All monetary numbers on this article are in Canadian {dollars} except famous in any other case. Oil and fuel costs are all the time in US$.

Introduction

The opposite day, I learn a really fascinating article on Bloomberg titled “Wall Road Merchants Are Too Scared To Combat The AI Rally.”

What fascinated me concerning the article is that it mentioned that tech has virtually develop into the one recreation on the town, with buyers being too scared to wager in opposition to it.

Apparently, regardless of considerations concerning the ongoing dominance of high-growth shares and potential dangers, the latest efficiency of NVIDIA (NVDA) has pushed bullish sentiment even larger.

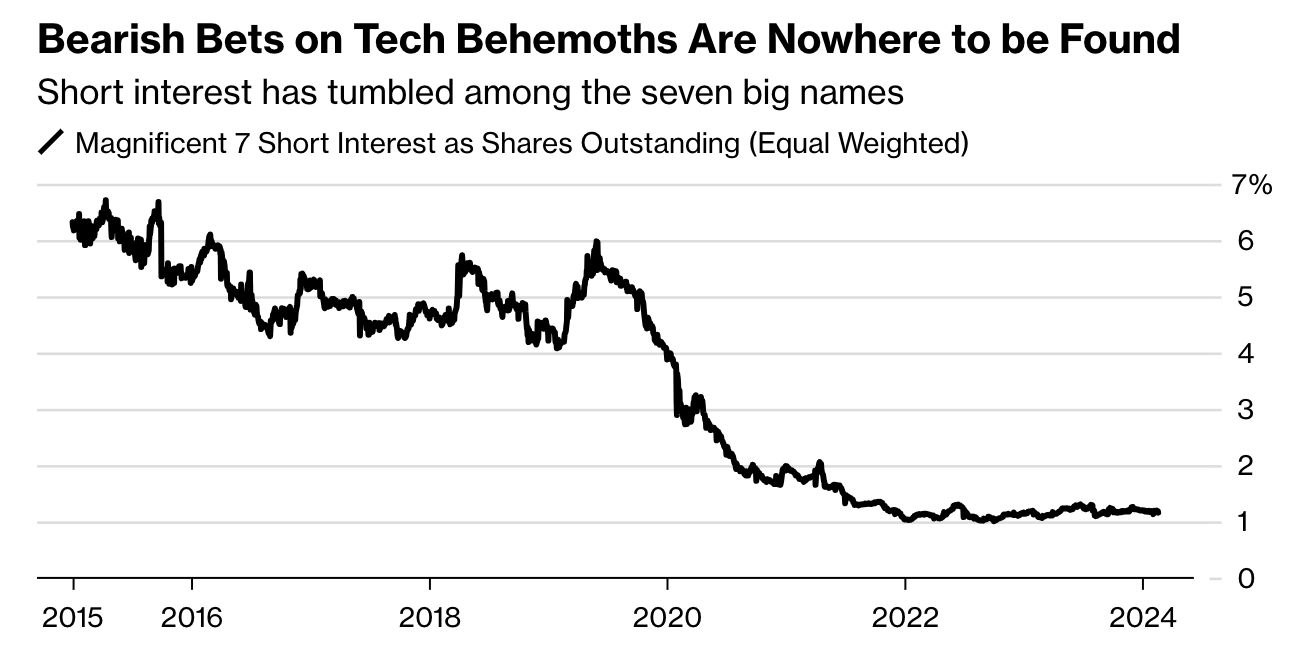

As we will see beneath, brief curiosity amongst main tech firms has fallen to historic lows, which completely displays the overwhelming bullish sentiment.

Bloomberg

Earlier than the pandemic, brief curiosity was hovering shut to five%. Now, it is at simply 1%.

Notice that even earlier than the pandemic, no person “hated” tech. It was already the perfect place to be!

What’s fascinating is that these developments remind me of a dialogue I lately had with certainly one of my readers.

We mentioned that we benefit from doing no matter we wish available in the market, as we do not need to beat the market each single yr.

I consider that after buyers cease making an attempt to beat the market yearly, they’ll construct portfolios that beat the market on a long-term foundation.

In any case, having to beat the market every year (which applies to most cash managers) creates the urgency to all the time purchase the “hot stuff.”

Or, as Bloomberg made the case, with tech-focused indexes persistently rising, energetic managers face growing stress to capitalize on this upward momentum – no matter valuation!

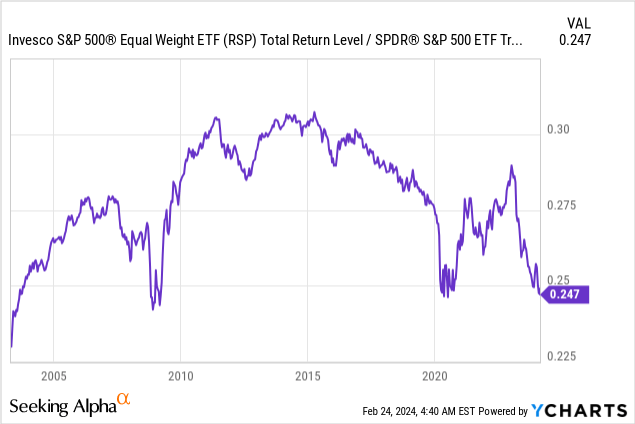

Moreover, as we will see beneath, the ratio of the equal-weight S&P 500 (RSP) to the S&P 500 is near lows not seen for the reason that pandemic and the Nice Monetary Disaster.

The rationale I am bringing all of this up is not to get anybody to brief or promote tech shares.

No, I’m doing what I all the time do. Each time “everyone” needs to wager on the identical theme, I am on the lookout for alternatives elsewhere. I did it in 2020/2021, and I really feel like we’re now in an identical state of affairs – at the very least on the subject of valuation variations.

