Editor’s observe: Searching for Alpha is proud to welcome Emanuele Mologni as a brand new contributor. It is easy to change into a Searching for Alpha contributor and earn cash in your finest funding concepts. Lively contributors additionally get free entry to SA Premium. Click here to find out more »

MoMo Productions

Funding Thesis

Nexi (OTCPK:NEXPF, OTCPK:NEXXY) was, till a number of years in the past, a comparatively small Italian firm, working in a type of “niche”, taking good care of digital cost enterprise solely within the nationwide market. Ranging from 2021 it has began a revolutionary work of internationalization with essential acquisitions on the European market, turning into one of many main gamers in that space.

I contemplate Nexi a extremely attention-grabbing firm in a fast-growing sector (digital funds), with a particular concentrate on a deeply under-penetrated market (the European one) and in a terrific place from the place it is able to reap the following years of development, due to its robust entrenched enterprise mannequin.

With this evaluation, I need to show how Nexi could be a good addition to the portfolio of those that function with a long-term buy-and-hold technique, due to the great development expectations paired with the superb solidity of the enterprise mannequin. I particularly just like the robust positioning of Nexi in its markets (each by enterprise sort and geographical space), and I discover the monetary historical past of the corporate an excellent instance of regular however steady development, and a strategic administration of funding.

Within the following paragraphs:

-

We are going to analyze the corporate ranging from a fast abstract of the enterprise mannequin, income sources and the research of present market scenario of the corporate and its sector.

-

We are going to see at a macro degree the factors of energy and danger of Nexi’s enterprise, then we are going to take these issues within the evaluation of the corporate financials of the previous couple of years, and see how these are mirrored within the enterprise numbers.

-

Having drawn up a steadiness of the present execs and cons at a macro-economic and monetary ranges, I’ll attempt to give a worth goal to Nexi shares based mostly on the DCF calculation and by comparability with direct opponents.

-

Lastly, I’ll topic what has been analyzed up thus far to a type of “crash test”, hypothesizing varied danger conditions, to determine how they may affect the corporate’s efficiency.

A Transient Overview On Enterprise Mannequin

Nexi was integrated in 2017, because of a protracted collection of Italian monetary teams mergers began in 1939, subsequently it represents the end result of a phenomenon of “cooperation and centralization” on the digital funds enterprise by the Italian banking sector, characterised quite the opposite by appreciable fragmentation.

Initially an organization with a powerful nationwide character it has rapidly change into, thanks specifically to the acquisition of the Sia and Nets teams in 2021, a number one firm in Europe within the digital funds sector.

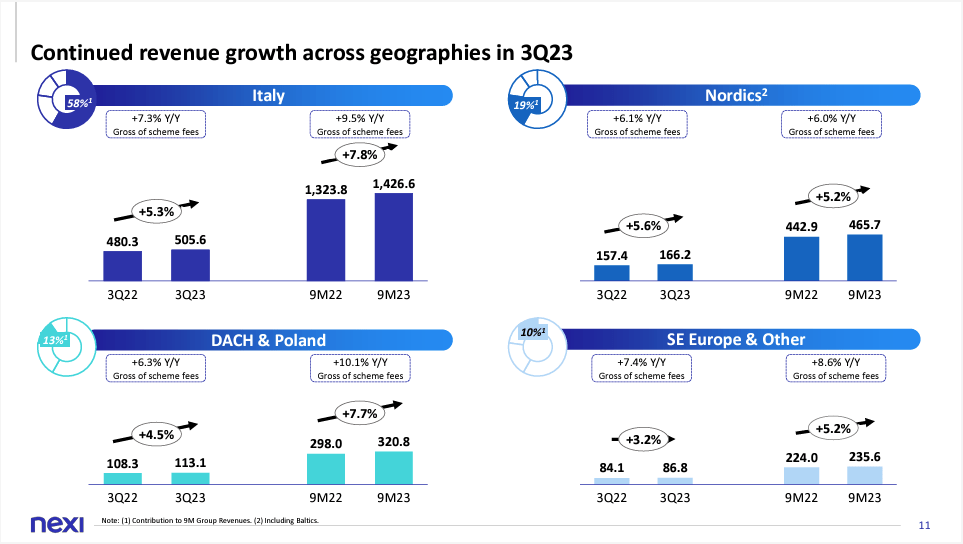

As for the final quarterly report (9M 2023) the corporate’s enterprise is split into three fundamental branches:

– Service provider Options (57% of whole income)

The Service provider division is answerable for offering digital cost providers to retailers (buying providers), each at a bodily degree (POS) and in ecommerce. It represents the core enterprise of Nexi, which presents itself as a “one-stop-shop” for its clients, taking good care of your complete cost chain: from the sale and configuration of the POS, to upkeep and integration with pre-existing software program, fraud and disputes administration, and buyer care usually.

– Issuing Options (32% of whole income)

This division offers with issuing and administration of cost playing cards; it must be famous that Nexi points playing cards virtually completely via companion banks (and completely at all times for the “revolving” sort, with repayments on deferred deadlines), thus offloading the credit score danger onto the banks themselves.

– Digital Banking Answer (11% of whole income)

The latter division offers with community providers, ATM administration, digital banking for third events and software program associated to financial institution funds.

