Picture Supply/DigitalVision by way of Getty Photographs

Introduction

Dividend progress investing is a method that actually fits me as an individual. I additionally wish to have a mixture of completely different dividend progress shares. My portfolio consists of firms which can be extra secure and the place the dividend is rising steadily, however I’m additionally keen on firms with excessive dividend progress potential. Since I’m in my early thirties, I can afford to purchase high quality firms with a comparatively low dividend yield however with the potential to develop into dividend monsters.

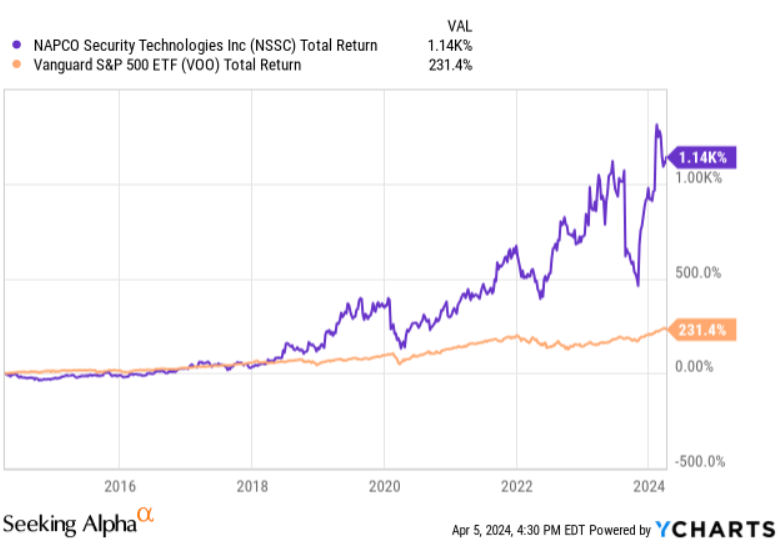

With this in thoughts I got here throughout the corporate named Napco Safety Applied sciences, Inc. (NASDAQ:NSSC). The corporate has been round for a very long time and has achieved an enormous outperformance in comparison with the S&P 500 index.

NSSC 10Y efficiency (Ycharts)

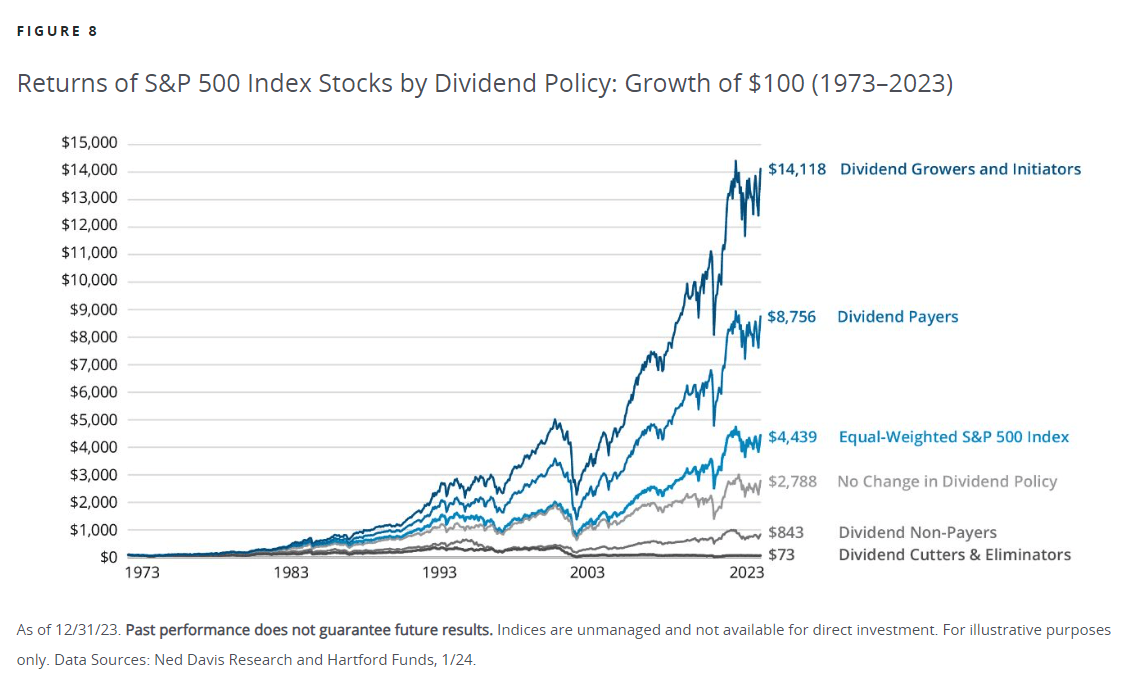

And if we took an extended timeframe the distinction in efficiency is even larger. Final yr, the corporate has initiated a dividend and has elevated it a number of occasions, the final time it was really 25%! Does that imply that much less progress will be anticipated? I do not assume so. The corporate seems to be turning into increasingly mature and initiating dividend funds definitely doesn’t must have an effect on the long-term inventory efficiency.

Efficiency dividend progress shares (hartfordfunds.com)

There are a whole lot of issues that I like concerning the firm and I want to decide whether or not NSSC is price including to my (dividend) portfolio.

