PhonlamaiPhoto

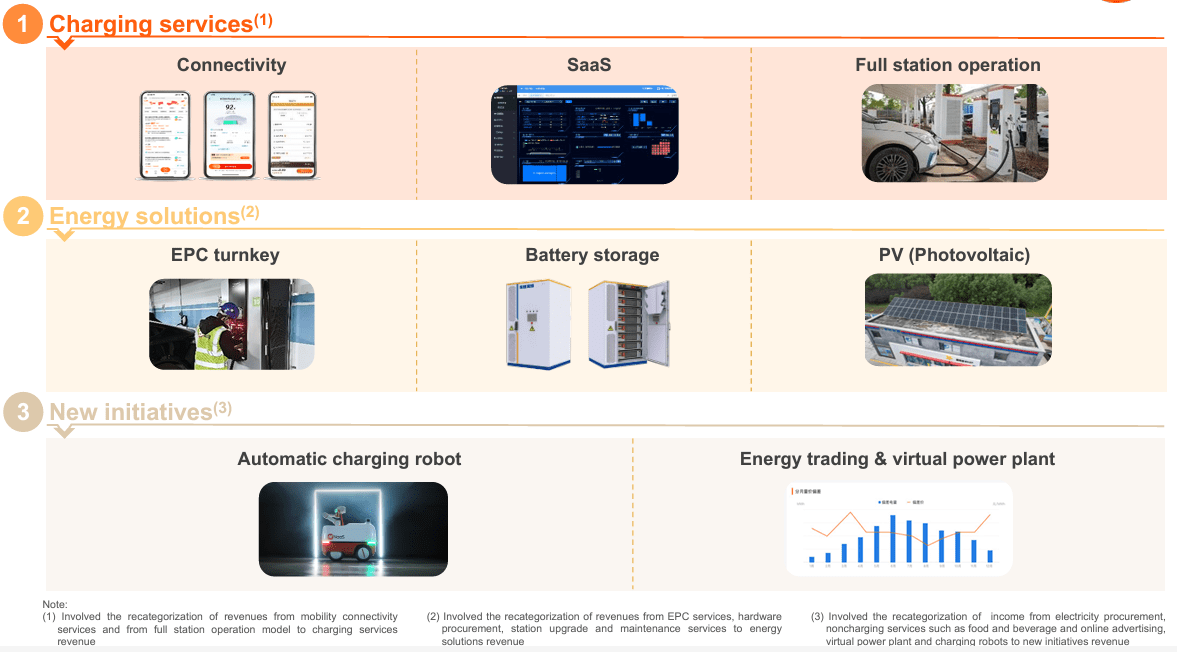

NaaS Expertise (NASDAQ:NAAS) is a one-stop charging resolution supplier to charging station homeowners providing providers via a station’s preliminary constructing, working and improve, in addition to extra service levels. Its providers span throughout your complete life cycle of a charging station, together with 1) mobility connectivity providers to public customers throughout a station’s operation stage, 2) offline providers together with website choice, charging gear procurement, EPC and financing to charging station homeowners on the preliminary station constructing stage, 3) offline working/upkeep providers, different non-charging station improve and extra providers like ESS/PV EPC, Digital Energy Plant (VPP) buying and selling and battery testing and recycling and battery swap providers to charging station homeowners on the stations’ working and improve/extra service levels.

In Oct’23, Jefferies revealed ‘First Mover in International Charging Ecosystem; Provoke Protection on NaaS’, and set NAAS goal value as $4.50. Key funding thesis included 1) rapidly-rising EV inhabitants, 2) benefit of “all-in-one” options, and three) Abroad enlargement.

Firm Web site

My earlier article revealed on March 4th 2024, Green Energy Leader NaaS Expecting 4-5x Topline Growth In FY24, centered on its potential for topline progress, the sturdy demand for public charging in China, and the important thing partnership improvement with Geely. NAAS Inventory value dropped by 23% since then on account of traders’ fear about NAAS’ path to profitability. For my part, topline acceleration and correct value effectivity management are key to NAAS turning worthwhile. On this article, I need to focus on its key drivers alongside an replace on its Q4’23 earnings release.

