8vFanI

Enterprise Growth Firms, often called BDCs, have been reaping the rewards of upper rates of interest over the previous yr and a half, on account of the truth that their investments normally characteristic floating charges, whereas their borrowings have a excessive % of mounted charges.

As you may see within the Earnings part of this text, New Mountain Finance (NASDAQ:NMFC) had sturdy earnings development in 2023.

Firm Profile

NMFC makes a speciality of immediately investing and lending to center market firms in defensive development industries. The fund prefers investing in buyout and center market firms, with EBITDA between $10 million and $200 million.. It additionally makes investments in debt securities in any respect ranges of the capital construction together with first and second lien debt, unsecured notes, and mezzanine securities.

NMFC went public in 2011. It’s externally suggested by New Mountain Capital, a worldwide funding agency with roughly $45 billion of property underneath administration.

Holdings

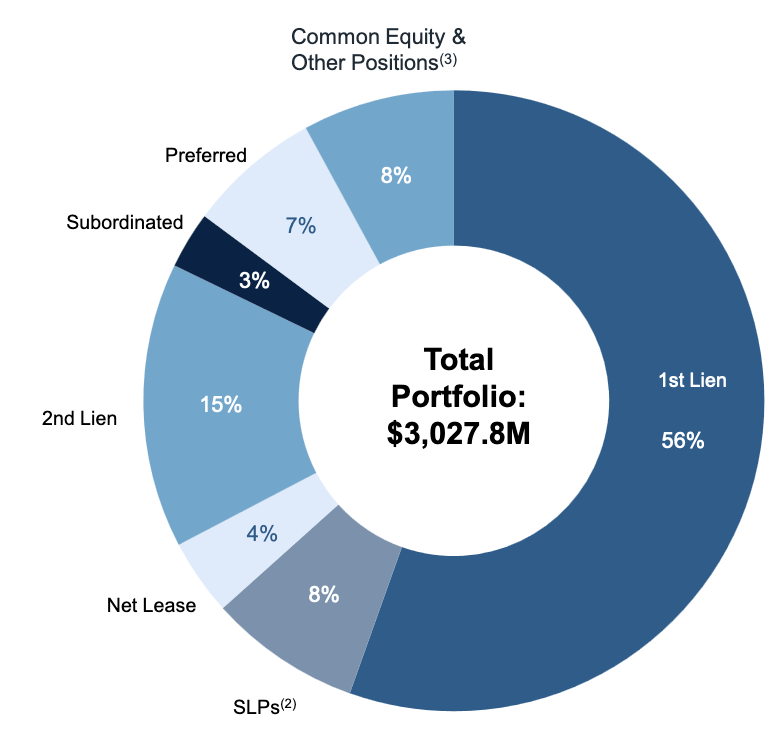

1st Lien, 56%, and 2nd lien loans, 15%, dominate the $3B portfolio, which additionally has holdings in Widespread Fairness, 8%; Most well-liked Fairness, 7%; Particular Loans, 8%; Internet Leases, 4%; and Subordinated Loans, 3%.

NMFC website

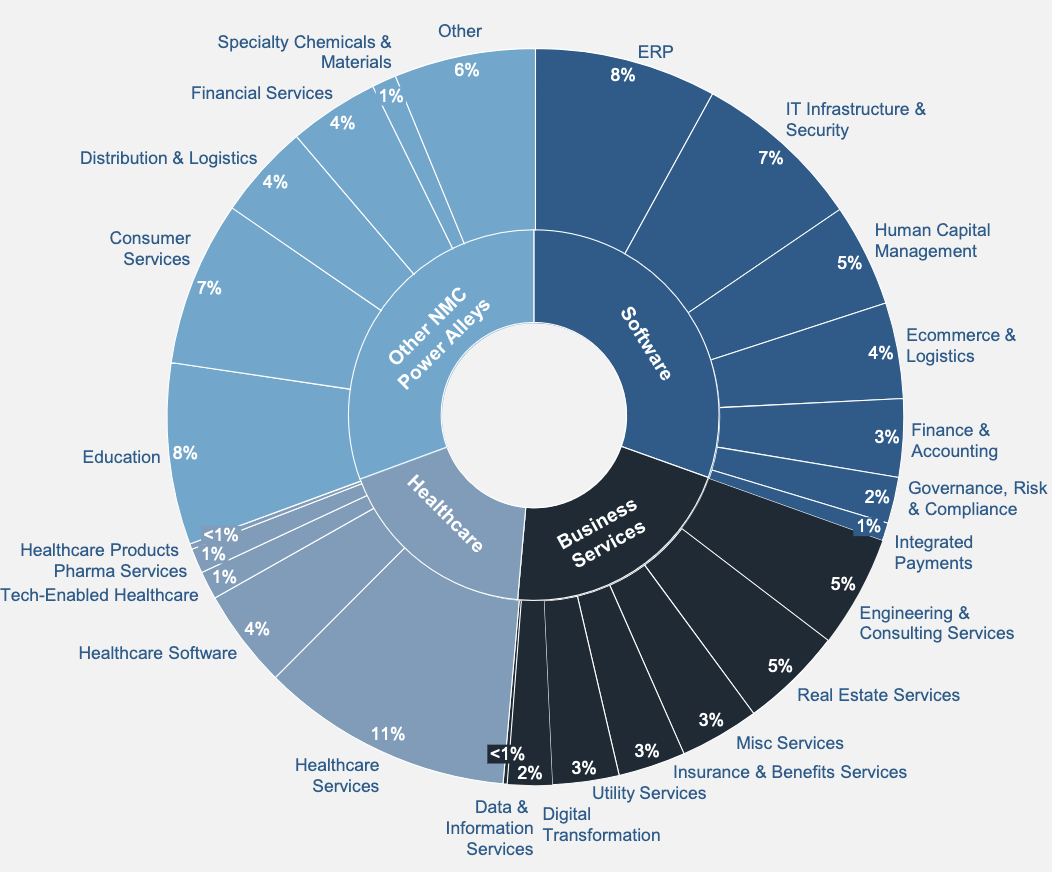

NMFC favors investing in non-cyclical industries – its predominant 3 sectors are Software program, Enterprise Companies, and Healthcare, but additionally has publicity to a various group of different industries, reminiscent of Schooling, Shopper Companies and Specialty Chemical substances:

NMFC website

Portfolio Firm Scores

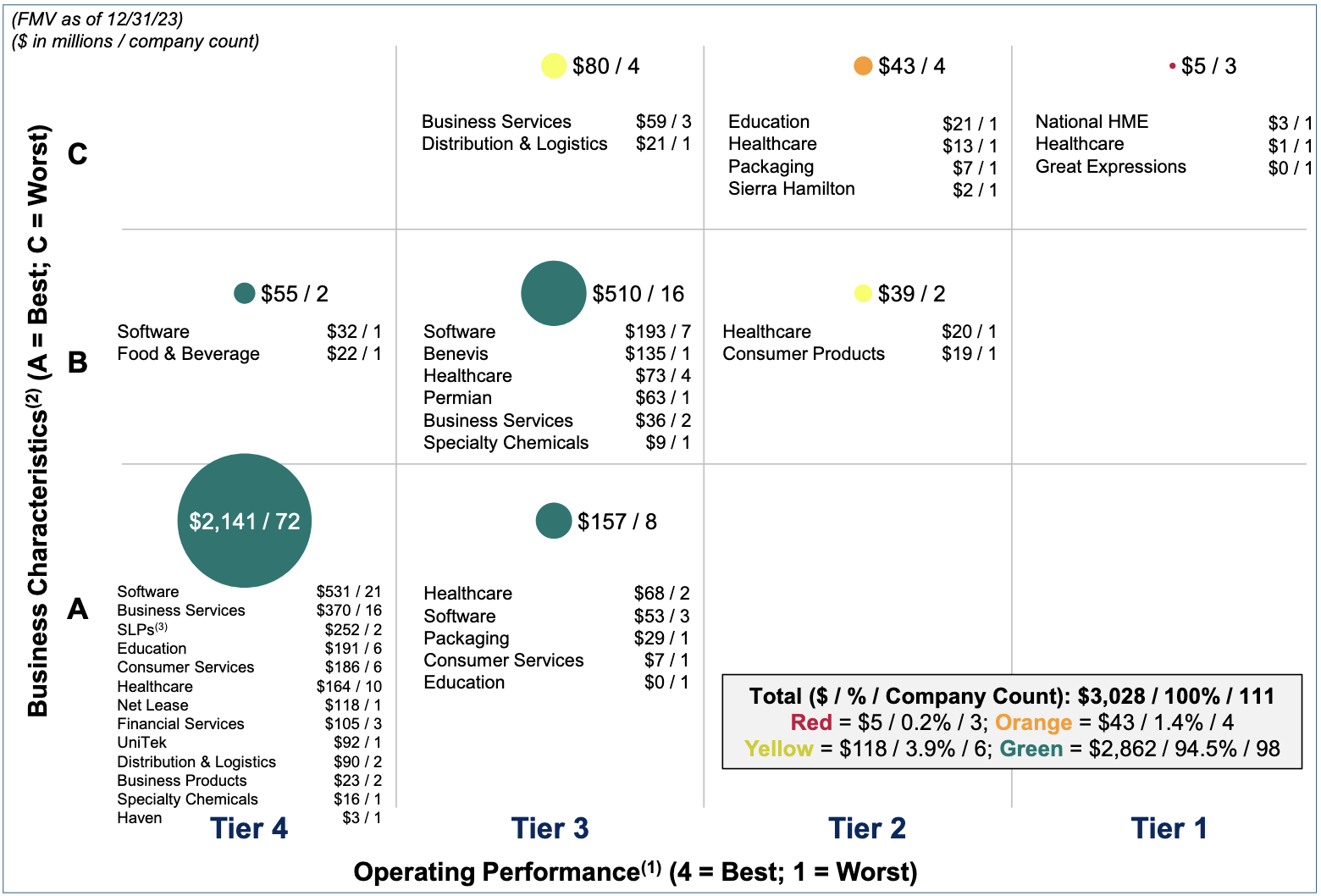

Like different BDC’s, NMFC re-rates its holdings each quarter- it makes use of a 1 to 4 tier system, with 4 being the very best and 1 being the worst for working efficiency. Additionally they fee the businesses’ enterprise traits on an A (finest) to C (worst) scale.

Administration supplies quantity of element on the present credit score efficiency developments for its holdings, itemizing trade, truthful worth and firm rely for every tier.

Of its 111 held firms, 74 have been within the prime tier, with a good worth of $2.196B, representing 73% of the portfolio; adopted by 28 in Tier 3, valued at $747M, 25% of the portfolio. Tier 1 had simply 3 firms, valued at $5M.

On a enterprise traits foundation, 98 A-rated firms represented 94.5% of NMFC’s portfolio, as of 12/31/23.

Positions representing $27M improved of their rankings, whereas positions representing $1M worsened in This fall ’23.

