Rastan

New York Community Bank First Quarter Results:

New York Community Bancorp, Inc. (NYSE:NYCB) reported Q1 results that seemed to miss some “consensus” estimates, but were better than some Draconian fears that had crept into the market recently.

The company lost $.45 on a GAAP basis. Non-GAAP adjusted earnings were $.25, which was worse than Bloomberg consensus estimates of $.15 loss but better than FactSet’s consensus estimates of a $.26 loss.

The loss was primarily driven by a $315 million increase in the allowance for credit losses to 1.48% from 1.17%. This was higher than the consensus of about $250 million, but much less than the $552 million provision in Q4. Personally, in the context of an ~$82 billion loan portfolio, I’m not going to get excited about an extra $65 million of provisions. Net charge-offs came in at $81 million, also lower than Q4.

NYCB’s Credible Management:

The conference call was impressive. These guys have chopped a lot of wood to stabilize the bank in just eight weeks. The NYCB Q1 earnings presentation is excellent.

The two most important factors in stability (at least to me) are deposits and liquidity.

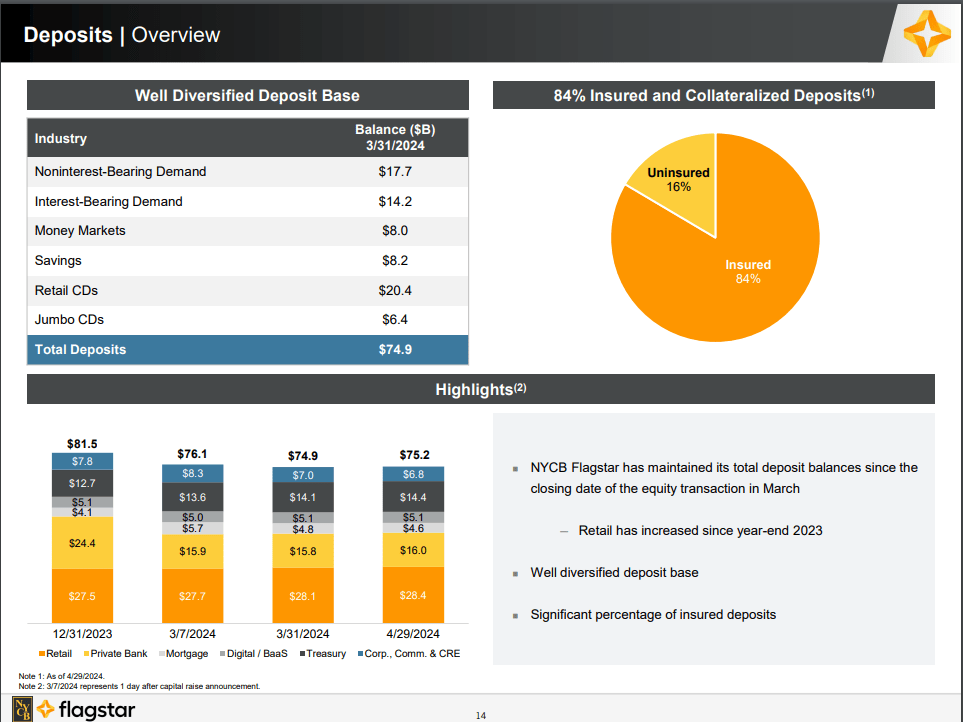

Deposits were $74.9 billion, which was slightly lower than the $77.2 billion the company reported at the beginning of March, when the Steve Mnuchin-led group injected capital into the bank and took over management. However, I’ve read many anecdotal stories of deposits flooding out of the bank. That is definitively not true. Deposits have grown since the end of Q1.

