BackyardProduction

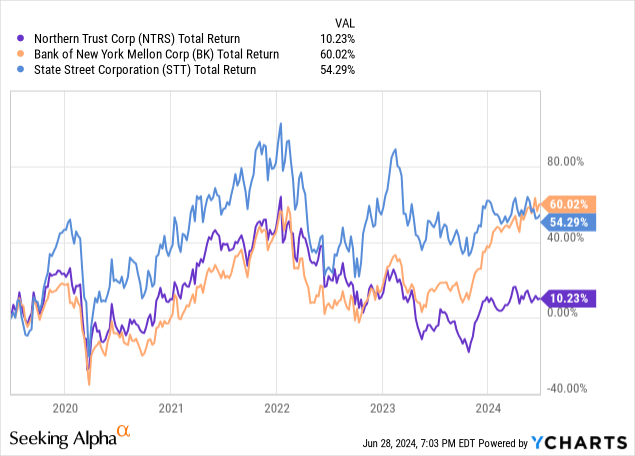

Declining underlying profitability can often drive particularly poor investment returns, as not only does this often result in stalling (or worse) earnings growth, but also a downgrade in valuation multiples applied by the market. Custody bank Northern Trust (NASDAQ:NTRS) has arguably fallen into this trap in recent times. The stock’s circa 10% five-year total return is not just bad in absolute terms, but is also poor compared to close peers State Street (STT) and BNY Mellon (BK).

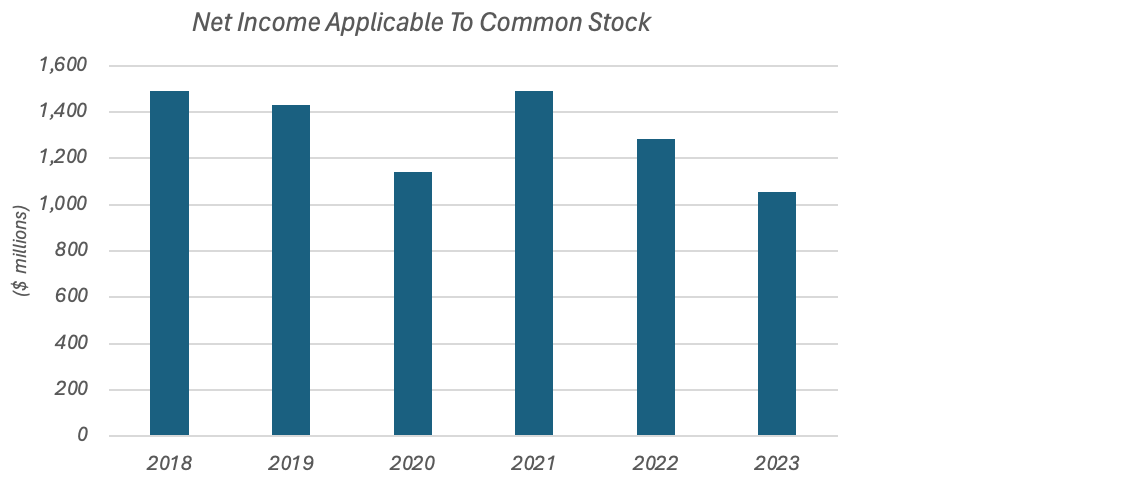

Northern has indeed struggled to grow earnings in that time. While the headline fall in net income available to common shareholders is not as dramatic as it looks on paper (FDIC special assessment charges and realized losses on the sale of investment securities have depressed earnings recently), it would still be generous to say that net income has been sluggish even after normalizing for one-offs.

Data Source: Northern Trust Annual Reports

More to the point, this has occurred on a growing capital base. Tangible book value per share (“TBVPS”) is up around 25% in that time, implying a contraction in Northern’s return on tangible common equity (“ROTCE”). Given that, it’s perhaps not surprising that the market has taken a dimmer view of the stock, with Northern’s P/TBVPS multiple contracting from around 2.2x five years ago to ~1.65x currently. Multiple re/de-rating can often be a source of unjustified gains/losses, but in this case I’d say it looks fair.

While this has ultimately resulted in a rough ride for Northern’s shareholders, the stock does appear more reasonably valued today as a result, offering investors circa high single-digit annualized returns assuming the bank can hold its current profitability steady and put on modest earnings growth. That’s not bad given Northern arguably operates a more stress-free business model compared to ‘regular’ banks, though given its headwinds I would want to see a slightly larger margin of safety before being a buyer here.

Battling Away Against Secular Trends

As mentioned, Northern Trust isn’t really a traditional bank in that it makes much of its income through asset servicing and wealth management fees. While it did have around $144B in interest-earning assets at the end of last quarter (including $47B in period-end loans), net interest income (“NII”) was only ~32% of its revenue in Q1.