NAAS reported strong income progress with vital margin enchancment, on observe to attain break-even by the top of 2024

Key takeaways from the NAAS This fall’24 earnings launch embody shiny spots resembling 1) distinctive topline progress, 2) a major enchancment in gross margin of 21 ppts, and three) stable progress in operational metrics. The first threat on its P&L facilities round profitability. See particulars as follows.

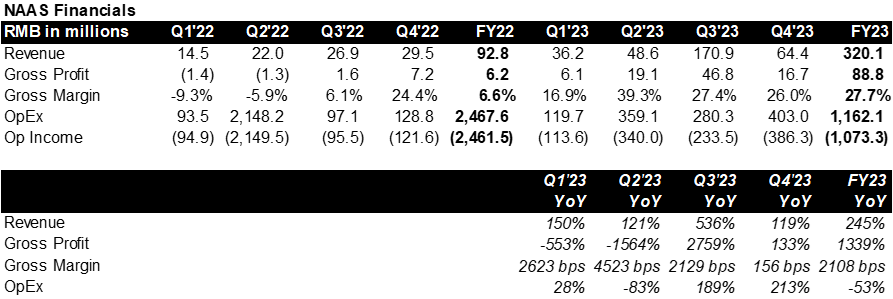

Income: RMB64.4 million (+119% YoY) in This fall’23, and RMB320.1 million (+245% YoY) in FY23. Whereas charging service revenues noticed strong progress in FY23 (RMB129.1 million, +56% YoY) benefiting from a rising charging community, vitality options revenues turned an exceptionally shiny spot (23x income improve YoY), accounting for 58% of whole income.

Gross margin: 26.0% in This fall’23, up from 24.4% in This fall’22, 27.7% in FY23, up from 6.6% in FY22. Gross margin enchancment was primarily pushed by product combine shift to Vitality options by capitalizing the corporate’s “know-how and capabilities in delivering and executing energy solution projects of different scales“.

Op loss: RMB386.3 million in This fall’23, and RMB1,073.3 million in FY23. Working bills decreased from RMB2,467.6 million in FY22 to RMB1,162.1 million in FY23 on account of a one-time Fairness-settled itemizing value of RMB1.9 billion in 2022. Excluding the one-time value, OpEx elevated from 136% from RMB283.3 million in FY22 to RMB669.8 million in FY23 (+136% YoY) primarily on account of “professional fees to initiate market expansion as well as increased expected credit losses that reflected market conditions“. At this level, NAAS, at a speedy enlargement stage, might proceed to incur value improve in gross sales and advertising and marketing. Nevertheless, if we exclude prices which can be seemingly not recurring, resembling skilled charges, I might suppose NAAS moved a lot nearer to a breaking-even level. If NAAS achieves 4-5x topline improve in FY24, I consider will probably be capable of break even inside FY24. What is the chance of hit that concentrate on? There are a few issues offering me the boldness. First, the corporate beforehand supplied income steerage of RMB2-3B in FY24, which is about 6x-9x of FY23 income. Second, as I mentioned in my earlier article, “NAAS has a solid Energy Storage solutions pipeline. According to its prior earnings call, the company has 380 contracted stations that requires energy storage solutions. In Q3’23, 43 out of the 380 was delivered. Looking at longer teams, the company mentioned 1,880 stations in midterm, and 73,000 in the long run. This leading indicator gave me conviction in NAAS future revenue growth.“

Capital IQ

Operational metrics: 1,324 GWh in This fall’23 (+55% YoY), and 4,958 GWh in FY23 (+81% YoY); RMB1.2 billion (+47% YoY) Gross transaction worth via Naas’ community in This fall’23, RMB4.7 billion (+74% YoY) Gross transaction worth via Naas’ community in FY23; 77,017 (+54% YoY) charging stations in FY23; 875,655 (+70% YoY) EV chargers in FY23. Operational metrics demonstrated that NAAS is ready to serve the sturdy demand in China very properly.