NYCB Deposits Breakdown (NYCB Q1 Earnings Presentation)

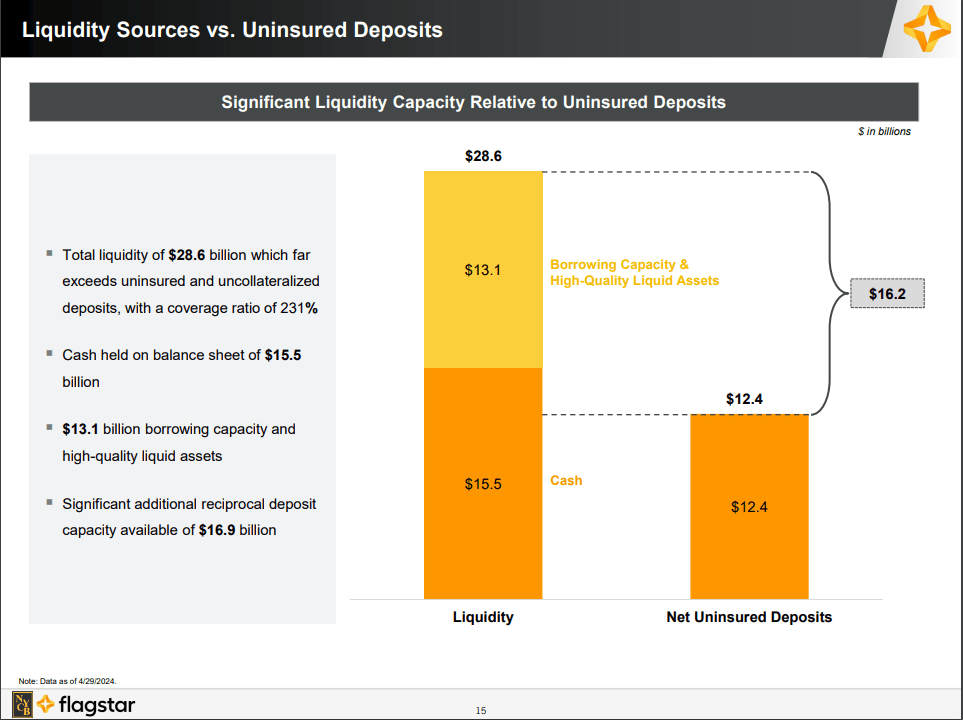

As important as the deposit number, the company’s liquidity is excellent versus its uninsured deposit base, which at 16% is lower than almost any bank I’ve seen. Cash now exceeds uninsured deposits.

NYCB Liquidity (NYCB Q1 Earnings Presentation)

NYCB’s Loan Book:

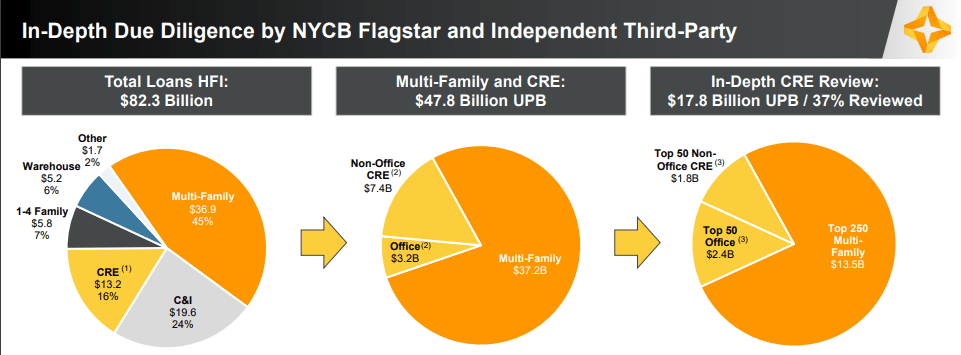

Much of the consternation surrounding NYCB involved its large CRE portfolio, especially its office and multifamily portfolio. The company has completed a deep dive on its biggest multifamily and office loans.

