Andrii Dodonov

By Matthew Norton & Daryl Clements

With high yields and compelling opportunities, we think the muni market looks exceptionally attractive today.

After a bumpy first half of 2024, the municipal bond market is starting to enjoy favorable tailwinds. In fact, from supportive “summer technicals” to high municipal bond yields and compelling credit opportunities, current conditions point to a strong second half of the year. For muni investors who have been waiting for the right time to return to the market, we think this is the time to end the waiting game and jump back in.

Muni Investors Shouldn’t Wait for Rate Cuts

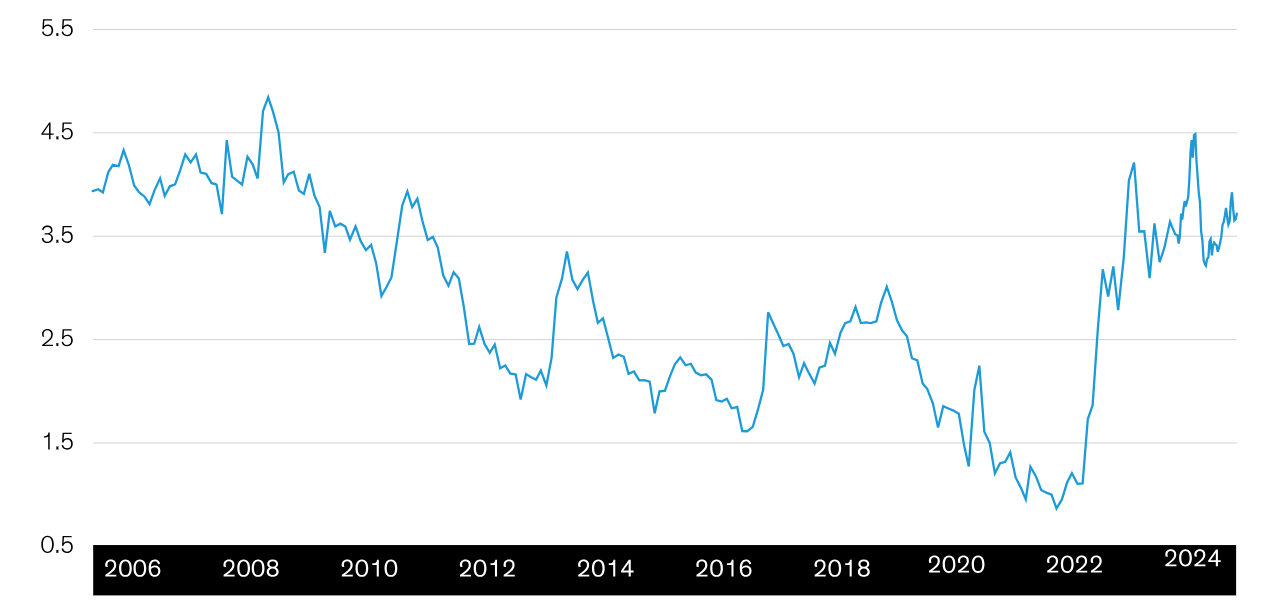

Municipal bond yields are among the highest levels they’ve been since 2011 (Display) and currently offer a 6.3% tax-equivalent yield, based on the top federal tax bracket. The Federal Reserve’s decision to delay rate cuts – likely until December, in our view – should keep yields (and income) elevated for some time.

Municipal Bond Yields Remain Compelling

Bloomberg Municipal Bond Index: Yield to Worst (Percent)

Historical and current analyses do not guarantee future results. Through June 28, 2024 (Source: Bloomberg and AllianceBernstein (AB))

