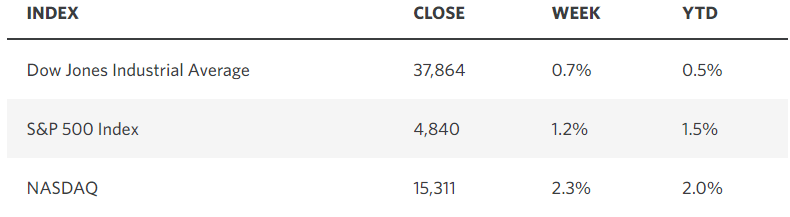

8vFanI

Final week, the S&P 500 joined the Dow Jones Industrial Common in reaching a brand new all-time excessive. In June of final 12 months, I advised traders to anticipate bettering market breadth, disinflation, and a continuation of the growth to lead to a new all-time excessive for the S&P 500 inside 6-12 months. It took simply seven, however bears are nonetheless questioning the validity of this accomplishment, pointing to the truth that only a few sectors of the index have achieved new all-time highs and that the renewed narrowing of breadth this 12 months is a type of weak point or instability. That appears like bitter grapes. New all-time highs are sometimes a bullish signal, and breadth has improved dramatically since June. One other spherical of bettering breadth is the place the alternatives lie.

Edward Jones

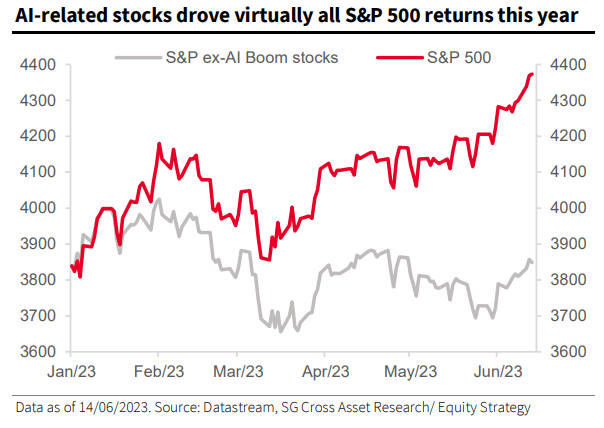

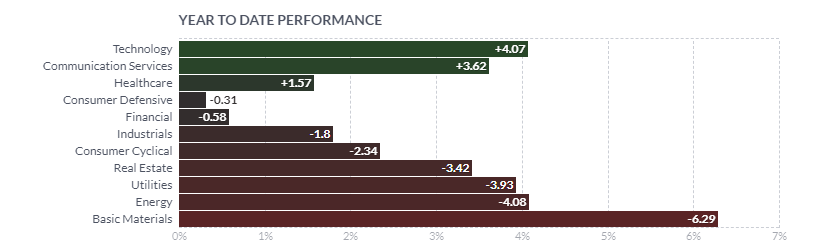

A part of final summer time’s bearish narrative targeted on the actual fact that know-how shares associated to synthetic intelligence (AI) had been chargeable for all of the year-to-date good points within the S&P 500. At first blush, that gave the impression of a unfavorable growth, and it was uncooked meat for these trying to feed their affirmation bias that the bear market was not over. But historical past steered this was not as ominous a growth as bears would have us assume.

Barron’s

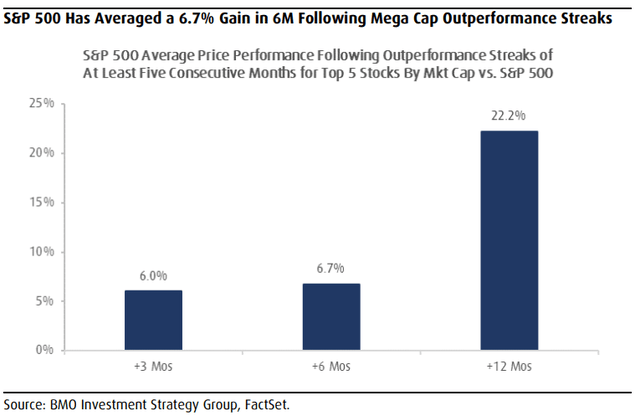

When the 5 largest firms within the S&P 500 outperform the index for 5 months or longer, as they’d final June, the S&P 500 goes on to outperform for the next three-, six-, and 12-month durations. The S&P 500 is up roughly 11.5% since I shared the chart beneath with traders final June. The one anomaly was within the 12 months 2000, however that was the exception and never the rule.

