Vladyslav Otsiatsia

In a previous report, I analyzed the gross sales and revenue fees that RTX Company (RTX) acknowledged within the third quarter, and people gross sales and revenue fees have been in keeping with expectations. RTX just isn’t the one firm that’s feeling the ache of the Pratt & Whitney GTF challenge. Airways are clearly additionally feeling the ache of it, however within the provide chain and amongst risk-sharing companions there is also price progress. MTU Aero Engines AG (OTCPK:MTUAF) is such a associate. In October, I already had a first look on the monetary penalties for MTU Aero Engines and concluded that there possible can be a $900 million to $1.26 billion impression.

Within the firm’s third-quarter replace, we’ve been given extra particulars on the prices, which I’ll talk about on this report accompanied by a dialogue of the third quarter adjusted outcomes to see how the underlying enterprise excluding the GTF challenge is performing. I can even present an up to date worth goal for MTUAF inventory, on condition that the inventory has gained 13% since I maintained my purchase ranking in October.

MTU Aero Engines Suffers The Ache Of GTF Engine Issues

MTU Aero Engines

I’m not going to rehash the complete story of the Pratt & Whitney PW1000G steel powder challenge, however do need to check out the prices that MTU Aero Engine may have as a risk-sharing associate. MTU Aero Engines has acknowledged $961 million in buyer assist prices and $69 million in extra MRO-efforts for a complete of $1.03 billion which hit the EBIT line and $1.013 hitting the highest line with extra MRO efforts of $200 million that can be acknowledged over time. So, the earlier estimate vary of $900 million to $1.26 billion precisely captures the acknowledged fees within the third quarter and even captures the follow-up MRO-efforts.

