Julia_Sudnitskaya/iStock by way of Getty Photos

We beforehand lined NIO Inc. (NYSE:NYSE:NIO) in September 2023, discussing its blended FQ2’23 earnings name, attributed to the underwhelming prime/ backside strains and the chance of it lacking the earlier FY2023 supply steerage.

We had opted to price the inventory as a Maintain then, because it was unsure if the automaker’s margins may enhance shifting ahead, as a result of intensified gross sales hiring, R&D, and capex for the mass market fashions.

That is on prime of the inventory persistently charting decrease lows and decrease highs, with it remaining to be seen when a flooring may materialize.

On this article, we will talk about why we’re lastly rerating the NIO inventory as a Purchase right here, due to its rising ASPs, rising gross sales, enhancing automotive gross revenue margins, and enhanced monetization methods, with these efforts more likely to reasonable its money burn price forward whereas preserving its steadiness sheet.

Mixed with the pulled ahead mass market mannequin launches, it seems that the worst is already right here, with its prospects more likely to raise from FQ4’23 onwards.

The NIO Funding Thesis Is Very Tempting Right here Certainly

For now, NIO has reported a greater than respectable FQ3’23 earnings name, with automotive revenues of 17.4B Yuan (+142.3% QoQ/ +45.9% YoY) and a recovering Common Promoting Worth of 314.05K Yuan per unit (+2.8% QoQ/ -16.8% YoY).

The latter sum is derived from the automotive revenues and growing deliveries of 55.43K units (+135.6% QoQ/ +75.4% YoY) by September 30, 2023.

The ASPs are improved than the impacted ASPs of 297.18K Yuan per unit recorded in FQ1’23 (-19.3% QoQ/ -17.1% YoY) certainly, implying diminished promotional actions and rising shopper demand for its choices.

This growth has instantly contributed to NIO’s recovering automotive gross margins of 11% (+4.8 factors QoQ/ -5.4 YoY) by the newest quarter, although nonetheless an ideal distance away from its FQ4’21 peak automotive gross margins of 20.9%, due to the ongoing price war lead by Tesla (TSLA) in China.

Moreover, we may even see this worthwhile pattern proceed in FQ4’23, with the projected ASPs of 341.45K Yuan per unit (+8.7% QoQ/ -7.3% YoY), primarily based on the administration’s income steerage of 16.39B Yuan and supply steerage of 48K items on the midpoint.

A part of the margin enchancment tailwind is probably going attributed to the automaker’s full transition to the NT2.0 platform by FQ3’23, with the improved price efficiencies already permitting the administration to information 15% (+4 factors QoQ/ +8.2 YoY) in automotive gross margin by FQ4’23.

Demand for NIO’s EV choices look like wonderful as effectively, attributed to the considerably secure stock ranges of $967.44M (-17.3% QoQ/ +3.1% YoY) by the newest quarter.

October 2023 has additionally introduced forth wonderful supply numbers at 16.07K units (+2.7% MoM/ +59.8 YoY) and November 2023 at 15.95K units (-0.7% QoQ/ +12.6% YoY).

Whereas the YTD sum of 142.02K items (+33.1% YoY) and up to date FY2023 supply steerage of 158K items (+29% YoY) falls behind the administration’s earlier steerage of 250K items (+104.1% YoY), we already applaud the reasonable enhancements noticed in its automotive gross margins.

This pattern could also be additional aided by the launch of NIO’s affordable EV line up within the EU, particularly Alps from Q3’24 and Firefly from 2025 onwards, seemingly to enhance its mass attraction and adoption, boosting its top-line efficiency within the intermediate time period.

For context, the automaker at present costs its flagship fashions at between €50K to €91K within the EU, with a view to compete with many different legacy premium automakers, comparable to BMW (OTCPK:BMWYY) and Mercedes-Benz (OTCPK:MBGAF).

Whereas the NIO administration has but to disclose the listed costs, the sub manufacturers are rumored to convey down the Common Promoting Worth vary to between €12.95K and €25.90K for the base-range Firefly EV fashions (primarily based on the FX price on the time of writing).

That is nearer to Toyota’s (TM) Lexus value vary, implying a drastic -72.4% low cost on the midpoint.

At the moment, NIO’s Alps is rumored to supply mid-range EV fashions, at an estimated value vary of between €25.90K to €38.84K, suggesting a beautiful -54% low cost from its premium vary on the midpoint.

With Alps already being examined on the roads in China, it seems that the rumors could also be proper in any case, triggering the automaker’s intermediate time period tailwinds.