Bloomberg

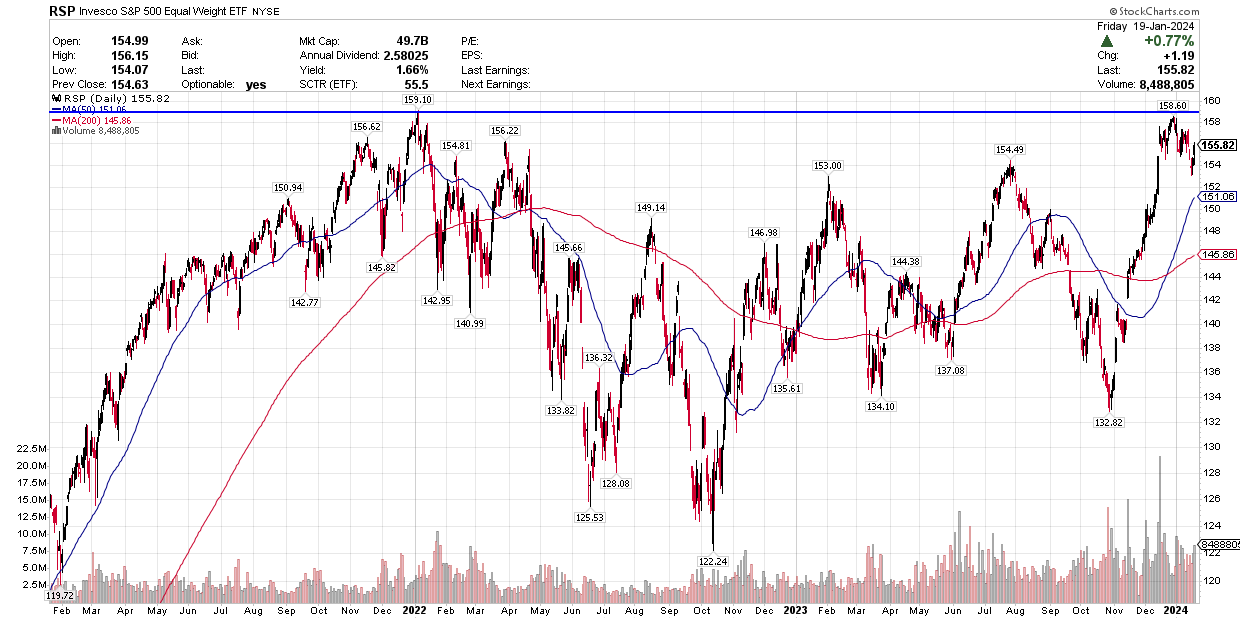

Moreover, the equal-weighted S&P 500 has improved its efficiency dramatically since then and now stands very near its all-time excessive achieved in January 2022. This index eliminates the affect of the highest 5 firms, in addition to the Magnificent 7.

StockCharts

Granted, we’re seeing know-how dominate sector efficiency once more on a year-to-date foundation, however I anticipate the continued interval of consolidation for the inventory market, which is extra seen within the S&P 500’s equal-weighted model, to result in one other enchancment in breadth.

