Nikada

Morgan Stanley Direct Lending Fund (NYSE:MSDL) is a BDC that was launched in January this 12 months and has already registered ~370 foundation factors of whole returns above the index. Additionally, from the NAV perspective, it falls within the Prime 10 record of largest BDCs, which makes MSDL a notable participant within the BDC area.

Trying on the Worth to NAV metric, we are able to see that regardless of the current inception date and no clear historic monitor document as a publicly traded BDC, MSDL already trades a slight premium (~7% over NAV, whereas the sector average stands at 0.97x).

It’s clear that the rationale why MSDL has tapped into the fairness market is due to fairly favorable circumstances each on the firm and sector ranges. The underlying fundamentals are robust (as elaborated under) and the BDCs basically are at present experiencing good tailwinds from greater SOFR and comparatively constrained banking exercise.

The query is whether or not the premium is justified and whether or not MSDL is positioned to maintain and even enhance its efficiency going ahead.

Thesis

The general technique of MSDL is reasonably typical, the place the first focus is on senior secured credit score investments in U.S. middle-market firms which have already established main market positions and generate robust money flows. The investments are made largely in companies which are backed by main PE homes (i.e., sponsor-backed transactions). Within the context of MSDL’s funding technique, it’s price mentioning that there’s an extra layer of security stemming from bias into non-cyclical industries.

Whereas all of those factors are fairly widespread within the BDC sector, we may think about the non-cyclical tilt as slight differentiator that definitely contributes effectively to the thesis right here.

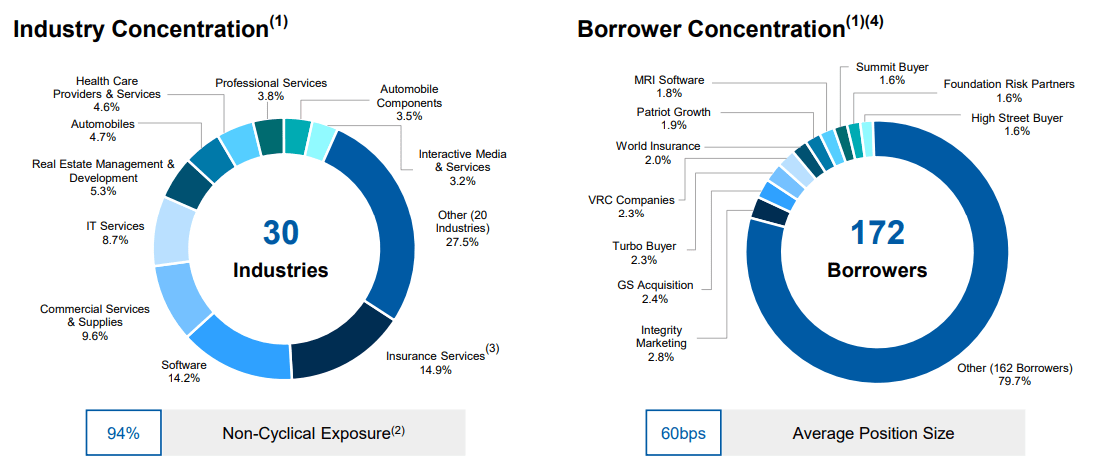

On the portfolio degree, MSDL appears to be like engaging because it has managed to significantly diversify the exposures amongst completely different industries and greater than 170 debtors. Word that roughly 95% of the sectors are deemed non-cyclical, indicating that the lion’s share of MSDL’s money flows (a minimum of top-line degree) are extra secure and predictable than for any common BDC on the market.

MSDL 4Q23 Earnings Presentation

On high of the robust diversification and publicity to defensive companies, virtually all the base of belongings is positioned in senior first-lien floating buildings, thereby rendering the portfolio much more strong.

On account of the aforementioned parts of protection (i.e., first lien, non-cyclical publicity, and diversification), MSDL has managed to maintain its portfolio very wholesome, recognizing virtually no non-accrual positions over the previous couple of quarters.

MSDL 4Q23 Earnings Presentation

Actually, as of year-end 2023, many of the investments have been categorized within the well-performing phase that’s in keeping with the dynamics ranging from Q2, 2023. Furthermore, throughout This fall, 2023 MSDL didn’t document any notable positions in threat ranking 4 territory, which is considerably reverse to what we may discover amongst many different BDCs (i.e., indicators of rising non-accruals of their This fall, 2023 outcomes). MSDL ended 12 months with solely three investments on non-accrual standing accounting for ~ $19 million or 0.6% of the portfolio at price. That is an insignificant quantity.

