Fabian Gysel

MTU Aero Engines (OTCPK:MTUAF, OTCPK:MTUAY) suffered a setback following the metallic powder points with the Pratt & Whitney GTF. As a threat sharing accomplice, a part of the fee burden is carried by MTU Aero Engines, which has affected the corporate’s monetary leads to 2023 and could have money impacts going ahead. Nevertheless, as I talk about on this report the adjusted figures are trying promising and because the GTF affect is progressively being acknowledged within the money circulation efficiency, we should always see the underlying efficiency radiate as soon as once more. Primarily based on this, I can be re-assessing my inventory worth targets and score for MTU Aero Engines.

MTU Aero Engines Buyers Have been Given An Engaging Entry Level

Looking for Alpha

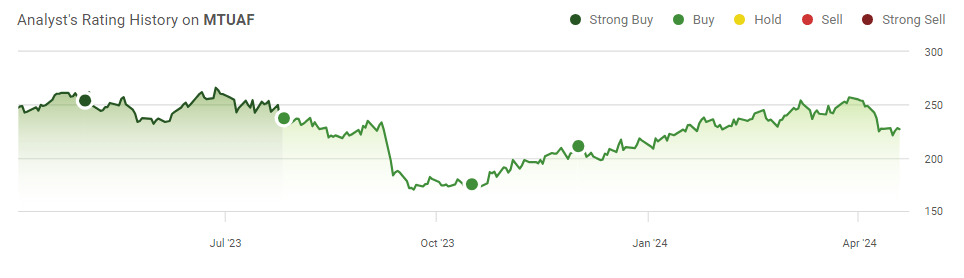

The snapshot above exhibits my score historical past on MTU Aero Engines, and it suffices to say that my first two rankings over the previous twelve months haven’t fairly labored out as anticipated because of the GTF engine points. Nevertheless, the buy rating for MTU Aero Engines in October 2023 has confirmed to be a really rewarding entry level because the inventory rebounded 28% in comparison with a 15% return for the S&P 500. Not all corporations with a crushed down inventory worth present continued compelling funding alternatives, however it appears that evidently MTU Aero Engines was not in that group.

