Leonardo Penuela Bernal/iStock via Getty Images

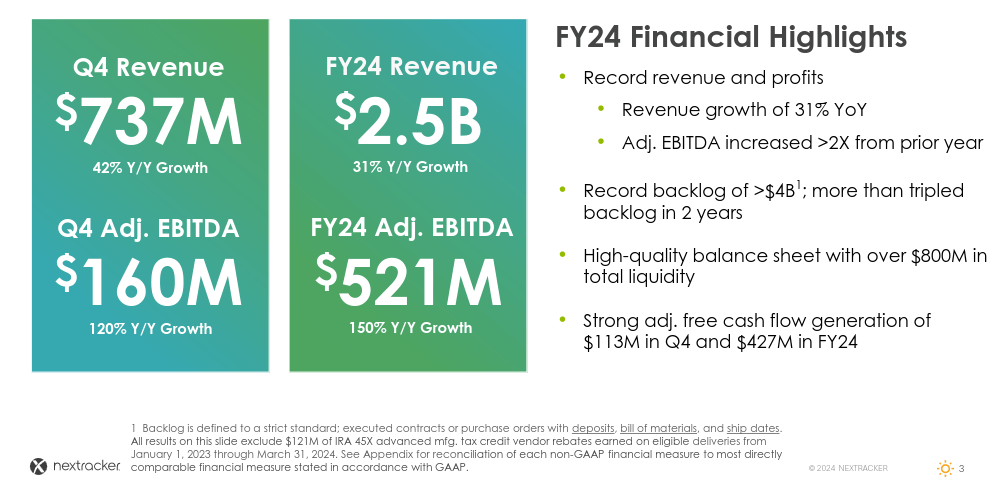

Nextracker (NASDAQ:NXT) just reported an impressive quarter with revenue growing 40% year-over-year, and adjusted EBITDA doubling despite the results excluding the significant IRA 45X tax credit benefits. Nextracker also reported record international revenue in Q4, delivering close to a 90% increase year-over-year. It is rapidly growing in markets such as India, Australia, Europe and Brazil. This is particularly impressive given the sector headwinds, including the high interest rate environment, high inflation, and supply chain issues.

As we recently discussed in an article about competitor Array Technologies (ARRY), we believe the benefits of adding solar-tracking to utility scale solar projects are increasing. Some of the reasons include higher efficiency panels, which means the benefit of solar-tracking is amplified for the same number of panels. It is also increasingly important to spread energy generation throughout the day, something solar trackers do, which reduces the need for extra energy storage. At the same time, the solar-tracking industry has been successful in reducing the cost of its products, and adding other benefits such as protection from extreme weather like hail storms.

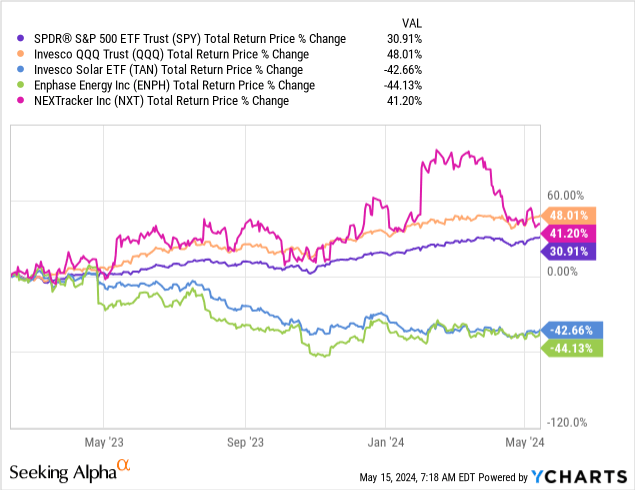

It appears Nextracker is quickly becoming the biggest star in the solar industry. The company was previously a subsidiary of Flex Ltd. (FLEX), but it became a standalone public company after its IPO in February 2023. Since then, it has significantly outperformed the Invesco Solar ETF (TAN), Enphase Energy (ENPH), the S&P 500 index (SPY), and if the current pre-market gains hold, it would also be outperforming on a total return basis the popular QQQ trust (QQQ). It appears we have a new rising star in the solar sector.

Fourth Quarter and Fiscal 2024 Earnings Results

Nextracker delivered solid results, with excellent revenue growth and improving gross margins. Its revenue mix for the quarter was 67% U.S. and 33% rest of the world. Impressively, gross margins for the quarter expanded by more than 10% to close to 30%. The company attributed this improvement to continued efforts optimizing their supply chain and exercising consistent pricing discipline. The company earned adjusted diluted earnings per share of $0.96 in the fourth quarter.

