bjdlzx

Pricey readers/followers,

Previously few months, about half a yr, I have been pushing cash to work in a brand new undervalued sector of the market – that sector being the utilities sector, particularly US utilities that present undervaluation. European utilities, corresponding to Enel (OTCPK:ENLAY) have proven important undervaluation for fairly a while – however that’s now additionally the case with their American counterparts. This undervaluation has now additionally develop into fairly pronounced over the previous few months. The corporate which I’m going to overview right here has in reality dropped over 20% for the previous yr.

There are causes for this. We’ll undergo them right here. However I need to make it clear that I’ve been investing extra capital into corporations like Black Hills (BKH), Ugi Corp (UGI), Evergy (EVRG) and different utilities – even purchased again some Fortum (OTCPK:FOJCF) at under €11/share.

Utilities and low cost, qualitative telecommunication shares proceed to make up a stable portion of my funding portfolio – as a result of whereas I do make investments a good sum of money into “riskier” performs, absolutely the majority of my funding capital goes into very conservative and risk-adjusted dividend shares with 10-17% annualized upside with a stable dividend.

On this article we’ll take a look at Northwest Pure (NYSE:NWN).

Northwest Pure – Why it is a nice utility to put money into

Utilities are fascinating corporations. I’ve been protecting them since I began writing on In search of Alpha a few years in the past, and I proceed to make them a considerable a part of my protection.

This explicit enterprise is just not in reality an enormous one. Northwest Pure, or NWN, is an A+ rated (the primary optimistic) firm with a sub-50% Lengthy-term debt (the second optimistic) in its fundamentals, and a dividend yield of over 5.4% (the third optimistic) that’s coated with a really conservative payout (the fifth optimistic).

So already going into this enterprise, you possibly can see that there are many issues to love about Northwest Pure.