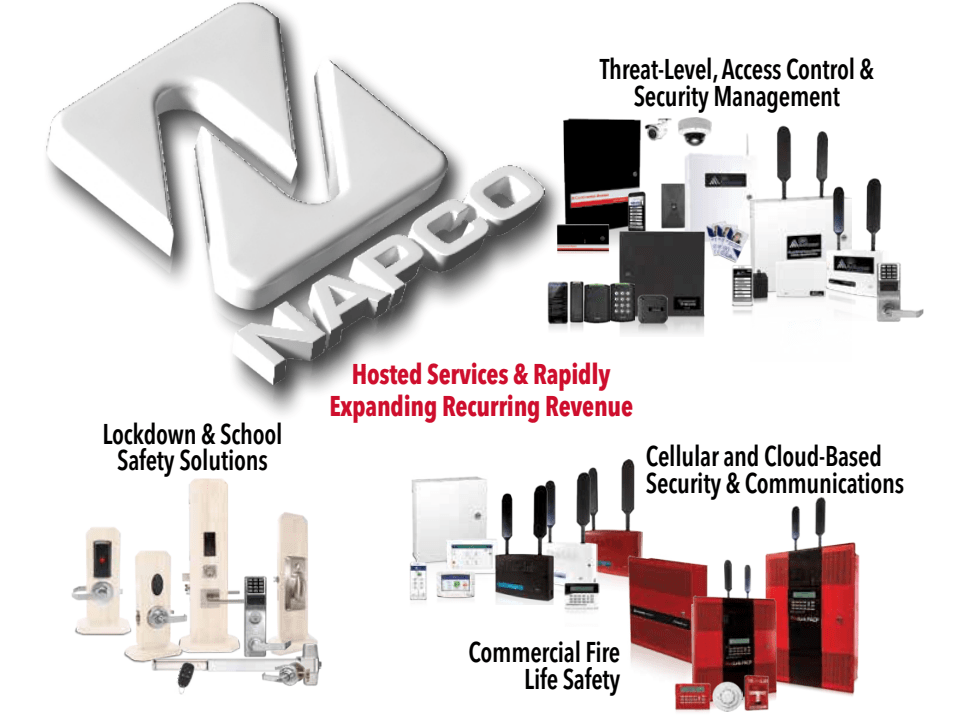

NSSC is all about safety. The corporate was based in 1969 and is headquartered in Amityville, New York. NSSC has a protracted historical past within the safety sector and remains to be one of many market leaders in manufacturing safety merchandise. This contains, entry management programs, business fireplace alarm programs, video intrusion alarm programs and architectural locking {hardware}.

Product portfolio (NSSC investor presentation)

If you’re keen on all the product portfolio, you may go to the NSSC investor relations web site.

The corporate can also be creating new merchandise to maintain forward. An instance of this within the all-in-one alarm for safety, fireplace, video and linked house referred to as “Prima”.

Prima (NSSC merchandise web site)

Prima has the potential to handle completely different goal audiences inside the safety market, resembling residential or small companies. This product additionally affords subscription choices, which ends up in a stream of recurring income.

So, now that we’ve got a way of what the corporate does, what makes NSSC a high-quality enterprise?

Aggressive benefit

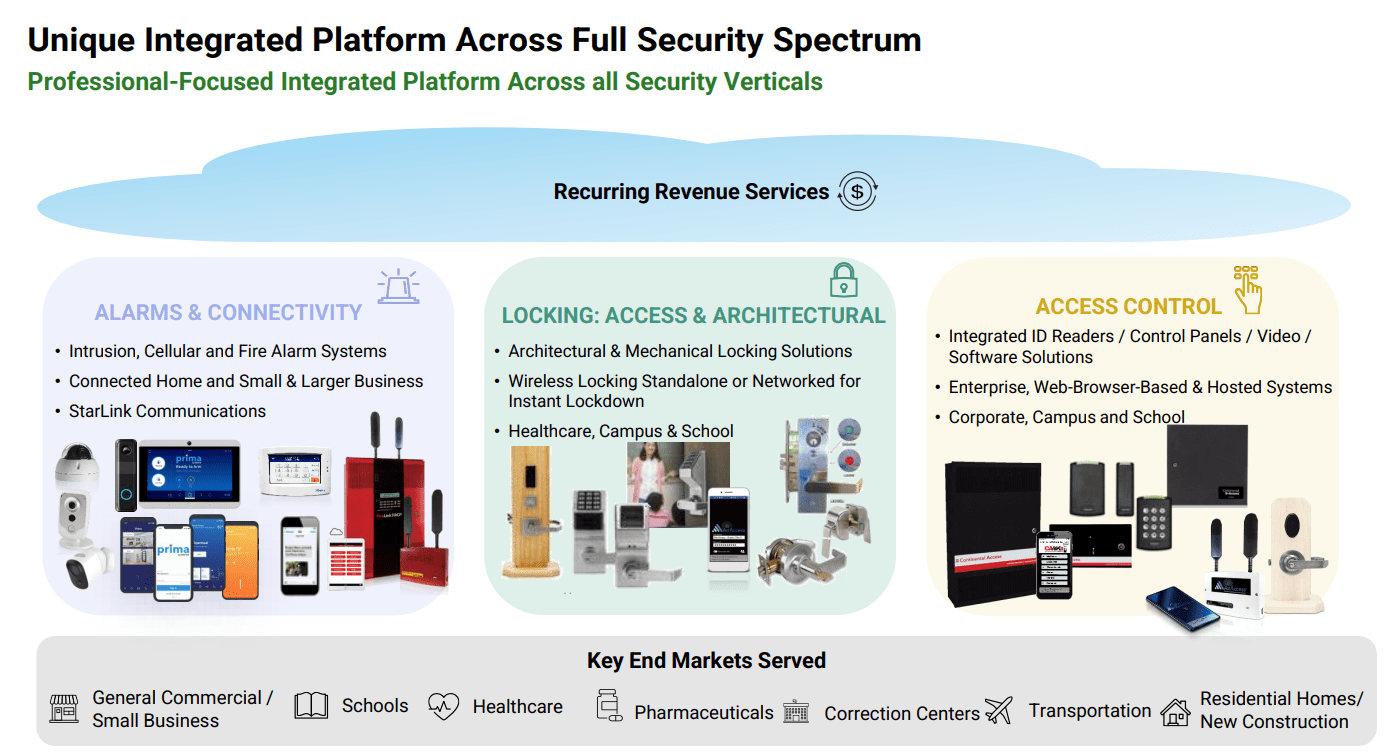

What the corporate differentiates from its rivals is that NSSC is concerned in several safety product segments. Usually these merchandise require completely different programs. Within the case of NSSC they will provide prospects one built-in resolution, this ought to be a profit for the corporate and the client in the long term.