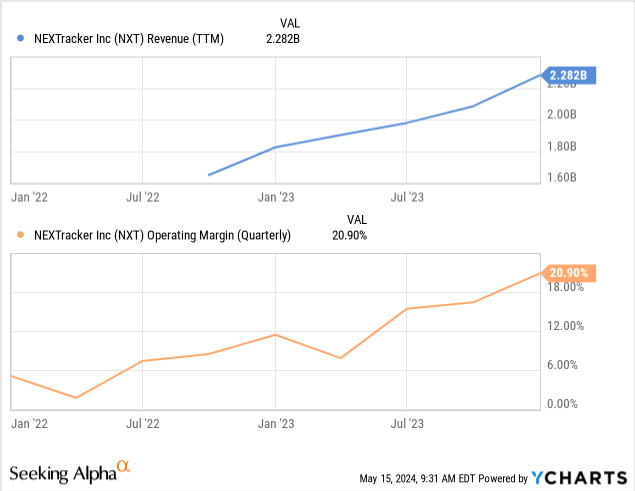

For the whole of fiscal year 2024, revenue was $2.5 billion, up 31%, with the U.S. representing 68% of the mix and the rest of the world 32%. Full-year gross margins expanded to 28% as the company optimized its global supply chain and increased localized content, resulting in lower material and logistics costs. Adjusted diluted earnings per share for the year came in at $3.06, and the company reported its balance sheet has a net cash position. Nextracker closed the quarter with $474 million in total cash, more than three times their total debt of $150 million. During the earnings call, the company also announced that it has successfully expanded its global supply chain to over 50 gigawatts annually, with U.S. capacity now at over 30 gigawatts annually.

Nextracker Investor Presentation

Industry Tailwinds

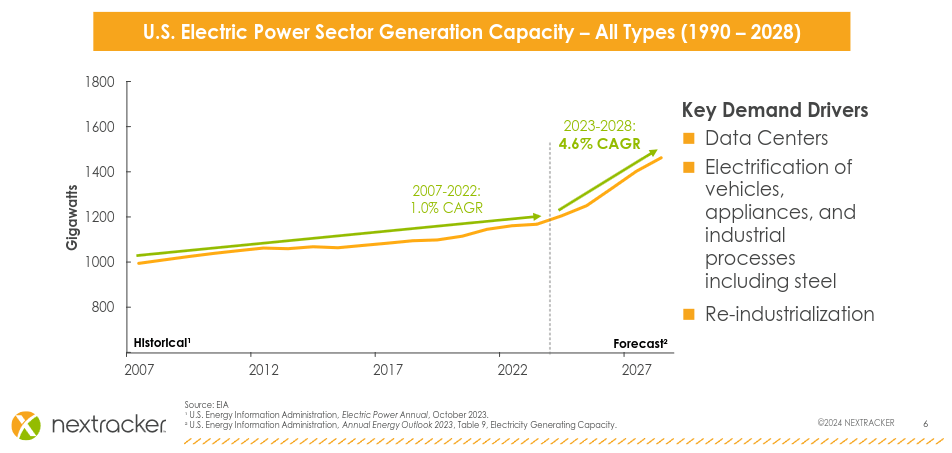

We believe the global clean energy sector will greatly benefit from the expected inflection point in energy demand growth. Very significant power generation capacity will need to be added to meet the rising demand, and most of it is expected to come from renewables. Some of the key demand drivers include data centers, electric vehicles, and the electrification and automation of the industrial sector.

Nextracker Investor Presentation

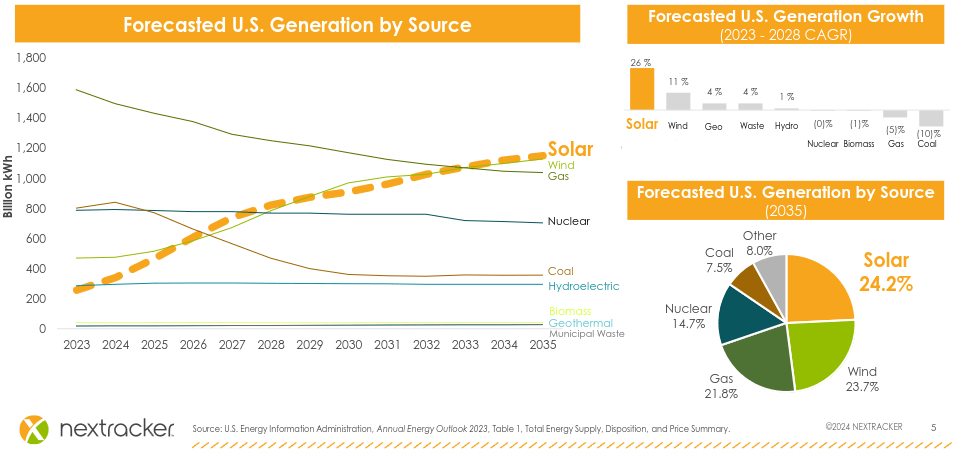

According to the U.S. Energy Information Administration, solar is expected to be the fastest-growing energy technology the next few years, with a 26% compounded annual growth rate (CAGR) over the next five years. This should make it the number one energy source within a decade.