NAAS is diversifying its income streams, with vitality resolution providers now accounting for 58% of whole income

The No.1 income progress driver for NAAS is their vitality resolution providers, which now account for 58% of whole income. Alongside the quickly rising market in China, NAAS stands out with its deep know-how and assets on each the provision and demand sides. This house has a excessive barrier to entry, making it extra worthwhile.

NAAS’ technique of doubling down on vitality resolution providers is an excellent one in my view. As new entrants more and more spend money on EV charging, NAAS can place itself greatest by serving gamers on this ecosystem with its differentiated functionality as a one-stop resolution supplier.

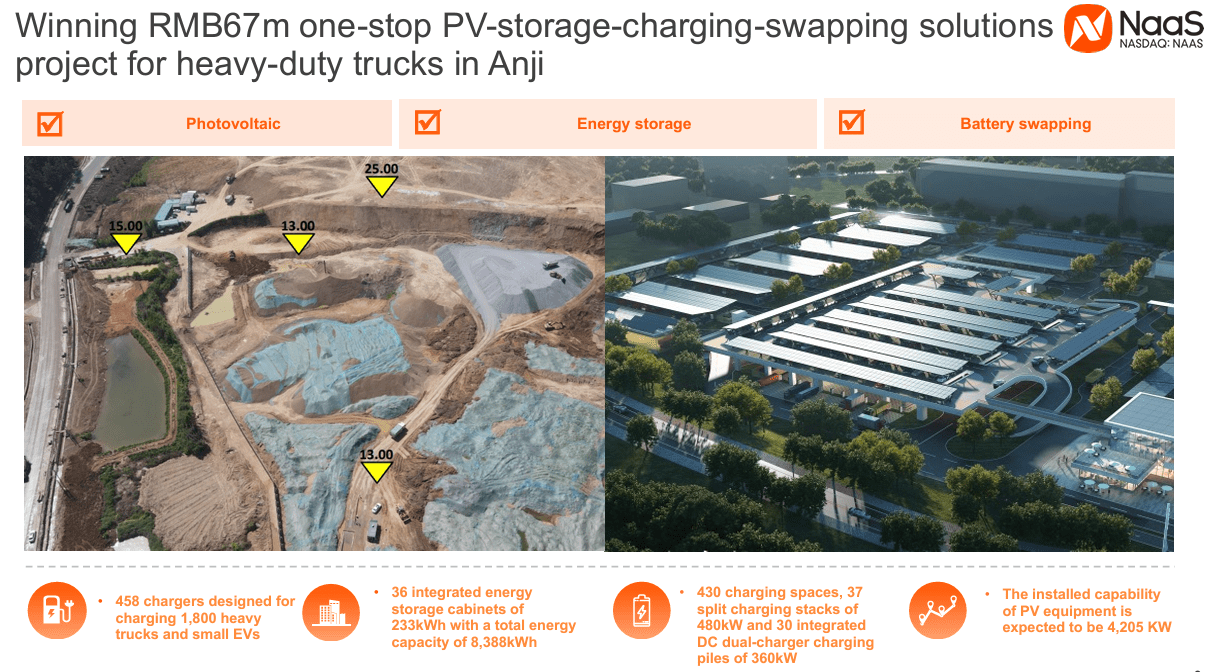

Here’s what a one-stop options mission seems to be like (see particulars within the company press release). As proven within the following image, this one-stop PV-storage-charging-swapping resolution consists of the provision, procurement, set up, and grid connection of charging techniques, battery swapping techniques, PV techniques, and vitality storage techniques. This resolution has a excessive influence, marking key milestones. In response to the corporate’s press launch, “upon completion, Anshan Station is expected to generate 4.328 million kWh of electricity annually, saving 1,358.9 tons of standard coal and reducing carbon emissions by about 3,580.5 tons per year.” Furthermore, that is simply the beginning through the development section. NAAS can also be creating an vitality administration platform and system for its operational stage.

Because the income combine continues to shift in the direction of resolution providers, NAAS’s working margin will seemingly enhance additional.