NMFC website

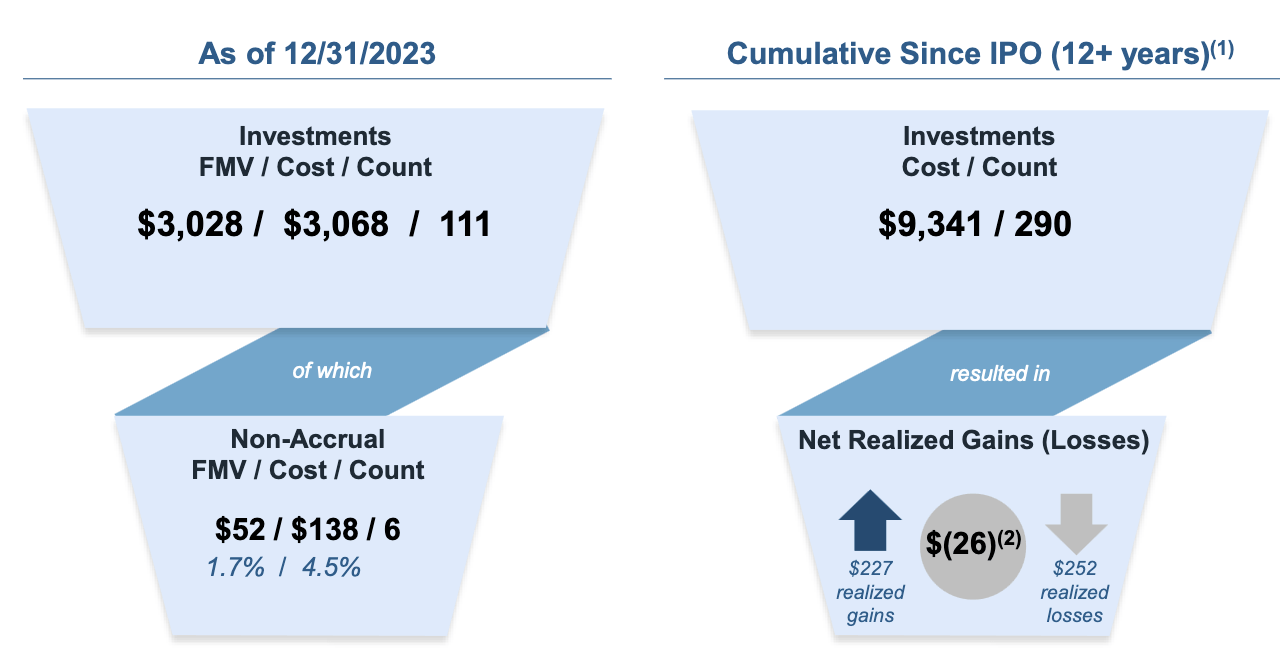

NMFC has 6 firms on non-accrual, with a good worth of $52M, 1.7% of its portfolio, representing a possible $86M loss vs. price. It has had $227M in realized positive aspects, vs. $252M in realized losses, for a web -$26M since its Might 2011 inception:

NMFC website

Earnings

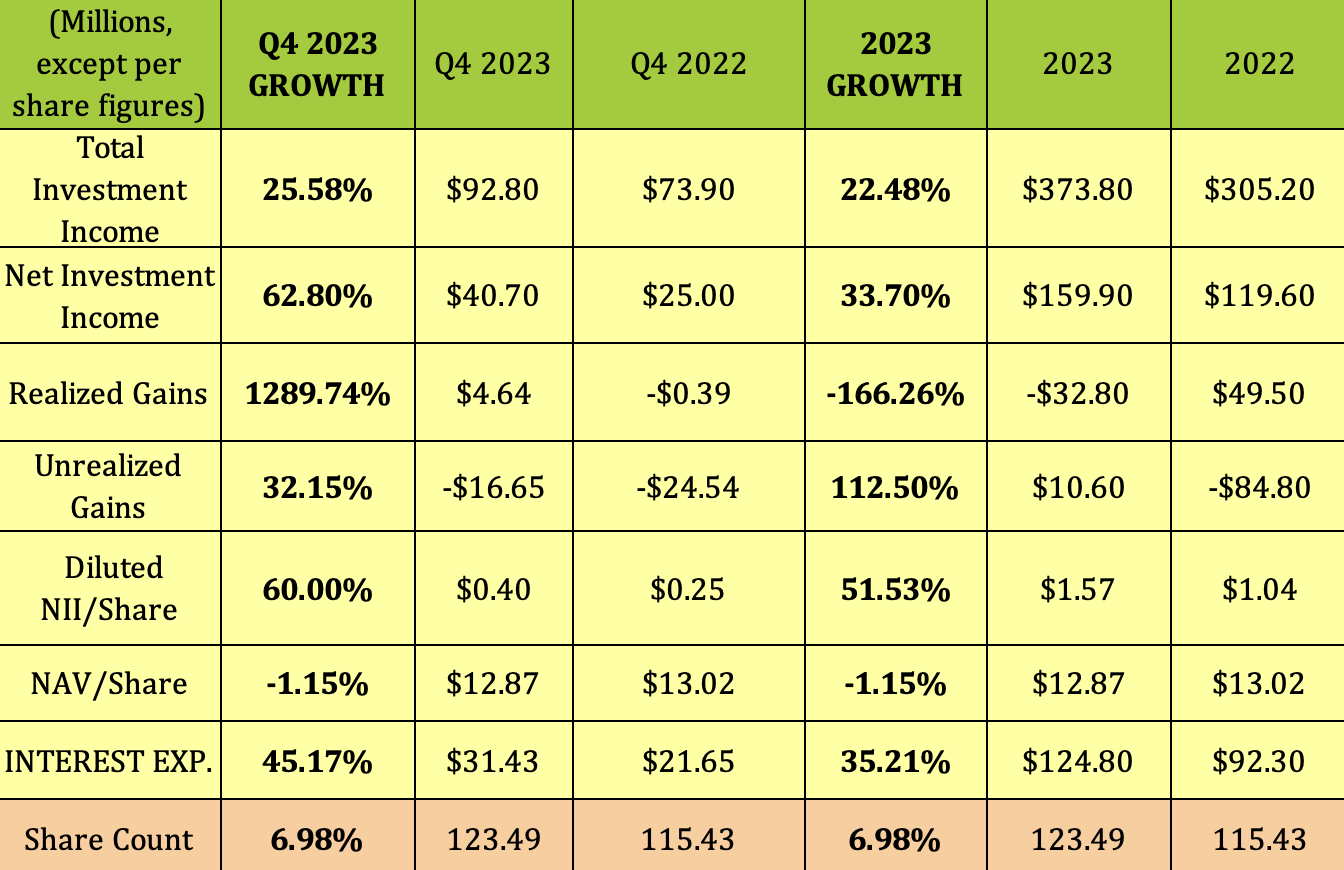

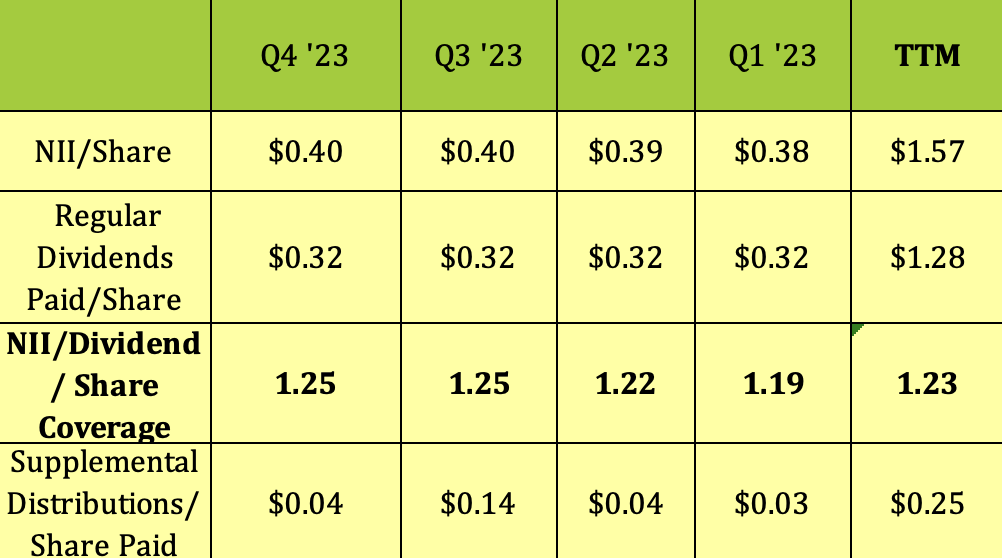

Q4 ’23 was a really profitable quarter for NMFC, with whole Funding Earnings rising over 25%, and NII surging ~63% vs. This fall ’22. NII/Share rose 60%, with the share rely rising by 7%. As seen elsewhere, NMFC had larger Curiosity bills, which have been up 45%. Realized Good points swung to $4.6M revenue, vs. a loss a yr in the past.

2023 was an enormous yr for NMFC, as with different BDC’s. Complete Funding Earnings rose 22.5%, whereas NII grew 33.7%, and NII/Share rose 51.5%. The flip facet to rising charges is that they’ll put extra strain on firms, as evidenced by Realized Good points swing to a $32.8M loss, vs. a $49.5M acquire in 2022.

NAV/Share ended the yr at $12.87, down 1.2% vs. This fall ’22, however NMFC did pay $1.53/share in distributions in 2023.

The common yield of NMFC’s portfolio decreased from 11.8% in Q3 ’23 to 10.9% for This fall, primarily as a result of downward shift within the base fee curve. The weighted common curiosity protection on the portfolio was flat at 1.5X in This fall ’23.

Hidden Dividend Shares Plus

New Enterprise

NMFC originated $142M of property, offset by $257M of repayments and gross sales in This fall ’23. The originations have been in core defensive development industries, reminiscent of veterinary providers, enterprise software program and infrastructure merchandise. 4 of the repayments have been second lien positions, and administration has line of sight into just a few extra second lien repayments.

Dividends

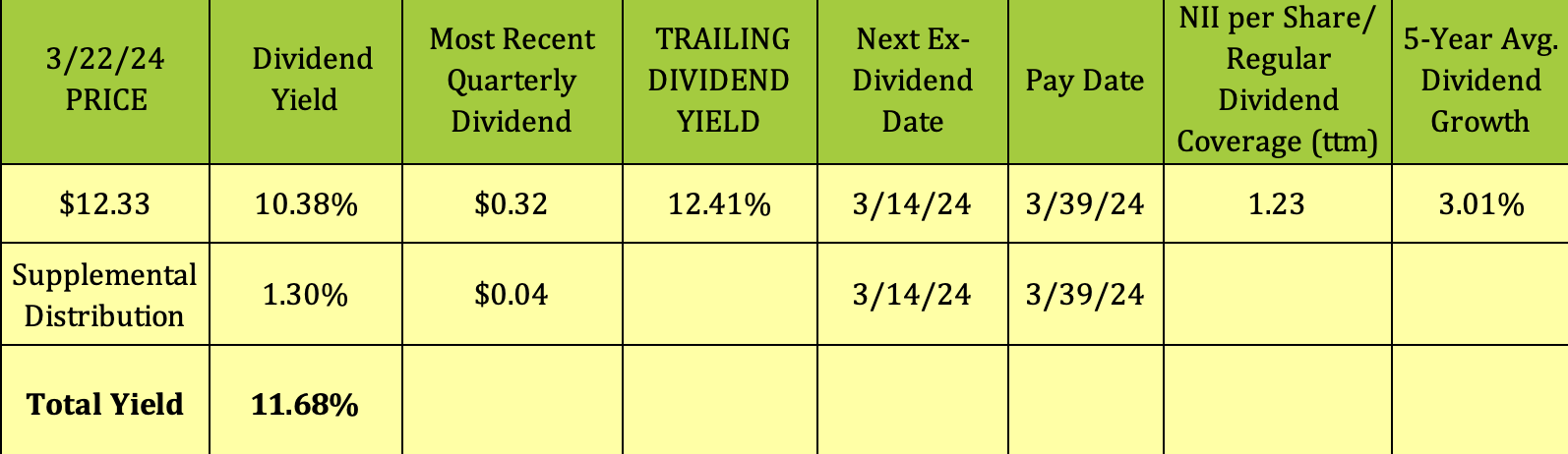

NMFC pays a base dividend of $.32/quarter. Management declared its 4th straight variable supplemental dividend fee, with this one being $.04.

