magical_light/iStock through Getty Photos

The final time I wrote on (NASDAQ:GLDD), I noticed some indicators of restoration, nevertheless it was nonetheless trying dicey within the brief time period. Nonetheless, I feel now is likely to be the appropriate time to enter the inventory. Because the macroeconomic circumstances are approach higher, GLDD appears low cost now, valuation-wise. So, I’m assigning a purchase score to it.

Monetary Evaluation

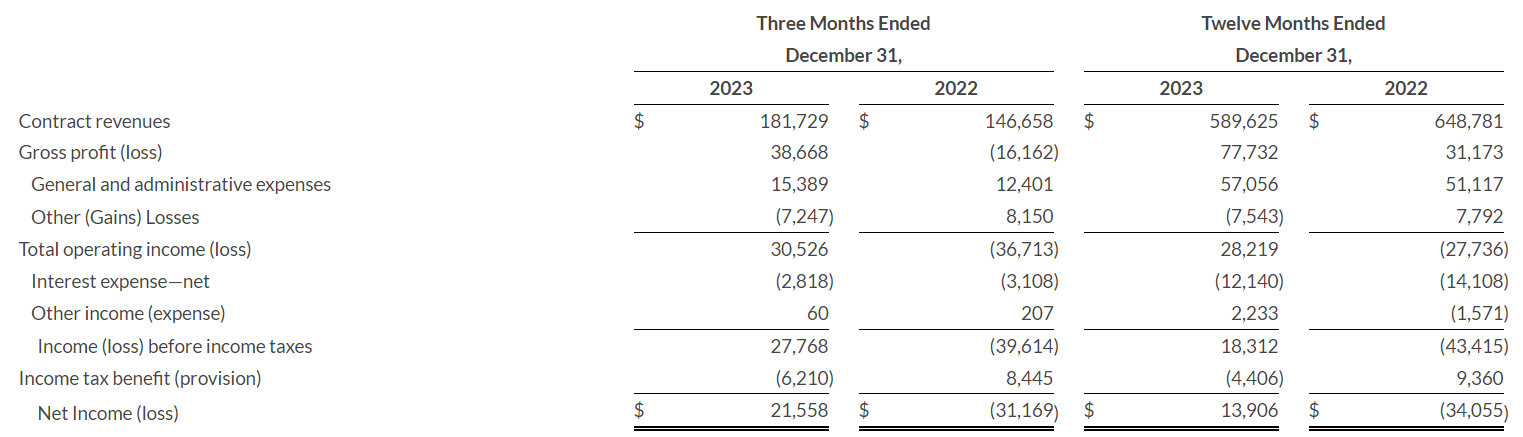

It just lately posted This fall FY23 and FY23 results. The contract revenues for This fall FY23 have been $181.7 million, an increase of 23.9% in comparison with This fall FY22. The primary cause for the rise was elevated coastal safety revenues. The upper coastal upkeep venture income additionally contributed to the rise. The gross margin for This fall FY23 was 21.2% in comparison with a unfavorable 11% in This fall FY22. The numerous enchancment was primarily resulting from higher venture efficiency. Aside from this, fewer drydocking and administration’s give attention to value discount additionally contributed to higher margins. The online earnings for This fall FY23 was $21.5 million, in comparison with a lack of $31.1 million in This fall FY22.

GLDD’s Investor Relations

It confronted unfavorable bidding market circumstances and an adversarial provide chain within the first half of FY23, resulting from which its annual income is decrease in comparison with FY22. Nonetheless, the quarterly outcomes clearly present an enchancment. Its FY23 income declined by 9.1% in comparison with FY22. Nonetheless, profitability improved considerably resulting from administration’s cost-reduction actions. The online earnings for FY23 was $13.9 million, in comparison with a lack of $34 million. The one factor that impressed me essentially the most on this consequence was the advance within the margins. Within the final report, I discussed that it could be fascinating to see if they’d be capable of preserve wholesome margins, and it appears just like the administration has been profitable in sustaining the margins. As well as, the bidding market is now in a greater situation than it was in 2022 and 2023. Its backlog has climbed to $1.04 billion in FY23, in comparison with $377.1 million in FY22. The administration expects round 60% of the backlog to be accomplished in FY24. So, with the easing macroeconomic circumstances and wholesome margins, I consider GLDD can see a turnaround in FY24.