The enterprise is characterised by a really robust geographical part with Italy alone accounting for 58% of whole revenues, Scandinavia and the Baltics for 19%, DACH Space (Germany, Switzerland and Austria plus Poland) for 13% and the leftover (10%) divided in South-eastern Europe.

Nexi 9M Y2023 Quarterly Report

Nexi comes from a really troublesome market interval: after reaching highs above €19 per share in July 2021, the costs started a downward spiral to the historic low of €5 on the finish of October 2023, for a proportion loss near 75%.

Such a loss can scare a prudent investor, and definitely represents a ringing bell for these like me preferring shares with slower development however with extra managed volatility and extra predictable actions.

On the similar time, it’s helpful to notice that this motion was not a singularity of Nexi shares however affected, kind of in the identical interval, your complete fintech sector: each European (the place certainly Nexi demonstrated even higher performances than its direct opponents, Worldline (OTCPK:WWLNF) (-90%) and Adyen (OTCPK:ADYEY) (-79%) but additionally abroad within the American market with Constancy Nationwide Info (FIS) (-70%) and World Funds (GPN) (-58%).

This collapse, which started instantly after the toughest section of the pandemic, has been in contrast by some to what occurred with the dotcoms within the 2000s: fintech corporations introduced themselves (ranging from the post-2008 disaster interval) as new gamers within the monetary market, the concept that they may substitute the “traditional” banking establishments, the favorable financial interval and the ever-increasing adoption of digital in folks’s lives, rapidly led to skyrocketing valuations, with a powerful disconnection from the basics of the businesses themselves.

In the end, I imagine that this collapse in inventory costs was a really painful however wholesome return to actuality for a sector (fintech) that was having non-sustainable costs and that now could be the time to search for alternatives available on the market, ranging from the businesses which have proven extra solidity on this troublesome interval and that are higher positioned to benefit from opponents’ weaknesses.

Macro Evaluation (Fundamentals)

Let’s now attempt to determine which in my view are the corporate’s biggest strengths and weaknesses; as usually occurs (and so is for Nexi) the 2 issues are carefully related: the foremost development drivers of Nexi additionally symbolize, in my view, the factors of larger danger for the corporate’s enterprise.

The primary factors to investigate are actually these linked to the enterprise mannequin listed within the earlier paragraph: income sources and geographical diversification.

Nexi’s whole enterprise, though diversified into the three branches Service provider Options, Issuing Options and Digital Banking Options, has a really robust part inside it, and that is the required relationship with banking establishments.

The revenues of all three sectors are in reality strictly depending on agreements and contracts between the corporate and the banks of the numerous international locations Nexi works in. All contracts symbolize long-term agreements which, even when stipulated with the intention of adequately defending Nexi’s market place and on the idea of a win-win relationship between the events, are nonetheless topic to a future expiry and subsequently expose Nexi to a possible danger of shedding market shares within the occasion of non-renewal, or of shedding revenue margins within the occasion of renewal underneath much less advantageous situations (as a result of larger competitors, market adversarial momentum or for the totally different pursuits of the banks on the time of renewal).

However, nonetheless, the presence of those contracts additionally represents (no less than so long as they continue to be in power) a really robust barrier to the doorway into the marketplace for any competitor, guaranteeing Nexi a powerful place of dominance in its key markets and a near-monopoly in its core markets.

One other attribute of Nexi’s enterprise is the very robust geographical focus, the corporate generates all of its revenues within the European market, and greater than half is in Italy alone.

In Italy Nexi covers a putting proportion of digital-format funds: in its fundamental enterprise department for instance (Retailers Buying), the AGCOM (Italian antitrust authority) estimated in 2021 earlier than Sia-Nexi merger an virtually 50% market share after acquisition, and Jefferies estimated an almost 70% whole market share in Italy.

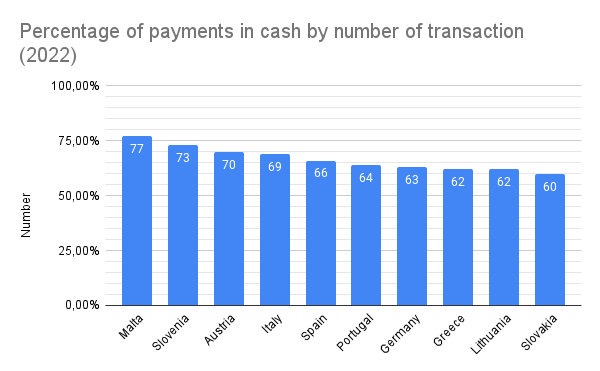

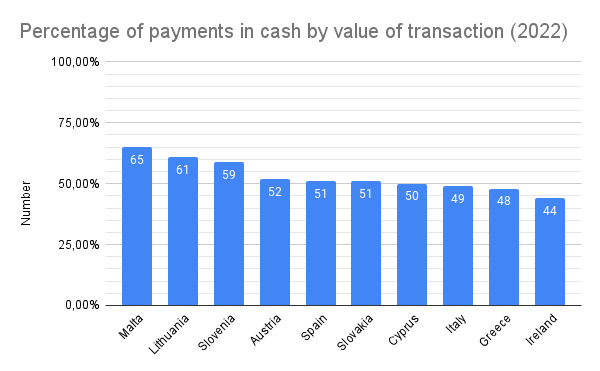

If we have in mind that in 2022 money funds in Italy nonetheless represented 69% of total transactions it’s clear how the shift in direction of digital on this nation might symbolize an enormous development alternative for Nexi.