At its 3/22/24 value of $12.33, NMFC has a base dividend yield of 10.38%. The $.04 extra payout provides 1.3%, for a complete yield of 11.68%. Its trailing yield is a bit larger, on account of a better supplemental dividend in Q3 ’23.

Administration expects to pay a variable supplemental dividend of a minimum of $0.02/ share payable within the second quarter of 2024, along with the same old $.32 dividend.

Hidden Dividend Shares Plus

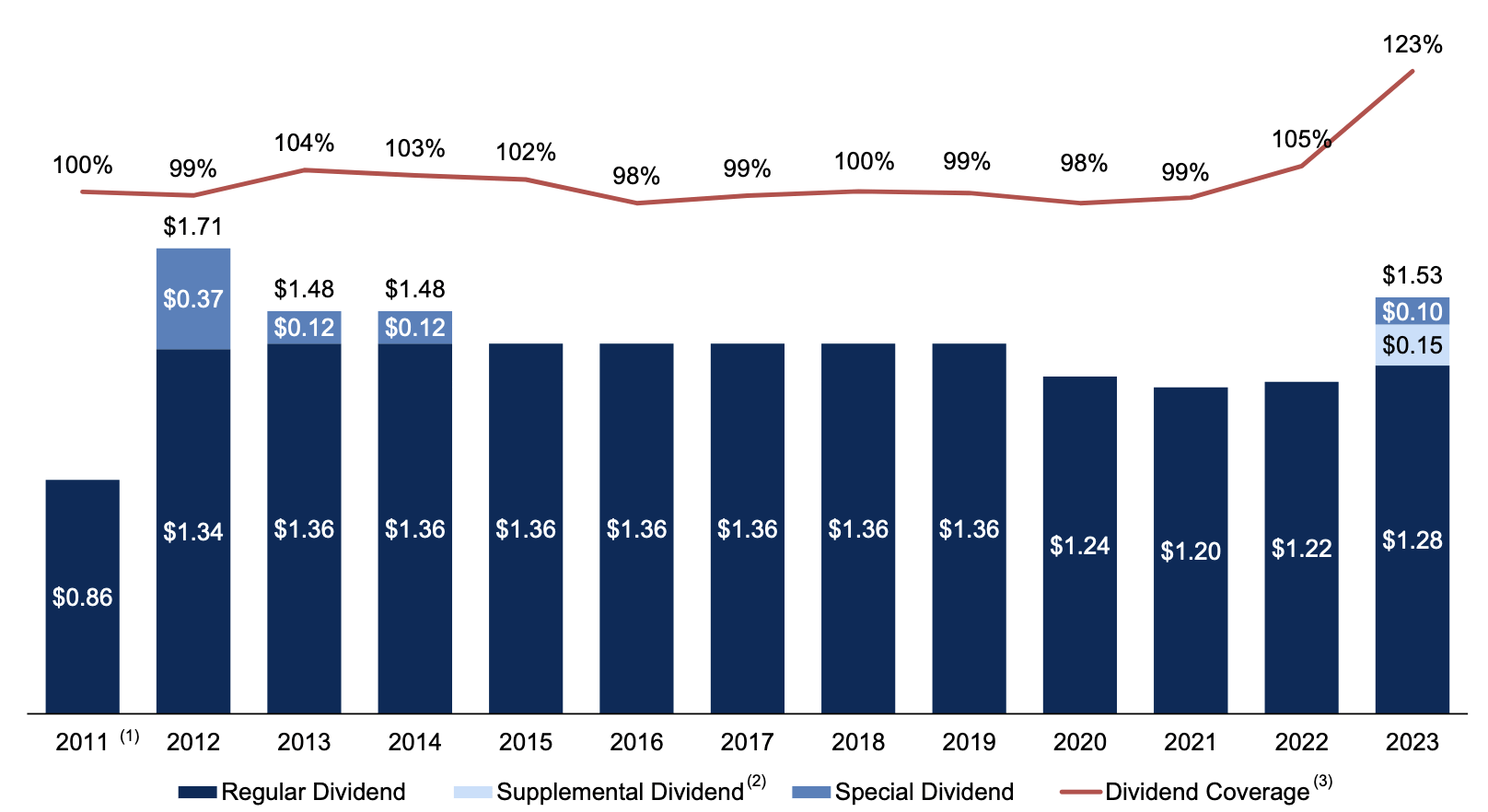

NMFC’s NII/base dividend protection issue is a wholesome 1.23X, larger than common for the BDC trade. It paid out $.25 in supplemental dividends in 2023:

Hidden Dividend Shares Plus

That 1.23X dividend protection in 2023 was a document for NMFC, as historic annual protection ratios have run from .98 to 1.05X:

NMFC website

Profitability & Leverage

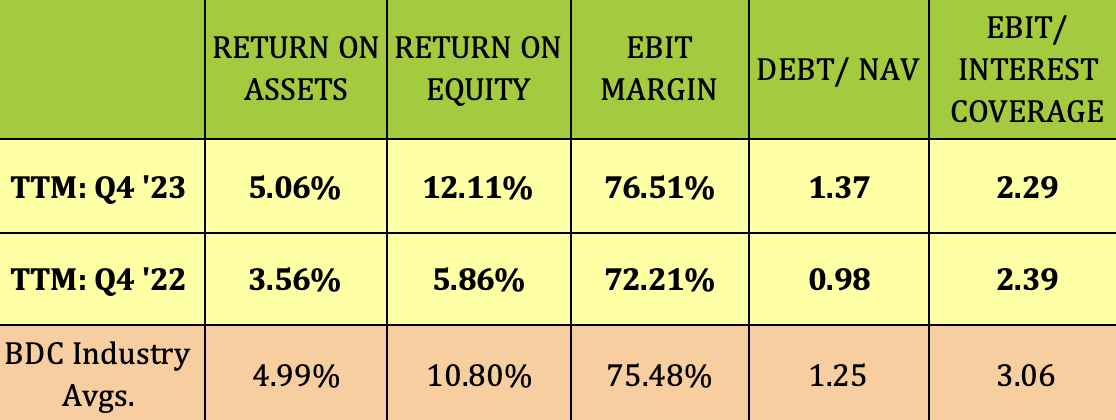

ROA and ROE each improved markedly in 2023, and at the moment are larger than BDC averages. EBIT Margin additionally improved, and is barely larger than common.

NMFC’s Debt/NAV rose from .98X to 1.37X in 2023, larger than the 1.25X BDC common, whereas EBIT/Curiosity protection fell barely, to 2.29X, under common.

Hidden Dividend Shares Plus

Debt & Liquidity

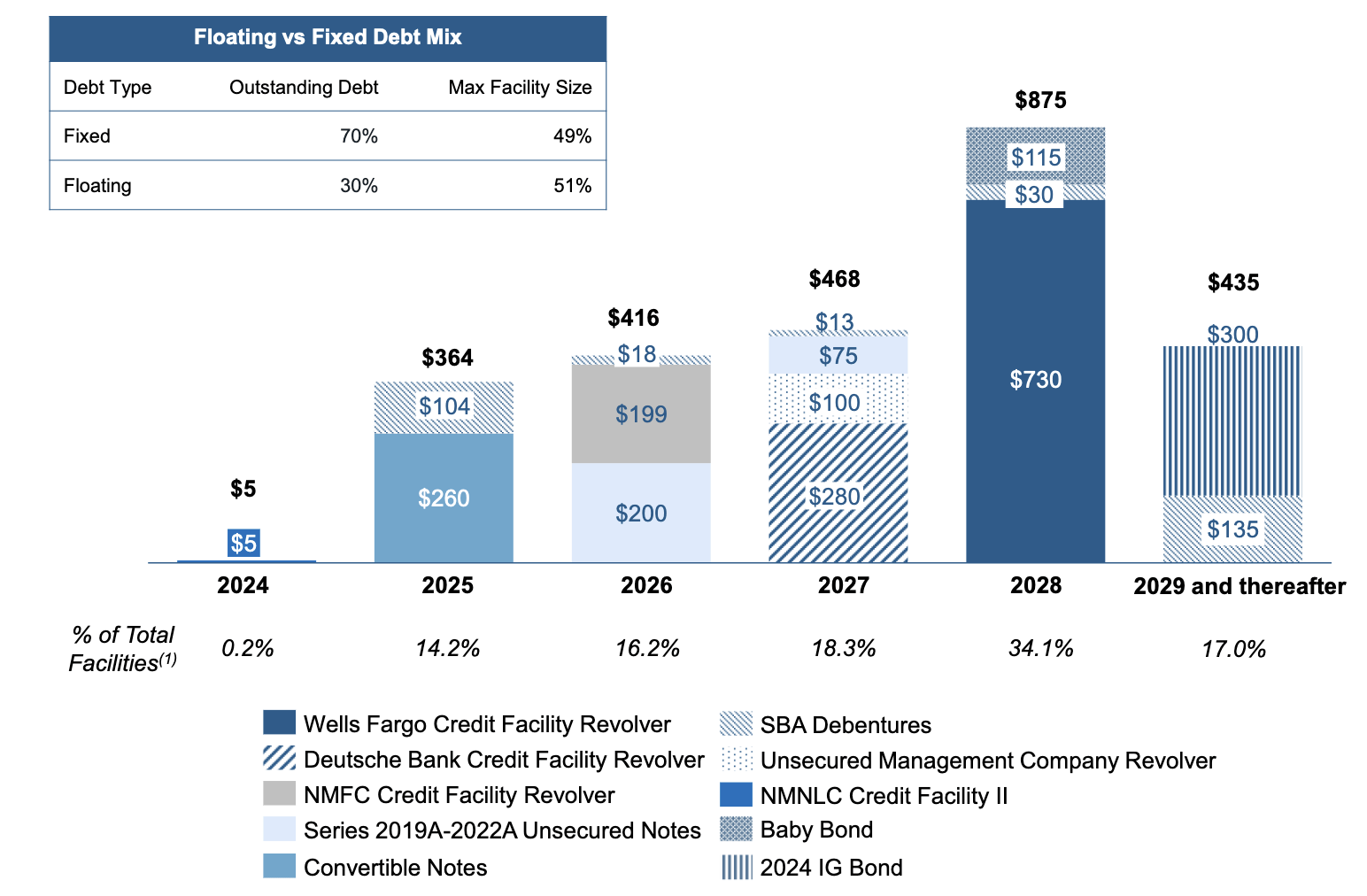

70% of NMFC’s debt is at mounted charges, whereas 88% of its property are at floating charges, a useful ratio which enormously aided earnings in 2023. Debt seems to be well-laddered out into the long run, with ~14% maturing in 2025, 16% in 2026, a8% in 2027, and 34% in 2028.

As of December 31, 2023, the Firm had money and money equivalents of $70.1 million and whole statutory debt excellent of $1,507.8M.