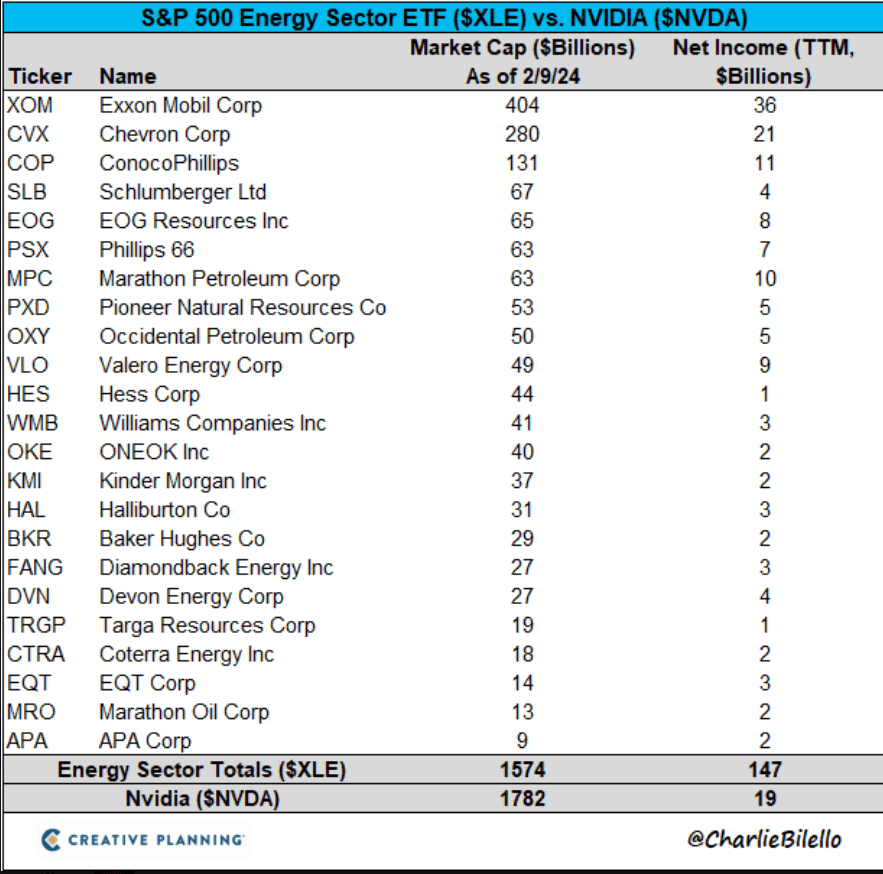

See, NVIDIA is now value greater than all shares within the power sector ETF (XLE) mixed!

Twitter/X @CharlieBilello

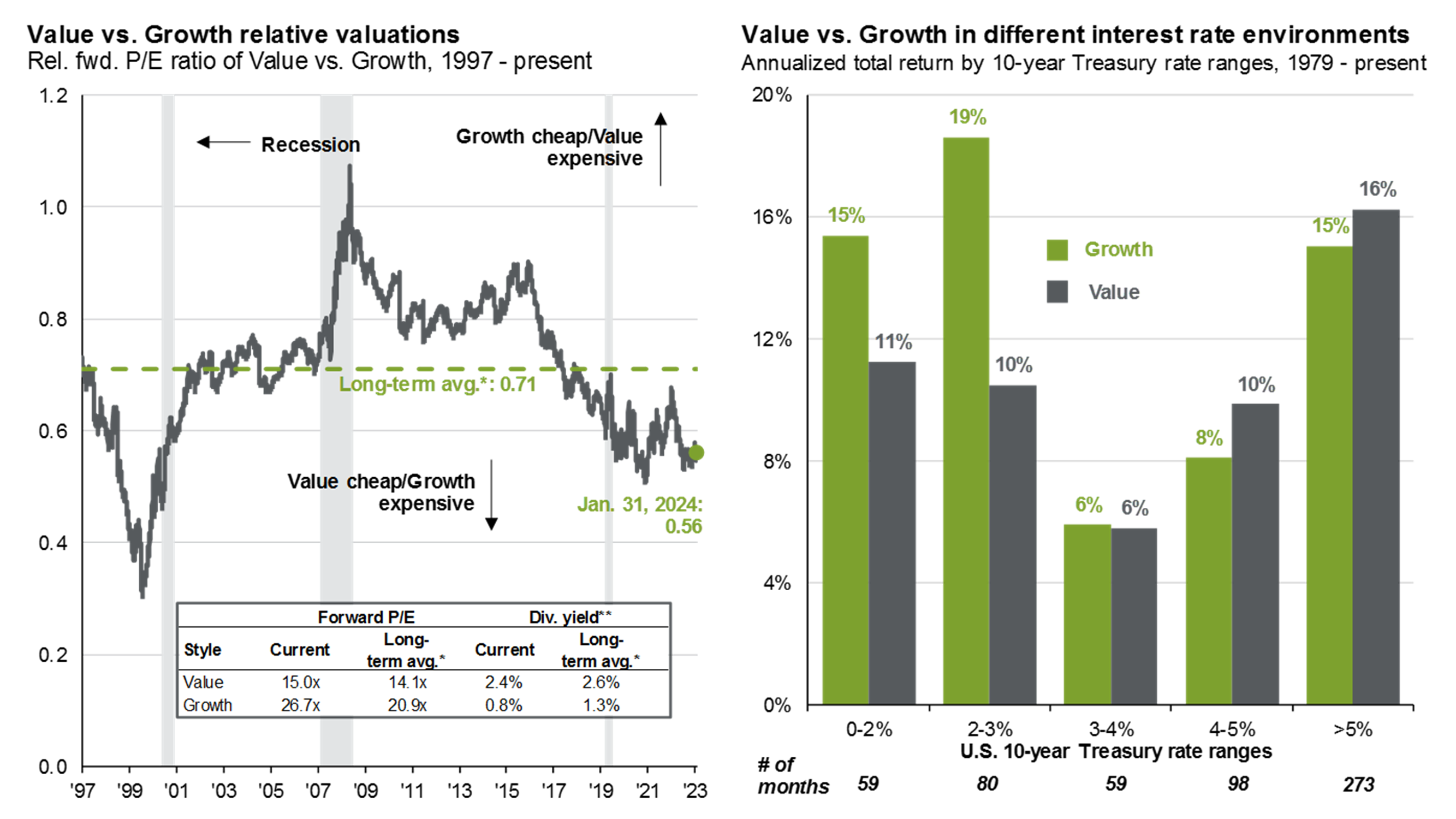

Moreover, we see that worth shares (power is an enormous a part of this) are buying and selling at a really engaging valuation in comparison with progress shares. That is very true if we assume that rates of interest stay larger for longer.

JPMorgan

Therefore, this text is about one of the crucial undervalued power shares on my radar. An organization that has develop into so low-cost that I consider it can present substantial returns the second the market begins to look into different areas past tech (rotation).

Because the title of this text gave away, that firm is the Canadian built-in oil and fuel big Suncor Power (NYSE:SU), the most important peer of my power funding, Canadian Pure Assets (CNQ).

My most up-to-date article on this Canadian firm was written on November 9, 2023, titled “Suncor Energy’s Shareholder Return Potential Is Impressive – 13% At $80 WTI.”

Since then, shares have returned 5.6%, together with dividends.