Built-in platform (NSSC investor presentation)

That is an instance that NSSC itself offers of their 2023 annual report:

One other instance is Pepperdine College in Malibu, California, the place the Firm offered a lockdown system in place for its over 1,700 dorm rooms that required each locking and entry management applied sciences. We had been chosen as a result of we had been the one safety firm that has each locking and entry management applied sciences that work on the identical platform and met the wants of the college.

Financials

NSSC has proven that it might probably develop constantly over longer durations of time.

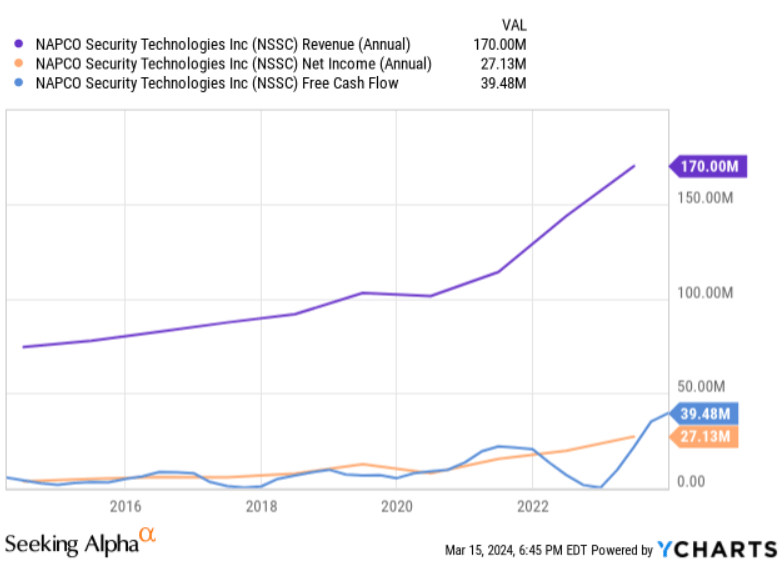

Monetary metrics (Ycharts)

In 10 years, the corporate has grew its income with a CAGR of 8.6%. Taking a look at web revenue is even higher with a 10Y CAGR or 22.7%. FCF per share has grew with a 10Y CAGR of 19.4%. This calculation was carried out over FY 2014 to FY 2023. But when I took FY 2014 as the start line to TTM, these percentages could be a lot greater, particularly from a backside line perspective.

Monetary metrics (Looking for Alpha)

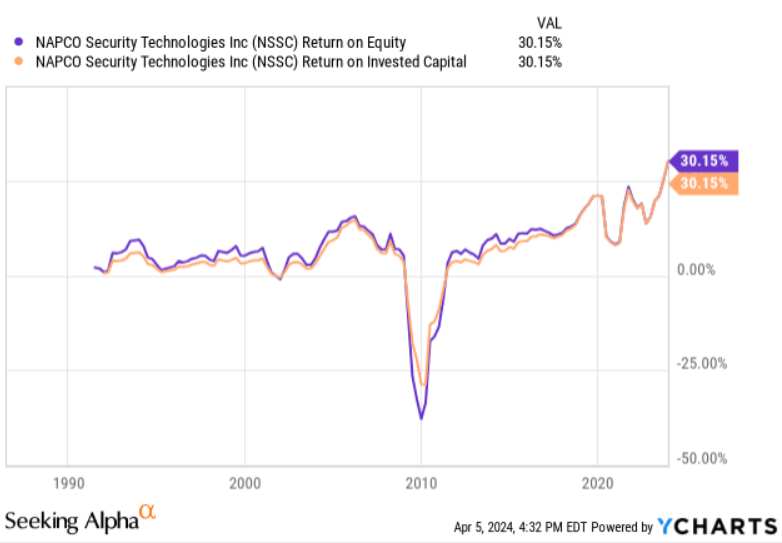

This is a sign that the corporate is turning into more and more worthwhile. NSSC appears to be a capital-light enterprise with a CapEx to gross sales ratio of 1.7% ($2.962 million /$170 million), which is right for worth creation. Speaking about worth creation, the ROE and ROIC exhibits that NSSC is superb at doing this.