NMFC issued $300.0 million in combination principal quantity of 6.875% Unsecured notes due 2029 in February ’24. It then paid off its 2019A Unsecured Notes.

NMFC website

Insiders

New Mountain staff and Senior Advisors are NMFC’s largest shareholder group, at 13%.

Efficiency

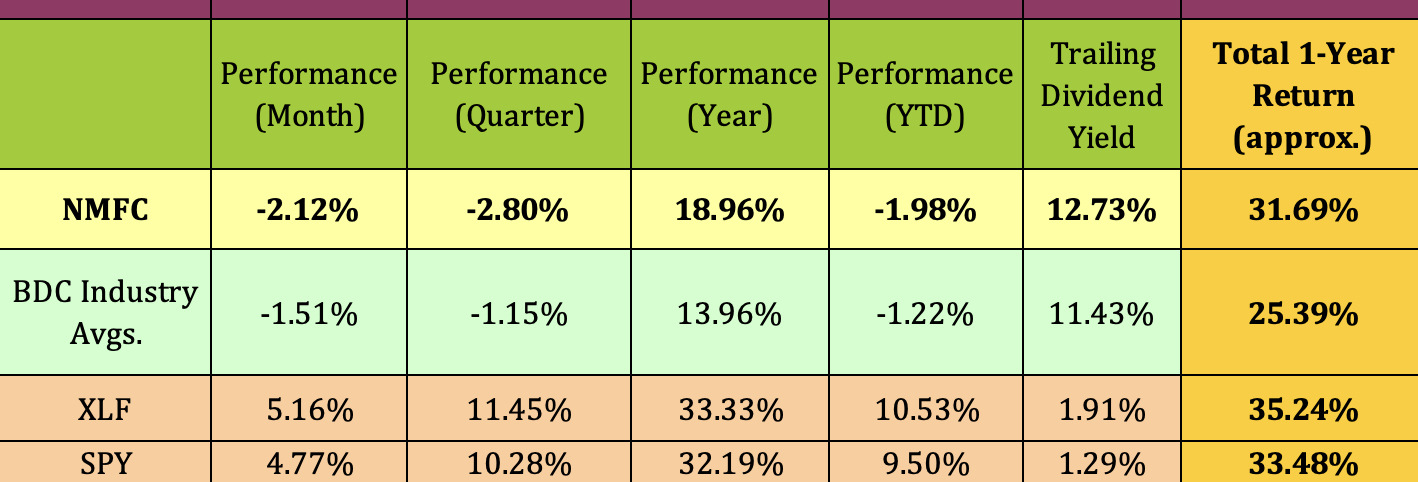

NMFC has outperformed the BDC up to now yr on a value and whole return foundation. Whereas it has trailed the broad Monetary sector and the S&P 500, its whole return was a beautiful ~31.7%, vs. 33.5% for the S&P, and 35.2% for Financials.

