Giuliano Benzin

Netflix’s (NASDAQ:NFLX) deal so as to add WWE programming needs to be a pleasant elevate for the agency, however the inventory is trying fairly near pretty valued in the meanwhile.

Firm Profile

NFLX is a streaming service that gives TV collection, movies, and video games to its subscribers throughout numerous genres and languages. The corporate has over 260 million paid subscribers in over 190 international locations.

Its income primarily comes from month-to-month membership charges. It additionally makes a small quantity on promoting. NFLX produces its personal unique content material, in addition to licenses content material from third events.

Alternatives & Dangers

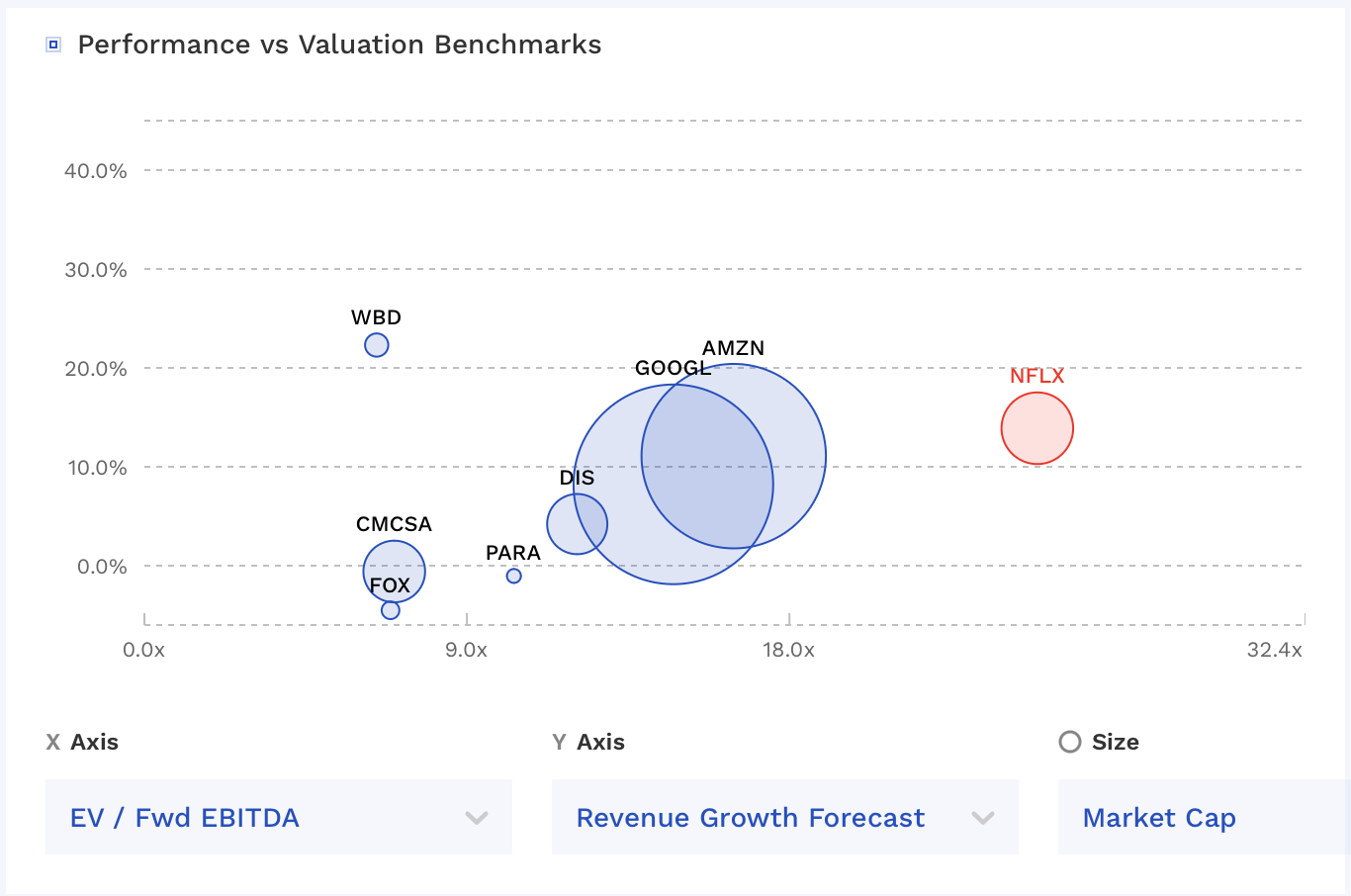

The streaming trade has been in flux over the previous few years, as conventional media firms with massive linear property have been shifting to streaming. For many of those firms, this has been a troublesome transition. It began with a push to usher in subscribers and create robust content material, whereas extra lately these firms have been trying to make these efforts worthwhile. Nonetheless, amongst Disney (DIS), Comcast (CMCSA) with Peacock, Paramount World (PARA) and Warner Bros. Discovery (WBD), solely the latter seems like its streaming service could also be EBITDA optimistic in 2023, and simply barely (~$200 million although the primary 9 months of 2023).

Regardless of the elevated competitors in streaming, NFLX has confirmed it may be a properly worthwhile enterprise. For 2023, the streaming big generated EBITDA of round $7.3 billion and free money move of $6.9 billion.

The enterprise can also be nonetheless rising properly regardless of NFLX’s measurement and elevated competitors. Income accelerated in 2023 to 12% from 6% in 2022, whereas it grew its paid memberships by almost 13% in the course of the yr to 260.28 million. Even in its extra mature U.S.-Canada market, it added 2.81 million memberships, in This fall, whereas Europe continues to be its largest progress market, including 5.05 million memberships within the quarter.