ROE & ROIC (Ycharts)

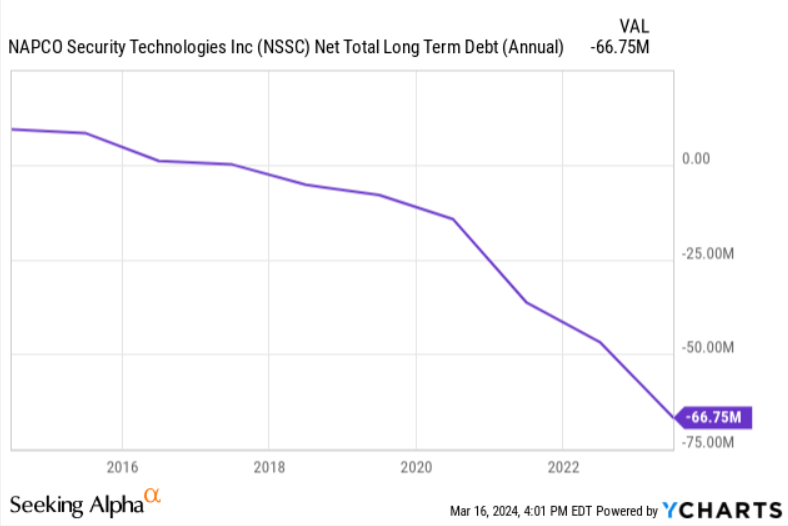

The corporate additionally has an especially wholesome stability sheet. Primarily based on their final report they’ve a complete money and equivalents of $79 million and a complete debt of simply $5 million.

Internet debt improvement (Ycharts)

As you may see within the chart above, the web long run debt is enhancing and in the meanwhile they do not have curiosity expense to fret about.

Briefly, NSSC has a whole lot of high-quality traits. The corporate can also be in wonderful monetary form and seems to be accelerating when it comes to profitability lately.

Alternatives for progress

The outcomes from the previous are in fact good, however investing is in fact concerning the future. So what’s left within the tank to maintain on rising when it comes to income and profitability?

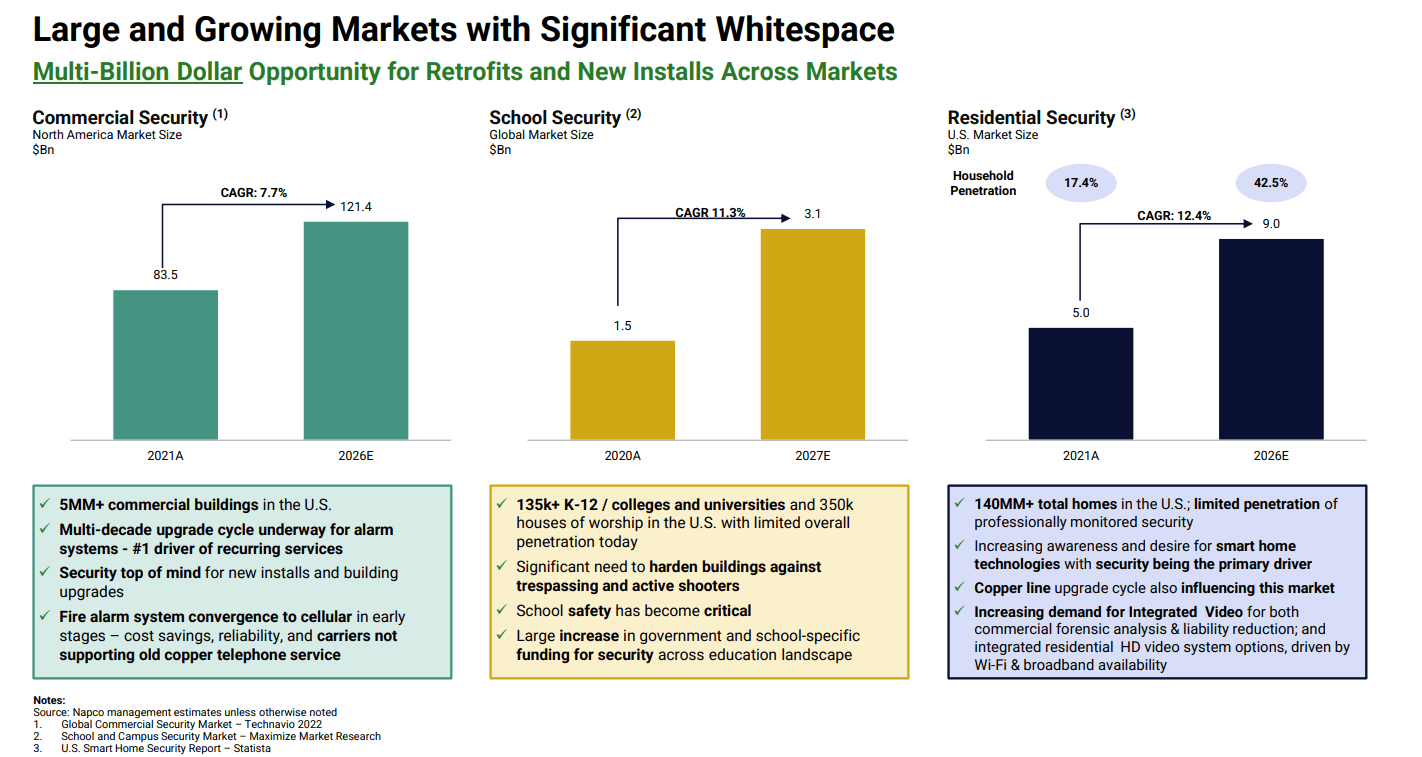

Growing demand for public security and college safety

NSSC is working in a rising market. Primarily based on the entire addressable market there’s nonetheless loads to win. NSSC itself says the next about this:

Within the U.S., there are over 100,000 Ok-12 faculties, over 5,000 faculties and universities and over 350,000 homes of worship. Administration estimates that lower than 10% of those establishments have ample safety from an energetic shooter or intruder.

Significantly in faculties, it’s important that public security is nearly assured. Nevertheless, the variety of terrorist actions and taking pictures incidents has continued to extend. Burglaries, theft and vandalism are additionally components that ought to set off market progress.

Primarily based on research, the college and campus safety market dimension was $1.82 billion in 2022 and is predicted to develop with a CAGR of 11.3% by way of 2023 to 2029. Additionally within the business and residential safety adequate market progress will be anticipated.