The subsequent two graphs present the rating of the primary ten international locations within the EU by proportion of money funds at level of sale (POS) over the entire, by variety of transactions and worth of transactions respectively.

Graph by the Writer, information from ECB Graph by the Writer, information from ECB

Transaction worth within the cell POS funds market is anticipated to indicate an annual development charge (CAGR) between 2024 and 2028 of 12.76% on the earth, 14.88% in Europe and 19.37% in Italy (Supply: Statista – The Statistics Portal).

We will clearly see the strategic place of Nexi, as a sector chief in Europe, who can simply profit from the upper development charge on this space as a result of present delays within the penetration of digital as a type of cost.

Likewise, such a powerful territorial focus can expose the corporate to macro-economic, forex and political dangers, similar to adjustments to sector rules, political selections unfavorable to the enterprise, weak spot of the European currencies (primarily the EUR), and so on.

Additionally noteworthy on this case is the robust publicity to Italy: we have now already seen the nice significance from the standpoint of revenues, however the Italian state can also be a stockholder of the corporate with a share of roughly 13.5% via the subsidiary CDP; subsequently along with a big affect on the monetary aspect (via legal guidelines and rules on the digital funds sector) it could possibly additionally mix management at a “governance” degree: an instance could possibly be the potential of stopping any exterior acquisition try, in case it ought to contemplate the Nexi sector strategic for nationwide safety.

Nexi is constantly working to broaden its market, no less than inside Europe: in Spain (a market not but touched by the corporate), Nexi signed a deal a number of months in the past for the acquisition of an 80% stake in Service provider Buying enterprise of Sabadell financial institution (OTCPK:BNDSF) PayComet along with a long-term partnership settlement (overcoming the affords of its main European competitor Worldline and the US firm Constancy Nationwide Info), which can assure the acquisition of over 380,000 retailers and transaction volumes of roughly 48 billion euros in that Nation upon completion.

This settlement, signed with the second service provider acquirer in Spain, will assure entry to an additional market in Europe, the fourth largest within the Euro space and one with a low penetration of digital cost (round 38%) subsequently with wonderful margins of development.

The closing of the settlement (topic to acquiring regulatory authorization for operations of this type) was initially scheduled for the final quarter of 2023, then moved to the primary half of 2024.

One other attention-grabbing alternative is given by Germany (a market nonetheless under-penetrated by Nexi): right here Nexi concluded an settlement in August to accumulate 30% of Computop, the principle nationwide supplier (greater than a 3rd of the market) of cost providers for e-commerce.

How Financials Mirror Macro-Evaluation

As we have now seen, Nexi comes from a troublesome second, and it is very important set up whether or not the corporate has the solidity and energy to reverse the pattern of the final two years.

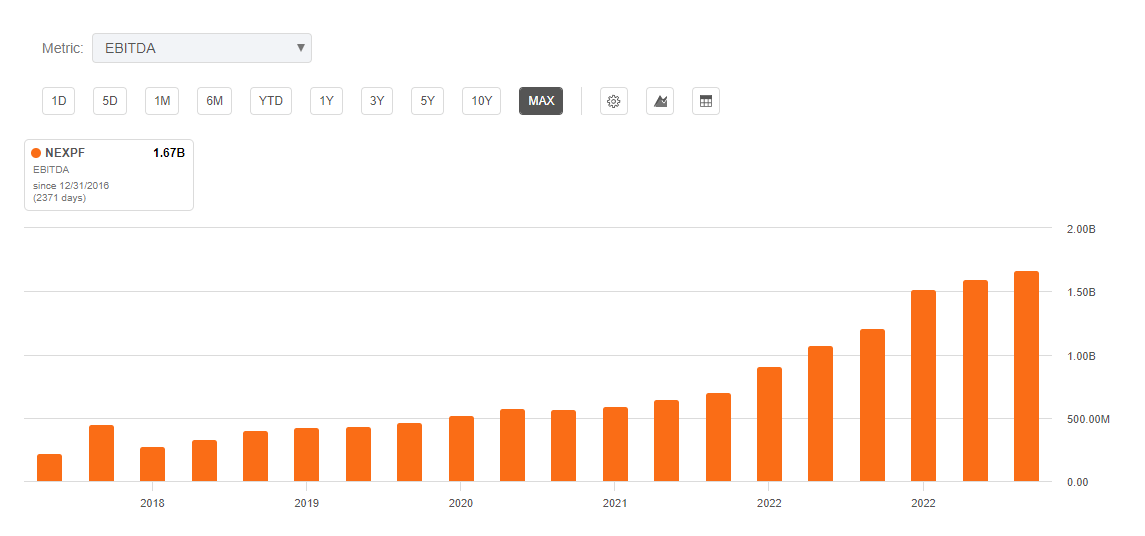

Over the previous couple of years, Nexi’s financial development has by no means stopped: looking on the fundamental monetary information, we will instantly discover a steady year-over-year development in revenues (in whole, over +500% from 2018 to 2022), undoubtedly pushed by the essential work in M&A, with the acquisition specifically of the Sia and Nets teams in 2021

Graph and information by Searching for Alpha

EBITDA grew greater than 3 times regardless of the numerous financial efforts made (each for the acquisition in M&A and for the variation of the organizational construction).

