olrat/iStock through Getty Photographs

MYR Group Inc. (NASDAQ:MYRG) is a holding firm of main specialty contractors that service the electrical utility infrastructure, industrial and industrial development markets within the U.S. and Canada.

The corporate has two enterprise segments, a Transmission & Distribution section (“T&D”) and a Industrial & Industrial section (“C&I”).

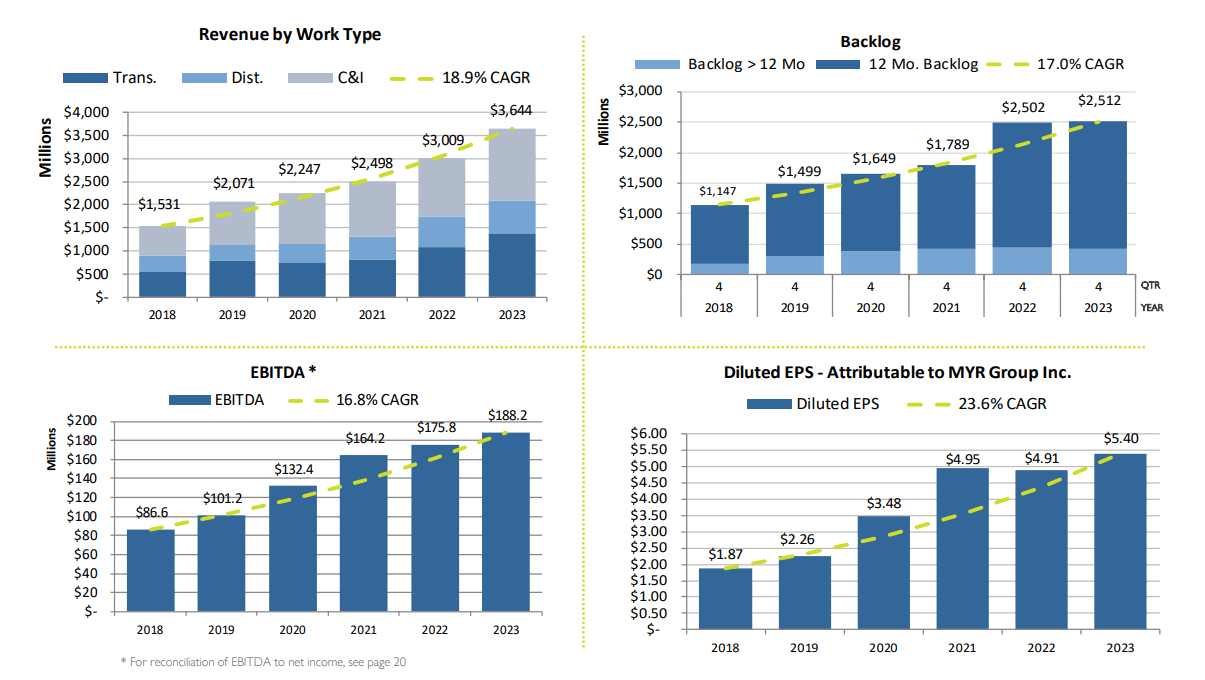

In 2023, MYR Group’s T&D section had full yr income of $2.09 billion and the C&I section had income of $1.55 billion.

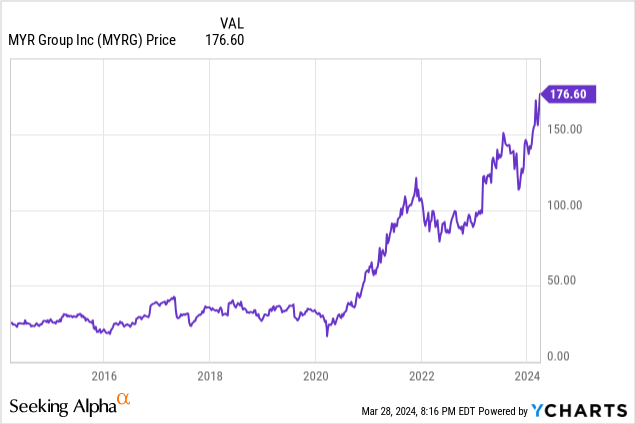

Since 2020, MYR Group’s inventory worth has carried out rather well, rising from round $32.43 at first of 2020 to round $176.60 as of March 28.

