Richard Drury

Transcript

We think central bank rate-cutting cycles will be far from typical.

1) High for longer

Central banks are set to keep rates above pre-pandemic levels due to persistent inflationary pressures. Mega forces are bolstering those pressures. They are structural shifts like geopolitical fragmentation, demographic divergence and the low-carbon transition that are driving returns now and in the future.

2) An atypical economic backdrop for easing

Falling inflation and weak economic activity have set the stage for the ECB to start cutting rates.

Yet, the economic backdrop is still atypical for rate cuts. Growth is improving, inflation remains above 2% and the unemployment rate is at a record low.

3) Central bank divergence

The ECB is set to ease policy before the Fed – and before it’s certain what’s next for U.S. monetary policy. U.S. inflation has proven sticky and volatile, so another rate hike is not impossible.

In the short term, the gap between Fed and ECB policy rates could widen and weigh on the euro against the U.S. dollar.

We still prefer U.S. stocks over Europe’s as they benefit more from the artificial intelligence theme. We’re neutral European government bonds but favor income from European credit.

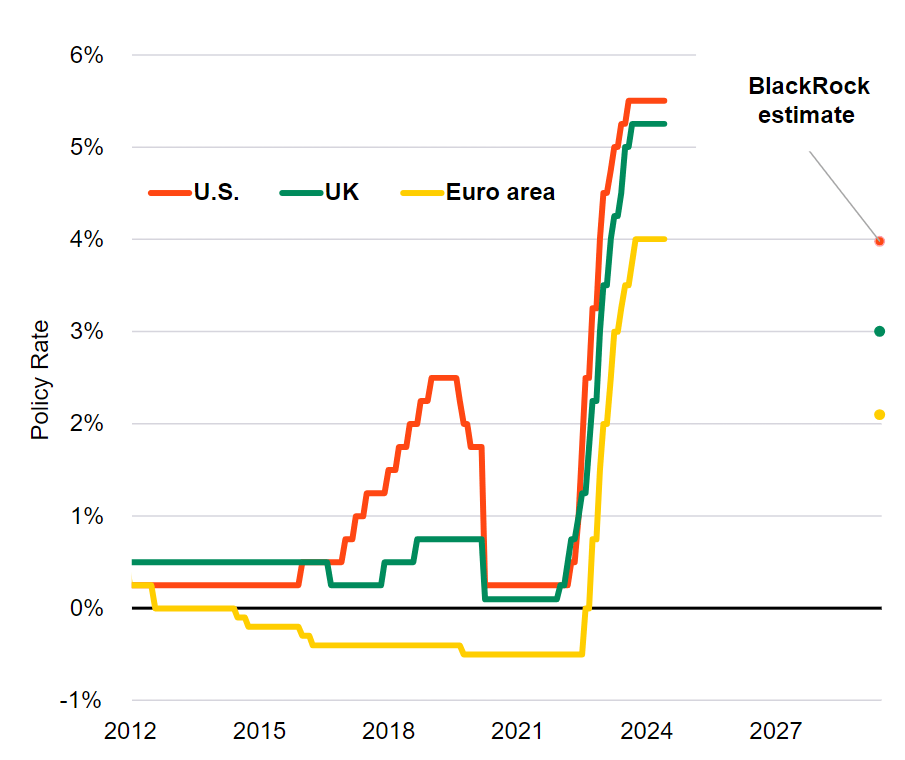

Coming down, slowly

Central bank policy rates, historic and our estimates, 2012-2029

Forward looking estimates may not come to pass. Source: BlackRock Investment Institute, with data from LSEG Datastream, May 2024. Notes: The chart shows the central bank policy rates until 2024 and our estimate of policy rates in five years. The dotsshown reflect our view of the neutral policy rate – that neither stokes nor dampens growth – and our assessment of the factors that will influence it. These estimates are subject to uncertainty and based on assumptions that may not come to pass

European government bond yields have swung as markets question how far the ECB will ease policy beyond a first cut expected this week. Falling inflation and 18 months of weak economic activity make the case for the ECB to start cutting rates. But we don’t think it will cut far and fast. Likewise, in the U.S., we see just one or two Fed cuts this year. This is not your typical rate cutting cycle. Central banks are set to keep rates above pre-pandemic levels (see the dots in the chart) due to persistent inflationary pressures – and last week’s euro area inflation data again showed stalling inflation progress. Unusually, the ECB is readying to cut when growth is improving, inflation is above its 2% target and the unemployment rate is at a record low. That’s a far cry from the economic crisis and low inflation in the past decade that spurred the ECB to introduce negative interest rates and buy bonds at scale.

In another unconventional step, the ECB is on the verge of easing policy before the Fed – and before it’s certain what’s next for monetary policy in the U.S., in our view. U.S. inflation is proving volatile and services inflation especially elevated, so another rate hike is not entirely off the table. This means that in the short term, the gap between Fed and ECB policy rates could widen and weigh on the euro against the U.S. dollar until the Fed starts cutting rates. Investors may see opportunities in further policy divergence, but we think it will be temporary, as both central banks ultimately keep rates high for longer.

Supply constraints in play

Even with anticipated rate cuts, we see policy rates in the U.S. and Europe settling at a far higher level than they were pre-pandemic. The reason: inflation. We don’t see euro area inflation falling below 2% as it did when central banks cut rates before 2020. That’s because we are in a world shaped by supply constraints – a reality ECB officials have acknowledged recently. Among those constraints are mega forces – structural shifts driving returns now and in the future – like geopolitical fragmentation, demographic divergence and the low-carbon transition. Those forces are also playing out in the U.S. As a result, we expect ongoing inflationary pressures and structurally lower growth than in the past across major economies.

The ECB trimming rates and recovering euro area growth should favor European stocks. Yet, we are underweight, preferring U.S. stocks on a tactical, six- to 12-month horizon as they are set to get a bigger boost from mega forces like AI. Within fixed income, our preference flips. We scoop up the higher total yields on offer in euro area credit. Improving growth in the euro area could also limit any spread widening relative to the U.S. We are neutral euro area government bonds and UK gilts as market pricing of near-term rate cuts aligns with our view. We see support for European bonds due to smaller fiscal deficits than in the U.S. Rules on limiting deficits now apply again after being suspended during the pandemic. We await the results of the European parliamentary election in June and UK general election in July – but expect a muted impact on bonds.

Our bottom line

An ECB cut is unlikely to be the start of a meaningful global easing cycle. We favor U.S. stocks over Europe’s on stronger corporate earnings and the AI theme. We’re neutral European government bonds but get income in European credit.

Market backdrop

U.S. stocks receded last week from record highs. Markets remain sensitive to Fed policy signals and the path of interest rates, helping lift the VIX index of implied S&P volatility from four-year lows. U.S. 10-year Treasury yields ticked up – partly due to weak Treasury auctions. German 10-year bund yields set fresh 2024 highs last week and sit near 2.64%. Ultimately, we see supply constraints creating persistent inflation pressure, keeping policy rates above pre-pandemic levels and growth below.

Markets will be parsing signals for future ECB rate cuts from its updated macro forecasts and President Lagarde’s press conference this week. We see the expected June 6 cut as the start of an atypical easing cycle as central banks keep interest rates high for longer. In the U.S., we rely on data – like this week’s employment report and service-sector PMI reading – rather than Fed signals to determine the policy path.