Graph and information by Searching for Alpha

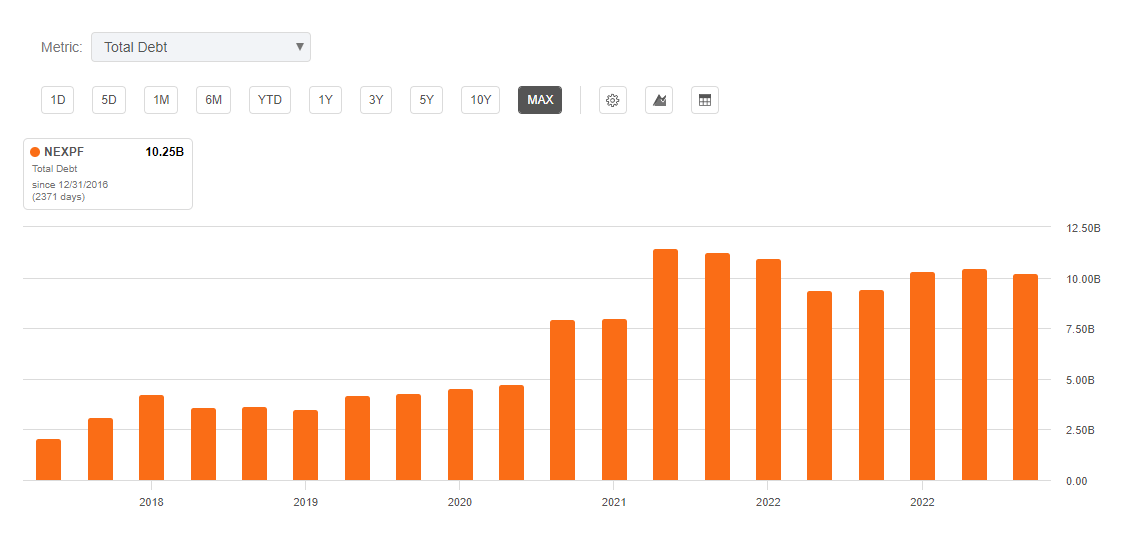

Let’s as a substitute see the principle “flaw” of Nexi’s steadiness sheet: the entire debt is actually notable, partly because of the M&A acquisitions talked about earlier; talking concerning the Web Debt / EBITDA ratio we will find it at 3.1 (as from final Nexi’s quarterly report), though at degree that we will not contemplate good, in my view it’s not excessively worrying: it must be highlighted that in latest quarters the corporate has carried out a accountable work of partial reduction, and in accordance with the administration it ought to proceed no less than till the ratio is introduced again beneath 3 (earlier than 2025).

Graph and information by Searching for Alpha

From a monetary standpoint, subsequently, we will assert that the collapse of share costs was neither a trigger nor a consequence of an financial deterioration of the corporate, which quite the opposite was in a position to show attention-grabbing underlying development, regardless of the big variety of “economic scenarios ” that the market has proposed.

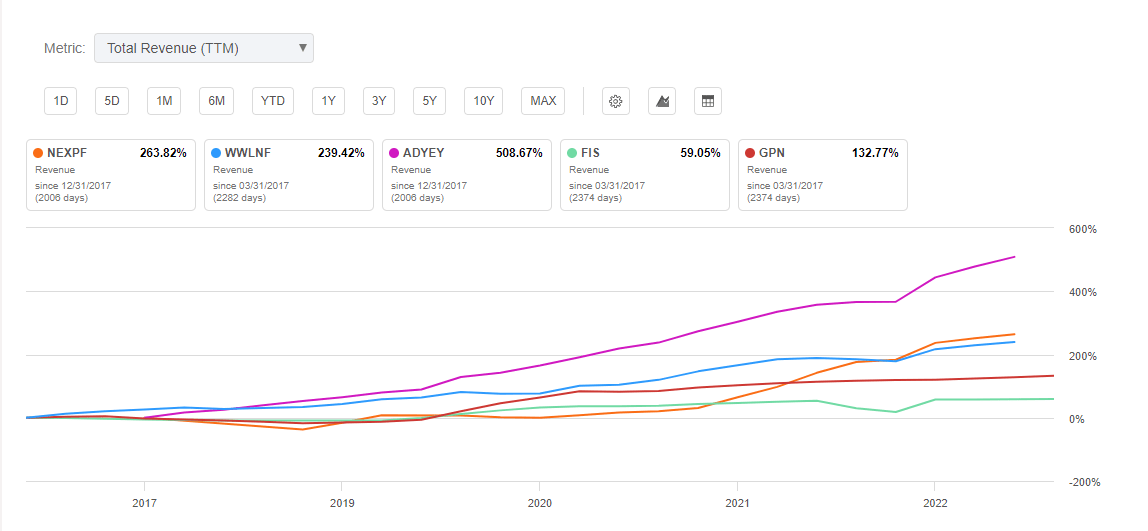

The next graph is in my view very attention-grabbing: it represents the share enhance in Nexi’s Complete Income (TTM) within the interval between 1/1/2017 and 12/21/2023, in comparison with some corporations in the identical sector, together with two of its direct opponents in Europe.

