Jose Luis Pelaez Inc/DigitalVision via Getty Images

Myomo (NYSE:MYO) is a wearable medical robotics company designing, developing, and manufacturing myoelectric orthotics for people suffering from neurological disorders. Its brace is mainly used to offer expanded mobility for stroke survivor’s paralyzed arms.

All-time share performance has been disappointing so far. MYO went public in 2017 at $433 per share, but shares price continued to trend down in the next few years. Most recently, MYO is trading at $3.8 per share, losing almost all of its value since going public. Nonetheless, MYO has gained significant momentum over the past year, with the stock delivering a price return of over 700%. Yet, MYO is still down more than -20% YTD.

I rate MYO a buy. My 1-year price target of $4.42 per share projects about 16% upside. At this level, MYO presents an attractive buy opportunity. In my opinion, the company will continue to benefit from the recent policy changes by CMS, which has provided MYO with a TAM expansion catalyst.

Financial Reviews

ycharts

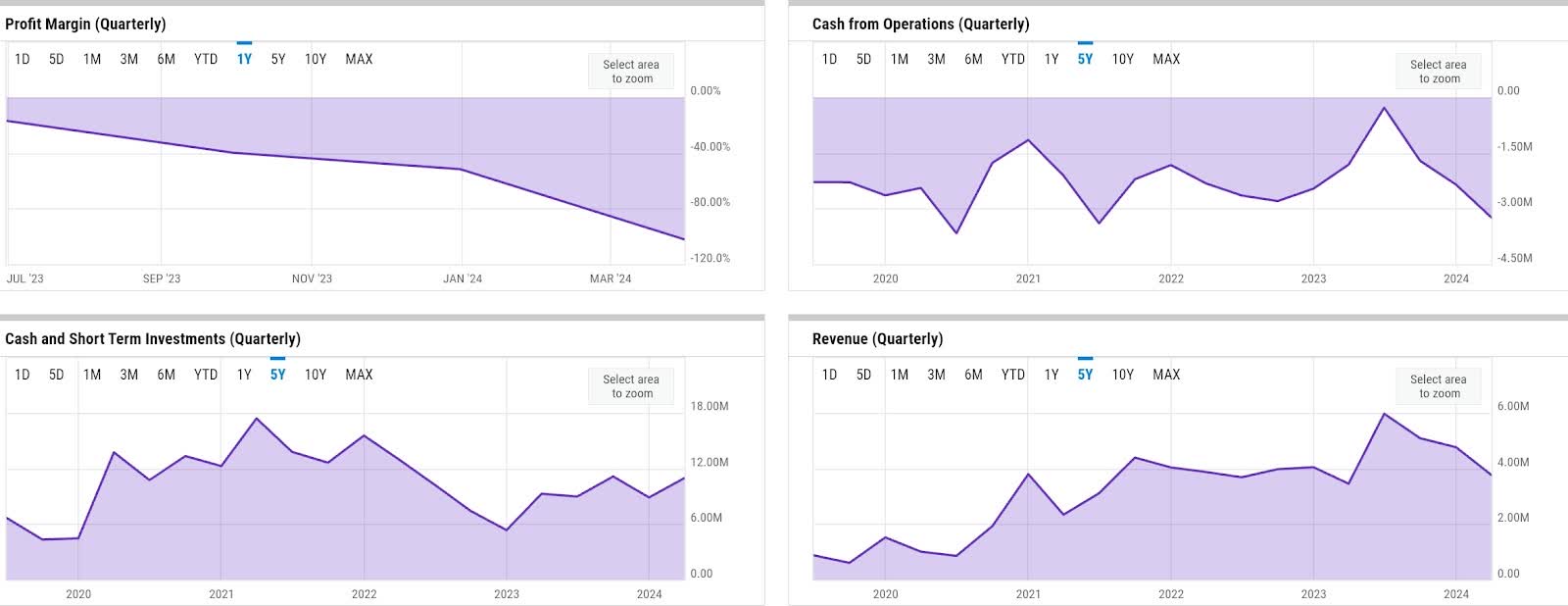

Fundamentals have been quite underwhelming. While revenue growth has normalized to about 20% as of the last FY, profitability and operating cash flow (OCF) generation have continued to weaken as of Q1. MYO saw just under 9% YoY top-line growth in Q1 with net loss margin widening to -102%. MYO also burned through over -$3.2 million of OCF, higher than the last few quarters.

In fact, MYO has never generated positive OCF in the last five years, and its main source for liquidity has been equity financing from common stock issuances. In Q1, MYO raised over $5.3 million from common stock issuance. While this has helped MYO maintain steady liquidity, dilution has also been quite pronounced within the same period. In Q1, MYO ended the quarter with almost $11 million of cash and short-term investments. However, shares outstanding was 36.75 million as of Q1, which represents an almost 5x dilution since the end of 2022 alone.

Catalyst

In FY 2024 and beyond, I believe MYO should continue to benefit from the recent policy changes by CMS (Center for Medicaid Services), which recategorize MYO’s main offering, MyoPro, into brace category, and also determine new pricing for the offering. As commented by the management in Q1 earnings call, I would expect this to be a major catalyst for MYO, since the new categorization will expand the number of patients who could access MYO’s offerings with the standard Part B Medicare:

These decisions by CMS opened a new world for stroke survivors and others with neurological injury or disease by increasing access to the MyoPro for the many patients enrolled in standard fee-for-service Medicare, or Part B. Prior to this clarity on reimbursement, we are not able to provide a MyoPro to traditional Medicare patients and approximately half of seniors in the United States are covered by standard Part B Medicare. Most of the others are enrolled in a Medicare Advantage plan where we’ve had mixed results with the payers.