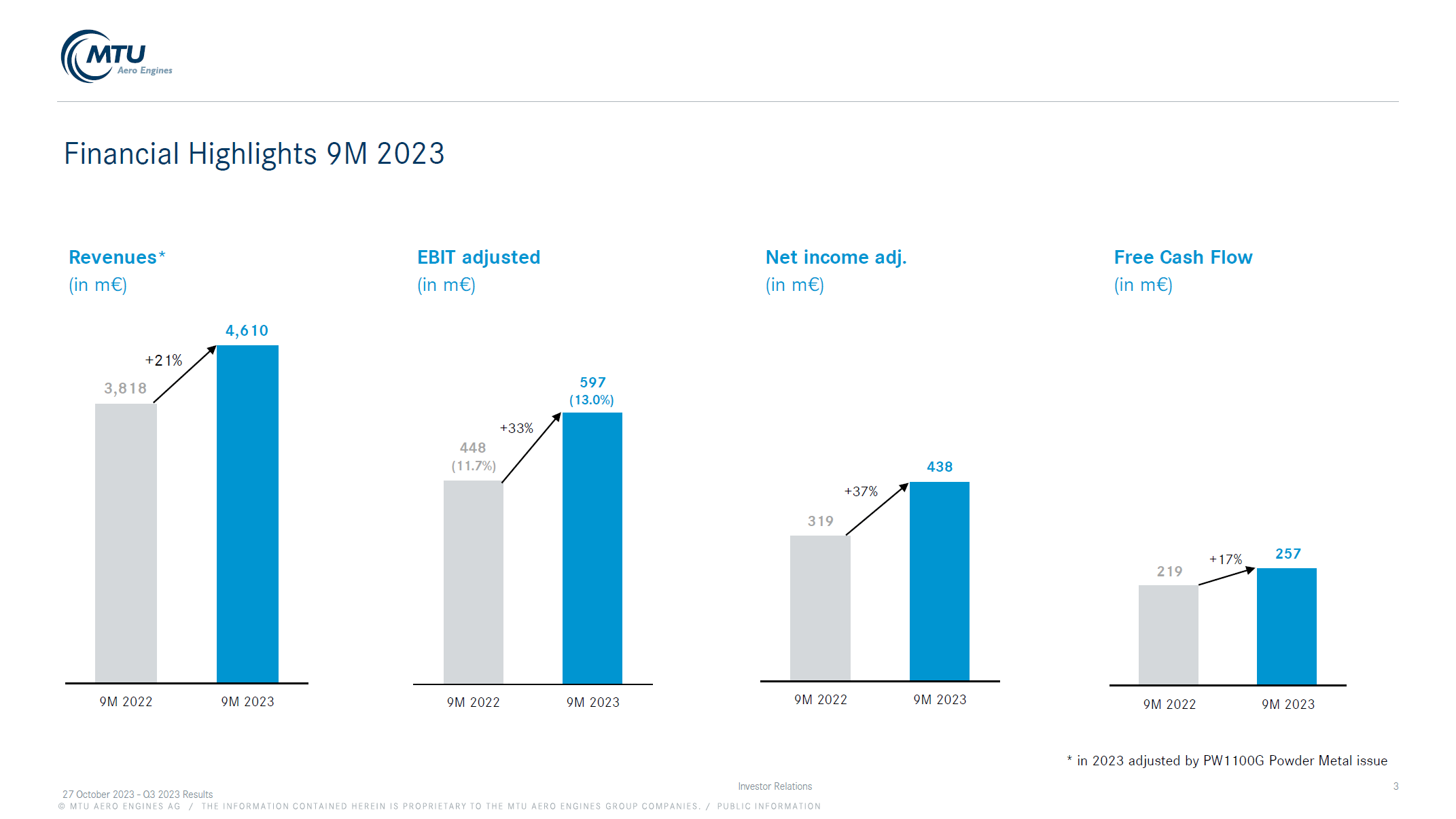

Robust Adjusted Earnings For MTU Aero Engines

MTU Aero Engines

The adjusted earnings are usually not used as a result of we’re blind to the truth of the GTF price progress in the course of the quarter, however as a result of the adjusted earnings and revenues present a greater overview of undisturbed efficiency. Adjusted revenues grew 21% whereas adjusted EBIT and web earnings grew 33% to 37%. Whereas earnings outpaced income progress, free money move producing was solely 17% greater, however this may be pushed by a backloaded free money move profile that we normally see. MRO (Upkeep, Restore & Overhaul) which accounts for two-thirds of the income stream noticed 18% progress with slight combine stress bringing the adjusted EBIT margin to 7.2% from 7.4% in 9M 2022. Revenues within the OEM section have been up 26% with 19% progress within the army enterprise and 29% progress within the industrial enterprise.

What I discovered fascinating is that the army enterprise noticed important progress. In lots of aerospace firms, we see the army enterprise lagging a bit, however at MTU Aero Engines that isn’t the case. Margins improved to 23.6% from 20% a 12 months in the past on robust combine, income progress, and comparatively low prices for the 9 months in 2023.