Graph and information by Searching for Alpha, Tickers selection by the Writer

With out judging different corporations from this easy graph (every case must be studied intimately), it’s clear that from its basis to immediately, Nexi has been working to carve out its personal market share, which if at a world degree stays somewhat irrelevant, is totally exceptional in its geographical space (the European one).

A First Recap, DCF Calculation And A Look To Opponents

Nexi forecasted in its “Growth Plan“, launched on 2022 Capital Markets Day, a income development (CAGR) of 9% per yr, an EBITDA development of 14% and money synergies of 365 million from the merger with Nets and Sia (rising from 320 million initially anticipated) from the publication to yr 2025, all of this along with an working money movement and EPS CAGR of roughly 32% and 20% respectively.

This could assure Nexi a “cash excess” of two.8 billion € by 2025, for which the administration has already recognized three areas of spending: return to shareholders with buybacks or dividends, additional M&A or larger debt discount (the latter outlined as “less likely”).

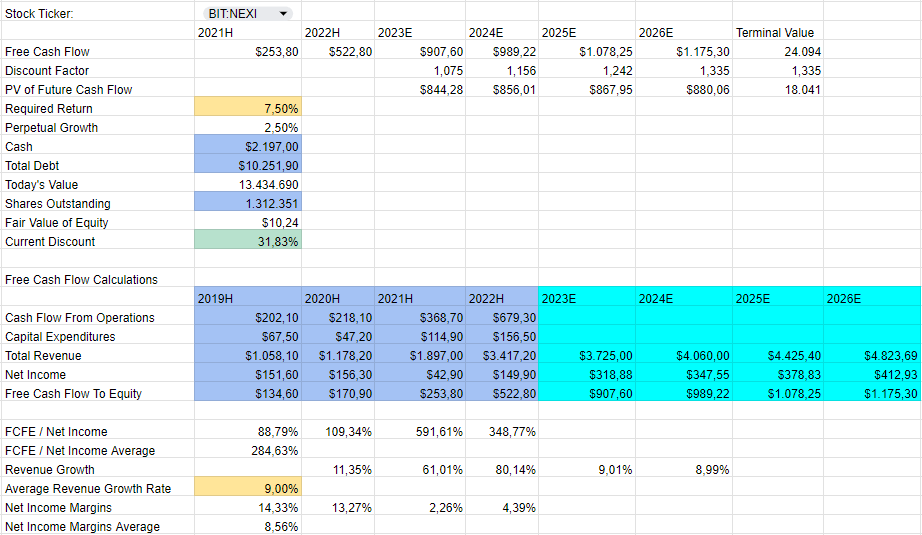

Let’s now attempt to set up a goal worth for Nexi in accordance with DCF calculation; for monetary information, we are going to depend on numbers from Searching for Alpha.

We are going to use Nexi’s “Growth Plan” indication for future income development information (9%), for now, we won’t have in mind the benefits as a result of synergies, or the expansion in working money movement and Web Revenue envisaged by the Progress Plan, however as a substitute, we are going to use the historic common development for the calculation, and as a reduction proportion we are going to use an “average” determine of seven.5%.

The latter is an estimated worth, midway between the WACC calculated on 2022 information (5.36%) and the worth that Nexi itself used for honest worth calculation on its branches for goodwill repartition throughout impairment tests (simply over 9%).

We will see right here my DCF calculation:

Spreadsheet from the Writer

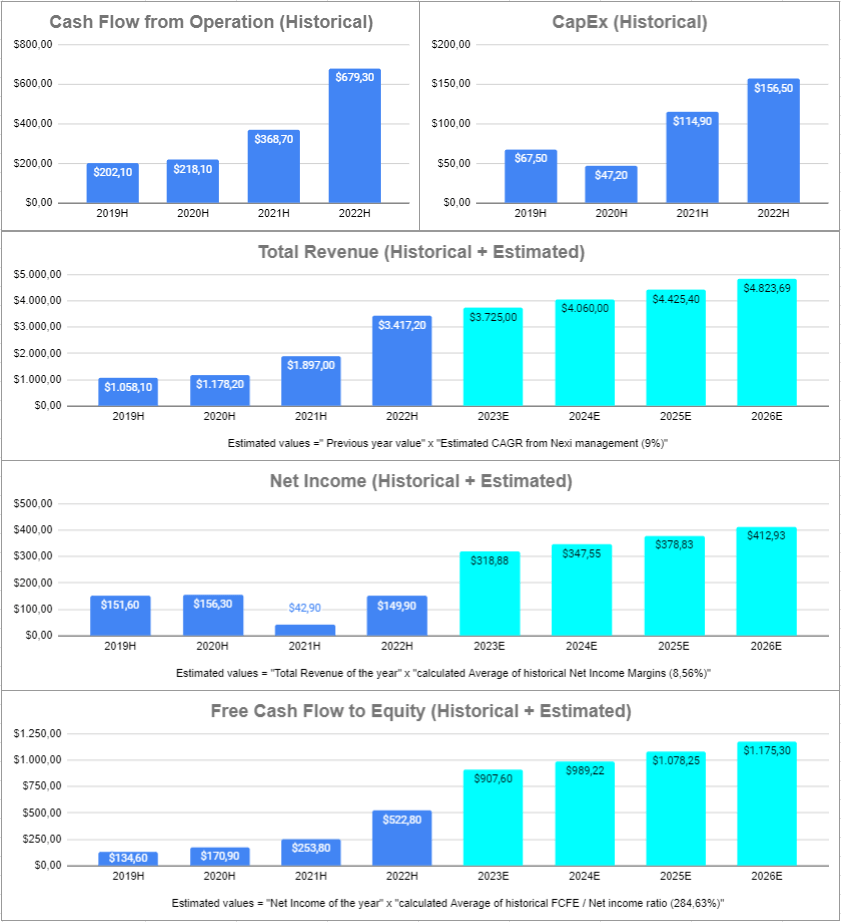

Here’s a visible recap of the principle information used for DCF calculation (each historic, in darkish blue, and estimated, in lighter blue)

Graph from the Writer

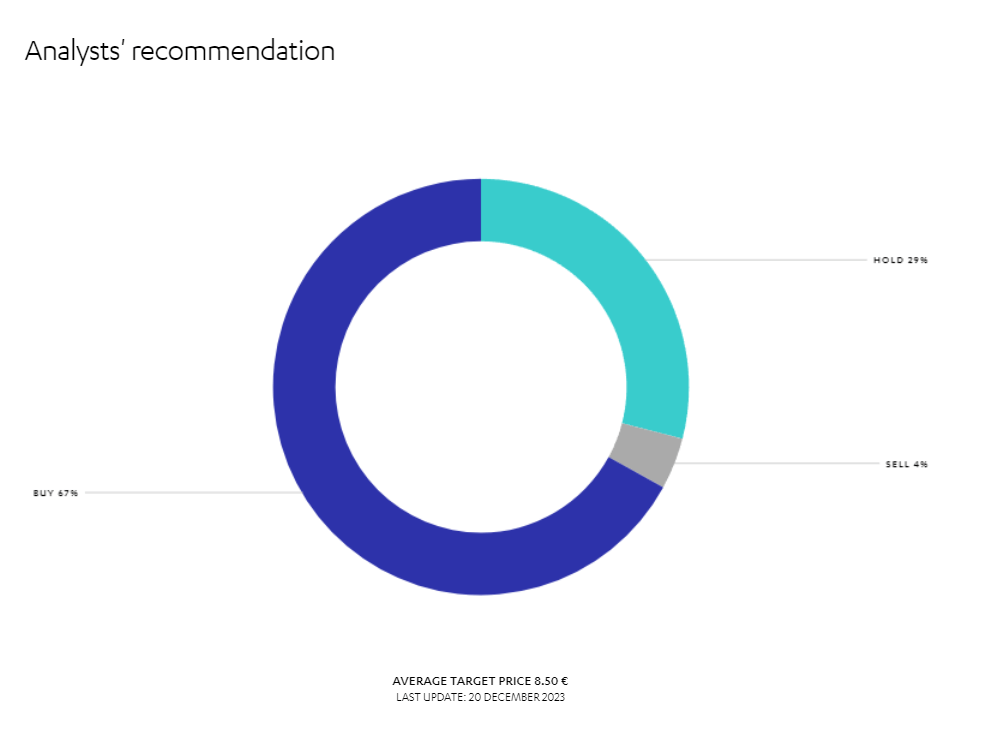

With these values, my DCF mannequin signifies a goal worth of €9.35 (round $10.2 on the present charge), with a reduction to the present worth (€7.11) of round 30%.

The calculated goal is sort of aligned with the typical goal of Wall Avenue analysts (€8.5 as proven within the graph beneath).

Nexi’s web site

If we have now to keep up a “defensive” estimate lets say that Nexi shares are presently fairly properly priced, or perhaps at a small low cost in comparison with their “real” worth.

What’s going to make the distinction (and this justifies my purchase ranking, in addition to the prevalence of purchase rankings among the many analysts within the graph above) would be the respect of the estimates on the rise in Web Revenue and Working Money Stream (CAGR estimated at 20% and 32% respectively); i.e. what I anticipate is, along with an excellent “quantitative” enhance at Income degree, a larger “qualitative” enchancment in revenue margins.

I contemplate these aims fairly reasonable, stating the robust tailwind Nexi can benefit from, and the great “defensive” positioning it has available on the market.