Safety progress tendencies (NSSC investor presentation)

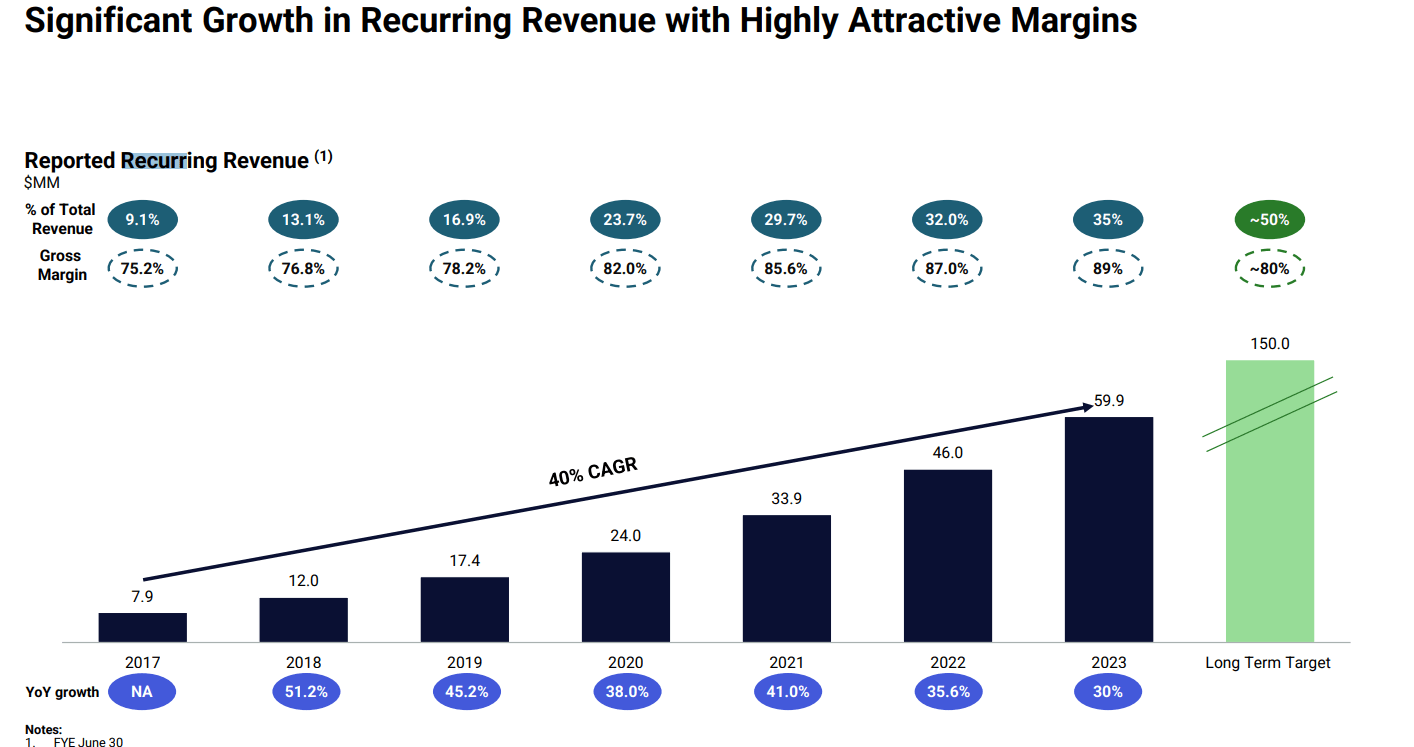

Recurring income potential

What I actually like about NSSC is {that a} important a part of their income (39%) has a recurring nature, generated from their communication companies. This primarily consists of month-to-month subscription charges. Primarily based on the numbers of the 2023 annual report, revenues of those companies have elevated 77% from FY 2021 to FY 2023. In the meanwhile this companies have a gross margin near 90%. Even supposing these margins are insanely excessive, the recurring income additionally affords a security cushion for volatility in tools demand.

Income distribution (NSSC 2023 annual report)

NSSC is constant to introduce merchandise that generate recurring revenues, resembling StarLink, iBridge, iSecure and Prima. Administration will proceed to give attention to it they usually have a long-term recurring income goal of fifty% with a gross margin of round 80%.

Recurring income improvement (NSSC investor presentation)

Administration

High quality firms are sometimes led by excellent managers. An enormous plus is that the corporate remains to be founder led. Founder led companies typically are likely to outperform the remaining. The CEO and Founding father of NSSC is Richard Soloway. He has a whole lot of expertise within the safety area, similar to the opposite members of administration.

Administration overview (NSSC investor presentation)

Additionally the CFO, Kevin Buchel has been working at NSSC for a very long time (1995). Contemplating the corporate’s efficiency over the previous a long time, administration has a superb monitor document. Additionally it is crucial that the pursuits of the managers match these of you as a shareholder. Primarily based on the 2023 annual report administration personal roughly 10% of complete frequent inventory, in order that they have important pores and skin within the recreation. Administration with pores and skin within the recreation are usually extra targeted on the long run , which affords the next probability of outperformance.

