lnzyx

NetEase (NASDAQ:NASDAQ:NTES), initially an early web firm working a preferred area within the late 90s, at this time is a sprawling know-how firm working in a various vary of industries. Primarily although, it’s a recreation growth firm now with virtually 80% of the income generated by the broader gaming section. Latest regulatory issues precipitated a major drop in inventory value, adopted by a restoration which noticed all losses erased. The restoration will not be totally justified, however essentially the corporate is doing effectively and has a broad array of profitable video games in addition to a robust pipeline for the long run.

This autumn

For the quarter, income was up 7% YoY to $3.8 billion, whereas complete income for the yr additionally rose 7% to $14.6 billion. The video games section outperformed the common barely, up 9% yearly and This autumn up 10% YoY by way of income, the positive factors being attributed to the launch of Justice Cellular and continued success of Eggy Occasion. Youdao, which provides academic and translation centered providers, was solely up 2% YoY for the quarter, which is said to the continuing discount in sensible units gross sales courting again to Q3 as a part of a deliberate technique to enhance income long term. The music section in the meantime skilled a 13% FY income decline whereas profitability improved resulting in the primary full yr web revenue, and the progressive companies and others section noticed a 9% improve for the yr.

The Gaming Pipeline

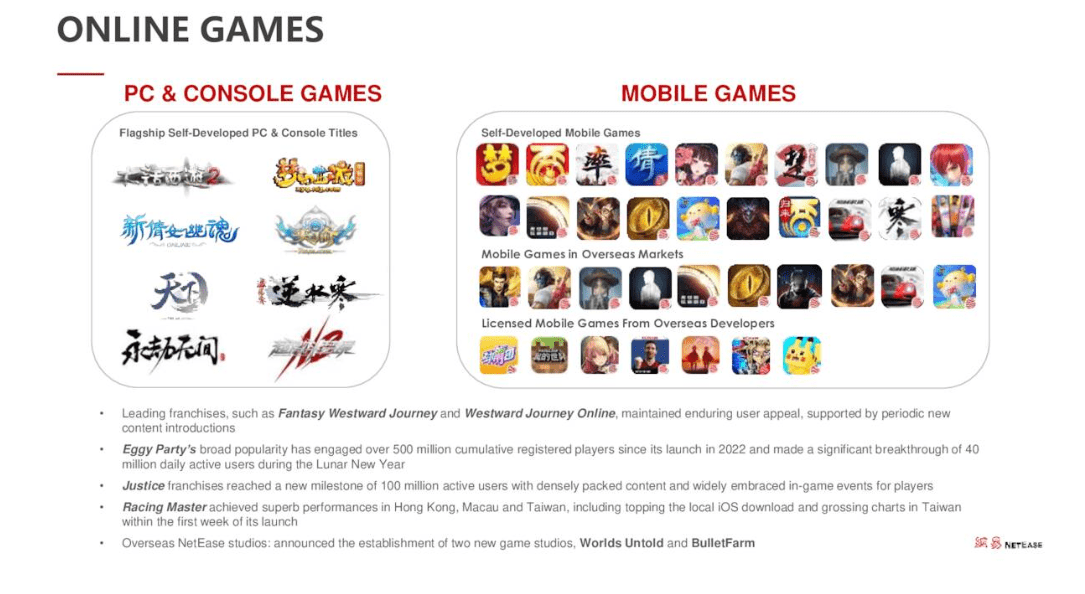

NetEase has a mixture of cellular and PC/Console video games however the majority of income comes from cellular with about 77% of the income share. Among the extra profitable present titles the corporate owns throughout each cellular and console embrace fashionable battle royale Naraka Bladepoint, the favored informal cellular recreation Eggy Occasion and MMORPG Fantasy Westward Journey. The pipeline of upcoming titles additionally holds a whole lot of promise, with a cellular model of Naraka Bladepoint due round Q2, The place Winds Meet, an open world martial arts recreation due later this yr in addition to She Diao Condor Hero, one other martial arts recreation primarily based on a preferred Chinese language novel.

One other sturdy possibility for progress is enlargement into the worldwide market which the corporate is has been endeavor quickly, growing titles for the worldwide viewers and establishing two new worldwide studios just lately, World’s Untold and BulletFarm. These studios are engaged on growing AAA titles, boasting expertise behind the Mass Impact and Name of Responsibility collection respectively. If even one in every of these new studios can develop successful, it might present a robust catalyst for progress in addition to helpful diversification each into western markets and the PC/console income break up. Present western titles embrace Lord of The Rings: Rise to Battle and Harry Potter Magic Woke up in addition to a few Marvel video games.

NetEase This autumn earnings

NetEase video games span many genres and they don’t seem to be overly reliant on a single title like some gaming corporations these days may be, so if the present technique to additional lengthen into western markets works then the corporate will show very enticing to traders searching for a gaming inventory with some security.

Gaming Laws

In December, NetEase was one in every of many Chinese language shares rattled by new draft guidelines introduced supposed to curb gaming time and spend by customers. The draft guidelines focused issues like day by day login bonuses, and rewards that incentivised ingame purchases, mechanisms which are pretty ubiquitous within the cellular gaming trade, in addition to NetEase’s personal video games. Since then, there was obvious backtracking, with one prominent regulator being dismissed and the proposed laws being faraway from the Nationwide Press and Publication Administration’s web site. Accordingly, the preliminary dip has since been erased, with the inventory at the moment buying and selling across the similar value as earlier than the announcement. Nonetheless, there stays appreciable uncertainty about what the subsequent steps will likely be and what the ultimate laws will entail, with a point of restrictions presumably nonetheless seemingly. The true concern right here is that within the medium time period extra information comes out about pending regulation and causes a renewed selloff.