Source: Q1 earnings call.

Moreover, the positive impact from the changes appears to have been felt by MYO in Q1, as demonstrated by the strong backlog, indicating future revenue growth. In Q1, the number of authorizations and orders were significantly up 48% YoY, driving the 56% YoY increase in backlog, which also included Part B patients.

Risk

Though the tailwinds here should be significant enough to drive MYO’s business, I consider execution risk to be the major risk factor for MYO. In particular, the risk lies in the clinical reimbursement and also manufacturing processes to capture the opportunities in the backlog. Meanwhile, backlog conversion remains the only driver to revenue generation.

Moreover, as the management has mentioned earlier in the earnings call, MYO has made significant investments as well to serve the growing demand, as highlighted by the additional hiring within the clinical reimbursement team which resulted in -44% increase in operating loss. As such, this may have raised market expectation of the stock, in my opinion, and may result in MYO’s share price seeing downward pressure on any news of execution-related issues.

Valuation / Pricing

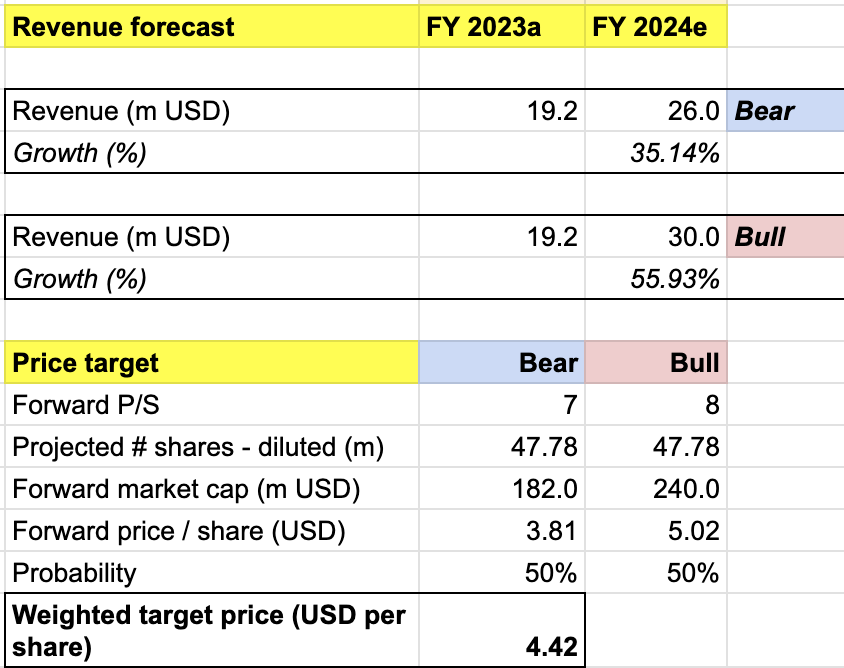

My target price for MYO is driven by the following assumptions for the bull vs bear scenarios of the FY 2024 projection:

-

Bull scenario (50% probability) assumptions – I expect revenue to grow by 56% YoY to $30 million, in line with the company’s guidance. I assume forward P/S to expand to 8x, implying a share price appreciation to $5 price level, as I expect strong market reaction once MYO is able to deliver revenue growth acceleration, driven by solid execution.

-

Bear scenario (50% probability) assumptions – MYO to deliver FY 2024 revenue of $26 million, a 35% YoY growth, which is $2 million lower than the company’s low-end target. Nonetheless, despite missing the target, a 35% growth is still a solid outlook for the company. As such, I would expect P/S to slightly expand to 7x, though the stock may still trade sideways into FY 2024.

own analysis

Consolidating all the information above into my model, I arrived at an FY 2024 weighted target price of $4.42 per share, a projected 1-year upside of about 16%. I would rate the stock a buy.

Overall, I believe the rebound opportunity in FY 2024, driven by the policy tailwinds, suggests that MYO could be an attractive buy today. My 50-50 bull-bear probability assignment remains conservative, especially with MYO having better revenue visibility today, as highlighted by its strong backlog. Furthermore, I also lowered my bear case revenue projection by $2 million, which was another conservative assumption.

In my opinion, an important thing to monitor by investors here would be share dilution, which is one of the key factors driving my price target. My price target model assumes a 30% share dilution in FY 2024. Though it seems a bit high, it is already a lower figure than the 50% dilution YTD. Based on my simulation, the price target will be much lower if MYO maintains the current level of dilution in FY 2024.

Conclusion

MYO is a company developing myoelectric orthotics mainly for the US market. The recent policy changes by the CMS that have put MYO’s solution in a category that is more accessible by Part B patients should present a TAM expansion opportunity for the company. Given the strong backlog, what is left to do would be executing strongly to convert it into revenues. MYO has indeed provided strong guidance in FY 2024. This may have been the reason why the stock has been up over 10% in the past month alone. My price target of $4.42 that implies 16% 1-year return, however, suggests that there is still upside to realize for the FY. I rate the stock a buy.