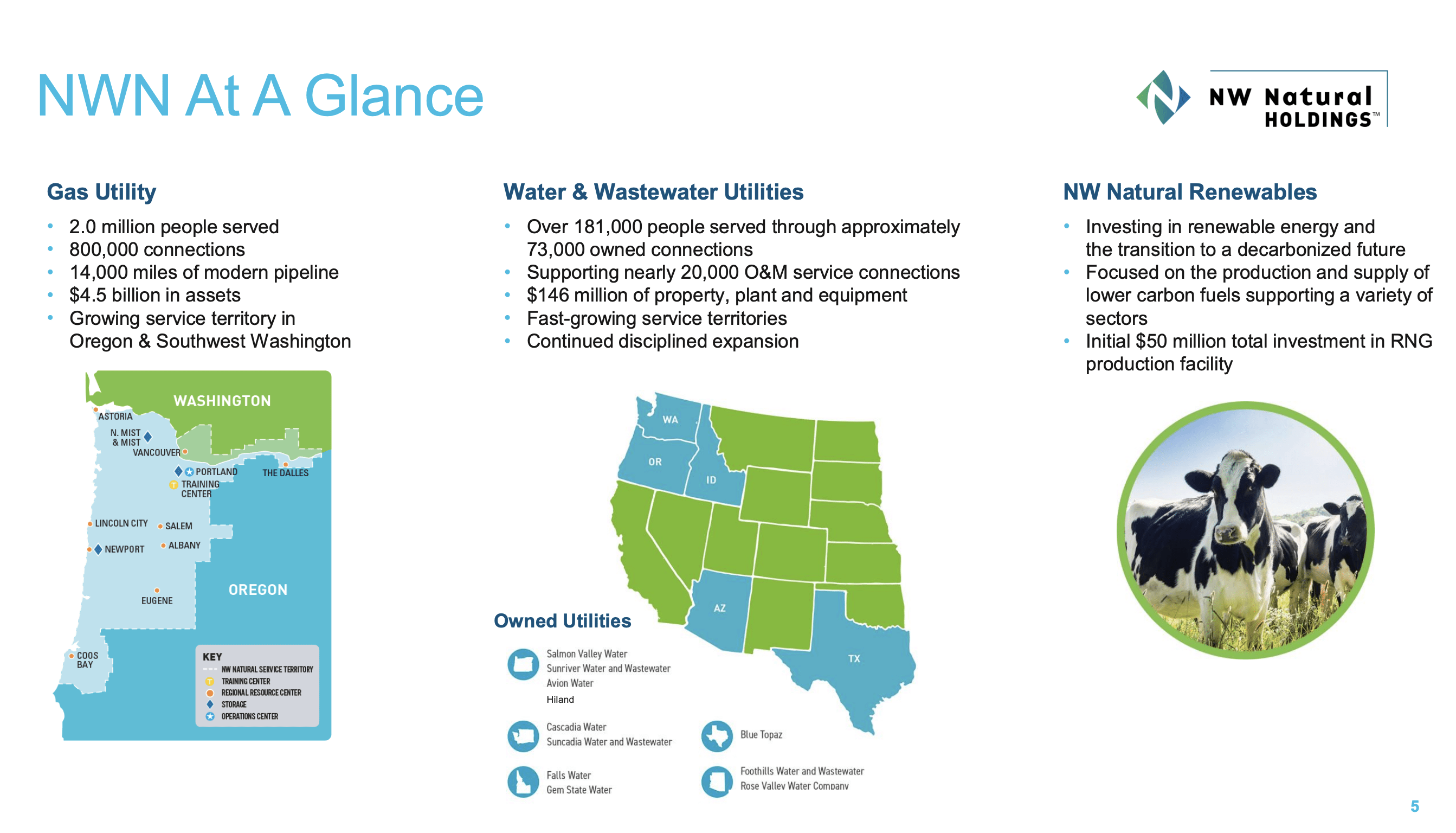

NWN is categorized as a gasoline utility. As an organization, it serves 2 million individuals with 800k connections, managing 140k miles of pipelines.

The place precisely does the corporate do that?

Principally within the Oregon and Southwestern Washington state areas.

However this isn’t all the corporate does.

Northwest Pure IR (Northwest Pure IR)

The corporate additionally owns substantial property in Water & Wastewater, with as you possibly can see, tons of of 1000’s of shoppers throughout an excellent bigger geography – and very like different water corporations, this enterprise is rising these service areas with the acquisition of latest companies the place that is attainable, including inorganic development to its profile.

So – a really fascinating mixture of gasoline and water.

I imply, the corporate additionally does have a renewable arm, as you possibly can see with the pure renewables section – however at a $50M funding that is so small that I do not imagine it’s greater than value mentioning. In order that out of the way in which, let’s transfer on.

Being a water and gasoline firm, NWN is topic to very steady margins within the water sector, with considerably extra volatility within the gasoline utility sector. In gasoline, the primary results are climate, decoupling, and environmental prices in addition to restoration mechanisms and the automated adjustment clauses for renewable gasoline in some states, like Oregon. The corporate views its relationship with the working regulators as constructive, and over the previous few durations has largely managed to get its needs and calls for by way of in a great way.

That is extraordinarily regulated as a enterprise, and whereas water remains to be small when it comes to revenues (solely 5% as of but), the shopper profile may be very engaging, with many of the clients (over 60%) residential.

Like most of the corporations within the residential house, NWN targets an annual price of EPS development between 4-6% – mid-single digit. It is also one thing that many of those corporations haven’t got a problem managing, which additionally provides them the flexibility to pay a rising and engaging dividend.

NWN grows, as I’d say, slower than the typical, with lower than 1%. It is a mixture of inorganic additions by way of the water section at a gradual price, in addition to working in areas that are not essentially among the many most engaging within the US to dwell in. We’re not speaking about Texas or Florida, we’re speaking about Oregon and Washington.

The corporate has a going capital plan of between $1.4-$1.6B which does not sound like a lot in comparison with one thing like Enel, however is far when you think about that the corporate would not have a market cap above 1.4B USD.

A lot of the firm’s investments are earmarked for investing in new Meters for gasoline, services for Fuel, security and reliability for the gasoline community, and controlled RNG investments. Solely a small quantity for the subsequent few years is estimated to be put into the water section.

When it comes to its capital state of affairs, NWN has entry to over half a billion {dollars}, which explains its A+ score, with the senior unsecured debt even at an AA-/A2 score.

NWN has a historical past of 165 years of service. It is the most important distribution firm in the entire Pacific Northwest, and it has good buyer satisfaction scores (Supply: J.D energy).

The enterprise mannequin for a utility like that is extremely resilient. Headwinds from the general ranges of rates of interest are type of over presently, with the lows coming final yr and final summer time.

The first challenges to this utility are available in two varieties, as I see it. First, the corporate is not rising as quick because it has. It is in reality slowing additional, with solely sub-1% development charges, and the corporate is clearly speaking that that is partly due to a inhabitants decline. That is by no means a optimistic. Secondly, it is infrastructure CapEx and hardening bills are popping out of a slower-growing price base, which has necessitated tapping debt. The corporate is not massively extremely leveraged, but it surely’s extra indebted now than it was previously. To that we have to contemplate dangers like climate and such issues – however these are issues that have an effect on each utility, not simply NWN (even when NWN’s working areas may see hotter climate).