On this article, I will replace my bull case, utilizing its just-released earnings and new developments that bode properly for the Canadian upstream sector.

So, let’s get proper to it!

Suncor’s World-Class Property Pave The Street For Development

Suncor Power is corresponding to an organization like Exxon Mobil (XOM), as it’s an built-in oil and fuel firm, which means it additionally refines (downstream) oil into value-adding merchandise.

It combines upstream and downstream operations as a substitute of solely specializing in upstream like its peer, Canadian Pure.

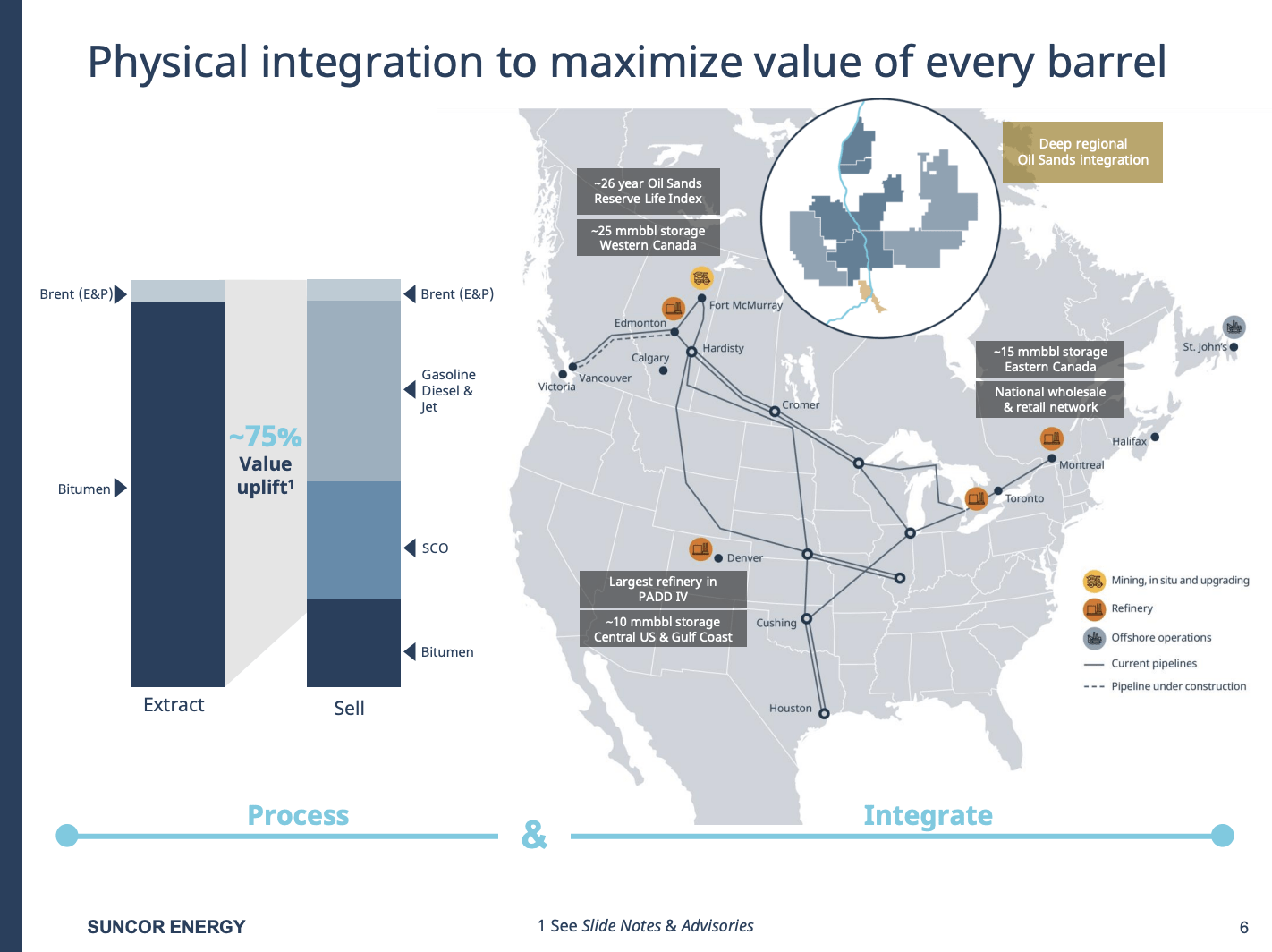

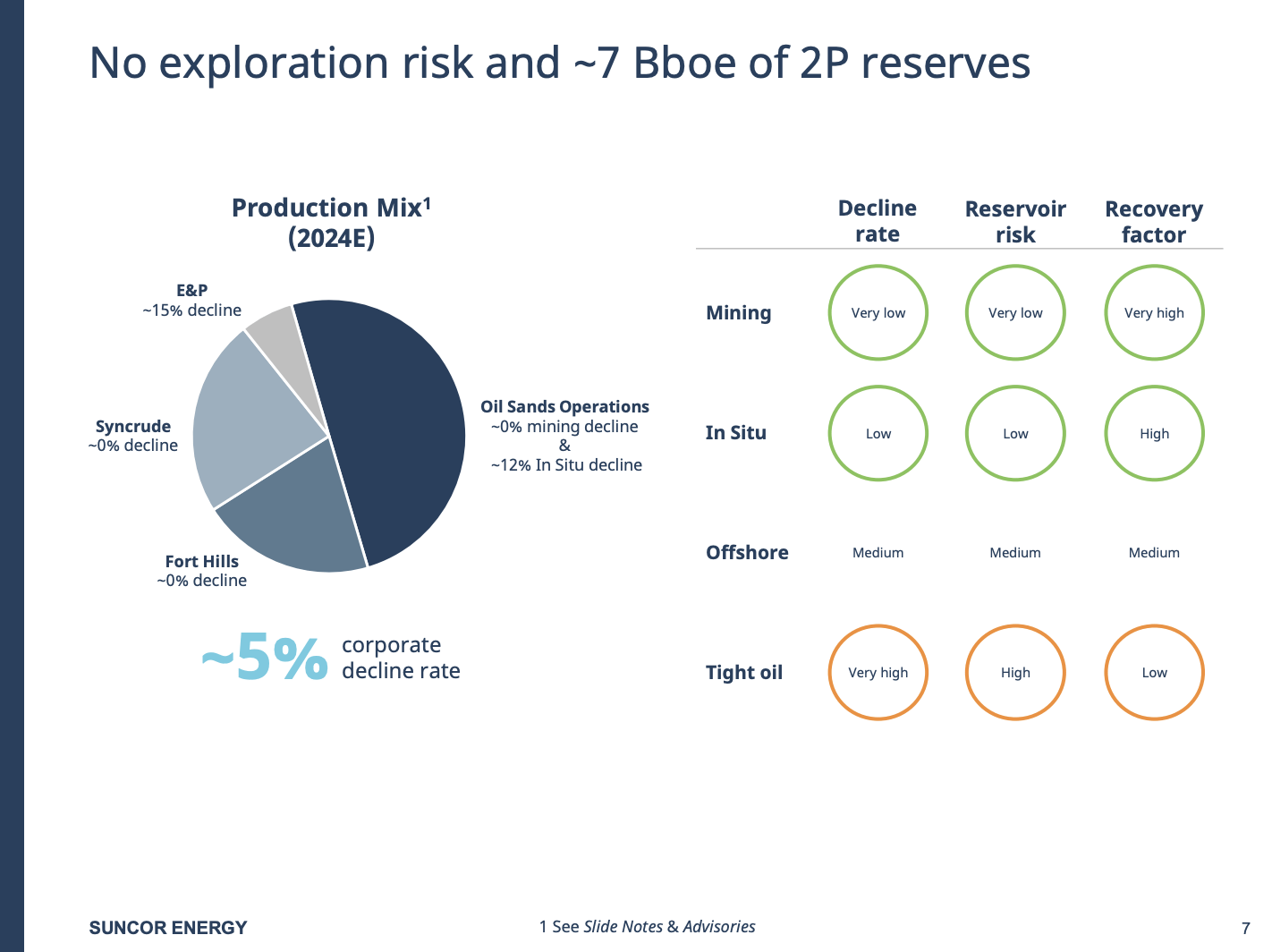

The corporate, which has main operations in Canada’s oil sands, has a reserve lifetime of 26 years, giving it one of many greatest reserves in the whole business.

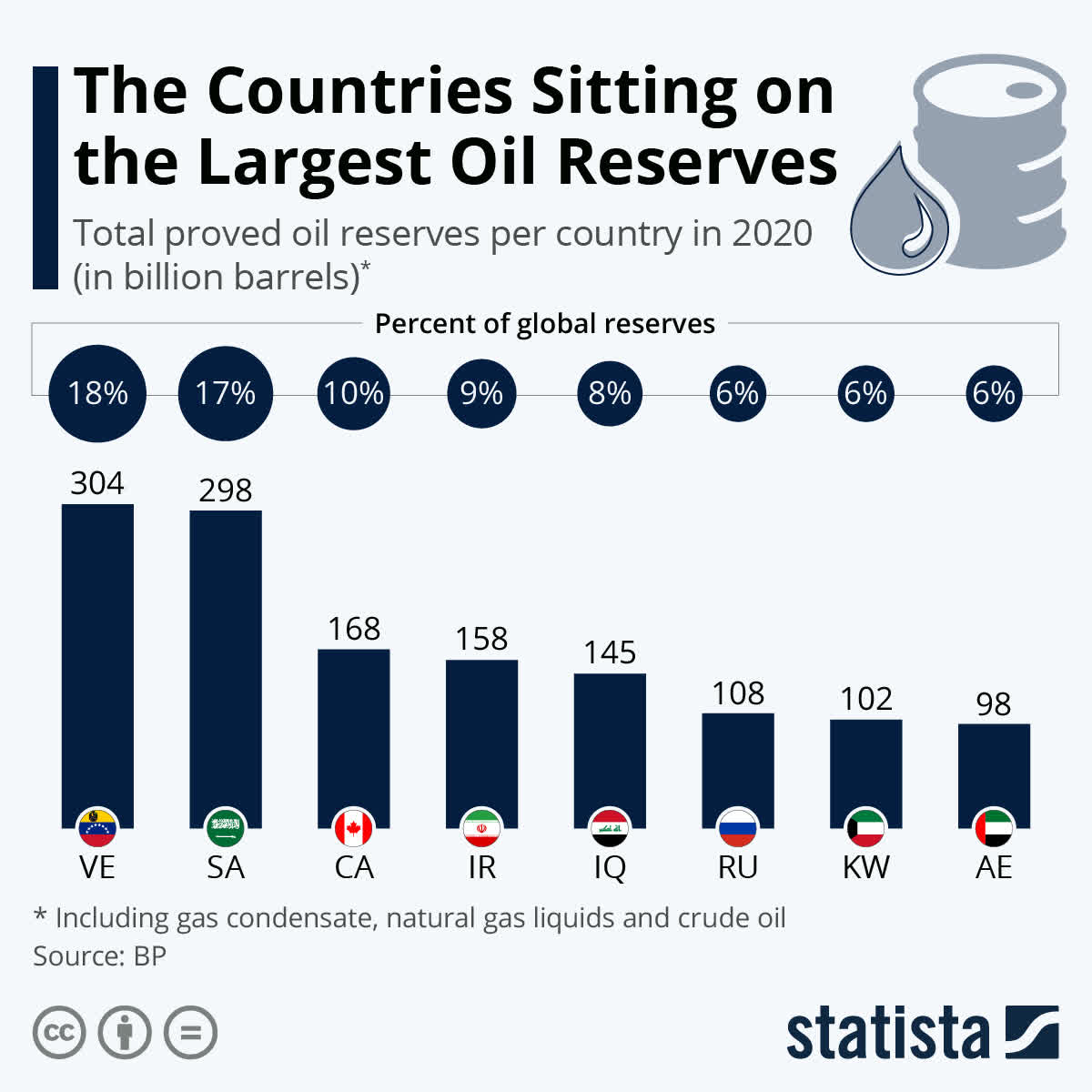

Normally, Canada is dwelling to a few of the world’s largest reserves. Utilizing 2020 numbers (which are nonetheless up-to-date), we see that Canada is dwelling to 10% of the world’s oil reserves. Most of those reserves are within the Western Canadian Sedimentary Basin (“WCSB”), the place SU operates.