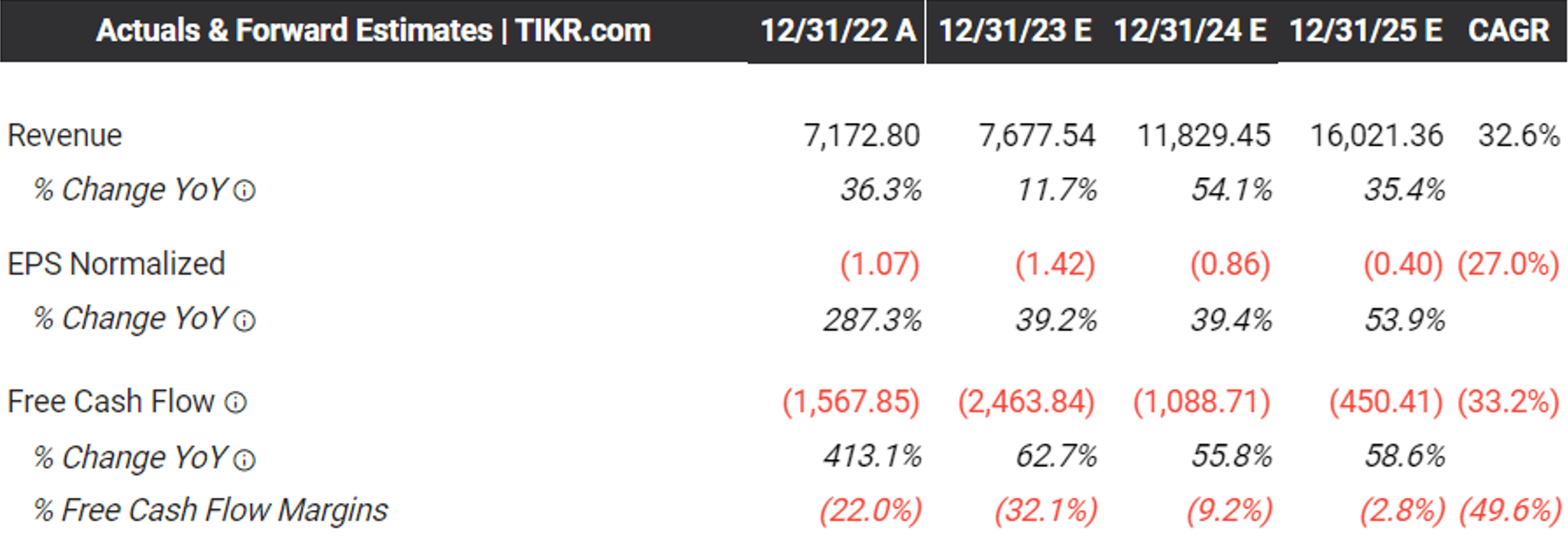

The Consensus Ahead Estimates

Tikr Terminal

Maybe that is why NIO remains to be anticipated to generate a strong top-line progress at a CAGR of +32.6% by means of FY2025, constructing upon its historic progress at a CAGR of +77.6% between FY2018 and FY2022.

Whereas the automaker just isn’t anticipated to interrupt even over the subsequent few years, we’re not overly involved since its steadiness sheet stays strong, with a money/ short-term investments of $5.33B by the newest quarter (+39.1% QoQ/ -15.2% YoY).

Assuming that NIO is ready to proceed rising its gross revenue margins forward, we consider that its quarterly money burn price of roughly -$600M might decline from henceforth, permitting it to reasonably develop its operations forward.

If something, the administration can also be exploring a number of paths to enhance its margins and liquidity forward.

Firstly, NIO has acquired sure tools and belongings for 3.16B Yuan from its present manufacturing accomplice, JAC, on December 5, 2023, with the train anticipated to enhance its high quality management whereas bringing its general manufacturing prices down by roughly -10% in the long term.

Secondly, the administration has introduced its partnership with Changan Vehicle and Geely Holdings Group (OTCPK:GELYF), permitting the 2 Chinese language automakers to make the most of NIO’s battery swap community for a charge, with a number of others already in negotiation.

This technique is considerably just like TSLA’s opening up of the Supercharger community within the US, permitting the corporate to boost its monetization price by means of “access fees & revenues from different OEMs.”

Lastly, there are already market rumors of NIO probably spinning off the battery production unit/ swapping know-how as a separate unit, with the train more likely to convey forth extra liquidity for the dad or mum firm.

Because of this, we’re cautiously optimistic in regards to the automaker’s intermediate time period prospects, with liquidity unlikely to be a serious concern.

So, Is NIO Inventory A Purchase, Promote, or Maintain?