Since 2018, MYR Group’s financials have benefited from rising demand given tailwinds from the clear power transition, and rising funding in upgrading and bettering the electrical grid.

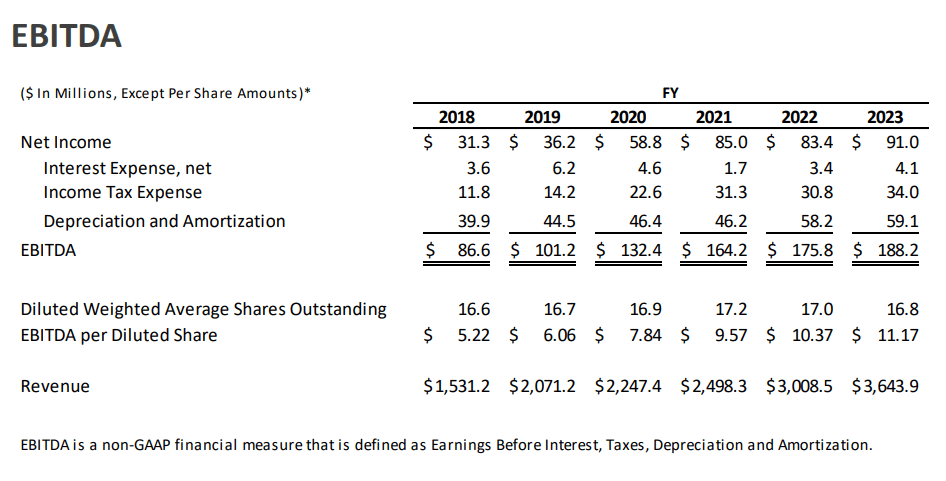

When it comes to financials, MYR Group’s diluted EPS has greater than doubled from $1.87 in 2018 to $5.40 in 2023. In the meantime, income, EBITDA, and the corporate’s backlog have elevated significantly since 2018 as properly.

MYR Group Investor Presentation

On February 28, 2024, MYR Group reported full yr 2023 outcomes that indicated substantial demand power and continued monetary progress.

2023

In 2023, MYR Group income rose 21.1% yr over yr to $3.64 billion.

Income within the T&D section rose 19.7% yr over yr to $2.09 billion given will increase in income on transmission tasks and distribution tasks. Gross sales in transmission tasks rose primarily associated to a rise in income on clear power tasks.

Income within the C&I section rose 23.1% yr over yr to $1.55 billion due to larger income associated to scrub power tasks in sure geographical areas.

Full yr EBITDA rose to $188.2 million in 2023 from $175.8 million in 2022.

MYR Group Investor Presentation

Web revenue for the yr rose to $91 million, or $5.40 per diluted share, from $83.4 million, or $4.91 per diluted share, for a similar interval of 2022.

MYR Group’s backlog additionally elevated marginally to $2.51 billion on the finish of 2023, up from $2.5 billion on the finish of 2022. T&D backlog was $959.6 million and C&I backlog was $1.55 billion on the finish of 2023.

Moreover, MYR Group maintained a powerful steadiness sheet with funded debt to LTM EBITDA leverage of 0.19x as of the tip of 2023. On the finish of the yr, MYR Group had $442 million of availability below its $490 million credit score facility, giving administration flexibility when it comes to capital allocation selections.

When it comes to M&A, MYR Group has had lots of organic growth lately and administration is prepared to be affected person when it comes to acquisition alternatives in consequence.

My takeaway is that 2023 was one other robust yr of monetary progress for MYR Group as demand continued to strengthen within the final a number of years.