MTU Aero Engines Adjusted Earnings Present Robust Development

MTU Aero Engines

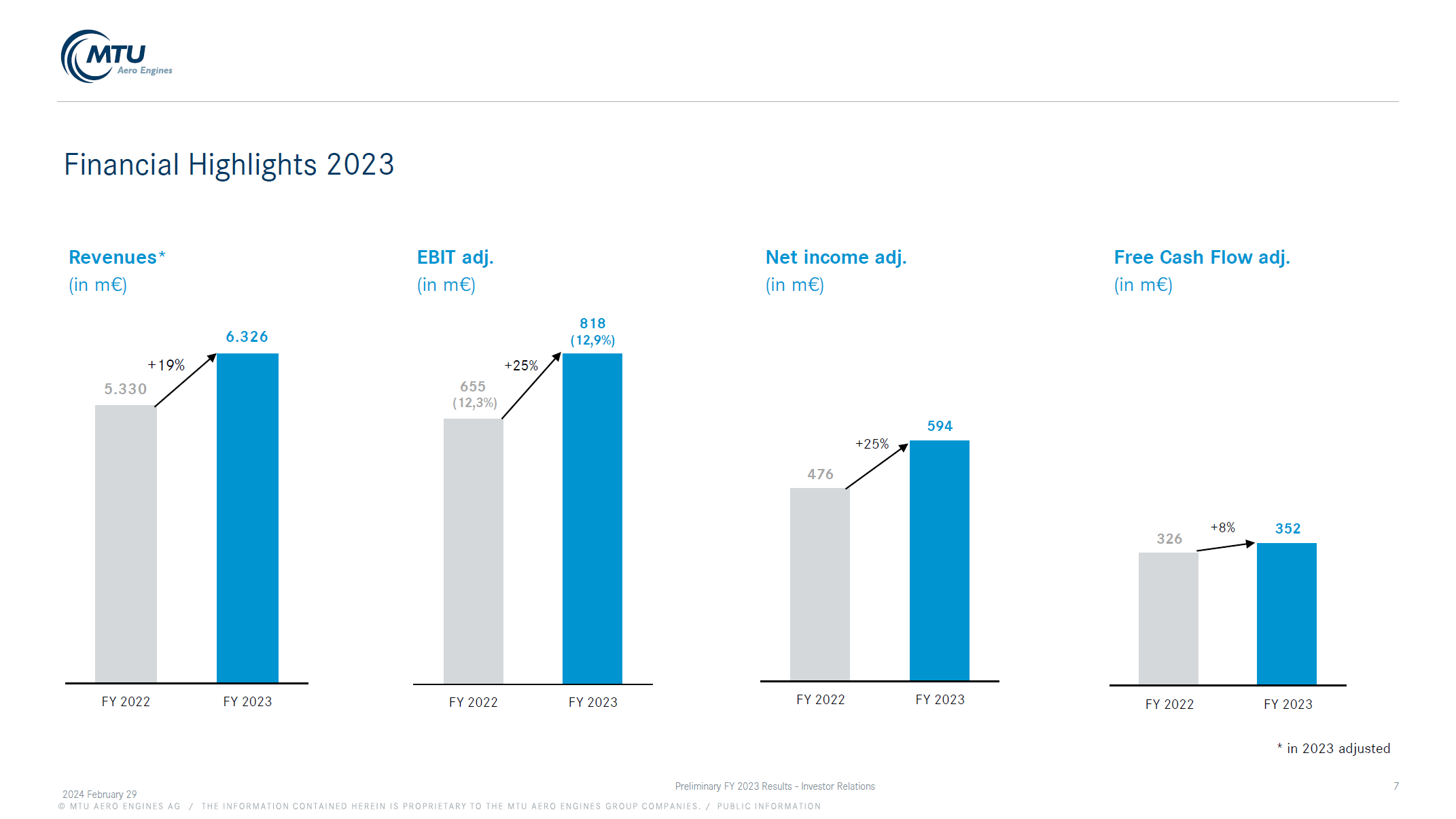

Adjusted revenues for 2023 confirmed 19% development to €6.3 billion, excluding the €956 million revenue impact recognized earlier. Equally, EBIT adjusted grew 25% to €818 million. The adjusted margin growth was primarily pushed by a decrease share of the GTF within the combine, which offers a tailwind to margins. Free money circulation grew 8% however fell in need of the EBIT and income development pushed by greater taxes, partially offset by decrease modifications in working capital.

The OEM section noticed its revenues develop 21% with navy revenues up 8% and industrial revenues rising 25% contributing to a 26% development in EBIT with the enterprise combine driving the margins barely greater from 21.1% to 22.1%. Business MRO revenues grew 17% with EBIT adjusted rising 23% with margin growth from 7.4% to 7.8%. Drivers of the EBIT margin had been a decrease share of GTF, which has decrease margins, a robust enterprise combine in any other case and optimistic contributions from fairness corporations.

So, on adjusted foundation, we do see very sturdy outcomes each by way of revenues and earnings. Free money circulation efficiency trailed considerably because of greater taxes paid throughout the 12 months. General, the underlying enterprise (which means excluding GTF affect) is performing effectively and that gives shiny prospects for the longer term.