Hidden Dividend Shares Plus

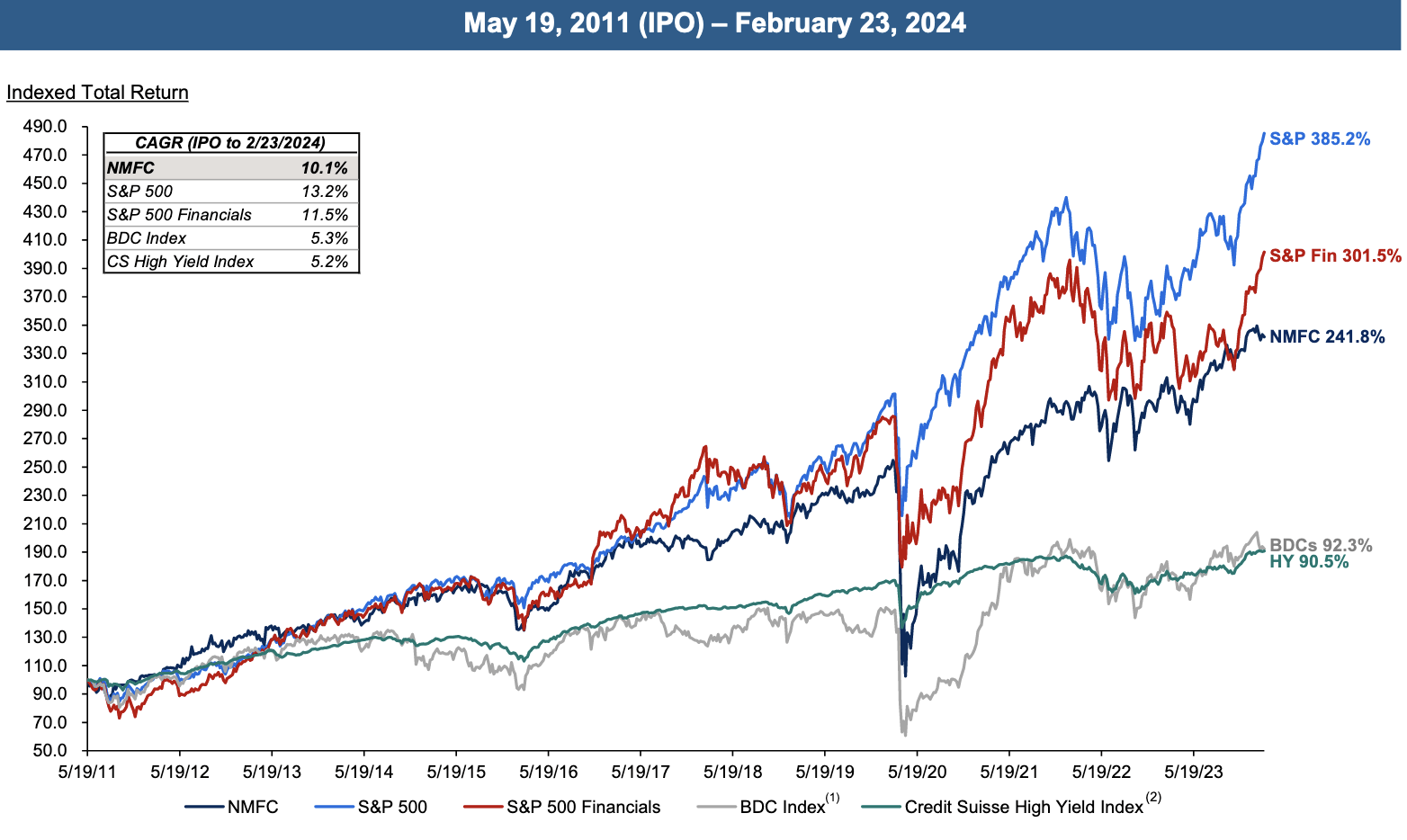

Administration’s long-term efficiency chart exhibits NMFC with a 241.8% whole return since its 2011 IPO, vs. 92.3% for the BDC trade.

By the way in which, should you’ve ever questioned in regards to the knowledge of shopping for throughout massive market pullbacks, this chart is a good illustration of that technique – the massive COVID Disaster pullback in 2020 was an unimaginable alternative for individuals who put their dry powder to make use of.

NMFC website

Analysts’ Value Targets

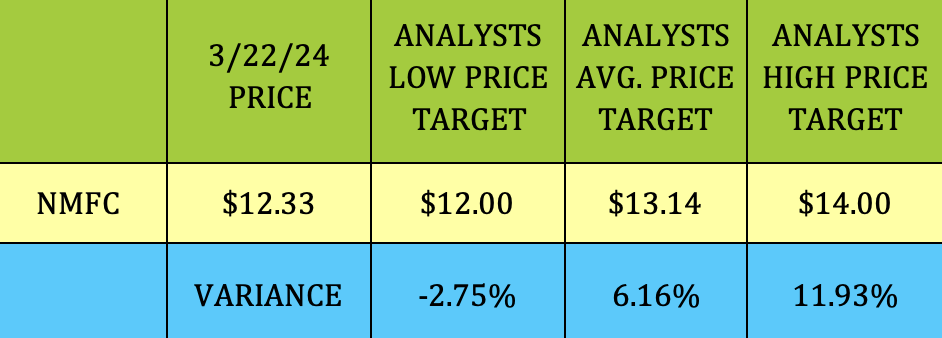

At $12.33, NMFC is 6% under Wall Street analysts’ $13.14 common value goal, and ~12% under their $12.00 highest goal.

Hidden Dividend Shares Plus

Valuations

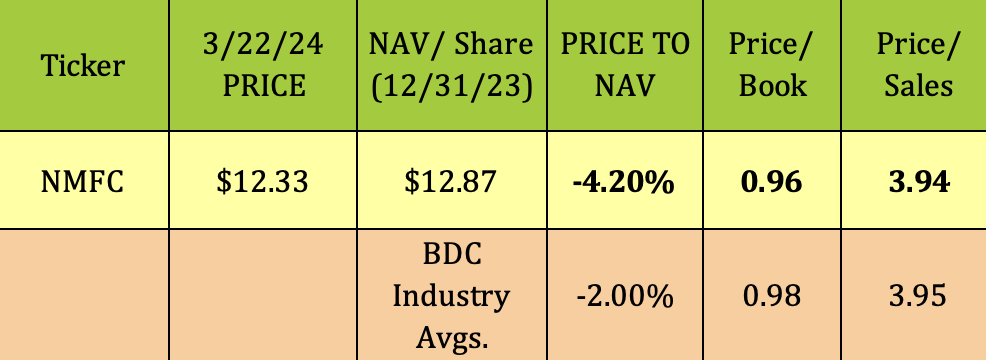

At $12.33, NMFC is promoting at a 4.2% low cost to its 12/31/23 NAV/Share of $12.87, vs. an general 2% common BDC trade low cost. Its P/Gross sales is consistent with the BDC trade common.

Hidden Dividend Shares Plus

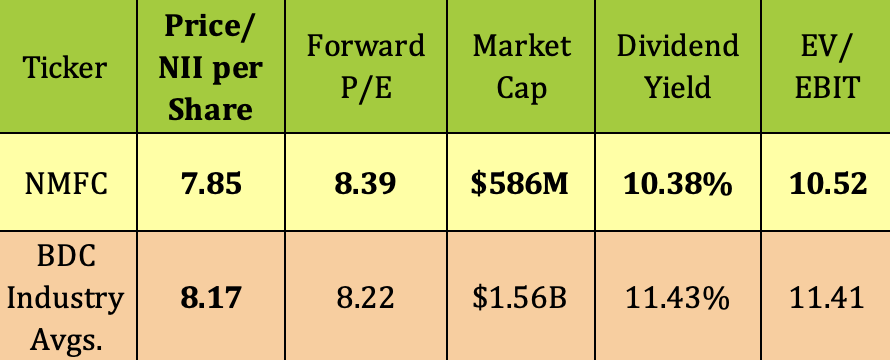

NMFC seems to be comparatively pretty valued on an earnings valuation foundation, being barely undervalued for trailing earnings, and barely overvalued for ahead earnings. Whereas its base dividend yield of 10.38% seems to be decrease than common, its supplemental payout places it into the 11%-plus bracket, consistent with the trade. EV/EBIT is considerably decrease than common.

Hidden Dividend Shares Plus

Parting Ideas

At $12.33, NMFC was ~5.7% above its 52-week low, and seemed oversold on its gradual stochastic chart.

We fee New Mountain Finance inventory a Maintain – it is a good firm, however we favor to attend for a less expensive value earlier than shopping for new shares.

All tables furnished by Hidden Dividend Shares Plus, except in any other case famous.