Firm presentation

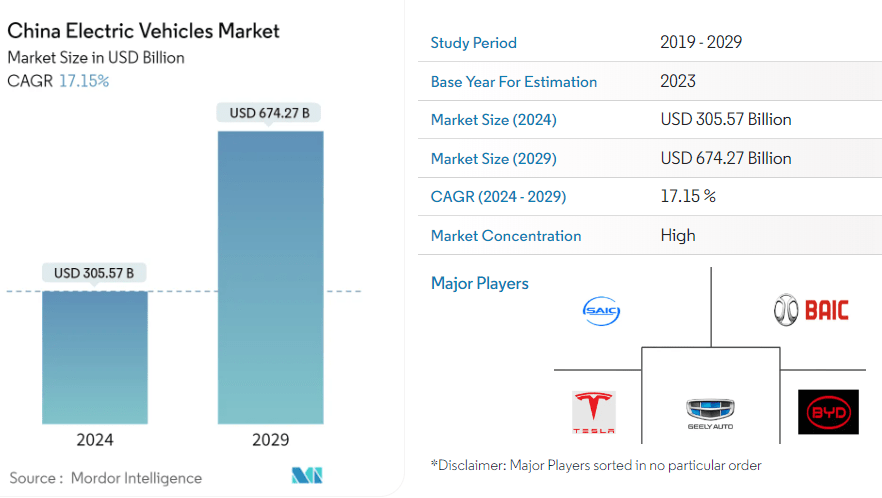

China’s EV trade leads globally, experiencing unparalleled progress, which fuels substantial enlargement within the EV public charging sector.

The EV trade in China is experiencing unparalleled secular progress. In response to Mordor Intelligence, “the China Electric Vehicles Market size is estimated at USD 305.57 billion in 2024, and is expected to reach USD 674.27 billion by 2029, growing at a CAGR of 17.15% during the forecast period (2024-2029).” This progress price is sort of 2x of the growth rate of EV market worldwide.