NYCB Loan Book (NYCB Q1 Earnings Presentation)

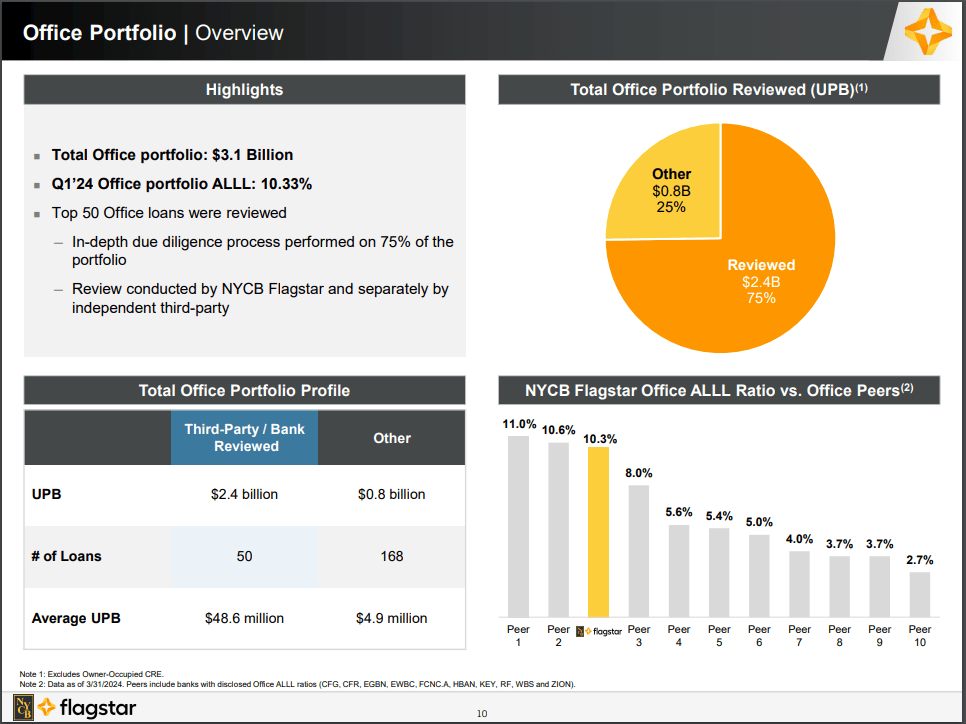

Office is the biggest area of concern and is where the company completed its most comprehensive review. The company has now increased its ALLL (allowance for loan losses) to 10.3%. This puts it near the top among its peers in terms of allowances.

NYCB Office Loan Portfolio (NYCB Q1 Earnings Presentation)