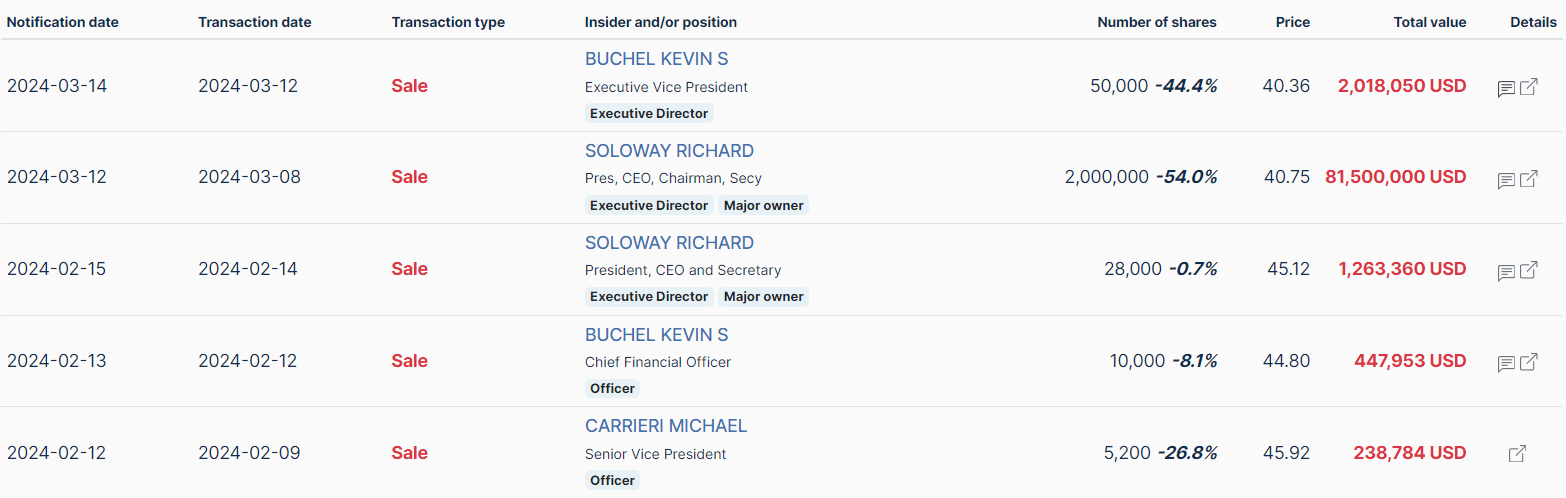

It ought to be famous that there was some important insider promoting this yr. That is would not must be a purple flag, however you will need to control. It is not the primary time administration has bought massive quantities of shares, which on the time couldn’t be linked to dangerous efficiency of the corporate.

NSSC insider promoting (Insiderscreener.com)

Dividend

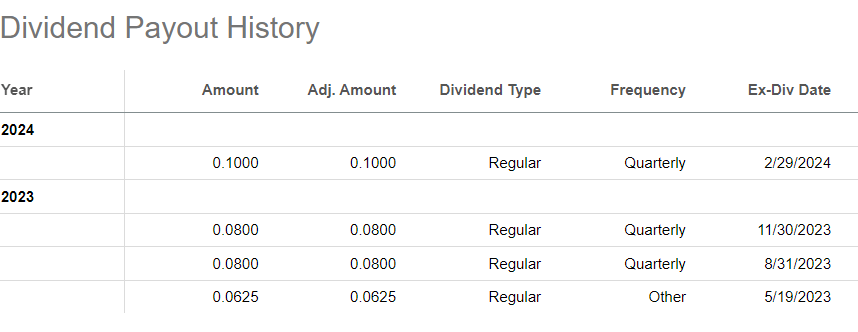

NSSC’s dividend historical past has simply begun. On the eighth of Might 2023 they initiated a quarterly dividend of $0.06 per share. Since then they elevated it in August with a whopping 28% and in 2024 they hiked it once more with 25%.

Dividend payout historical past (Looking for Alpha)

I believe it is a logical step for NSSC as it’s turning into a extra mature firm that’s producing increasingly free money circulation.

In the meanwhile the corporate has a TTM dividend yield of 0.8%, which is pretty low, but when we take the expansion charges under consideration this might grow to be a gorgeous dividend progress inventory. Mix this with the longer term progress prospects and a protected payout ratio of 18.7% and I believe NSSC has the potential to grow to be an fascinating dividend play.

Dividend abstract (Looking for Alpha)

I have not learn something particular a couple of dividend progress coverage but, but it surely appears to be a part of their capital allocation technique now.

Q2 2024 outcomes

NSSC is delivering excellent outcomes. In Q2 2024 they managed to report document gross sales once more. Which was their 13th consecutive quarter of document gross sales, which is spectacular.

NSSC monetary outcomes (Q2 2024 earnings report)

An vital a part of my funding thesis is the recurring month-to-month income progress. This was 25% greater ($18.5 million) in comparison with the identical interval final yr ($14.9 million).

It does seem that tools gross sales have discovered their approach again up. Tools gross sales elevated 6% ($29 million) in comparison with final yr, because of elevated gross sales in Alarm Lock, door-locking merchandise and intrusion merchandise. Over a half yr interval the rise in sale was simply 1% in comparison with the yr earlier than.

Their gross margin elevated from 34% to 53% from a Q2 to Q2 foundation. That is primarily as a result of enhance in recurring income, with a gross margin of 90%. Gross margins within the tools phase are additionally rising once more, with a robust rebound from 7% to 29%. Lengthy story brief, NSSC has delivered sturdy outcomes. The corporate expects persevering with to take action sooner or later. NSSC has skilled some provide chain points, which have led to considerably greater prices. This isn’t utterly resolved however issues are actually getting higher.