Nextracker Investor Presentation

Innovation and Competitive Moat

One of our key concerns with respect to the solar-tracking industry has been the lack of differentiation and competition focused on prices. Here we are encouraged that Nextracker appears to be finding a way to differentiate itself, and that it appears to be gaining economies of scale that give the company a low-cost producer competitive moat.

A recent innovation announced by the company is a tracker built with a significantly lower carbon footprint, and which is being well received by customers. Other innovation efforts are focused on lowering the cost of production, and maximizing the energy yield. Nextracker offers an intelligent energy yield maximization software called TrueCapture, which, in a similar fashion to what Tesla (TSLA) does, is constantly upgraded through automatic over-the-air updates to customers.

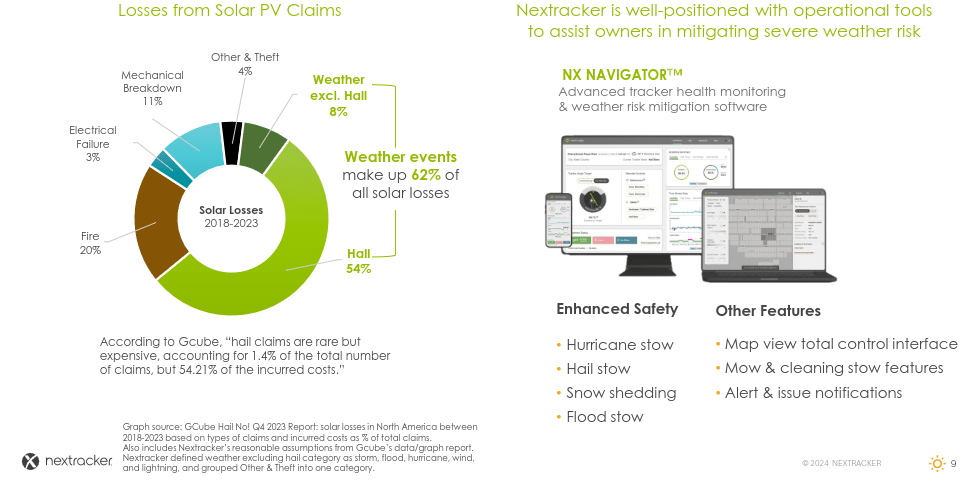

Nextracker shared during the earnings call that over the last two years they have doubled their R&D investments. They also recently opened a third global R&D center in India, which complements their existing R&D efforts in Brazil and Silicon Valley. Some of the innovations include being responsive to extreme weather that could damage the solar power plant. During the call, company president Howard Wenger claimed the company has the industry’s most capable and responsive tracker for severe weather.

On multiple sites and occasions around the world Nextracker Systems have endured extreme wind events reliably while adjacent competitive tracker system suffered extensive and widespread damage. Customers understand that engineering and technology really matter.

The quality and durability of the system is definitely important, as solar plants are often expected to deliver energy for 30 years or more, and they have to withstand tough weather conditions. Given their highly optimized designs, the company claims to have the most bankable product with the lowest levelized cost of energy. Its innovations are also protected by a large number of patents, and Founder and CEO Daniel Shugar explained during the earnings call.

We believe our technologies, protected by over 500 issued and pending patents enable our customers to achieve the best financial returns, because they operate at the lowest levelized cost of energy. We further believe this is achieved because our systems generate more energy and our lower cost to operate and lower risk across a wide range of extreme weather including wind, hail and flooding.

Nextracker Investor Presentation

Financials

Nextracker has been able to deliver profitable growth, with both revenue and its operating margin growing rapidly. This is particularly impressive, as it has been accomplished at a time when other solar companies, including Enphase Energy, SolarEdge (SEDG), and its competitor Array Technologies, talk about significant industry headwinds.