Statista

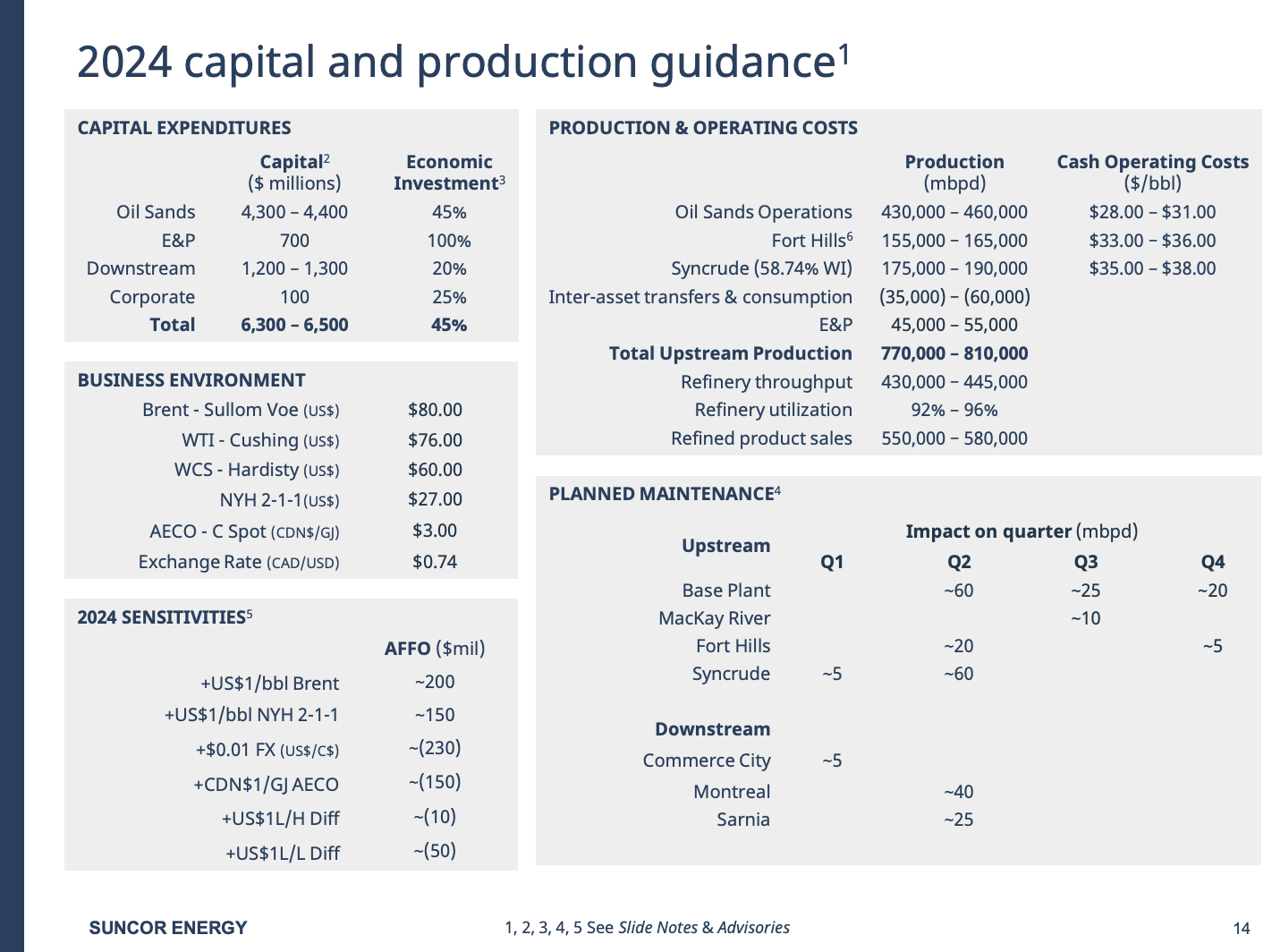

This yr, the corporate is predicted to provide between 770 and 810 thousand barrels per day. Greater than half of that is anticipated to come back from its oil sands operations.

On high of that, it’s anticipated to show between 550 and 580 thousand barrels per day of its manufacturing into refined merchandise this yr, with a refinery utilization fee of at least 92%.

Suncor Power

Actually, throughout its 4Q23 earnings name, the corporate famous that each upstream and downstream segments confirmed a powerful operational efficiency throughout the quarter.

For instance, upstream manufacturing reached 808 thousand barrels per day, which is the second-highest within the firm’s historical past.

Moreover, main achievements included record-breaking manufacturing in November and December, profitable completion of turnarounds at numerous amenities, and over 100% utilization on the Syncrude facility.

Furthermore, refining utilization stood at a powerful 98% within the quarter, with sturdy downstream margin seize pushed by larger realizations from seasonal diesel differentials.

Including to that, throughout the quarter, the corporate closed the acquisition of Complete Power Canada, which makes it the only real proprietor of Fort Hills.

That is what the corporate mentioned when it announced the acquisition of Complete Power Canada final yr:

With 100% possession of Fort Hills we’ll pursue alternatives to create extra worth by way of regional synergies and basinwide administration of our unparalleled, built-in oil sands asset base. This transaction is aligned with our technique to wholly personal and function long-life strategic belongings.

As we will see beneath, Fort Hills is predicted to provide as much as 165 thousand barrels per day, roughly a fifth of its complete manufacturing.

Suncor Power

It is also one of many firm’s premier belongings, with a 0% decline fee, which is another excuse why I like Canadian oil sands.

Primarily, there are two strategies to provide oil within the oil sands:

Floor mining: This technique recovers deposits lower than 75 meters (82 yards) beneath the floor.

In-situ: This technique makes use of steam injection to extract bitumen underground.

Therefore, the 0% decline fee refers back to the sustained manufacturing degree.

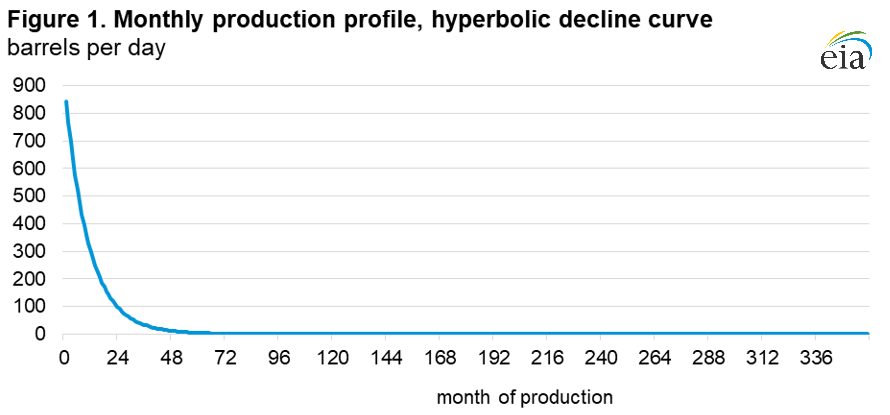

U.S. shale, for instance, has a decline fee of someplace between 10% and 20%, which means that present wells shortly lose productiveness, requiring producers to persistently drill new wells.