Valuation

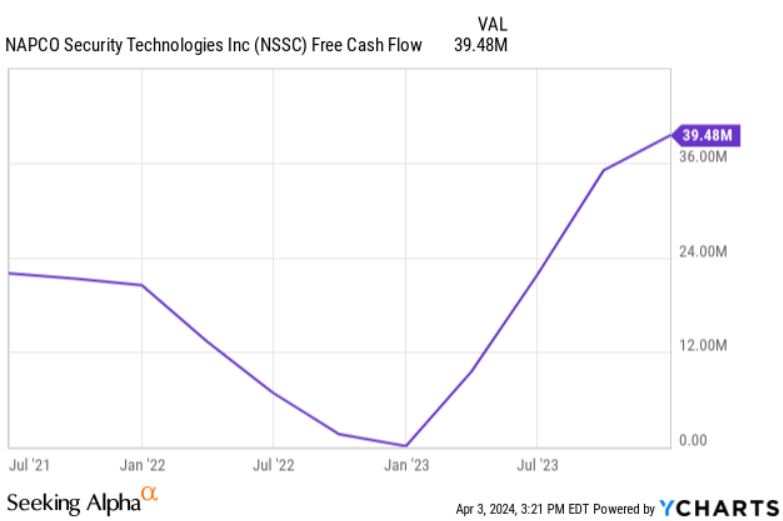

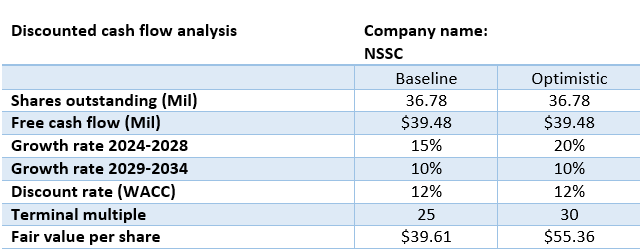

To calculate the intrinsic worth of NSSC, I used discounted money circulation evaluation. For the evaluation I used the present FCF of $39.74 million. I created two situations, a extra conservative baseline case and a extra bullish case.

FCF improvement (Ycharts)

For my calculations it is a good place to begin, as a result of I anticipate extra consistency and progress in FCF within the coming years .

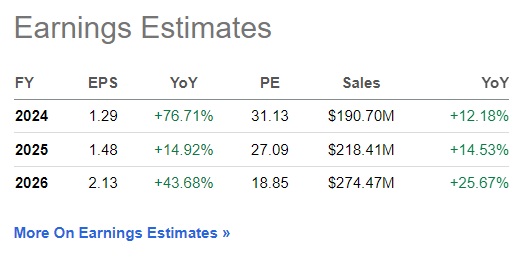

If we check out the earnings estimates on the Looking for Alpha web site, analysts even have excessive progress expectations.

Earnings estimates (Looking for Alpha)

I believe a 5Y free money circulation progress of 15% is cheap. The safety market is already rising double digits year-over-year and since there are alternatives for important margin enchancment, 15% is on the conservative facet. I used 10% for the 5 years thereafter, as a result of it’s tougher to make assumptions additional into the longer term.

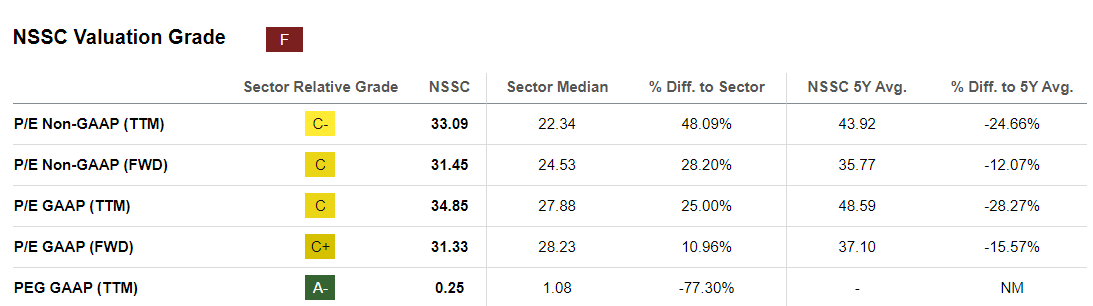

In the meanwhile, NSSC has a PE non-GAAP of 33 and GAAP of 34, which is considerably beneath its 5Y common of 43 non-GAAP and 48 GAAP. Since this firm nonetheless has appreciable progress potential, additionally it is good to take a look at the PEG ratio, which is 0.25 and implies undervaluation.

Valuation metrics (Looking for Alpha)

I used a PE of 25 as a terminal a number of, as a result of NSSC is a high-quality enterprise the place I believe this a number of will be justified. The sector median is 22.34 and I believe NSSC is an above-average enterprise. If the corporate continues to supply these spectacular numbers, a PE of round 30 won’t be misplaced.

Lastly, I used a reduction price of 12% as private hurdle price I demand for NSSC. That is greater than typical, due to the upper danger related to the funding. I’ll clarify this additional within the subsequent a part of the article.

DCF evaluation (Google spreadsheets)

If we do the maths, this involves a good worth of $39.61 per share and a $55.36 per share for the extra bullish case.

As most individuals know, discounted money circulation evaluation is very delicate to the enter given. What will be concluded is that even when utilizing the extra conservative numbers, the present share value of $40.82 is near the honest worth of the baseline case.

