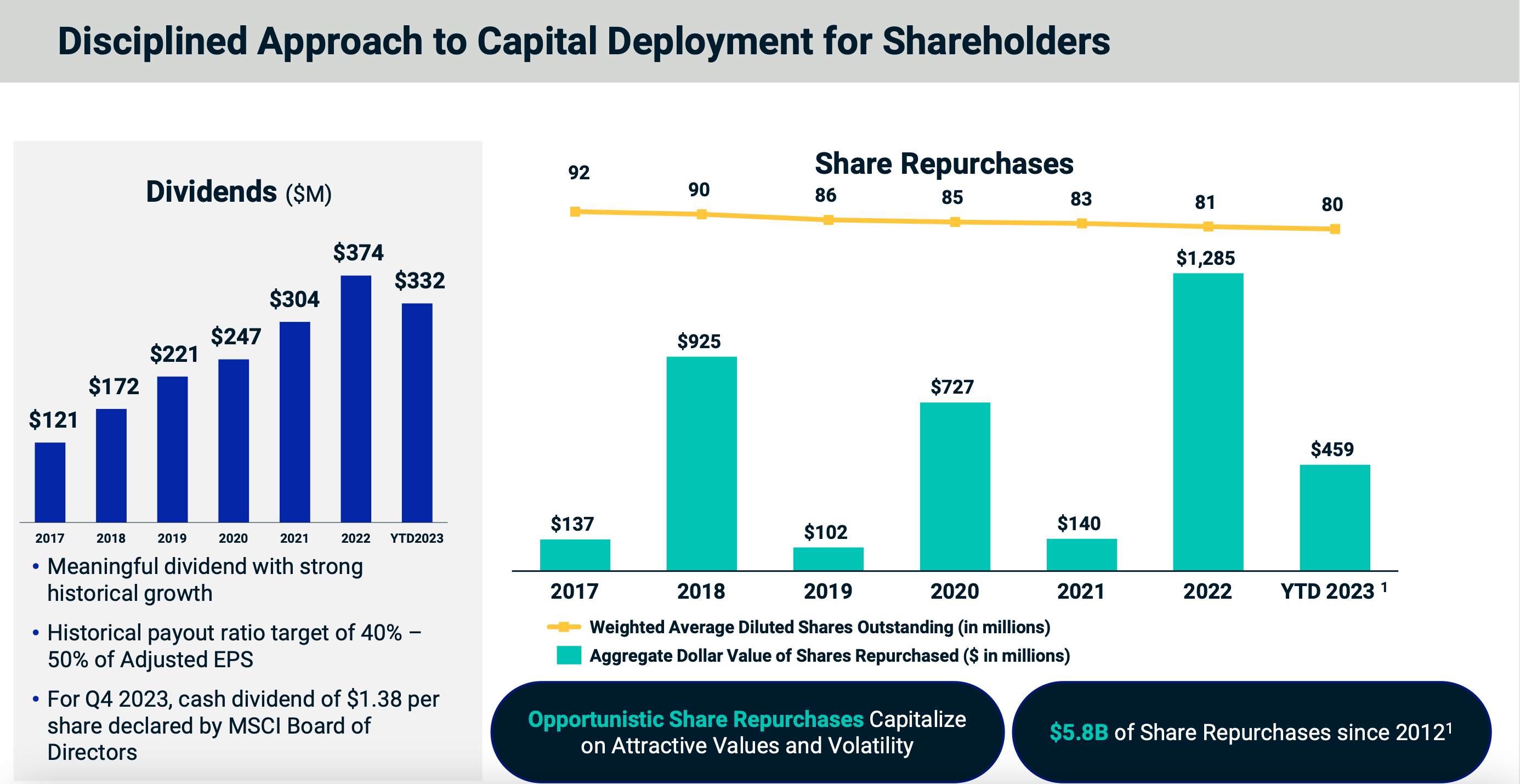

MSCI has proven its prowess when investing in its personal enterprise, MSCI has additionally proven quite a lot of shareholder friendliness when returning capital to shareholders:

MSCI Investor Presentation

There’s at all times an incredible debate about whether or not dividends or buybacks are extra worthwhile to shareholders. The reply largely will depend on how disciplined administration is, as buybacks might be roughly accretive than dividends relying on the costs they’re executed. As proven, MSCI has been extraordinarily considerate when deploying buybacks. One other feather within the cap of an incredible administration crew.

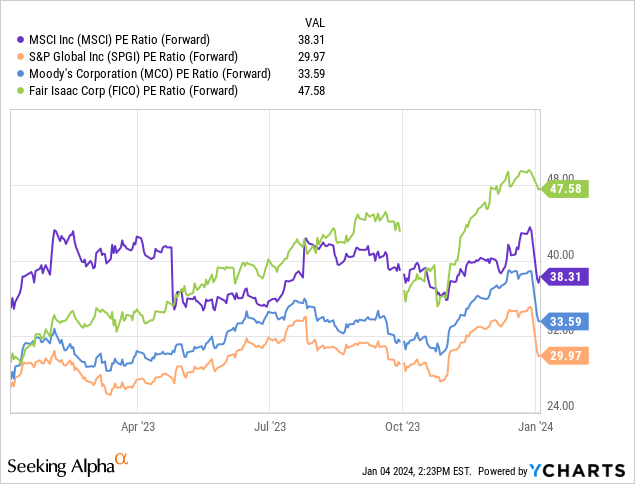

MSCI trades at round 38x subsequent 12 months’s ahead earnings estimates, which is effectively above the market a number of, and fairly above its closest friends:

MSCI has set a gold customary, not solely in benchmarks however in administration competency. However sadly, that is effectively understood by the market contemplating the premium valuation.

Even with the anticipated double-digit development charges for the foreseeable future, MSCI’s inventory seems fairly costly. Whether or not or not MSCI is a purchase relies upon solely on what buyers assume the long run a number of might be. In cases like this, it is doubtless macro, rates of interest, and hypothesis would be the largest driver of the share worth. It is troublesome for fundamental-based buyers to make a stand when multiples get stretched. MSCI could be a fringe purchase, however within the present higher-rate surroundings, it is doubtless buyers will see higher alternatives.