That is what the EIA wrote in March 2023, together with the graph that goes with this remark:

The decline curve converts from a hyperbolic decline to an exponential decline when the month-to-month decline fee falls to 0.8% (10% annual decline). An instance of a manufacturing profile utilizing a hyperbolic decline curve is proven in Determine 1.

Power Info Administration

The overview beneath reveals this comparability as properly, together with the truth that nearly all of Suncor’s manufacturing has a really low decline fee.

Suncor Power

These numbers additionally clarify why Suncor is ready to increase manufacturing by 6% this yr with out having to threat exploiting an excessive amount of high-quality stock.

On high of getting the “luxury” of not having to fret about elevated decline charges, the corporate is utilizing its operations to reinforce efficiencies (decreasing complete prices).

For instance, the variety of vehicles working autonomously has elevated from 31 to 45 prior to now three months, with plans to achieve 91 by the top of this yr.

The corporate goals to move 100% of ore on the Base Plant autonomously, with potential annual price financial savings of $1 million per truck per yr.

So, what does this imply for shareholders?

Deep Shareholder Worth

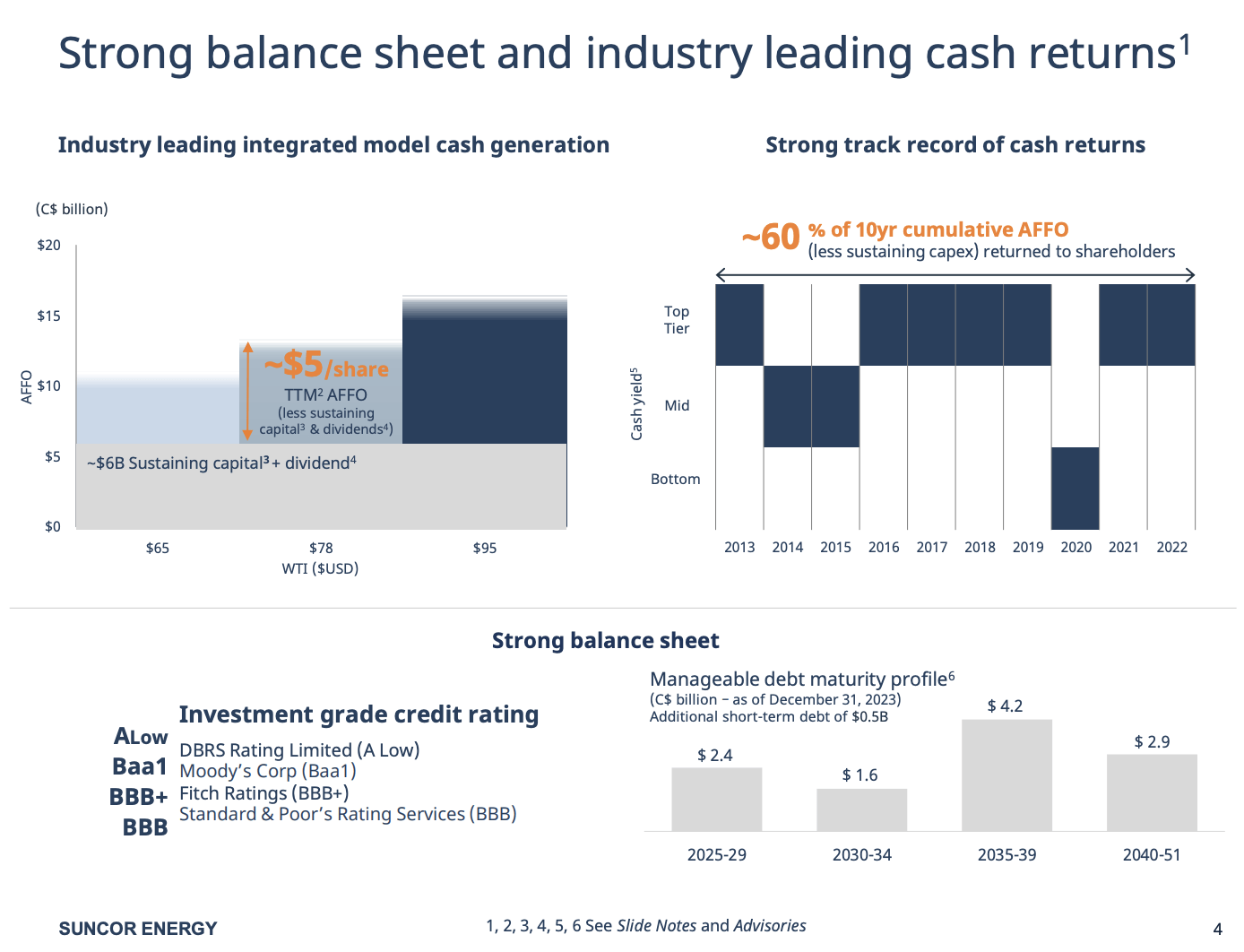

One of the vital vital issues to debate is the corporate’s means (and willingness!) to reward its shareholders.

For instance, throughout the fourth quarter, the corporate confirmed its dedication to shareholders by returning almost $1.1 billion, which included a 4.8% dividend hike and $375 million in buybacks.

The 4.8% hike was introduced on November 15 and brings the annualized dividend to $2.18 or 4.8% of its inventory value. Once more, I am utilizing CAD and Toronto-listed shares right here. The identical yield applies to U.S. shares as properly.

Nonetheless, dividend progress for buyers primarily based within the U.S. and different nations relies on the Canadian greenback.