NIO Valuations

Searching for Alpha

For now, since NIO stays unprofitable, the one metric that we might use to measure its valuations is the FWD EV/ Gross sales of 1.74x.

This quantity seems to be considerably cheap, after the a lot wanted correction from the pre-pandemic imply of three.16x and the hyper-pandemic peak of 23.14x, nearer to the sector median of 1.27x.

That is particularly since NIO is predicted to generate a powerful top-line progress shifting ahead, well-exceeding TSLA’s projected progress at a CAGR of +21.5% with a FWD EV/ Gross sales of 8.04x, and nearer to XPeng’s (XPEV) price of +41.7% over the identical time interval with a FWD EV/ Gross sales of two.93x.

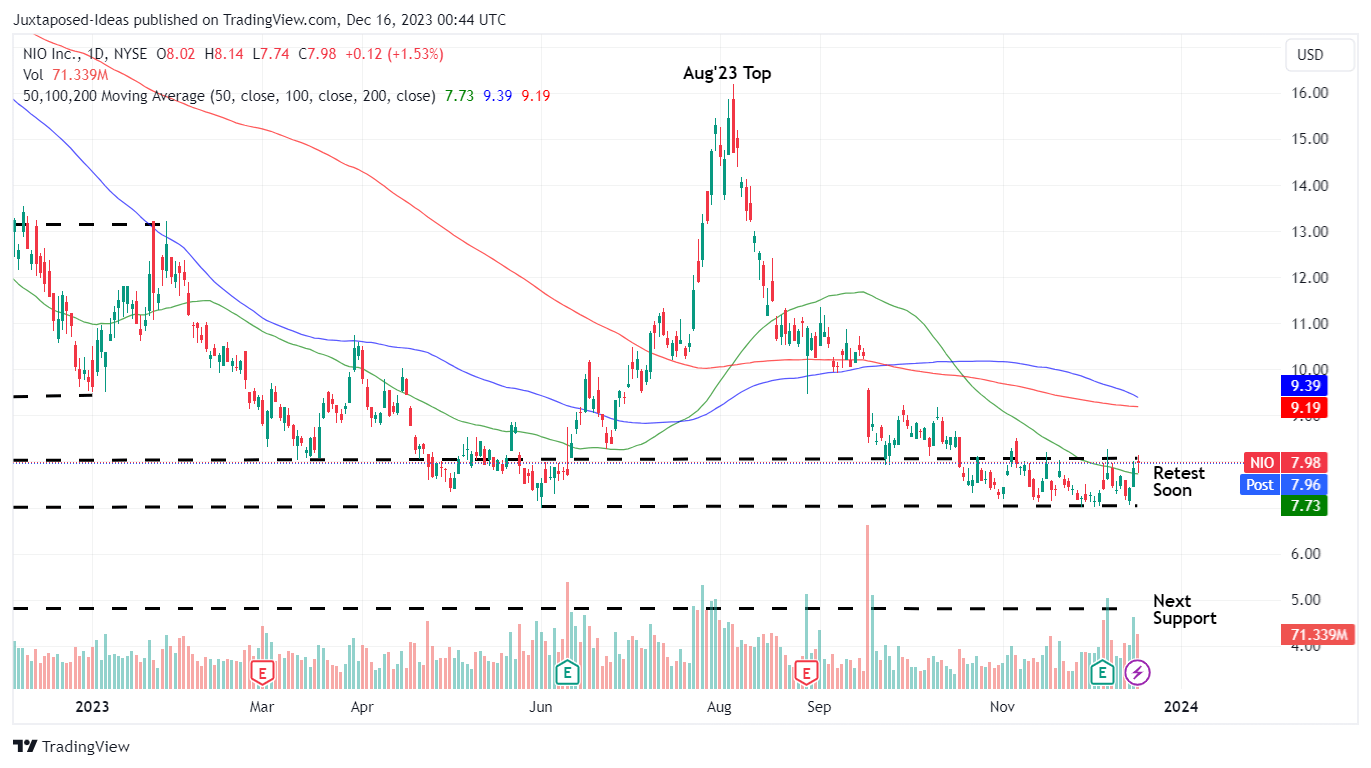

NIO 1Y Inventory Worth

Buying and selling View

The NIO inventory can also be buying and selling beneath its earlier resistance ranges of $8s, with it showing to be effectively supported at $7s. Because of its engaging valuation and potential reversal in FQ4’23, we’re cautiously rerating the inventory as a Purchase right here.

Nonetheless, buyers should additionally dimension their portfolios in accordance with their threat urge for food, for the reason that inventory data an elevated brief curiosity of 10.69% on the time of writing, with the long run upside potential more likely to be negated by aggressive brief sellers.