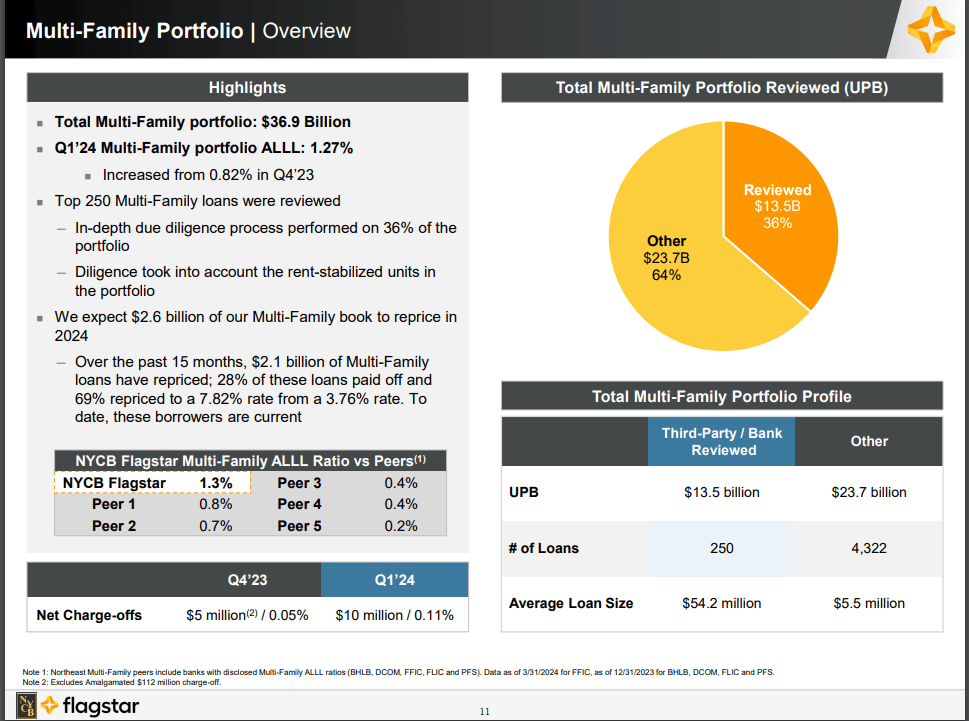

The company reviewed its largest multifamily loans as well. As I laid out in my first article on NYCB, the bank should be able to out earn even the worst case 100% default environment, as MFE loans came due. While the company did not break out which types of MFE loans matured in the past 15 months, there were no major defaults and 28% paid off.

NYCB Multi-Family Loan Book (NYCB Q1 Earnings Presentation)

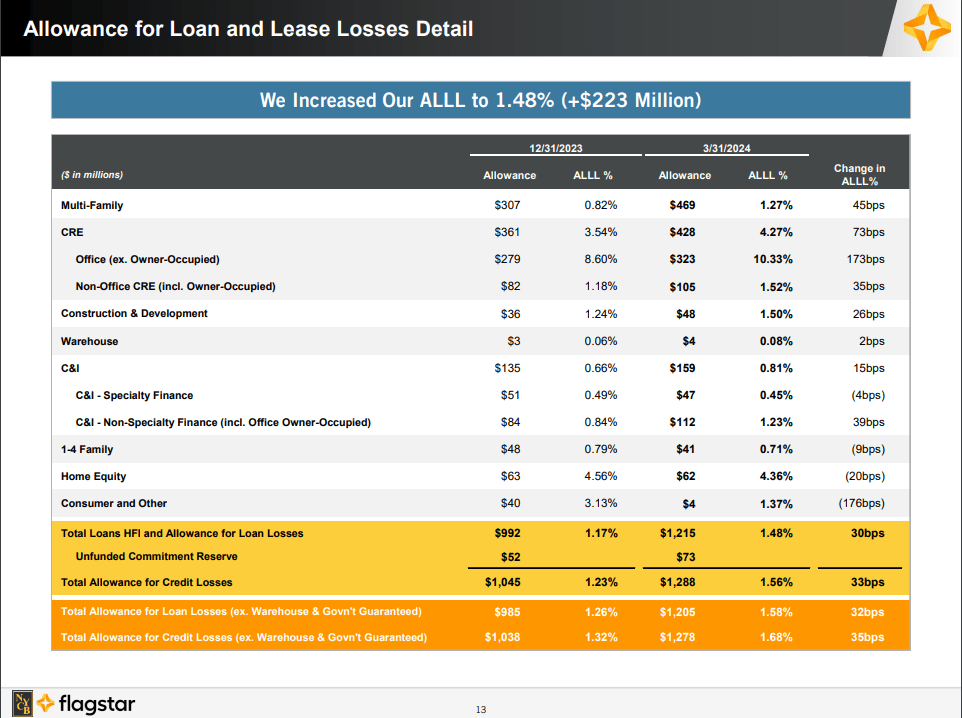

Overall, as you can see, the biggest percentage increase in ALLL was in office. There will be more losses this year, but management indicated Q1 was the highest expected quarter for allowances.