MTU Aero Engines

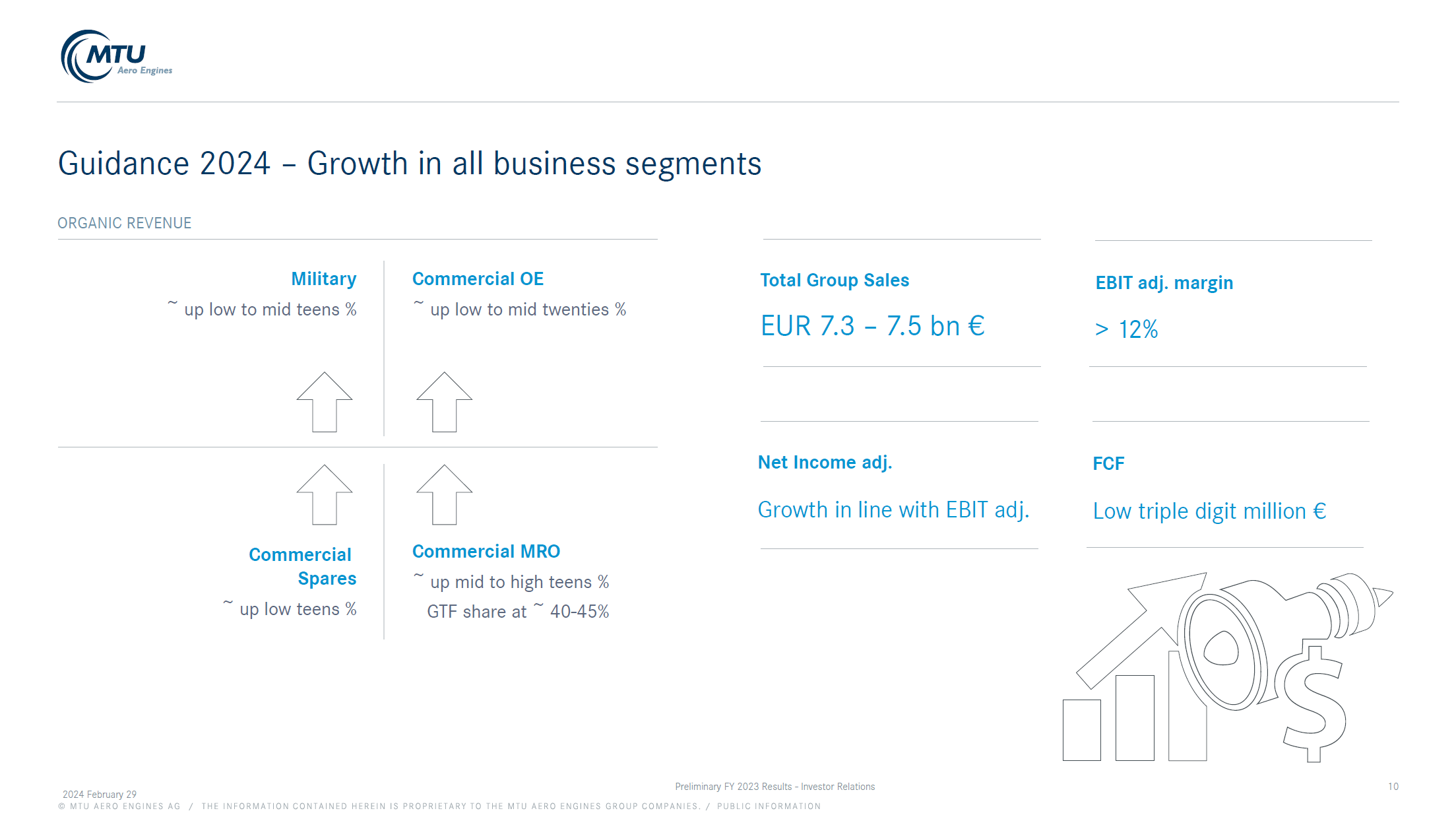

For 2024, MTU Aero Engines is guiding for natural income development to be as much as low mid-teens for Army, pointing at an acceleration in income development pushed by deliveries and extra income acknowledged from the Future Fight System. Business OEM gross sales are anticipated to be up low to mid-twenties pushed by greater manufacturing charges on the Airbus A320neo, Airbus A229, Embraer E-Jets and Boeing 787 with the GE9X powering the Boeing 777X additionally including to gross sales. Spare half gross sales are anticipated to be up low teenagers, pushed by utilization of legacy engine platforms and continued checklist worth will increase for stated engines. Business MRO revenues are anticipated to be up mid to excessive teenagers, with the next share for the GTF at 40 to 45 %.