Closing factor that’s price highlighting about MSDL’s portfolio is the important thing monetary statistics of the underlying investments. Particularly, on the finish of the This fall, 2023, MSDL’s weighted common LTV of its investments stood at 43% with the median LTM EBITDA technology of $80 million.

Now, if we fuse the next gadgets collectively, I feel it could be honest to say that the present premium of ~7% over NAV is justified:

- Circa 94% of the portfolio is in non-cyclical and already cash-generating companies.

- Virtually 100% of the portfolio is in senior first lien buildings.

- Robust diversification at each sector and firm degree.

- Properly-performing companies as implied from the superb threat ranking desk, immaterial non-accruals and sound LTV metric.

Other than the abovementioned traits, there are two further elements, which I like about MSDL.

First, the leverage is under common and the construction of borrowings is favorable. As of now, MSDL carries a debt to fairness ratio of 0.87x, which is by 0.32x under sector common and, on an absolute degree, gives a strong foundation from which to both capitalize on the incremental alternatives or play defence in case the sector-level dynamics deteriorate.

As well as, the borrowings profile embodies some nice parts that ought to assist MSDL safeguard its margins for fairly a while.

MSDL 4Q23 Earnings Presentation

Particularly, roughly 40% of the excellent principal is predicated on mounted fee financing, the place the price of debt is decrease than what could possibly be accessed out there at present. This creates favorable circumstances for MSDL to extract attractive spreads between portfolio yield and price of capital. Plus, the primary maturity is about to kick in solely in September 2025. Adjusted for this, the extra engaging one, which can be a bigger ticket measurement financing comes due in early 2027.

Second, we’ve got to understand the good thing about MSDL’s ties with the Morgan Stanley franchise. In my view, the important thing benefit of that is the entry to bigger funding volumes from which MSDL may cherry decide the fitting investments.

Jeff Levin – President and Chief Government Officer – captured this essence properly throughout probably the most recent earnings call:

To start Morgan Stanley Direct Lending Fund’s sourcing platform is comprised of our captive devoted funding crew, Morgan Stanley’s funding financial institution and the non-public market options crew inside our funding administration platform that makes LP commitments to center market buyout funds. This strategy permits us to persistently consider vital deal circulate, and in flip be extra selective with investments. Morgan Stanley funding administration has roughly $1.5 trillion of belongings below administration with a deep historical past in alternate options.

The figures – indicating consistency in optimistic web funding volumes – function a proof of MSDL’s capacity to synergize with the Morgan Stanley franchise.

MSDL 4Q23 Earnings Presentation

In the course of the previous couple of quarters, many BDCs have struggled to develop the asset base and in a number of situations, the portfolios have decreased resulting from a scarcity of enough funding volumes that would offset the repayments of beforehand made investments. To navigate such an surroundings of comparatively depressed funding exercise (weak M&A and capital markets transactions), gaining access to Morgan Stanley comes with a major benefit. There’s a profit each on the quantity and deal high quality aspect.

The underside line

All in all, Morgan Stanley Direct Lending Fund is a transparent purchase. The present premium of ~7% is, in my view, totally justified by the defensive portfolio, which is additional backed by under common exterior leverage ranges and entry to Morgan Stanley’s broader transaction platform.

The ahead yield, assuming common dividend per share of $2.00 (which is in keeping with the historic quarters) and excluding particular dividends, lands at a lovely 9.2% degree. Given the robust adjusted NII technology, I might not be shocked of further particular dividends, the place if we think about the newest particular distributions, the ahead yield goes as much as 11.1%.

When it comes to the dangers, I don’t see any alerts or indicators within the underlying fundamentals that would set off MSDL underperforming the general BDC market. The component of diversification, non-cyclical publicity, low LTV ranges and de-risked steadiness sheet at MSDL degree ought to maintain the efficiency secure going ahead. Lastly, the power to supply offers from the Morgan Stanley platform ought to assist defend the present portfolio base even when the M&A and/or capital markets transactions stay muted.

It’s a purchase.