Allowance for Loan Loss Detail (NYCB Q1 Earnings Presentation)

NYCB’s Forward Guidance:

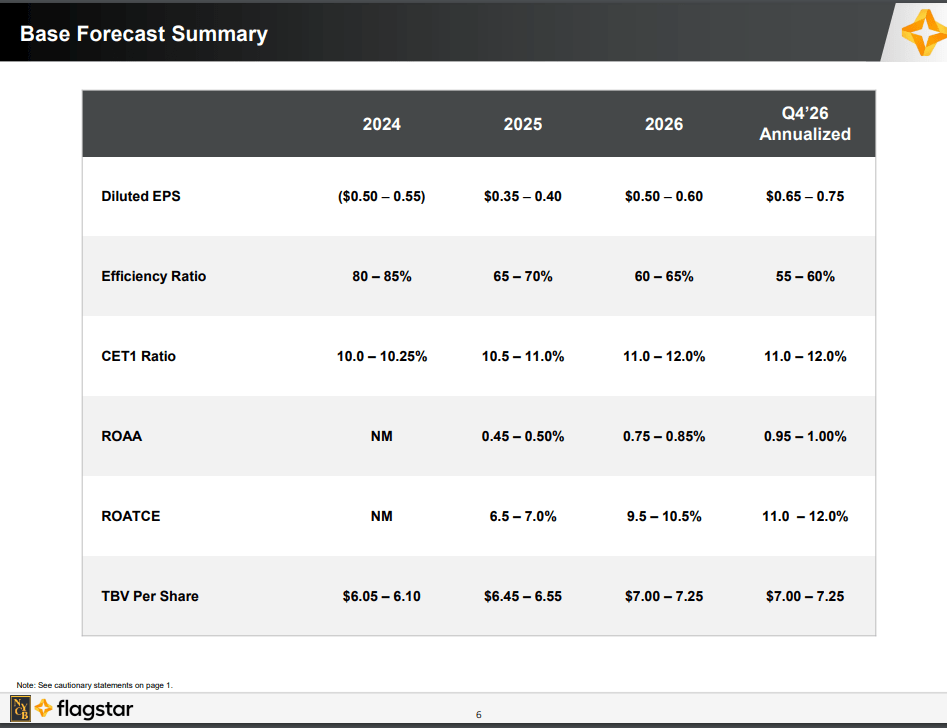

The company provided guidance for 2024 that was better than the worst fears. Moreover, (and more important for me) guidance for 2025 and beyond showed a glide path to a more normalized bank.

NYCB Base Forecast 2024 thru 2026 (NYCB Q1 Earnings Presentation)