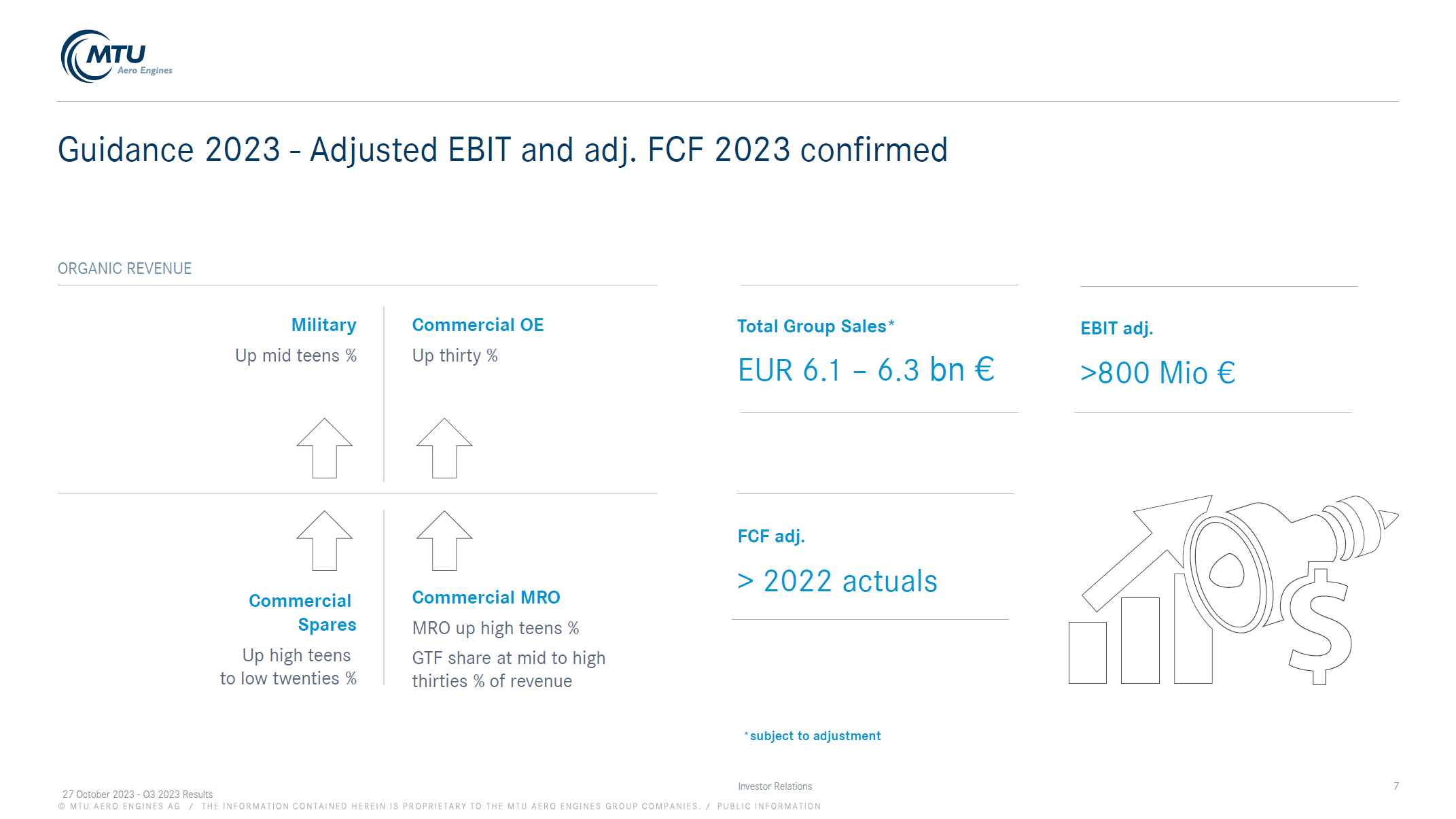

MTU Aero Engines Confirms Steerage

MTU Aero Engines

MTU Aero Engines stored its guidance constant with >€800 million in adjusted EBIT on €6.1 billion to €6.3 billion in revenues, indicating >13% margins. MTU expects revenues to be on the greater finish of the guided vary, with FCF and EBIT barely above the minimal values guided. The steerage being maintained to me is a sign of energy that appreciates the enterprise subsequent to the realities of the problems with the Pratt & Whitney PW1000G.