Custody & Fund Administration accounted for around 26% of Northern’s revenue last quarter. As the name implies, this includes fees for the safekeeping of the assets of mutual funds, pension schemes and so on. This service provides a nice utility-like source of revenue for the bank, but fee margins have come under pressure from ongoing secular trends, chiefly asset managers being forced to lower their own charges in light of the rise of cheaper passive solutions like ETFs. This collective belt tightening has had a negative knock-on effect for service providers like Northern.

With that, assets under custody/administration (“AUC/A”) in Northern’s Asset Servicing segment have risen by around 50% over the past five years (to ~$15.4T as of Q1), but Custody & Fund Administration fees have only risen by around 16% over the same timeframe (to ~$437M in Q1). Not all of these fees are directly linked to asset levels, but fee margin pressure has nonetheless been a large driver of this disconnect.

While management prefers to compare fee income to expenses (rather than AUC/A levels), Northern hasn’t really been doing well on this score either. Non-interest expense growth outpaced revenue growth by around 15 percentage points over the past five years (and that excludes the FDIC special assessment charge last year), with the bank’s expense to trust fee ratio up to 119% last quarter from around 110% in Q1 2019. Having said that, inflation has been unusually hot recently, and normalization on that front should help alleviate some of this cost pressure.

It’s Not All Bad

The above amounts to a fairly significant set of negatives, but it’s not all bad here. For one, Northern does have a good wealth business, albeit pre-tax margins have slipped a little in recent years on negative operating leverage. Still, there are some bright spots, including in Global Family Office, where fee income has been growing at a high single-digit annualized clip. Northern’s wealth business does skew heavily to high and ultra-high-net-worth clients, and these groups have been growing wealth faster than other segments. Assuming that trend continues, Northern could stand to benefit.

Additionally, Northern doesn’t really come with some of the worries that other bank stocks do. Earning assets skew toward cash and securities, while the loan book is generally quite conservative. Net charge-offs only peaked at around $140M in the Global Financial Crisis (versus a then-loan book of around $28B), with credit risk a bit lower on the list of things to be concerned about here compared to normal banks. Perhaps relatedly, Northern was one of only two S&P 500 banks to avoid cutting its dividend during that downturn (M&T Bank (MTB) being the other), and that kind of consistency can appeal to more conservative-minded investors.

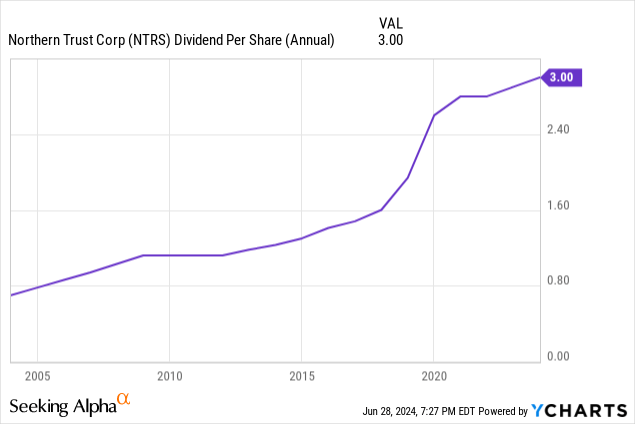

I do expect the bank to continue to be pretty active in returning cash to shareholders. Northern has paid out around 45% of reported net income by way of dividends over the past five years (based on reported earnings, so a little lower on normalized levels), while buybacks have been another 30%-plus of net income. I don’t see any reason why Northern won’t maintain a fairly high total payout ratio going forward.

Valuation

While Northern Trust is arguably a decent “sleep well at night” stock, at least relative to the wider banking sector, to a large extent this is also reflected in its valuation. At $83.98 currently, the shares trade for around 1.65x first quarter TBVPS (my preferred metric for banks), or 1.53x plain book value per share (management’s preferred metric and the one disclosed with results). This would put the P/E at around 12x based on Northern’s recent underlying ROTCE (in the low-teens area).

With that, Northern doesn’t have to move mountains to justify its current price, with low single-digit annualized earnings growth and a stable low-teens ROTCE enough to clear a 9% cost of equity. That’s not a bad outlook, and conservative investors may be content to trade away some upside for a slightly less bumpy through-the-cycle ride, though it’s unlikely to excite most readers. Moreover, there is a chance that even this relatively modest outlook proves a tad optimistic given the bank’s long-term headwinds.

Summing It Up

Fee margin pressure and the resultant negative operating leverage has been an issue for Northern Trust for a while now. With the market walking down its multiple of TBVPS as a result, shareholders have paid the price with very lackluster returns in recent years.

At around 1.65x TBVPS, Northern Trust isn’t aggressively valued by any means, with low single-digit growth and a stable low-teens ROTCE pointing to high single-digit annualized returns for investors. Although not bad, this still doesn’t clear the 10%-plus hurdle that many readers will seek, while conservative-minded investors who might otherwise be happy to swap some upside for lower earnings volatility still face the risk that Northern’s travails aren’t over just yet. Given that, I would be looking for a larger margin of safety before being a comfortable buyer here.