Finviz

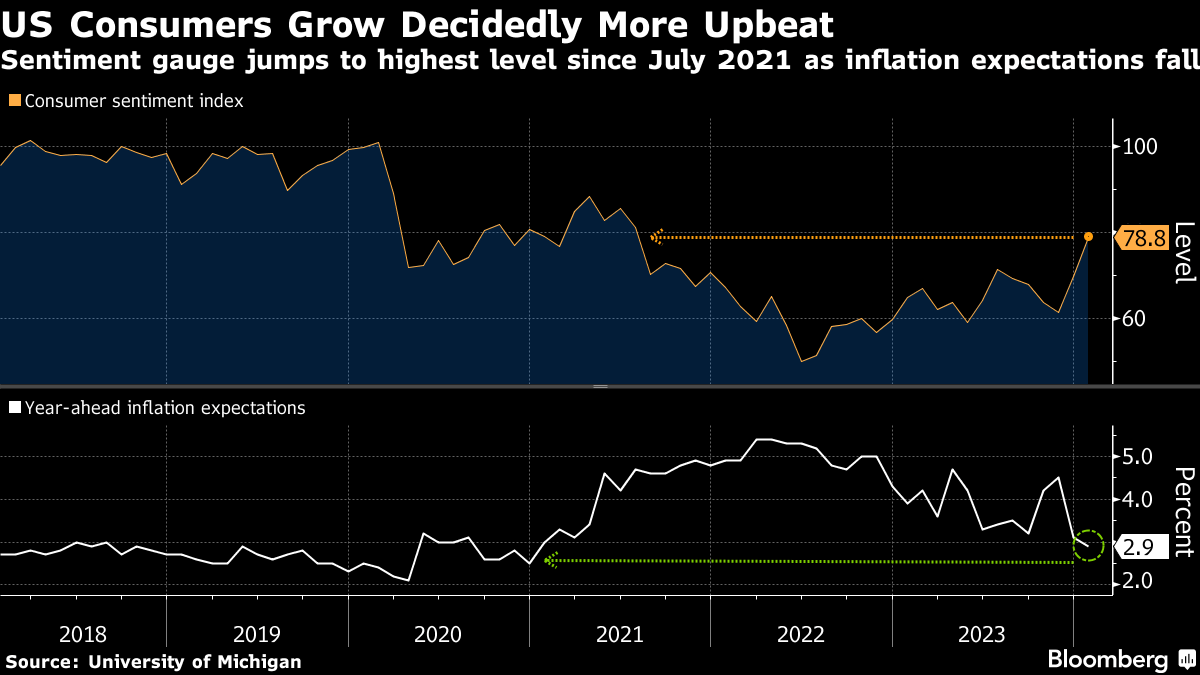

Final week’s financial knowledge moved us nearer to the comfortable touchdown that threat asset costs have began to replicate over the previous three months. The headline numbers for labor and shopper spending regarded sturdy, which has raised doubts for some concerning the want for fee cuts by the Fed, however the finer particulars behind each present we’re on observe for decelerating charges of progress. We want a interval of sub-trend progress within the financial system to lastly obtain secure costs. It’s such a positive line between progress and contraction that the high-frequency financial knowledge will proceed to offer fodder for each bulls and bears. It’s uncommon that we see one quantity that’s pure Goldilocks, however final week’s shopper sentiment report for January from the College of Michigan met that mark.

The index rose to a two-year excessive with customers broadly extra assured about their incomes, present monetary state of affairs, and their future monetary state of affairs. On the identical time, their expectation for value will increase over the following three years declined from 3.1% to 2.9%. This can be a well timed report prematurely of the Fed’s subsequent assembly.

Bloomberg

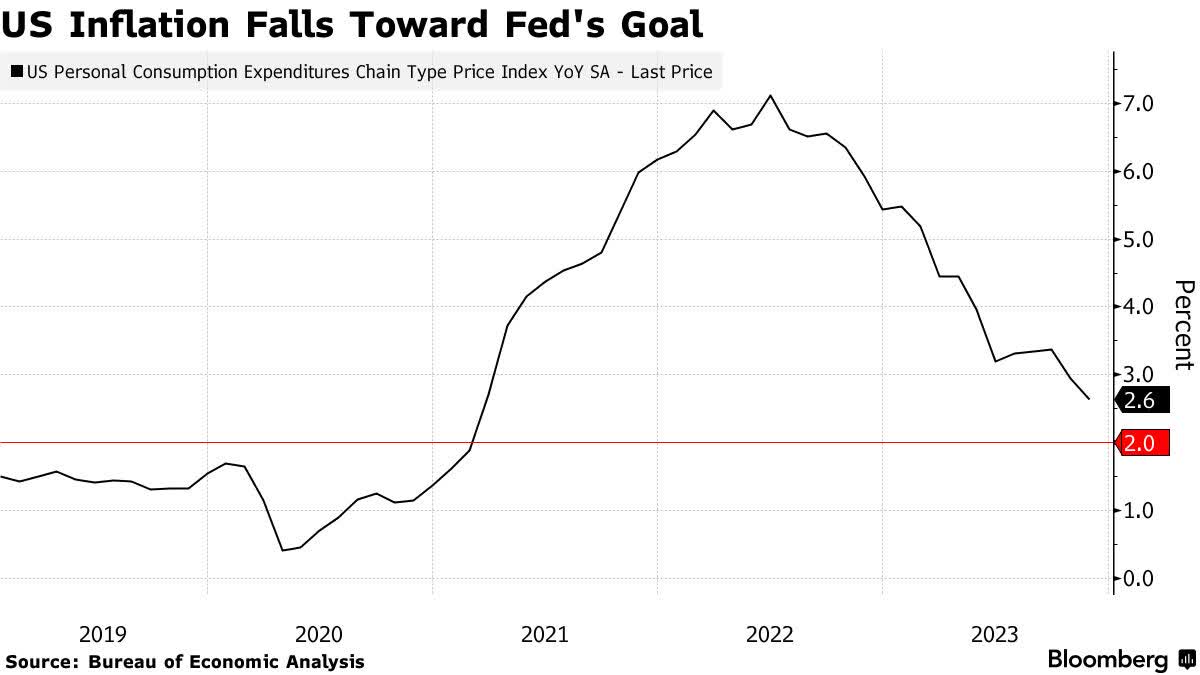

Market pundits proceed to say, together with Fed officers, that the Fed won’t begin to ease financial coverage till it is rather near its 2% inflation goal. That is as nonsensical as saying that the Fed ought to have waited till inflation was near peaking at 9% earlier than it began to tighten financial coverage, which it did. The primary-rate enhance was in March 2022, and the Shopper Value Index was 8.5% a month later. Right this moment, the Fed’s most well-liked measure of inflation (PCE value index) has fallen to 2.6%, and the core fee rose simply 1.9% on a six-month annualized foundation. I perceive Fed officers espousing hawkish rhetoric to keep away from fueling higher-risk asset costs, however I additionally assume they do not wish to make the identical mistake twice with regards to coverage. The Fed ought to begin step by step reducing charges in March.

Bloomberg

I believe the foremost market averages might be range-bound over a lot of the following two months, churning inside a channel, as traders rotate between sectors and shares, and the hole between what Fed officers say they are going to do collides with investor expectations. The 2 are very far aside at present. This Friday’s PCE report might be essential in that equation. The expectation is that the headline quantity might be flat at 2.6%, whereas the core falls from 3.2% to three%. The Fed is projecting each to fall to 2.4% by the tip of this 12 months, however we should always understand that quantity properly prematurely.