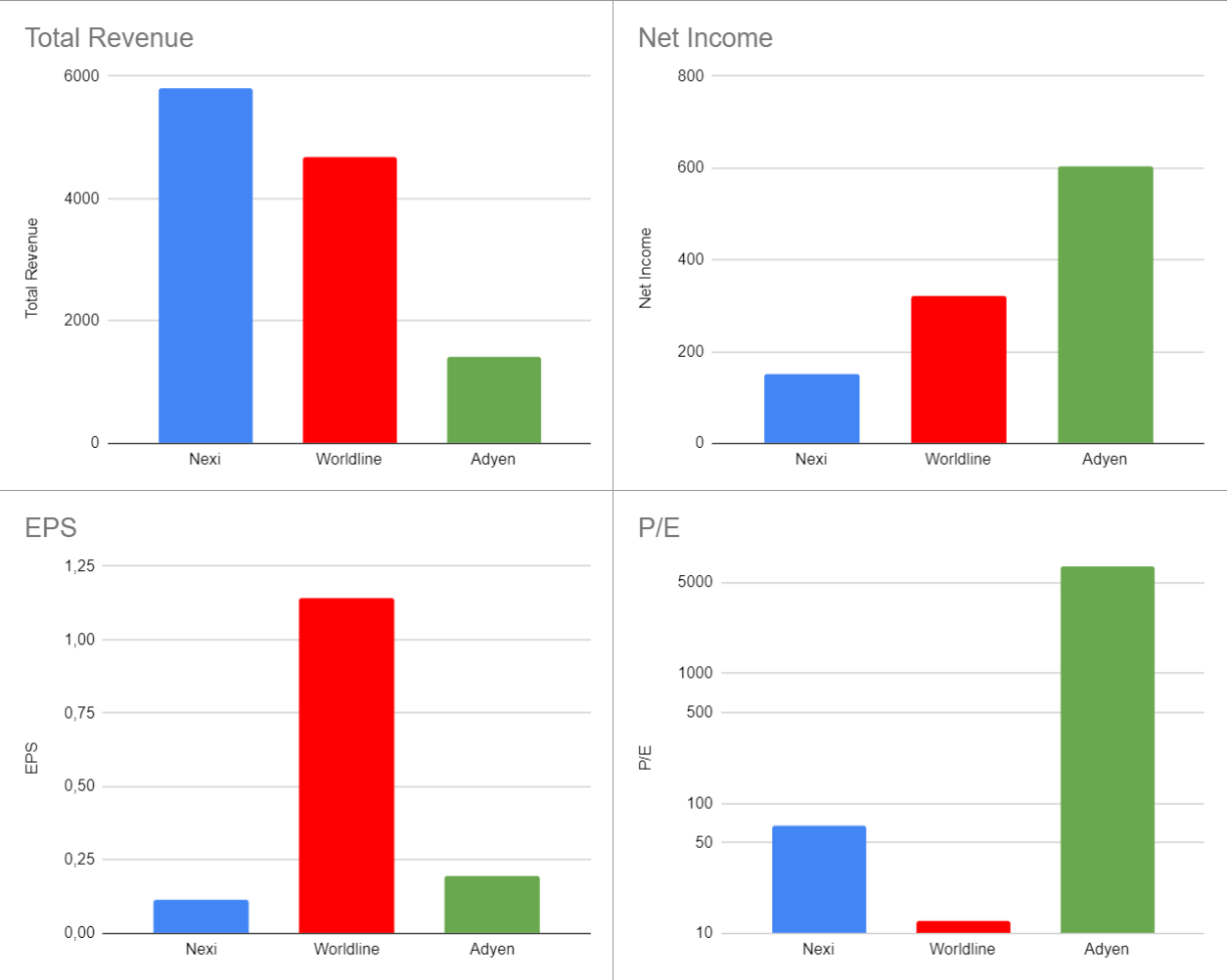

Let’s now examine Nexi’s scenario versus two of the principle European opponents: Worldline and Adyen.

We are going to use information from the final full yr (2022), taking numbers from Searching for Alpha.

As already talked about earlier than, the graph proven is just not supposed to be an analysis of the efficiency of opponents (the info reported must be learn of their context, in a devoted evaluation), nonetheless we will draw some concepts to “frame” Nexi’s place in relation to comparable corporations, for enterprise mannequin and geographical space.

Graph by the Writer, information from Searching for Alpha

As a primary remark, it may be famous that Nexi is properly positioned among the many three by way of income quantity, with an excellent 20% margin over its direct European competitor Worldline (which is a really comparable firm in time period of enterprise mannequin and was, earlier than the Nexi-Nets merger, the undisputed European chief), whereas Adyen presently represents solely a fraction of the market of the opposite two. The scenario adjustments fully with reference to revenue margins, with Adyen declaring a Web Revenue greater than 3 times the Nexi’s one (on a lot decrease volumes, an indication of a theoretically far more worthwhile enterprise mannequin).

Lastly, trying on the P/E ratio, this appears to point a median place between the very conservative analysis on Worldline and the very optimistic one among Adyen (however a lot nearer to the previous).

What I need to finally spotlight is how Nexi has managed to carve out an essential place in its market with the strategic work carried out lately and with essential financial investments; now could be the time it could possibly begin to “capitalize” its place. The development in monetary “margins”, if forecasts are met, will make the corporate far more enticing to the market.

The Street Forward

As we have now seen, I imagine that Nexi’s present monetary scenario represents an excellent place to begin to start, within the medium-short time period, a section of enchancment of financial margins which must also have constructive implications for buyers.