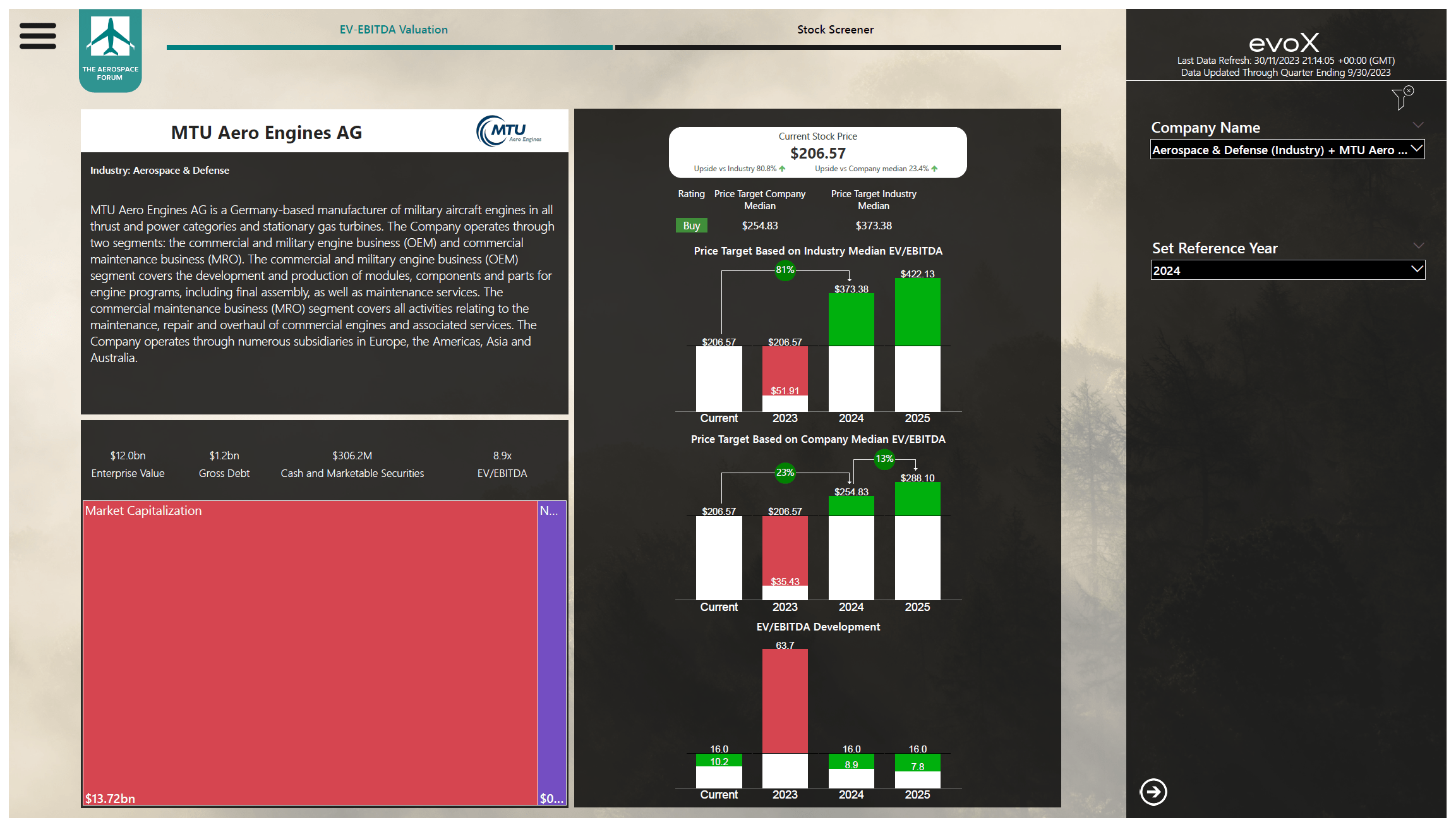

The Aerospace Discussion board

The impression the price recognition had on 2023 valuation is relatively clear, with no upside for MTU Aero Engines. On the identical time, I might not wish to concentrate on 2023 because the hit is acknowledged in 2023, however the precise impression will largely be felt within the years after with a money move hit of lots of of thousands and thousands of {dollars} that MTU Aero Engines will attempt to recoup from RTX. If profitable, that would offer a lift to the corporate’s valuation and unlock upside. Even after we don’t issue within the restoration of those money flows, I really feel comfy assigning a purchase ranking with a $255 worth goal, representing a 23% upside.

Conclusion: MTU Aero Engines Has Upside Regardless of The GTF Value Affect

In the event you’re an investor for present 12 months earnings, MTU Aero Engines just isn’t the identify you’ll wish to be invested in, however that might be the case for a lot of aerospace firms. 2023 provides little to no worth on an unadjusted foundation, as MTU is struggling the implications of being a risk-sharing associate. Nevertheless, within the years after, we see that there’s important upside from present ranges and that’s even after we contemplate a free money move hit of round $500 million from 2023 by 2025.

I wouldn’t say the GTF debacle is within the rearview mirror for the reason that price has been recognizing, however many of the work and related money burn will happen in 2024 and 2025. Nevertheless, MTU Aero Engines nonetheless rides the long-term demand pattern, and we’re already seeing how it’s seeing important progress in OEM gross sales in addition to MRO. The GTF points present a sizeable headwind to earnings, however even with related pressures current, I do see a major upside forward within the years to come back. Because of this, I keep my purchase ranking for MTU Aero Engines inventory.

Editor’s Word: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please concentrate on the dangers related to these shares.