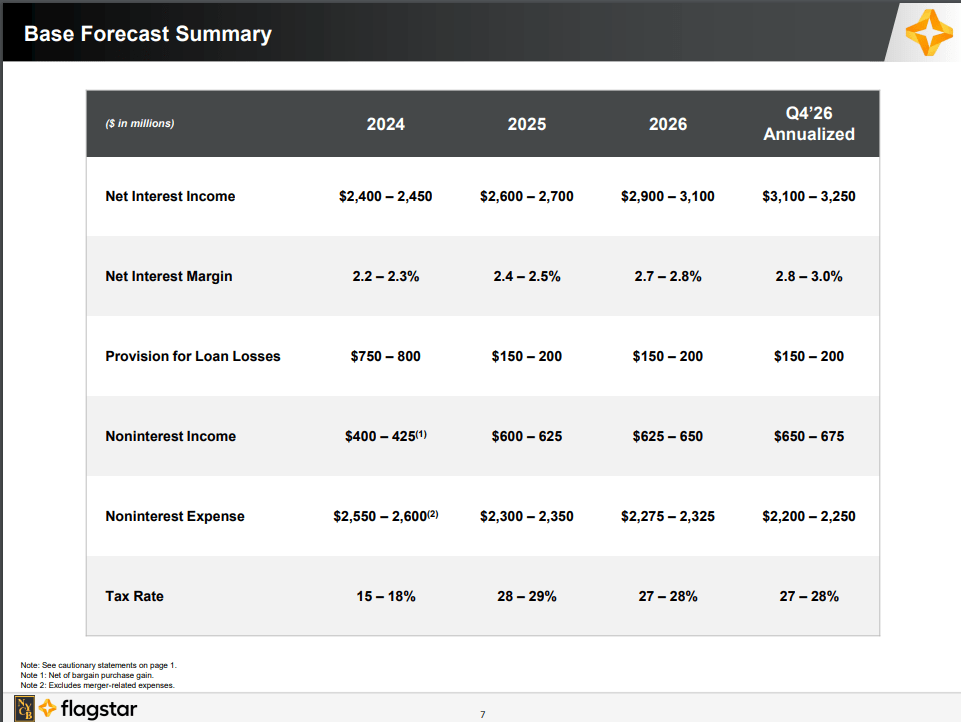

These headline results should be driven by the following operational assumptions.

NYCB Base Forecast Operational Detail (NYCB Q1 Earnings Presentation)

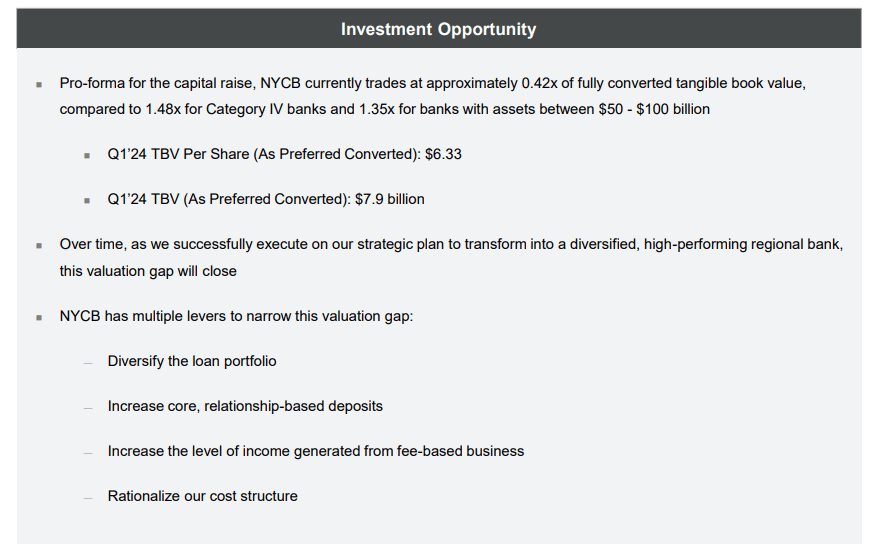

NYCB’s Discount Valuation:

NYCB trades at a huge discount to tangible book value. I believe most of this discount is due to fears that the bank would continue to bleed deposits and that loan losses, particularly in its office and multifamily real estate portfolio, would swamp whatever the bank earned elsewhere. Going into the print, the stock (@$2.65) traded at 42% of tangible book value. Even at $3+ post the results (as of this writing on Wednesday morning, May 1), the stock is about 50% of tangible book value. In my opinion, that prices in continued major problems rather than the relatively stable profile management laid out and backed up with numbers.

NYCB Investment Opportunity (NYCB Q1 Earnings Presentation)

Risks to NYCB Investment:

The major risks are:

- deposits going from stable to flying out the door

- a major uptick in losses from the loan portfolio

- trouble with regulators

- compression of NIM.

I think the company did a good job of addressing these risks, and most of them are not major concerns as things stand right now.

Conclusion:

My instincts, which I laid out in my first write-up on NYCB and a follow-up interview on SA after the Mnuchin group investment, were that this was a first-class management team that had invested in a distressed bank before. In my opinion, they knew exactly what they had to do to stabilize NYCB and acted quickly to do so. They have exceeded my expectations so far. This bank is not “fixed” yet, but the glide path is clear. I think New York Community Bancorp, Inc. stock should at least trade at tangible book value, implying 100% upside from here.