Investing in utilities has for the longest time not been a highly regarded type of avenue. The reasoning has been stable – simpler development and revenue have been accessible, and valuations had been considerably stretched given what was accessible. That’s not the case with the businesses buying and selling down, and NWN is certainly one of them.

As issues stand although, I contemplate NWN to be an organization with a low valuation and a superb upside for the long term at this worth, and I will present you why right here.

Why Northwest Pure makes for an interesting funding right here.

To be clear, I view it as a possible funding in a basket of utility shares the place I’m already at full publicity to corporations like Enel and Fortum. If I wasn’t, I’d most likely purchase extra of these corporations. It’s because I at all times evaluate companies to 1 one other as investments.

Conservatively talking, I’d say that NWN has an upside of round 12.5-15% per yr, which is nice, however not nice (however wonderful given the protection of the corporate).

Now, what makes me say this, and provides these targets?

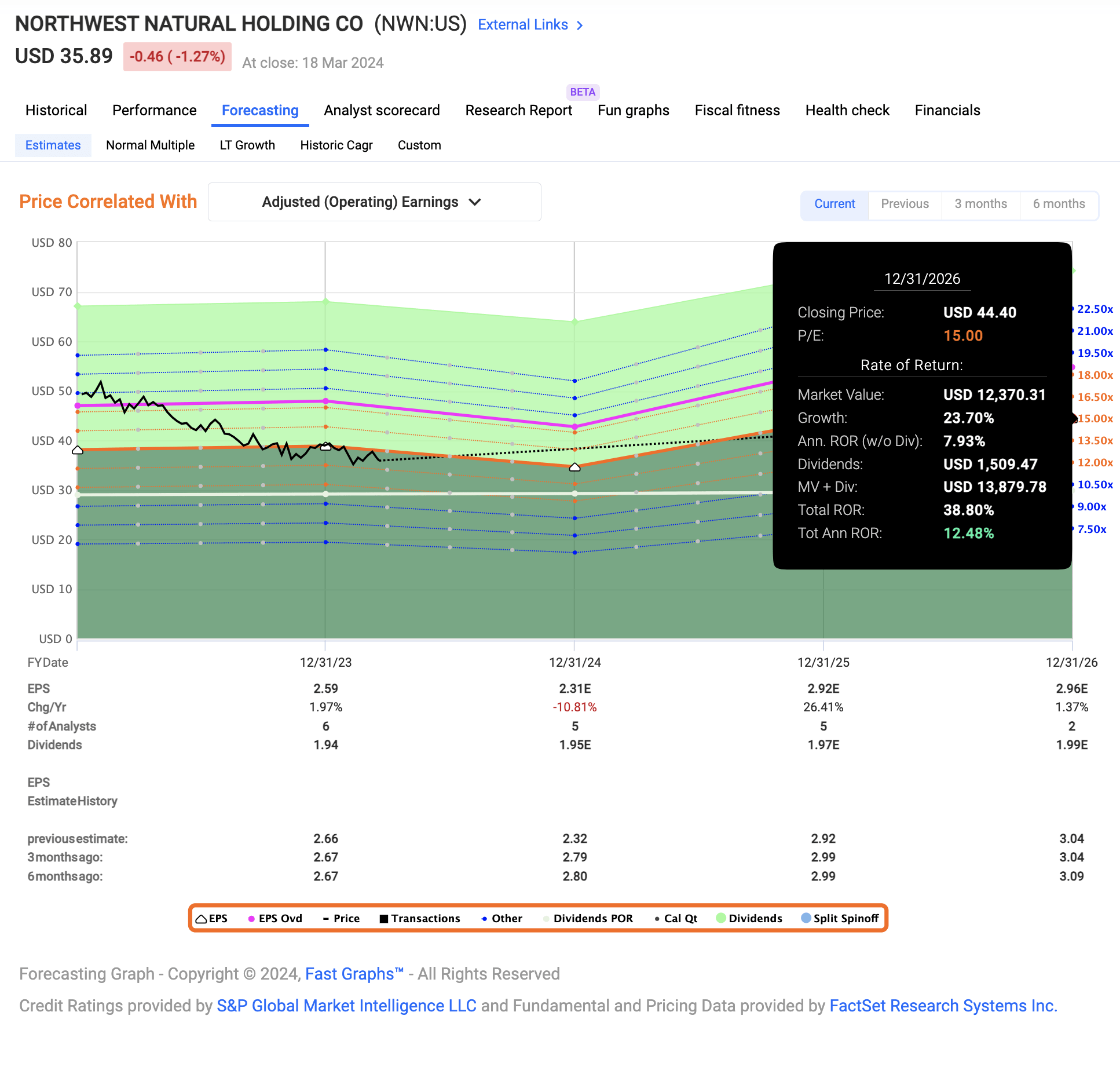

My estimates are at all times a mixture of my very own estimates, which in flip are based mostly on a mixture of sector-average development, firm forecasts and historic development patterns for the enterprise, together with my very own assumptions. Now, this firm has traditionally at all times, with a 20% MoE, hit its targets 100% of the time for the previous 10 years or so. Nonetheless, given the environmental and demographic elements of the world, I’d assume that the shopper development price goes to hover at or concerning the 1% stage, which does not lead me to imagine that this firm ought to commerce a lot above a 15x P/E baseline. That is under the corporate’s 5-year and longer-term averages, the place the corporate has managed to commerce at between 20x P/E, a big premium.

If these forecasts maintain, then it’s best to count on round 12.5% annualized RoR at a 15x P/E based mostly on how issues look now. It is a honest expectation and a conservative one. It could take very low multiples – under 10x, so that you can lose cash right here – so I view that as unlikely for the long term.

F.A.S.T graphs NWN Upside (F.A.S.T Graphs)

A extra bullish case for the corporate would come with estimating at about 16-17x – a superb midpoint right here is the 16.5x estimate, which involves an annualized price of return of 16.5% – above the market by an honest margin if you happen to take a look at normalized market returns.

I’d not estimate the corporate at any larger a number of than this. That is as a result of pretty damaging development estimates, which even the issue grades at In search of Alpha have rated a D-. Valuation and security is the important thing right here. The corporate’s dividend comes at a ahead payout ratio of lower than 75%, and whereas the corporate’s DGR on a 5-year foundation has been abysmal at 0.52% per yr, the corporate is closing on the twenty fifth yr of consecutive dividend development. Additionally, at that yield, I do not imagine you are able to do plenty of “wrong” issues right here.