Mordor Intelligence

NAAS Inventory Valuation

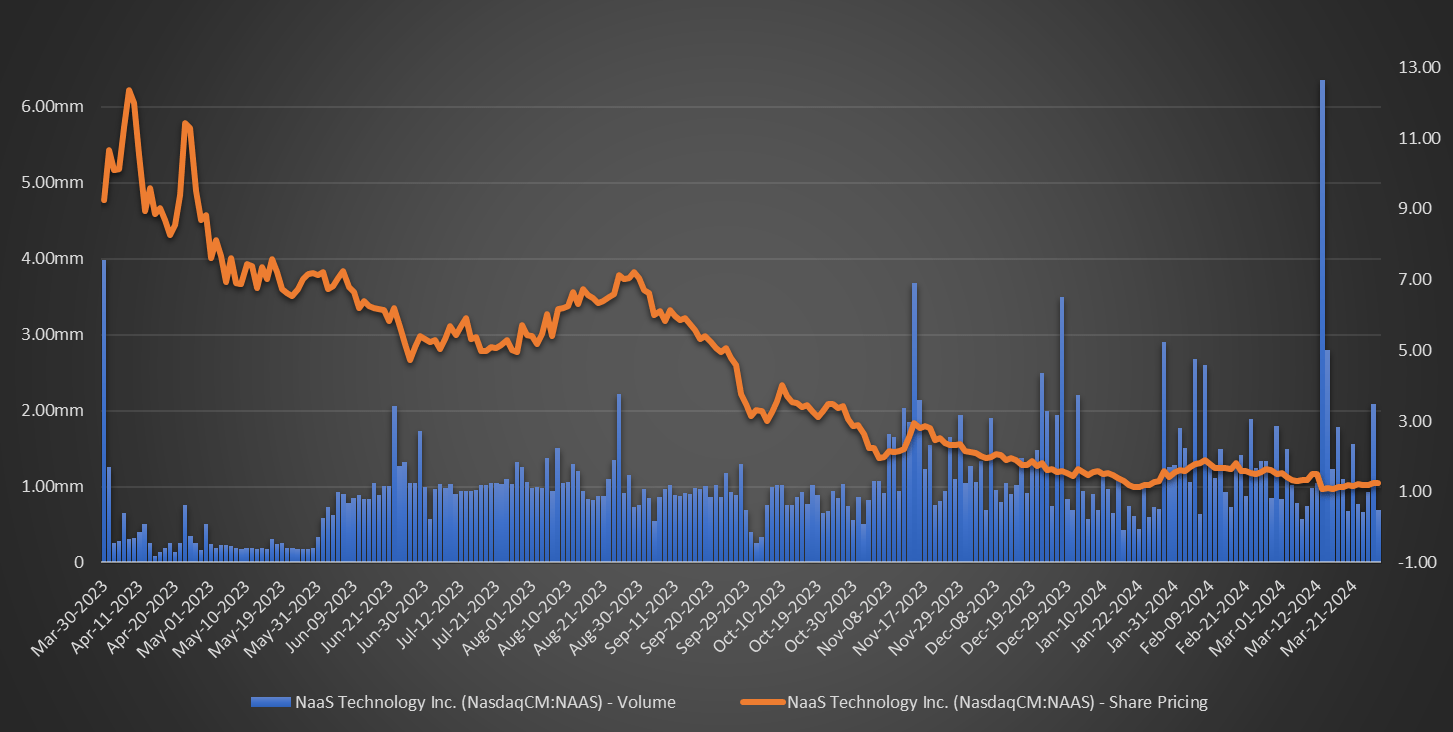

NAAS is at the moment traded at $1.24, in comparison with a 52-week excessive of $12.78 and a 52-week low of $1.07. 12 months-to-date, it has been trending round its decrease certain value.

Right here is how I calculate NAAS’s worth for a base case. For its vitality resolution enterprise, its closest peer, Qingdao TGOOD Electrical Co., Ltd. (SZSE:300001), is at the moment traded at 55x P/2024 Earnings. Qingdao TGOOD Electrical LTM income was RMB2 billion, ~6x of NAAS, and Gross margin 21% is akin to NAAS. I utilized 30x for NAAS vs 55x for Qingdao TGOOD Electrical, and the low cost was on account of totally different enterprise measurement and threat profiles. For its charging service enterprise, its closest peer, Allego N.V. (NYSE:ALLG), is traded at 2.7x P/2024 Gross sales. Allego LTM income is ~4x of NAAS, and Gross margin 23% is akin to NAAS. I utilized 2x for NAAS vs 2.7x for Allego to account for various enterprise measurement. Subsequently, making use of 30x P/E for its vitality resolution enterprise, and 2x P/S for its charging service enterprise to my projection for 2024 (RMB2.5 billion in whole income, and RMB180 million in vitality resolution earnings), the estimated honest worth can be $4.3 per ADS.

Evaluating with my earlier article I utilized extra conservative multiples (30x P/E for vitality resolution enterprise vs 40x prior, 2x P/S for charging service enterprise vs 5x prior) to account for dangers round profitability.

Capital IQ

Conclusion and Funding Dangers

NAAS is underpriced, particularly contemplating its potential income progress acceleration in FY24. Buyers on the lookout for ESG alternatives ought to undoubtedly test this out.

Buyers ought to be conscious of the next dangers related to NAAS:

Operation threat: NAAS remains to be experiencing vital working losses (RMB1,073 million in FY23). Attaining profitability depends on accelerating progress in its topline and enhancing operational effectivity through the enterprise enlargement stage. One query from traders could also be “what about NAAS’ ability to fund its operations“? In response to NAAS SEC filings, RMB 600 million banking facility was newly entered into in 2022. As of Dec’31 2023, NAAS had RMB506 million in money and short-term funding, and RMB1,144 million in whole present Property. For brief-term liquidity, present ratio 1.4x, and fast ratio 0.8x. For long-term solvency, long-term debt to capital ratio was 69%. I’m optimistic about NAAS’ capability to fund its operations.

Competitors threat: In a market experiencing secular progress, competitors will rise, and new gamers might disrupt the market with totally different enterprise fashions or modern services or products.