What I need to do now could be to show how Nexi couldn’t solely be an organization with good development margins, but it surely will also be positioned a lot better than different sectors to defend itself from the attainable financial and geopolitical crises that might await us in 2024 and within the following years.

I’ll make a brief checklist of some macro occasions that might create turbulence within the financial system within the close to future, ranging from those who I contemplate most believable as much as probably the most distant (however nonetheless attainable) circumstances.

-

Volatility within the US market because of the presidential elections

Nexi is a European firm and, as we have now already seen, Nexi’s enterprise is totally targeted on Europe. If we’re going to have a powerful enhance in volatility within the US for political causes this might be transmitted for certain additionally to the European markets, however no less than on the elementary degree, there shouldn’t be monetary penalties for Nexi both because of the elections or to any reglementation swing within the occasion of a “changing of the guard” within the US authorities.

-

Worsening geopolitical crises (Ukraine, Center East, Taiwan…)

Additionally on this case, the geographical positioning of Nexi’s enterprise ought to assure a sure immunity from geopolitical turmoil exterior Europe (no less than till they keep exterior of the EU space); then, as a monetary firm, Nexi could be very little depending on issues associated to chip provides, freight transport, worth of oil, and so on.

-

Financial recession / Arduous-landing

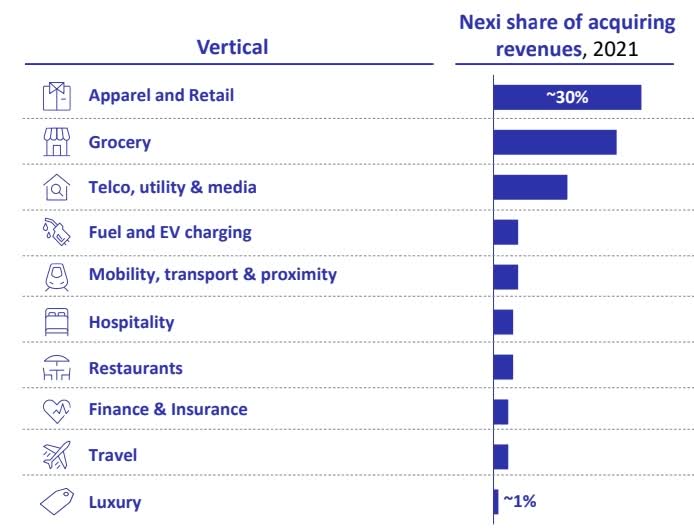

That is most likely probably the most unfavorable case for Nexi: it’s clear {that a} recession state of affairs will inevitably trigger a decline in client spending, particularly within the discretionary sector, and this might trigger a drop in income for Nexi. It’s also essential to have in mind the truth that from this standpoint, the European market has proven indicators of larger weak spot in comparison with the US market, and subsequently a attainable “hard landing” might hit Nexi’s market tougher. However, we should remember the fact that greater than half of the transactions processed by Nexi are within the attire, retail, and grocery sectors, “defensive” sectors by nature, and the place customers might cut back spending solely as much as a sure level.

Nexi’s “Winning in Merchant Solutions” Presentation

Moreover, virtually 40% of Nexi’s revenues come from “fixed” revenue, not depending on the volumes of transactions processed however from contracts linked to subscriptions, POS month-to-month or annual rental charges, playing cards fastened fee, and so on. subsequently a lot much less impacted by a basic decline in consumption.

Nexi’s 2022 Full Yr Outcomes Presentation

Additionally on this case, the best dangers for Nexi might come from a attainable drop in client spending: if persistent inflation had been to cut back folks’s buying energy, this might flip right into a scenario of generalized drop in consumption, with penalties (and arguments) just like what we have now already seen.

Quite the opposite, inflation shouldn’t have “direct” penalties on Nexi’s enterprise, which is solely “financial” and shouldn’t be troubled (or in any case in a really restricted approach) by issues associated to the costs of products, transport, and so on.

As already talked about, Nexi is a purely monetary firm, subsequently it has no issues associated to the provision of supplies for its actions, moreover, it often offloads the credit score dangers for its cost playing cards on companion banks, subsequently it’s not topic to delays in cost for any motive.

Conclusion

I believe Nexi is a stable firm, that has seen virtually steady development lately, each in monetary phrases and market volumes, and which has a terrific management place within the European market.

Dangers that must be highlighted embrace the precise unhealthy market scenario (for the inventory’s latest previous and for the potential of an incoming recession in 2024), and the dearth of geographical diversification (I’m referring specifically to the very excessive dependence on Italy, financially and politically). Lastly, an additional danger is Nexi’s robust dependence on the connection with companion banks, with a big a part of the income coming from contracts with them.

Even when these dangers are points to be monitored, for now, I see Nexi as a wonderful buy alternative, as a result of I discover the present share worth an excellent level of entry on an organization properly positioned, after the essential investments of latest years, to essentially begin to enhance earnings from a powerful main place which might be troublesome to erode.

Editor’s Be aware: This text discusses a number of securities that don’t commerce on a serious U.S. trade. Please concentrate on the dangers related to these shares.