I price the corporate a sexy funding in case your different utility investments that are “better” are full – which mine presently are. I say {that a} 16.5% annualized RoR is excellent, and one thing I’m keen to place cash into right here. I say the corporate is value no less than $44/share, or round a 15x ahead P/E contemplating 2026E development and valuation estimates. That is above analysts’ estimate. 5 analysts from S&P World (Supply: S&P World) have the corporate at a variety beginning at $36 on the low aspect to $61 on the excessive aspect, with a median of $42.6, making it an upside of round 18.7% at this explicit time with the corporate’s share worth at $36.37.

The primary danger to the thesis as this stands is the corporate’s sub-par development price and climate results. Nonetheless, at under $40/share, I imagine these dangers are even excessively discounted, and I’m prepared to take a position on this firm right here and make it a part of my “basket” of utility investments that generate above-risk-free price revenue for me.

Right here is my introductory thesis for the enterprise.

Thesis

- NWN is a regulated gasoline/water enterprise with an excellent valuation. The corporate affords A+ security, with a stable 5.4%+ yield. This firm affords a really stable upside of over 15% even at a conservative estimate, that means an estimate properly under the valuation of this firm’s 20-year common.

- I am a frequent investor in utility shares, in search of new shares so as to add to my utility portfolio – and this firm is one I’ve had my eye on for a while. I didn’t contemplate it interesting above $45/share, however I do contemplate the corporate engaging at under $40/share.

- I give the corporate a conservative long-term PT of $44/share and price the corporate a “BUY” for the primary time right here.

Keep in mind, I am all about:

- Shopping for undervalued – even when that undervaluation is slight and never mind-numbingly huge – corporations at a reduction, permitting them to normalize over time and harvesting capital features and dividends within the meantime.

- If the corporate goes properly past normalization and goes into overvaluation, I harvest features and rotate my place into different undervalued shares, repeating #1.

- If the corporate would not go into overvaluation however hovers inside a good worth, or goes again all the way down to undervaluation, I purchase extra as time permits.

- I reinvest proceeds from dividends, financial savings from work, or different money inflows as laid out in #1.

Listed below are my standards and the way the corporate fulfills them (italicized).

- This firm is general qualitative.

- This firm is basically protected/conservative & well-run.

- This firm pays a well-covered dividend.

- This firm is presently low cost.

- This firm has a practical upside that’s excessive sufficient, based mostly on earnings development or a number of growth/reversion.