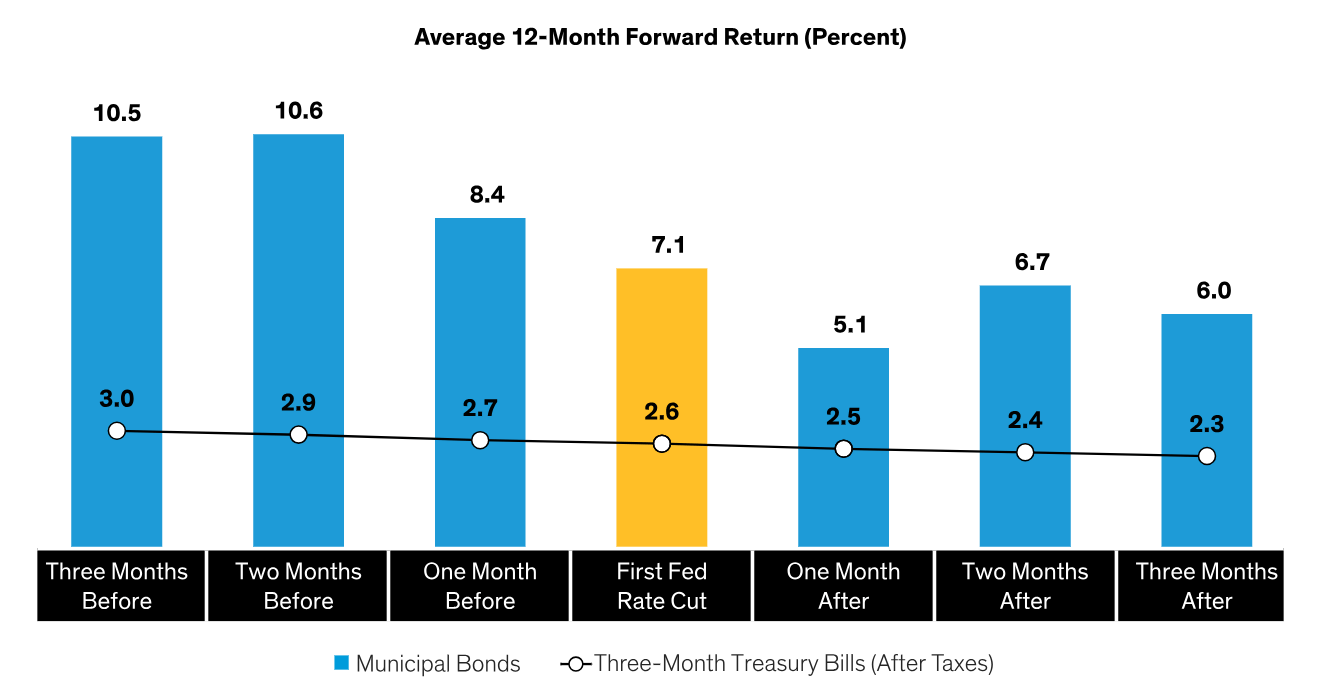

But central bank rate cuts will come eventually, and it’s generally better to already be invested when they do since bond prices rise when bond yields fall. In fact, waiting too long to invest can be a costly mistake. That’s because those who invested before rate cuts began enjoyed the strongest returns historically (Display).

Historically, Early Birds Enjoyed Stronger Muni Returns

Historical analysis and forecasts do not guarantee future results. Returns based on Fed easing cycles whose first cuts occurred on the following dates: September 20, 1984; June 7, 1989; July 6, 1995; January 3, 2001; September 18, 2007; and August 1, 2019. Assumes a 40.8% tax rate. Muni bonds represented by the Bloomberg US Municipal Bond Index; three-month Treasury bills represented by Bloomberg US Treasury 1-3 Year Total Return Index. As of December 31, 2023 (Source: Bloomberg, US Federal Reserve and AB)

What’s more, the recurring phenomenon known as “summer technicals” should help support muni prices over the next couple of months. More bonds mature in June, July and August than in the rest of the year; combined with calls and coupon payments, these maturities create a seasonal tidal wave of income that needs to be reinvested. This year, that wave is expected to be around $46 billion. When that much money is looking for bonds to buy, it can lift bond prices.

We think such conditions provide one of the best entry points for muni investing in years. Environments this compelling are infrequent and usually fleeting. For example, in November and December 2023, when yields began to reverse direction in anticipation of a Fed rate cut, the Bloomberg Municipal Bond Index returned 8.7%.

Unique to today’s scenario is a record $6.5 trillion sitting idle in money market funds. The first Fed rate cut is all it should take for investors to start moving off the sidelines – even more reason to get back in now, in our view.

Muni Investing for Current Conditions

Here’s how muni investors can take advantage in today’s market:

Extend duration targets. Extending the portfolio’s duration, or sensitivity to changes in interest rates, takes advantage of falling yields when they occur. As the Fed’s first rate cut approaches, we think it’s far more likely that rates will decline than that rates will rise. And falling yields translate into rising bond prices – and into strong potential returns today, in our analysis.

We also think it’s not too early to act. Easing cycles tend to be much faster than hiking cycles. Investors who don’t want to miss out on the opportunity should consider adding duration exposure well before the Fed’s first rate cut.

Consider a barbell structure. Intermediate munis – those with five- to 15-year maturities – currently offer lower yields than shorter- and longer-term bonds. In this environment, a barbell maturity structure can capture high front- and back-end yields while avoiding the lower yields in the “belly” of the curve.

For example, a combined investment in a one-year and a 16-year AAA muni bond today would add 32 bps more yield compared to an eight-year bond, while providing the same average duration.

Own muni credit. Muni credits – those rated BBB, for instance – have meaningfully outperformed their higher-quality counterparts. Although credit spreads have tightened somewhat, we think valuations remain attractive.

Issuer fundamentals are also solid, with borrowers sitting on more cash as a percentage of expenses than ever, according to the National Association of State Budget Officers. Some state and local government revenues may fall short of budget expectations, but most are well-equipped with rainy day funds and other tools to navigate such gaps.

Rotate out of Treasuries. In early 2024, we found that Treasuries offered better value than munis, as measured by their relative after-tax yield advantage. However, this is no longer the case. As yields rose in the first half of the year, after-tax spreads on 10-year Treasuries rose from negative territory to 47 bps by the end of May. At that point, munis looked more attractive. Munis then outperformed Treasuries in June, and the after-tax spread narrowed to 27 bps.

While not quite as attractive as one month ago, those levels continue to suggest investors should rotate out of Treasuries in favor of munis. Above all, we think investors should pay attention to the after-tax relationship between munis and Treasuries and adopt a flexible approach that allows them to take advantage of frequent shifts in relative value.

While we wait for the Fed to act, we expect municipal market conditions to remain supportive, barring economic and other surprises. Yields remain high, valuations remain attractive, and a welcome summer technical is already supporting bond prices. Investors who stayed the course should be ready to lengthen duration and add to credit positions. For those still waiting on the sidelines, we see few obstacles standing in their way.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.