Funding dangers

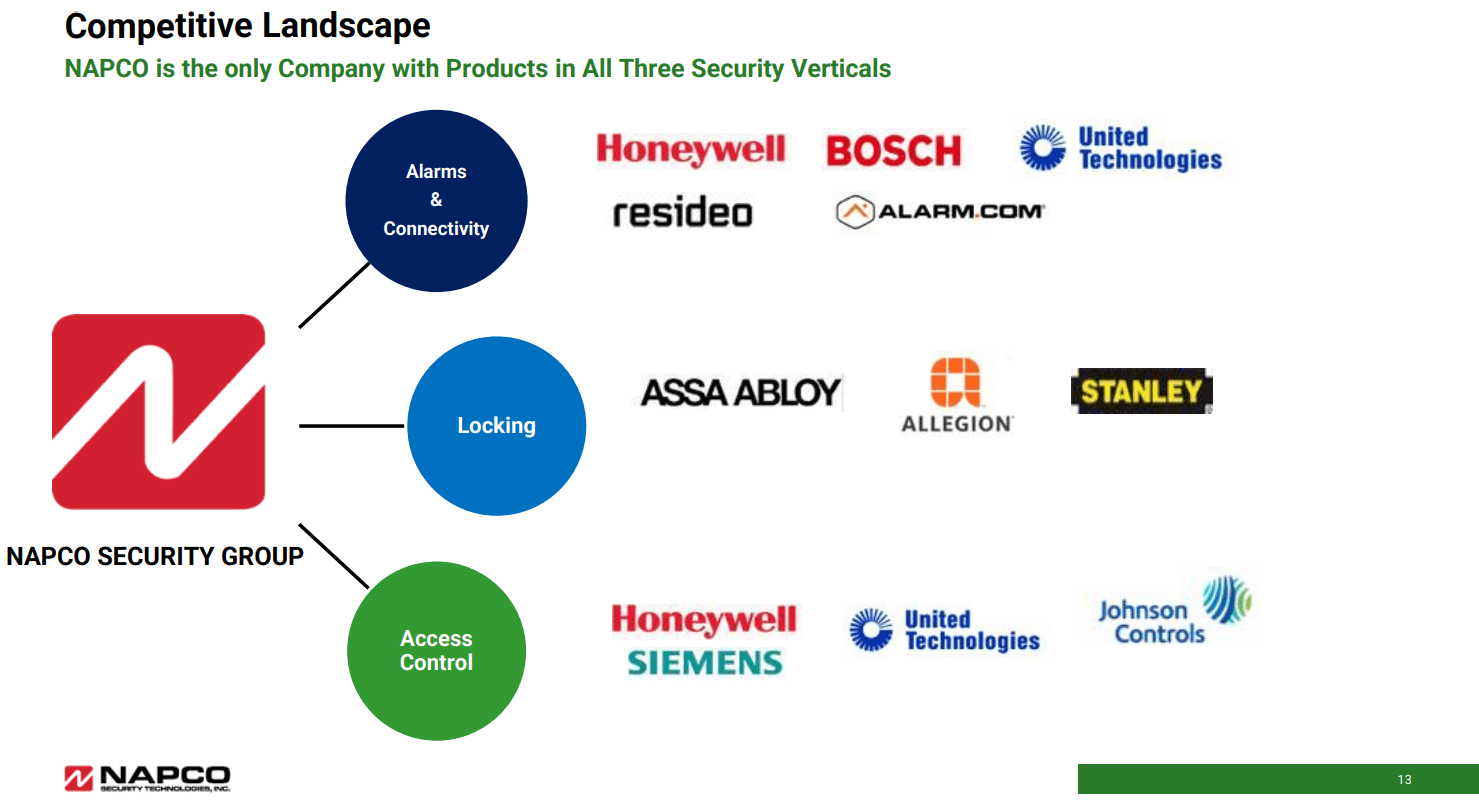

Regardless of there’s a lot to love concerning the firm, there’s additionally some danger concerned. Small companies generally carry extra danger with regards to investing. NSSC has a market cap of $1.5 billion and the primary danger is the potential disruption by the larger gamers within the aggressive panorama. There are no less than 12 different companies which can be additionally working within the safety tools sector, which additionally contains a number of massive firms.

Aggressive panorama (NSSC investor presentation)

These firms can doubtlessly make a lot bigger investments that may typically be financed extra simply in comparison with NSSC. It’s subsequently vital that NSSC allocates adequate capital to keep up its aggressive benefit.

Even supposing the corporate makes numerous R&D investments (traditionally 5 to eight% of complete income), it is just a small quantity in absolute phrases.

A constructive level, NSSC does have a stable long-term monitor document and, because of its dimension and the massive complete addressable market, nonetheless has a whole lot of upside when it comes to progress. Nevertheless, small caps even have extra draw back danger as properly and if the corporate loses its aggressive edge, income progress and enhancement in profitability can go the opposite approach round.

Additionally it is not simple to efficiently roll out the technique with recurring income. This can be a comparatively new half inside the firm and it stays to be seen whether or not this may succeed. Competitors will even know this enterprise mannequin is sort of worthwhile and interference from different firms can presumably trigger margin stress.

Conclusion

NSSC is a high-quality enterprise. The corporate has a superb long-term monitor document and there’s definitely potential to do properly sooner or later. NSSC has wonderful financials, good progress prospects and a pristine stability sheet. The corporate is founder led and administration nonetheless has important pores and skin within the recreation.

Their free money circulation is prone to be extra secure and is rising quickly. Because of extra money, NSSC has began paying a dividend and the corporate definitely has the potential to be a robust dividend grower.

The shares are buying and selling round my calculated honest worth in the meanwhile. NSSC is buying and selling at a excessive PE ratio, however the progress prospects make up for it. Nevertheless, the chance related to this funding is for my part greater than common, however the potential reward is interesting as properly. Due to this, my recommendation is to not make NSSC too massive of a place in your portfolio.

Personally, I’ve definitely grow to be extra within the firm and throughout the course of I purchased some shares on the $39 greenback vary. At present costs I’m leaning extra in direction of a BUY and you must actually see it as a long-term funding, so do not be penny clever pound silly! I’m planning to make it a small portion of my portfolio and I’ll accumulate slowly in line with the greenback price averaging precept.

Pleased investing everybody.