Future Outlook

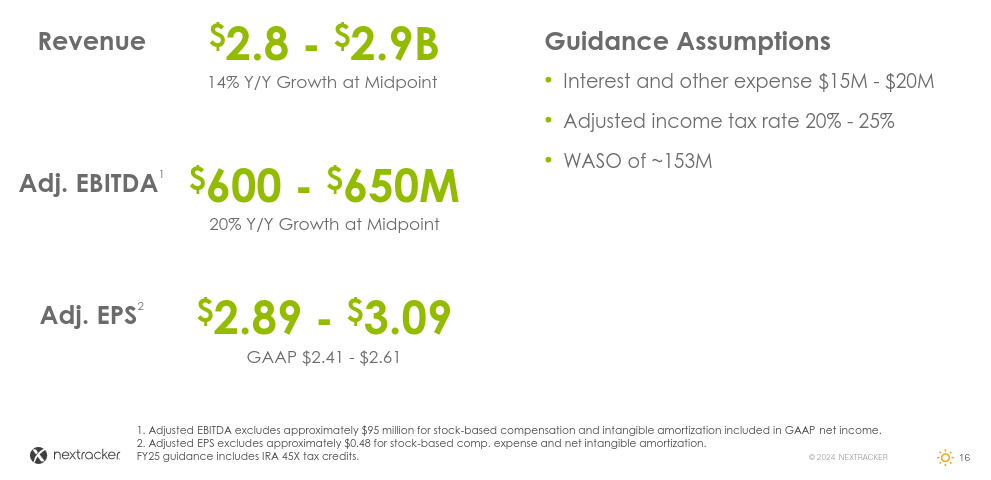

Nextracker shared fiscal 2025 guidance, which includes estimates for IRA 45X benefits, that calls for gross margin to increase to the high-20s. The company expects revenue to be in the range of $2.8 billion to $2.9 billion, and adjusted EBITDA to be in the range of $600 million to $650 million, or roughly 20% year-over-year growth at the midpoint. We appreciate that the company also shared an estimate for GAAP EPS, which is in the range of $2.41 to $2.61. With shares close to $50, that puts the forward Price/Earnings at ~20x.

Nextracker Investor Presentation

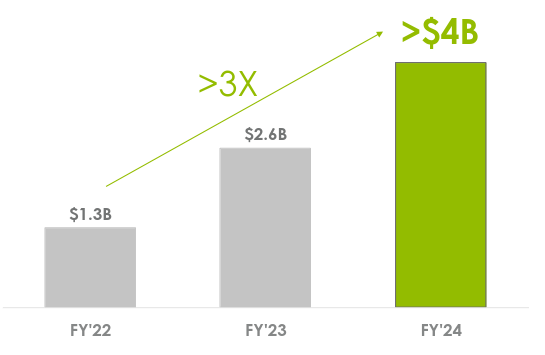

Guidance is backed by a significant increase in its backlog to $4 billion, an increase of more than 50% from last year’s $2.6 billion.

Nextracker Investor Presentation

Valuation

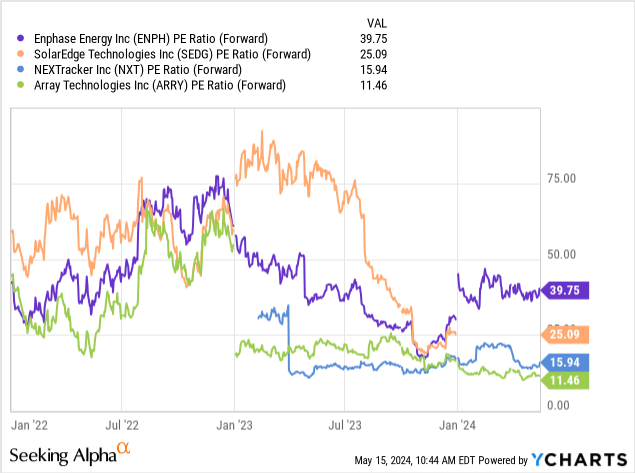

Given its growth potential, we find Nextracker reasonably priced with a forward Price/Earnings multiple of roughly 20x, and a Non-GAAP forward Price/Earnings ratio of about 16x. This is significantly lower than other solar companies like Enphase Energy and SolarEdge, but a premium to competitor Array Technologies. Still, given the rapid growth and improving margins, we believe the premium is well deserved.

Risks

The biggest risk we see is the solar-tracking industry becoming similar to solar panel manufacturers, where they tend to compete on price and their products have essentially become a commodity. We are encouraged by the R&D investments Nextracker is making, and the company appears to be succeeding in differentiating itself and is improving its profit margins. The company also has a solid capital structure, with ample liquidity, low debt, and significant cash and short-term investments that help reduce the risk profile.

Conclusion

Nextracker delivered impressive financial results despite headwinds in the solar sector. We believe the company is a rising star with enormous potential. The company is investing heavily into research and development, and claims it delivers the lowest levelized cost of electricity (LCOE) and highest financial returns for plant owners. Based on its revenue growth, it appears that customers are convinced. Based on fiscal year 2025 guidance, the company is trading at 20x estimated GAAP EPS, which we find very reasonable given the growth potential. We are starting coverage with a “Buy” rating.