Outlook

In terms of outlook for 2024, CEO Rick Swartz said the next through the This fall 2023 earnings name when requested about high line traits primarily based on the awards that the corporate has had,

I’d nonetheless take a look at the excessive single-digit progress for the yr, most likely just a little — weighted just a little extra heavy in the direction of the second half of the yr.

Swartz added,

And as we stated earlier than, this yr, we actually wish to give attention to although we do not thoughts rising our high line, and we nonetheless see it coming in, in form of that larger single-digit. We’re actually going to give attention to that backside line progress, and this all takes that into consideration. We wish to make it possible for the work we’re doing and we tackle is worthwhile going ahead.

My takeaway is that 2024 is likely to be a slower yr when it comes to high line progress than 2023 given demand will be lumpy sometimes. However, administration may be very constructive when it comes to the quantity of labor that is on the market and I believe MYR Group’s high and backside line will proceed to develop at a reasonably robust fee properly into the late 2020’s given how huge the demand tailwinds are.

Tailwinds

MYR Group advantages from rising electrical energy utilization and in addition the clear power transition.

Prior to now few many years, electrical energy utilization in the US and Canada has not elevated a lot attributable to rising power effectivity.

Based on the EIA, the truth is, complete U.S. electrical energy consumption rose solely 6.1% within the final 10 years from 3832 terawatt-hours in 2012 to 4067 terawatt-hours in 2022.

However that development would possibly change as electrical energy demand is predicted to extend from 2.6% to 4.7% in the US over the following 5 years, with doubtlessly $630 billion in close to time period funding required to fulfill load progress in accordance with the December 2023 report from the Clear Grid Initiative.

For the longer term, I believe electrical energy utilization will probably be significantly larger than anticipated given the substantial progress potential in EVs and information facilities. As such, I’d not be shocked if electrical energy demand progress had been larger than the 4.7% high vary that the Clear Grid Initiative predicts over the following 5 years.

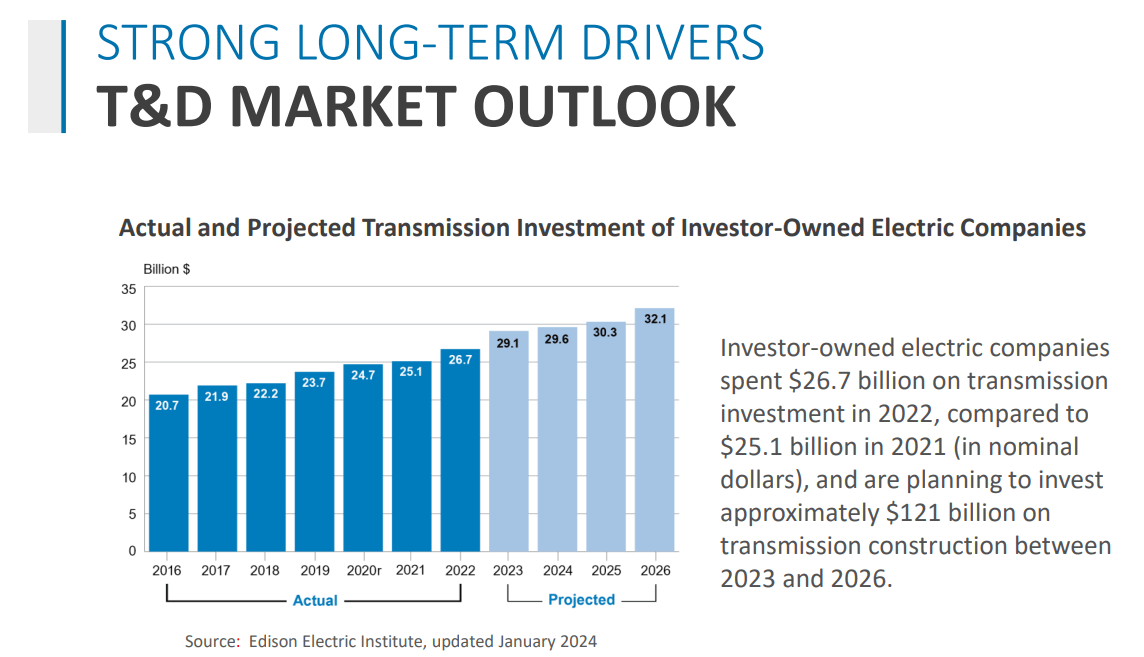

Because of the rise in want to fulfill load progress, investor-owned electrical corporations are anticipated to take a position $121 billion on transmission development between 2023 and 2026, doubtlessly serving to enhance demand for MYR Group’s T&D section.