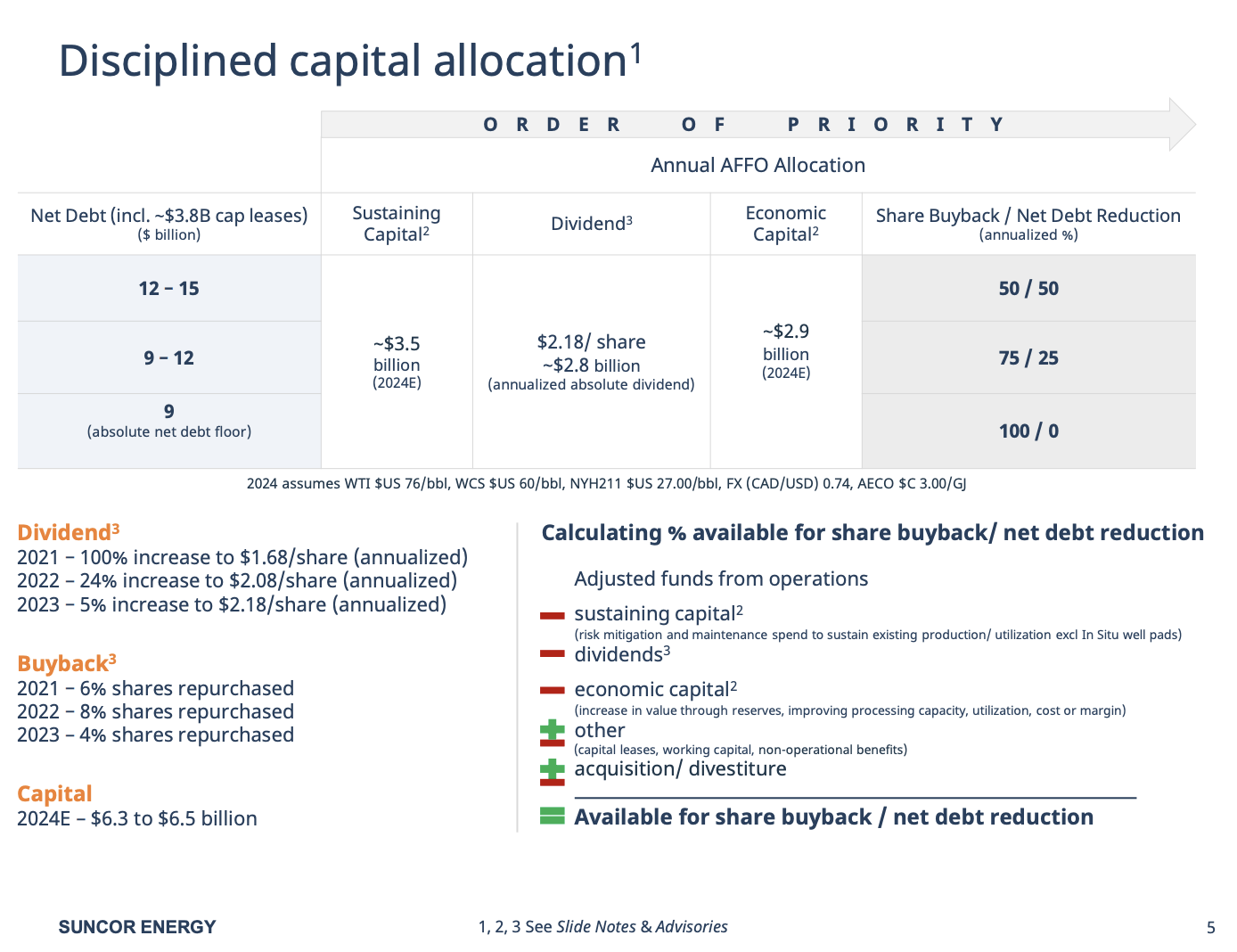

Including to that, regardless of the aforementioned closing of the acquisition of Complete Power Canada for CAD 1.5 billion, together with closing changes and prices, Suncor managed its web debt very successfully, which stood at $13.7 billion on the finish of the fourth quarter.

As I wrote in my prior article, the corporate ended the yr with web debt within the goal vary of $13.5 to $14.0 billion.

As soon as it lowers web debt to $9 billion, it plans on returning 100% of its free money movement to shareholders – primarily by way of buybacks. Under $12 billion, that quantity is 75%.

Suncor Power

Analysts anticipate the corporate to decrease web debt to $9 billion by the top of this yr, which suggests we’ll seemingly see a gradual shift in buybacks within the quarters forward – in favor of shareholders.

[…] our capital allocation construction is fairly clear. Once we hit $12 billion web debt, we go to 75, 25 buyback and discount. After which as soon as we get to $9 billion, and that could be a web debt foundation, together with capitalized leases. We’re centered on that framework. I believe to piggyback on Wealthy’s feedback, what we’re making an attempt to do is drive extra free money movement out of the enterprise so we will drive to these targets much more shortly. Now, clearly, it’s all going to be depending on the place commodity value lands, and other people will take various views of after we’re going to hit the $12 billion. However we’re centered on driving that debt down whereas persevering with to return money to shareholders. – SU 4Q23 Earnings Call

Moreover, to offer you an concept of how a lot capital the corporate can spend, it targets roughly $5 in per-share adjusted funds from operations after sustaining capital and dividends at US$78 WTI.

This suggests a complete potential payout yield of 11%, a quantity that ought to be capable of enhance exponentially if oil costs transfer larger.

Suncor Power

Having mentioned that, usually, I’d make the case that Suncor is not the only option for dividend-focused buyers.

Whereas it will not use particular dividends – at the very least not anytime quickly – I like that its base dividend is now shut to five%, which brings a implausible combine of standard quarterly dividends and buybacks to the desk.

The valuation is not unhealthy, both!