A part of NFLX’s success in 2023 was as a result of its crack down on shared accounts. It added options and plans to monetize account sharing, which labored. Nonetheless, this increase is now behind the corporate.

Going ahead, although, NFLX nonetheless has a variety of progress alternatives. The expansion of its ad-supported tier stays an enormous alternative. Its advert enterprise remains to be small, however 40% of recent subscribers are selecting this feature in supported markets. The corporate noticed 70% sequential progress in advert memberships in This fall. In the meantime, it would retire primary plans within the U.Okay. and Canada later this yr, pushing members to this extra worthwhile tier. On the identical time, as NFLX will get extra subscribers of its advert tiers, will probably be capable of higher scale and monetize the enterprise. It must also proceed to see enhancements in advert concentrating on and measurement down the road, which can even assist.

NFLX has additionally proven pricing energy through the years. And whereas some subscribers complain and a few do finally cancel, this has additionally been a lift to the corporate up to now. Given its tiered choices, together with advert supported choices, the corporate ought to be capable of retain extra clients when it decides to extend costs, as some will simply transfer to a lower-priced ad-supported choice.

One other large potential driver in 2025 would be the introduction of WWE content material on the streaming service. Beginning January 2025, NFLX will turn out to be the unique house to WWE’s flagship program Uncooked within the U.S., Canada, U.Okay. and Latin America. Different international locations are anticipated to be added later. In the meantime, NFLX can even function house to different WWE programming and premium reside occasions outdoors the U.S. in 2025 as nicely.

Discussing the deal on its Q3 earnings call, co-CEO Ted Sarandos stated:

“I’m going to say instead that we are thrilled to bring this WWE Live programming to our members around the world. WWE Raw is sports entertainment, which is right in the sweet spot of our sports business, which is the drama of sport. Think of this as 52 weeks of live programming every week — every year. It feeds our desire to expand our live event programming. But most importantly, fans love it. For decades, the WWE has grown this multigenerational fan base that we believe we could serve and we can grow. We believe that WWE has been historically under-distributed outside of North America. And this is a global deal. So, we can help them and they can help us build that fandom around the world. And I should add that this should also add some fuel to our new and growing ad business. We’re very excited about this deal.”

Adore it or hate it, the scripted sports activities leisure packages that WWE present have an enormous world viewers. Within the U.S., Uncooked tends to attract between 1.5 to 2.0 million viewers every week. WWE additionally has an enormous worldwide following. For instance, Saudi Arabia pays WWE a reported $50+ million for every reside occasion they host within the nation.

WWE has considered one of its most stacked rosters in a very long time with the current returns of CJ Punk and Randy Orton that would enhance fan curiosity. These are additionally principally reside occasions that attract large audiences and a variety of advertisers as nicely. I’d count on that this deal will assist add subscribers each within the U.S. and overseas, however the promoting aspect could also be much more enticing, and will help as the corporate scales up this a part of its enterprise.

In the meantime, NFLX ought to proceed to learn from the continued development of twine slicing. Whereas it could have slowed, this dynamic remains to be occurring. In the meantime, as reside sports activities and occasions transfer to streaming providers, it may hasten it much more.

Gaming can also be one other nascent space for NFLX. That is very small in the meanwhile, however may turn out to be a progress driver sooner or later.

Relating to dangers, saturation in some markets is considered one of them. Netflix has 80 million memberships within the U.S. and Canada, whereas there are an estimated over 131 U.S. households and round 16 million Canadian households. That’s over 50% of U.S. households which have NFLX, so progress needs to be extra of a grind on this market.

And whereas NFLX has run circles across the competitors, it’s nonetheless a threat. Anticipate some continued consolidation within the house as conventional gamers look to scale their companies and higher compete. NFLX has a bonus with no linear legacy property, however these firms are working arduous to make this transition to streaming, together with trying to transition sports activities over to their streaming providers.

With solely month-to-month memberships, the economic system may add threat. When instances get powerful, subscribers can definitely use ways comparable to transferring from one service to a different every month to avoid wasting prices. And as promoting turns into greater, that comes with its personal macro-sensitive dangers.

Valuation

NFLX presently trades at simply above a 26x 2024 EBITDA estimates of $9.9 billion. Based mostly on the present 2025 EBITDA consensus of $11.9 billion, the inventory trades at just below a 22x a number of.

Income is projected to develop almost 14% in 2024 and 12.6% in 2025.

NFLX presently has a free money move yield of about 2.8% primarily based on FCF of $6.9 billion within the final trailing twelve months.

NFLX is the most costly media firm, though it doesn’t have the linear TV legacy problems with lots of its rivals.

NFLX Valuation Vs Friends (FinBox)

On a subscriber foundation, NFLX trades at $1,000 per subscriber. ($260 billion EV and 260 million subscribers). ARPU is about $136 a yr. With about 41.5% gross margins, that’s an enormous worth for its buyer base for my part.

I’d worth the corporate between 20-25x 2-25 EBITDA given its progress and management place. That locations a $515-$650 worth vary on the inventory, with the center round $582.50.

Conclusion

NFLX reported a robust This fall, displaying it stays the dominant participant in streaming. In the meantime, the corporate remains to be within the early innings of its supported tier, which ought to assist drive subscriber additions, as nicely turn out to be extra worthwhile over time because it scales this a part of the enterprise.

The WWE deal, in the meantime, performs properly into this, and I feel it ought to assist give it extra scale in promoting given its 1.5-2.0 million weekly viewership numbers. On the identical time, I feel it ought to assist in worldwide markets the place wrestling may be very fashionable.

That stated, given its present valuation, even with the potential of some outperformance to the consensus numbers, the inventory seems fairly near pretty valued in the meanwhile. I’d be extra within the inventory across the $500 stage.