Technical Evaluation

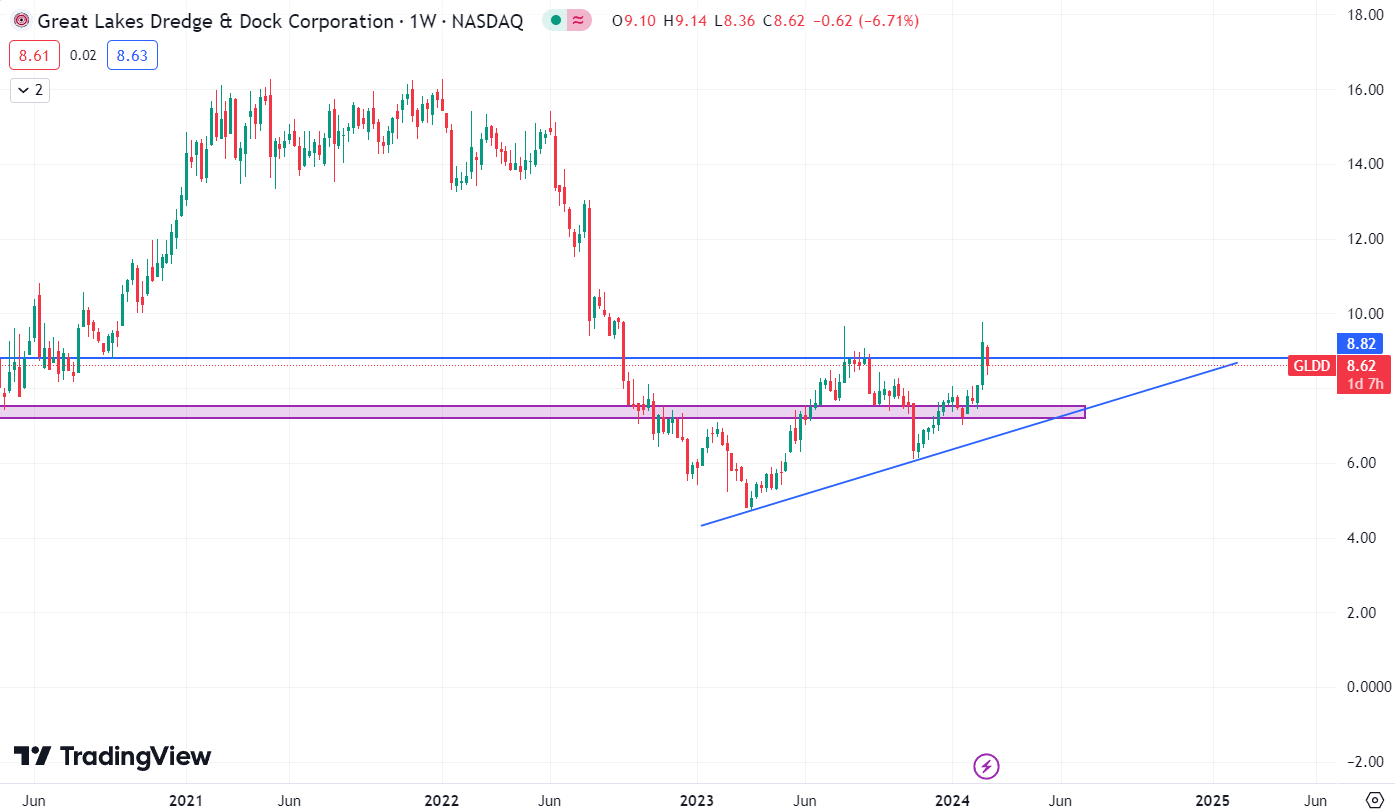

Buying and selling View

It’s buying and selling at $8.6. Just lately, the inventory broke the resistance of $8.8 in a weekly timeframe. Nonetheless, the breakout turned out to be a fake-out, which could look bearish. However I’m not involved concerning the fake-out as a result of if we have a look at the chart, we are able to see that the draw back from the present degree is minimal. The inventory is close to the sturdy assist zone of $7.6, which supported the inventory throughout the Covid crash. It is usually close to the trendline, which has been supporting the inventory since March 2023. Therefore, regardless of the breakout failure, I feel it’s time to accumulate the inventory because it has two sturdy assist ranges. As well as, the upper lows formation means that we’d see a development change within the inventory quickly. Therefore, I feel this is likely to be the appropriate time to build up the inventory.

Ought to One Make investments In GLDD?

GLDD is trying low cost, valuation-wise. GLDD has a P/E [FWD] ratio of 13.52x, which is decrease than its five-year common and sector median of 15.84x and 19.06x, respectively. GLDD is buying and selling at a PEG [FWD] ratio of 1.35x, which can also be decrease than the sector median of 1.76x. So, contemplating the favorable market circumstances, engaging valuation, and technical chart, I feel GLDD could be a good purchase. Therefore, I assign a purchase score.

Threat

Based on their evaluation, the contracts that also must be fulfilled will generate revenues, which is proven of their contract backlog. The money and time wanted to move the requisite sources to and from the venture website, the amount and form of materials that must be dredged, and the anticipated output of the equipment finishing up the duty are the primary components that go into these estimations. These figures, nonetheless, will inevitably differ relying on the precise circumstances. Sometimes, modifications to the scope of tasks could also be made about contracts which are included of their backlog. This might end in a lower within the complete quantity of their backlog in addition to a delay within the realization of income and earnings. As a result of nature of the venture and the timeliness of the precise providers or gear wanted, tasks could also be of their backlog for a substantial period of time. Backlog is just not all the time a dependable predictor of future gross sales or profitability resulting from these and different components that affect the period of time wanted to complete every process.

Backside Line

The administration has efficiently maintained wholesome margins, which is a optimistic signal as a result of its profitability may soar in FY24. The bidding market is now in a greater situation, and the corporate’s backlog has elevated considerably. So, I feel we’d see a monetary turnaround on this inventory, which is able to finally positively have an effect on its share value. Therefore, I assign a purchase score.