Robert Way

Shares in sneaker giant, Nike (NYSE:NKE), were pummeled in the aftermarket hours on Thursday following the release of its fiscal Q4 earnings results. The stock dropped about 12% after pairing a forward guidance cut with an underwhelming sales report.

Heading into the release, shares were already down 17% over the past year, including a 13% loss YTD. The added selling pressure in the after-hours session pulled shares down to a pricing level last seen four years ago during the start of the COVID-19 pandemic.

Seeking Alpha – 1-YR Share Price Performance Of NKE

I had previously expressed bullishness in NKE following a previous bout of market pessimism surrounding inventory levels. That update didn’t age well, given the over 10% decline in the stock since the update.

Nonetheless, I remain bullish on Nike. In fact, I believe the stock is ripe for new or further initiation at current pricing levels, which in my view may be near a bottom for the stock.

What Went Well In Nike’s Earnings Release

Nike’s performance products were a standout during the quarter. If these were the only products on tap at the company, sentiment would have likely been very different following the earnings release. In this category line, Nike reported double-digit growth. Contributing to the growth were Nike’s offerings of basketball apparel and footwear. The partnership with Caitlin Clark could have been a factor here. It could also be beneficial in the periods ahead.

Nike also reported strength in their fitness business, particularly in the women’s category. Statement leggings were up high double digits, according to CEO John Donahoe’s earnings commentary. Women’s fitness footwear also benefitted from strong demand for the Motiva brand. This contributed to market share gains in the category. Looking ahead, commentary was positive surrounding the fall order book. I would, therefore, expect continuing strength in both the performance and fitness product categories in fiscal 2025.

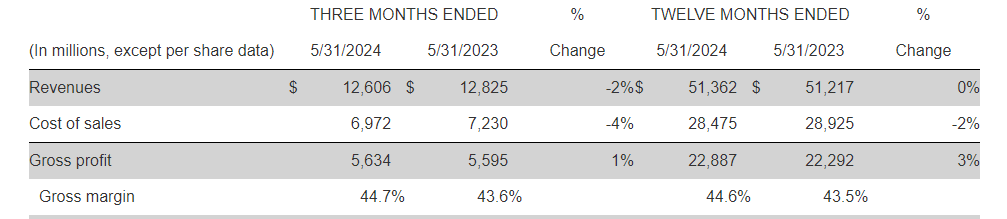

On the earnings front, Nike also reported a 110 basis point (“bps”) improvement in gross margins. This combined with improved SG&A leverage contributed to overall diluted EPS of $0.99/share during the quarter, up 50% YOY, and a consensus topping non-GAAP EPS of $1.01/share.

NKE Q4 Earnings Release – Snapshot Of Comparative Revenue And Gross Profit

What Went Wrong In Nike’s Earnings Release

The strength in Nike’s performance and fitness categories were overwhelmingly offset by weakness in their lifestyle categories. Donahoe attempted to inspire confidence in the category by elaborating on upcoming product initiatives, but this didn’t appear to land as intended with investors.

Nike also reported essentially flat full-year revenue growth, including a 2% decline in Q4, which was fueled by weakness in their digital channels. The company also reported soft traffic trends in their factory stores. This is indicative of the broader macro challenges faced by their value consumers.

Geographically, topline sales were held back by softer sales trends in China. While the region reported revenue growth of 7% during the quarter, much of this was due to an earlier start to the holiday shopping season.

Contributing most to investor disappointment was a dramatic cut to the forward outlook. In providing guidance, CFO Matthew Friend noted that total revenues would be down mid-single digits in fiscal 2025. This represents a significant pivot from previous estimates of sales growth. In addition, he guided for a double-digit revenue drop in Q1 and a high-single digit decline for the first half of the fiscal year. This compares to previous estimates of a more modest decline.

Is Nike Stock A Buy Following Earnings?

Nike is deep in the figurative woods. The company has warned of macro-related challenges and has lowered their full-year outlook accordingly. The lowered outlook is perhaps unsurprising, given that the company’s sales are growing at its most meager rate in decades at just 1% on a full year basis.

Strategic mishaps through the neglect of the running market has also contributed to the rise of Hoka-owner, Deckers Outdoor, a company that has fully capitalized on the market opportunity and is up nearly 100% over the last year. This compares to NKE’s 18% decline over the same period.

In my view, the challenges and the resulting share price weakness present an attractive opportunity for bargain hunters seeking basement bin pricing. Shares dropped to levels last seen four years ago following the after-hours release of its full year results. At current pricing, the stock is trading at about a 21x forward multiple. This is a steep comedown in valuation for a stock that has commanded 30x over the last five years.

Competitive pressures and strategic lapses perhaps justify the lower multiple at this moment in time. But despite its tribulations, Nike is still the top dog in the industry, generating annual sales that are more than double its nearest competitor, Adidas.

Strategic missteps and ongoing share price weakness create ripe conditions for the possibility of activist interest and/or leadership change. Dour forward guidance also sets a low bar for a surprise to the upside. Both possibilities could serve as a catalyst for forward momentum in a stock that appears overdue for a win.

Investors in NKE may presently find themselves deep in the equity woods. Greener pastures, however, may await those willing to see the forest through the trees.