Alternatively, one cause to suppose positively in regards to the course issues are headed on the regulatory entrance is that China has broadly come underneath some strain just lately by worldwide traders, inflicting the State Council to release an action plan to drive international funding. That is typically how issues have performed out with the CCP in recent times, regulatory strain ratchets up when the federal government feels the economic system is performing effectively, and lessens when it isn’t. From this angle, though seemingly counterintuitive, Chinese language shares which have regulatory issues might profit from Chinese language financial woes.

Youdao

Youdao (NYSE:DAO) is a blended bag by way of outlook. Offering academic providers like a web based dictionary, language studying apps and even AI tutors, the subsidiary is each uncovered to and utilising the present wave of AI disruption. On one hand, on-line advertising and marketing providers grew income to a document RMB474.1 million utilizing AI and translation charges attained 100% YoY progress as seen beneath.

Invoice Pang, This autumn name:

Our present LLM options, notably AI bots, proceed to obtain consumer acclaim, contributing to greater than 100% year-on-year progress within the translation substitution charges for 3 consecutive quarters.

Alternatively, there are compelling causes to suppose that each present and future LLM fashions pose a menace to academic and particularly translation service companies. LLMs are already virtually universally good at translating issues, particularly in extensively spoken languages like English and Chinese language. It might be anticipated then that even non-specialised LLMs being widespread ought to improve the availability of some of these providers (even when suboptimal) at low price, lowering the marketplace for some of these corporations.

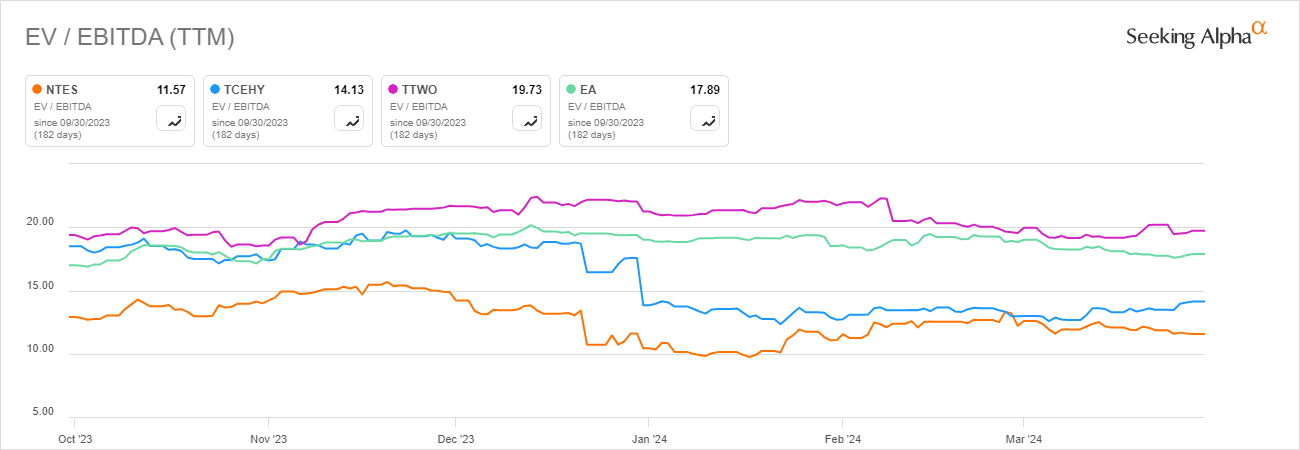

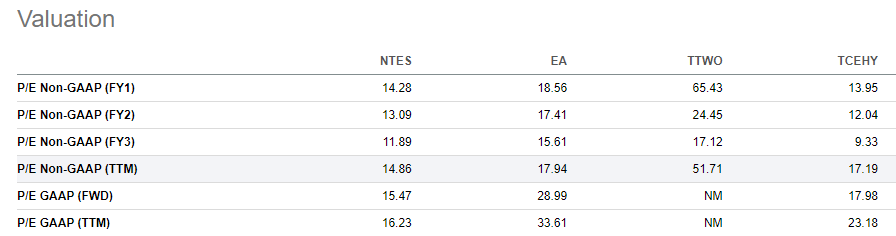

Comparative Valuation

NetEase trades at fairly low multiples in comparison with different gaming corporations, as seen beneath it has an EV/EBITDA of 11.57, decrease than the friends chosen. Among the many group NetEase additionally has the bottom P/E on each a trailing and ahead foundation. In fact, the decrease valuation of Chinese language shares partially explains this which is able to seemingly proceed for the foreseeable future.

Searching for Alpha

Searching for Alpha

Dangers

At first, as already addressed additional regulatory danger is well essentially the most urgent concern and is sufficient to closely weigh on my view at this value.

Failure to additional increase into the worldwide gaming market would even be problematic, there are essential variations between video games which are profitable in China in comparison with the west. Both the brand new studios overseas might fail, or video games which are profitable domestically will not be overseas for cultural or different causes.

The encroachment of AI capabilities on the interpretation and on-line studying providers that Youdao supplies can also be an imminent and fairly excessive chance danger, albeit comparatively low degree given the odds of complete income concerned.

Conclusion

NetEase has a powerful monitor document of hit video games in addition to a really promising line up of upcoming titles, with the potential for rather more enlargement into western markets. Nonetheless, the regulatory danger, whereas seemingly lowered in severity, is not at all erased though the inventory is buying and selling as whether it is. This raises questions on getting into at this value for my part, within the medium time period if there’s extra of a value correction a re-evaluation could also be warranted.