MYR Group Investor Presentation

Previous 2026, there’s extra demand progress potential.

Based on the DOE in 2023, U.S. transmission techniques must develop considerably by round 60% by 2030 and will must triple by 2050 to fulfill clear electrical energy calls for.

If electrical energy consumption exceeds estimates, I’d not be shocked if U.S. transmission techniques must develop even larger than 60% by 2030 as properly.

Along with non-public sector demand, there’s authorities assist in serving to enhance and broaden the grid. Particularly, a strong tailwind for demand for MYR Group’s T&D section is the $1.2 trillion Infrastructure Funding and Jobs Act (“IIJA”) that features $73 billion for the electrical grid and power infrastructure. Based on MYR Group, mixed federal spending deliberate for power over the following 5 to 10 years is over $300 billion between the IIJA and the Inflation Discount Act.

Likewise, MYR Group’s C&I section additionally advantages from the Infrastructure Funding and Jobs Act, serving to doubtlessly enhance demand for the section.

Dangers

MYR Group wins substantial enterprise from aggressive bidding processes. In consequence, its margins might slender if competitors will increase.

Weak financial situations might trigger utilities and different prospects to postpone some capital applications which could lower demand for MYR Group.

MYR Group might make a nasty acquisition.

If demand weakens for MYR Group, its financials might underperform.

My Take

When it comes to expectations as of March 28, analysts count on MYR Group’s earnings per share to proceed to extend sooner or later from the $5.40 per share it earned in 2023.

Particularly, analysts on common count on MYR Group’s EPS to rise to $6.44 in 2024, $7.97 in 2025, and $10.75 in 2026, giving the inventory a ahead PE ratio of 27.23 for 2024, 21.98 for 2025, and 16.30 for 2026.

In search of Alpha

When it comes to its valuation, MYR Group has a 5 yr common ahead PE ratio of 18.53 whereas the sector median for ahead PE ratio is nineteen.03.

From the 5 yr common ahead PE perspective, MYR Group’s valuation would not grow to be engaging till 2026.

Moreover, I do not assume the corporate deserves a valuation of over 20 when it comes to ahead PE ratio in a traditional progress atmosphere given MYR Group has to competitively bid for a considerable share of its tasks and the corporate works with comparatively low revenue margins.

With that stated, it is my view that MYR Group has substantial demand tailwinds that might final a number of years that can assist the corporate meet or exceed its 2025 and 2026 estimates. Given administration has guided for softer high line income progress in 2024, I’m extra cautious about 2024, however I believe there is a respectable probability the corporate will nonetheless meet EPS estimates for the yr.

When it comes to demand tailwinds, I believe there’s sufficient visibility and progress potential within the medium to long run for MYR Group to commerce for 19x 2026 EPS estimates, so I’ve a worth goal of $204.25 per share. I believe the inventory might obtain that worth in a yr or two as demand continues to strengthen given the corporate’s tailwinds.

As such, I fee MYR Group a ‘Purchase’ and I’d personal it in a diversified portfolio that features the Magnificent Seven. With that stated, I do not assume MYR Group is an ‘Obese’ as the corporate is not a dominant firm with quite a few aggressive benefits.

For the longer term, I’d comply with earnings studies and see if MYR Group’s income, EBITDA, EPS, and backlog are rising.

Moreover, I’d comply with electrical energy utilization traits. If electrical energy consumption progress exceeds expectations by a considerable margin, I believe there’s potential for much more demand for grid upgrades and upkeep.