This could deliver the Group Gross sales to €7.3 billion to €7.5 billion, offering over 18.5% development in revenues. Adjusted EBIT margins of >12% level at a minimal of seven to 10 % development. The free money circulation steering of low journey digit million is considerably imprecise, however I’d say that is totally comprehensible given the timing of buyer credit that MTU Aero Engines as a shareholder of Worldwide Aero Engines will grant to airline clients. A recent example is the compensation agreed on with Spirit Airlines (SAVE). The timing of the compensation isn’t totally sure as some may be in 2024 and a few would possibly find yourself in 2025 or there truly may be an acceleration inflicting a front-loaded money outflow. Both means, from money circulation efficiency, I do count on a pressured 12 months as buyer compensations are being rendered.

MTU Aero Engines Is Not To Blame For GTF Engine Disaster

As I’ve been protecting MTU Aero Engines for some time, one returning remark that I’ve obtained from readers is that MTU Aero Engines was answerable for the metallic powder concern. I have no idea the place this hearsay got here from, however it is very important bear in mind that this isn’t the case and MTU Aero Engines additionally confirmed this:

As beforehand stated, I want to emphasize that MTU isn’t a part of the issue, however we’re a part of the answer. We’re working very carefully with Pratt & Whitney to handle the plan in the very best means as we’re assessing choices tips on how to enhance MRO capability and to develop clever and good options to handle store visits and optimize workshops. The defining issue for this system stays the power to hurry up turnaround time and to make sure functionality of change elements.

As a threat sharing accomplice, MTU Aero Engines may not have induced the issue however is obliged to supply buyer credit. I believe it is extremely vital for those who assume that MTU Aero Engines induced the metallic powder concern to be effectively conscious of this and be told that MTU Aero Engines is definitely not the reason for the issue with the GTF. MTU Aero Engines has stated it will not sue Pratt & Whitney, however that doesn’t imply that MTU Aero Engines is not going to obtain any compensation from Pratt & Whitney in any respect as talks concerning compensation proceed.

MTU Aero Engines Inventory Stays Engaging

The Aerospace Discussion board

MTU Aero Engines had sturdy earnings in 2023 on an adjusted foundation, and its earnings within the years to come back are seemingly reflective of sturdy demand for air journey in addition to an uptick in navy enterprise revenues. Nevertheless, its free money circulation can be subdued pushed by the GTF engine points and because of this, the corporate has lowered its dividend from €3.20 beforehand to €2.00. I imagine that may be a prudent choice given the extra money outflows, and it offers MTU Aero Engines with a dividend foundation from which it may return worth to shareholders once more as soon as free money circulation begins to return to development.

