When entrepreneur Stephen Chen’s mother started approaching retirement age, she was compelled to borrow cash from Chen — and Chen’s brother — to make ends meet. They wished to assist, however the siblings additionally wished to determine a extra sustainable, long-term answer that’d assist their mother retire with out having to fret about funds.

Chen tried to get steerage from a monetary adviser, however nobody would take his mom as a consumer as a result of her web value wasn’t thought of excessive sufficient. So Chen began constructing spreadsheets and monetary fashions himself, doing his finest to determine how his mother might stay the retirement life-style that she wished.

“People like my mom lack the tools to look at their money holistically and strategically so they can make informed decisions, monitor their financial situation, understand which levers to pull and when and make the connection between the choices they make today and the long-term ramifications to their plan,” Chen advised TechCrunch. “There’s a confluence of factors that may alter the future of financial planning and advising.”

It was after Chen helped his mother decrease her bills, determine when to say Social Safety, determine when to downsize and take different steps to turn into financially unbiased that Chen realized a number of different older People have been dealing with the identical challenges.

So Chen based NewRetirement, a Mill Valley-based firm constructing software program to assist individuals create monetary retirement plans. Right now, NewRetirement’s direct-to-consumer merchandise energy monetary planning for 70,000 customers managing near $100 billion in their very own monetary plans, in line with Chen.

“Our models go beyond savings and investments, taking into account all of the other factors in a person’s life, from home equity, healthcare costs and taxes to Medicare and Social Security,” Chen mentioned. “Every time a user makes a change, we run thousands of simulations in order to help them optimize their plan … We account for thousands of different scenarios, enabling users to confidently map out accumulation and decumulation projections with digital guidance.”

NewRetirement is Chen’s second startup after Embark, a web based faculty search and admissions software he launched in 1995. And, like Embark, Chen sees NewRetirement as a digital answer to a transition confronted by thousands and thousands of People.

“120 million Americans over age 50 hold 80% of the wealth in this country,” Chen mentioned, “But running out of money remains a top 10 fear, with nearly half of Americans saying they are worried about it.”

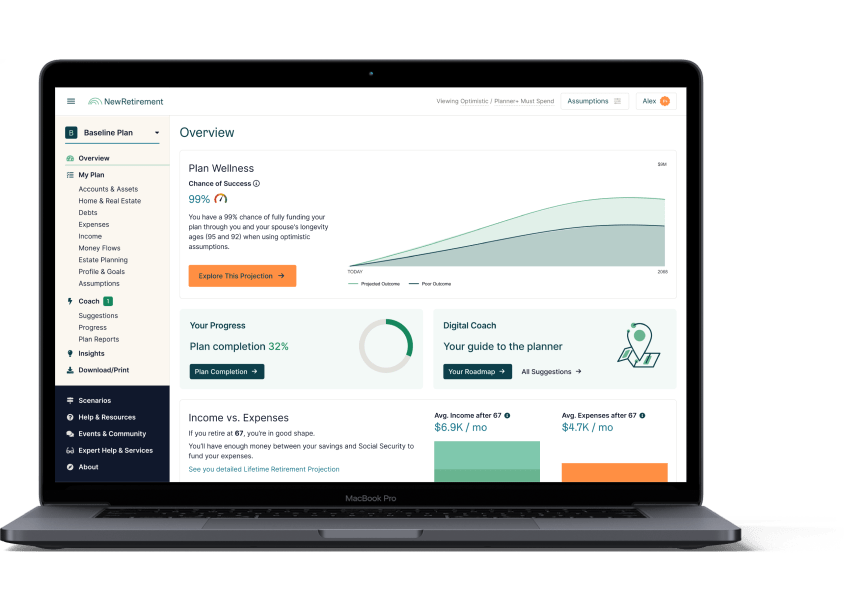

NewRetirement’s platform makes use of predictive modeling and knowledge analytics to assist customers suss out the precise financial savings approaches. Picture Credit: NewRetirement

Certainly, nearly all of People — as many as 65%, per Charles Schwab’s Modern Wealth Survey 2023 — don’t have any formal monetary plan. And whereas 37% of respondents say that they work with a monetary adviser, two-thirds of People consider that their monetary planning wants enchancment, in line with Northwestern Mutual’s Planning and Progress Study 2023.

NewRetirement, which started as a client providing and in 2021 expanded to the enterprise, costs $120 per 12 months for entry to a collection of instruments, calculators, suggestions and situation comparisons and ~$1,500 per 12 months for check-ins with a licensed monetary planner. As well as, NewRetirement sells a subscription-based non-public label model of its instruments geared toward monetary advisers.

Now, you may marvel, what makes NewRetirement completely different from startups like Retirable, which equally gives an array of retirement planning instruments and entry to asset managers? Chen asserts that NewRetirement is among the few — and maybe solely — monetary planning platform that serves customers in addition to advisers and workplaces.

“Our core innovation is allowing anyone to create a plan with industrial-strength tools, enabling advisers to collaborate with the end user and making this available at scale through enterprise partners who bring it to their customers,” Chen mentioned. “As more financial services companies see their offerings like investment management become commoditized, there’s huge value in helping clients and prospects think about their money holistically. By offering self-directed digital planning to clients versus starting with a human adviser, they can scale and serve any number of users, learn about them, help them make good decisions and position their products and services more effectively.”

Chen says that about 70% of NewRetirement’s income is enterprise presently, with the remaining 30% coming from client clients. The platform has 20,000 particular person subscribers and “several” wealth administration purchasers in addition to “multiple” enterprise clients together with Nationwide, which just lately expanded an present partnership with NewRetirement.

That momentum little question helped NewRetirement to cinch its Sequence A funding spherical this month.

The corporate raised $20 million in a tranche that brings its complete raised to $20.8 million, led by Allegis Capital with participation from Nationwide Ventures, Northwestern Mutual Future Ventures, Plug and Play Ventures, Motley Idiot Ventures and others. Chen says that the money infusion shall be used to broaden 50-employee NewRetirement’s enterprise merchandise, scale up onboarding, speed up R&D efforts and construct capability to fulfill future demand.

“With this new capital, we will have three to four years of runway,” Chen mentioned. “That gives us time to continue to scale our enterprise partnerships and enhance our product. What’s more, the current downturn is enabling us to bring in incredible talent. We have a strong team in place and will expand headcount further this year.”