Valuation

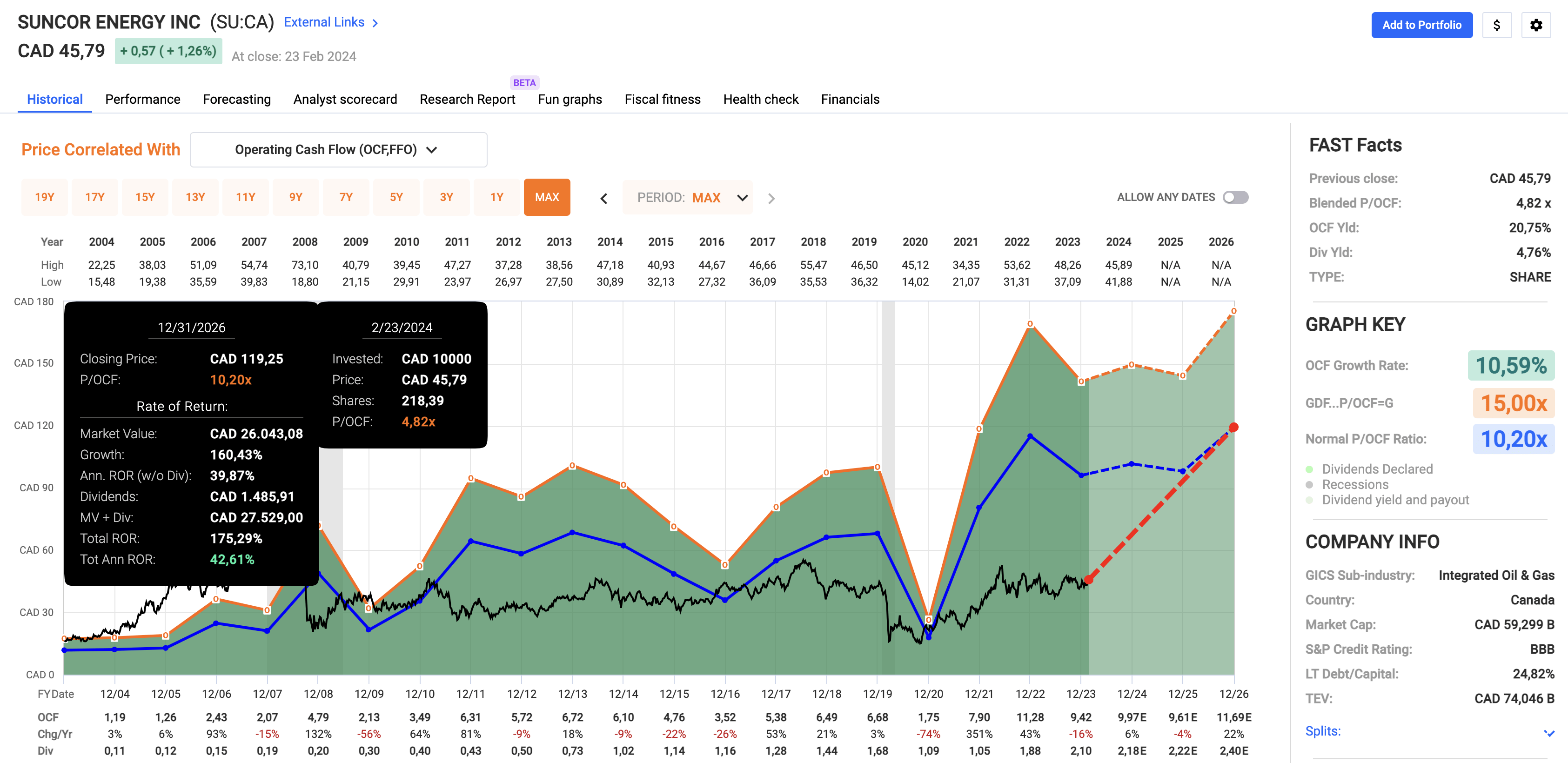

Suncor Power may be very low-cost.

Utilizing the P/OCF (working money movement) metric, the corporate is buying and selling at a blended a number of of simply 4.8x OCF, which is manner beneath its long-term normalized a number of of 10.2x OCF.

FAST Graphs

As analysts anticipate the corporate to generate roughly $11.70 in 2026E OCF, it has a theoretical truthful value of $119, primarily based on a ten.2x a number of.

This could suggest a 160% upside.

Whereas this can be a purely theoretical return, I do consider that SU is manner too low-cost.

Whereas I don’t disagree that tech/progress has been the higher place to be (till now), valuations are favoring power.

Regardless of financial pressures in Europe, China, and different areas, oil costs stay sturdy.

Even an 8x OCF a number of would suggest roughly 100% inventory value upside.

Particularly as soon as oil costs get cyclical tailwinds, I anticipate a rush towards beaten-down oil shares like SU. There’s simply an excessive amount of worth, in my view.

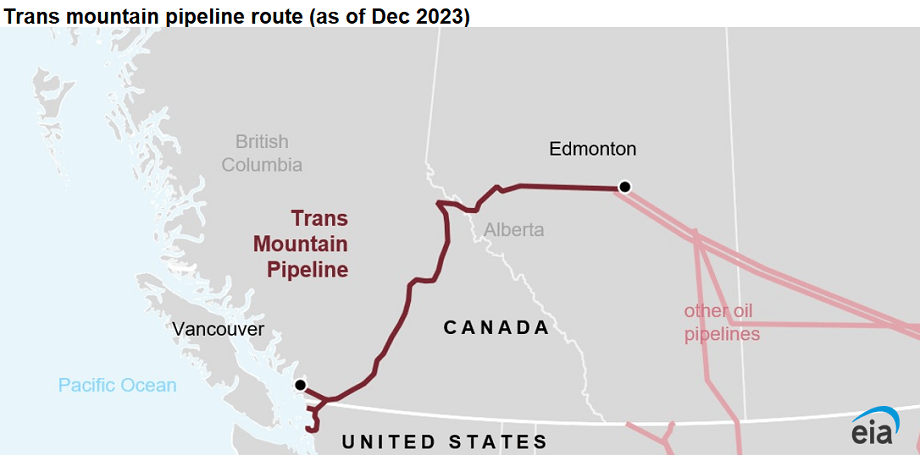

On high of that, the Trans Mountain Pipeline growth is near being accomplished.

Though it can shortly attain its limits once more, extra throughput will add important pricing advantages for Canada’s producers, enhancing margins for many WCSB-based producers.

All issues thought-about, I actually like SU and consider it can flip into one of many best-value shares for the following few years (and sure past).

The one cause why I’m not lengthy is that I’ve a place in its peer CNQ.

Takeaway

In a market of lofty valuations the place tech dominates, discovering worth elsewhere is vital.

Whereas many are fixated on the hovering tech sector, alternatives lie in undervalued sectors like power.

On this sector, Suncor Power stands out as a first-rate instance, with its strong operations and dedication to shareholder worth.

Regardless of its spectacular fundamentals and potential for important upside, SU stays undervalued, buying and selling at a mere fraction of what I consider to be its truthful value.

With favorable business dynamics and upcoming catalysts just like the Trans Mountain Pipeline growth, SU emerges as a compelling funding alternative.

Professionals & Cons

Professionals:

Deep Worth: Suncor Power presents a compelling alternative for worth buyers, buying and selling at a major low cost to its truthful value.

Sturdy Fundamentals: The corporate has world-class belongings and a diversified enterprise mannequin, together with upstream and downstream operations.

Shareholder Pleasant: SU has a powerful dedication to rewarding shareholders by way of dividend hikes and substantial buybacks.

Potential Upside: Analysts anticipate important upside potential for SU.

Business Tailwinds: Favorable business developments, together with doubtlessly elevated oil costs and upcoming pipeline expansions, bode properly for Suncor.

Cons:

Sector Volatility: Investing within the power sector comes with important volatility pushed by fluctuating oil and fuel costs.

Market Sentiment: Regardless of its intrinsic worth, SU’s inventory value could also be influenced by broader market sentiment.

Environmental Dangers: As an power firm, SU faces environmental dangers and regulatory scrutiny.

Forex Dangers: non-Canadian buyers like myself should be conscious that dividend funds are depending on the Canadian greenback.

Taxation: Canadian shares could also be taxed in another way than, for instance, U.S. C-Corps.