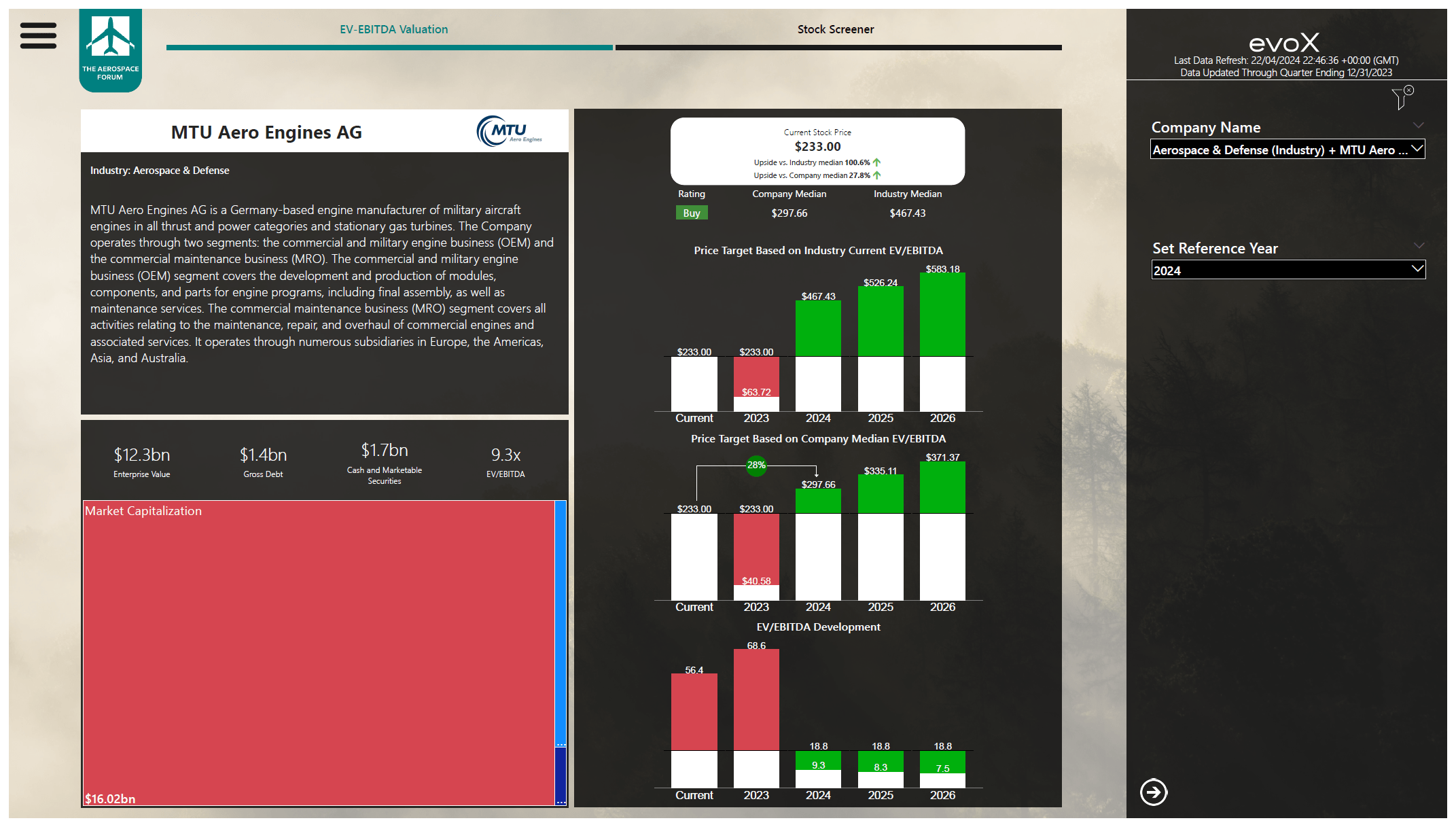

After processing the stability sheet information and ahead projections, I imagine that MTU Aero Engines stays engaging, with a $298 worth goal offering 28% upside.

Conclusion: MTU Aero Engines Navigates Pressures Effectively

MTU Aero Engines is seeing sturdy underlying efficiency and that’s unlikely to alter any time quickly as demand for turbofans stays excessive whereas navy initiatives are additionally about to speed up income technology. Within the coming years, free money circulation can be pressured because of buyer credit that MTU Aero Engines has to supply to operators of the troubled GTF engine. Nevertheless, even in that situation, I imagine that the funding case for MTU Aero Engines stays engaging for the close to time period in addition to the long term and that’s with out accounting for any compensation the corporate might finally get from RTX Company (RTX), which is the corporate’s program accomplice. Moreover, the corporate sees development alternatives as a number of industrial manufacturing applications go up in manufacturing charge and the engine enterprise stays one that’s laborious to penetrate for brand new gamers. Because of this, I do imagine that whereas the GTF points present a money drag on MTU Aero Engines, there may be enough enchantment to put money into the corporate.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a serious U.S. change. Please concentrate on the dangers related to these shares.